Accounts payable days outstanding at the end of Year 2 is closest to:

A. 57.0 days.

B. 66.0 days.

C. 72.0 days.

D. 43.2 days.

Which of the following would be considered the most discretionary of the following

cash outflows?

A. Interest payment

B. Payment to suppliers

C. Repurchase of stock

D. Administrative expense

Which of the following would be considered an extraordinary item?

I. Write-down of receivables

II. Gains on disposal of a business segment

III. Loss of inventory resulting from a fire

IV. Loss resulting from a strike

A. I and IV

B. I, III, and IV

C. III only

D. I, II, and III

Consolidation vs. Equity

Company ABC has a large, wholly owned consolidated finance subsidiary. For each of

the following ratios, state the effect (higher, lower, or no effect) that consolidation has

on the ratio of Company ABC compared to the ratio it would have if it accounted for its

finance subsidiary using the equity method. Briefly explain why each effect occurs.

a. Debt to equity ratio

b. Return on assets

c. Times interest earned

Treasury stock is:

A. investments in government securities.

B. retained earnings that have been appropriated to make equity investments.

C. a company’s own stock that it has repurchased.

D. assets held for safekeeping in company’s vaults.

Net account receivable at the end of March is closest to:

A. $7,503.51.

B. $7,886.17.

C. $8,218.93.

D. None of the above

Accounting standards are set by the American Institute of Certified Public Accountants

(AICPA).

How much would you be prepared to pay for a $500 bond which comes due in 5 years

and pays $80 interest annually assuming your required rate of return is 8% (pick closest

answer)?

A. $740

B. $660

C. $608

D. $500

If the beginning and ending property, plant, and equipment are $500 million and $550

million respectively, the gross book value of equipment sold was:

A. $120 million

B. $100 million

C. $80 million

D. $60 million

Two growing firms are identical except that one firm capitalizes, whereas the other firm

expenses costs for long-lived resources over time. For these two firms, which of the

following statements is generally true?

I. The expensing firm will show a more volatile pattern of reported income than

capitalizing firm.

II. The expensing firm will show a less volatile pattern of return on assets than the

capitalizing firm.

III. The expensing firm will show lower cash flows from operations than the

capitalizing firm.

A. I only

B. II only

C. I and III only

D. II and III only

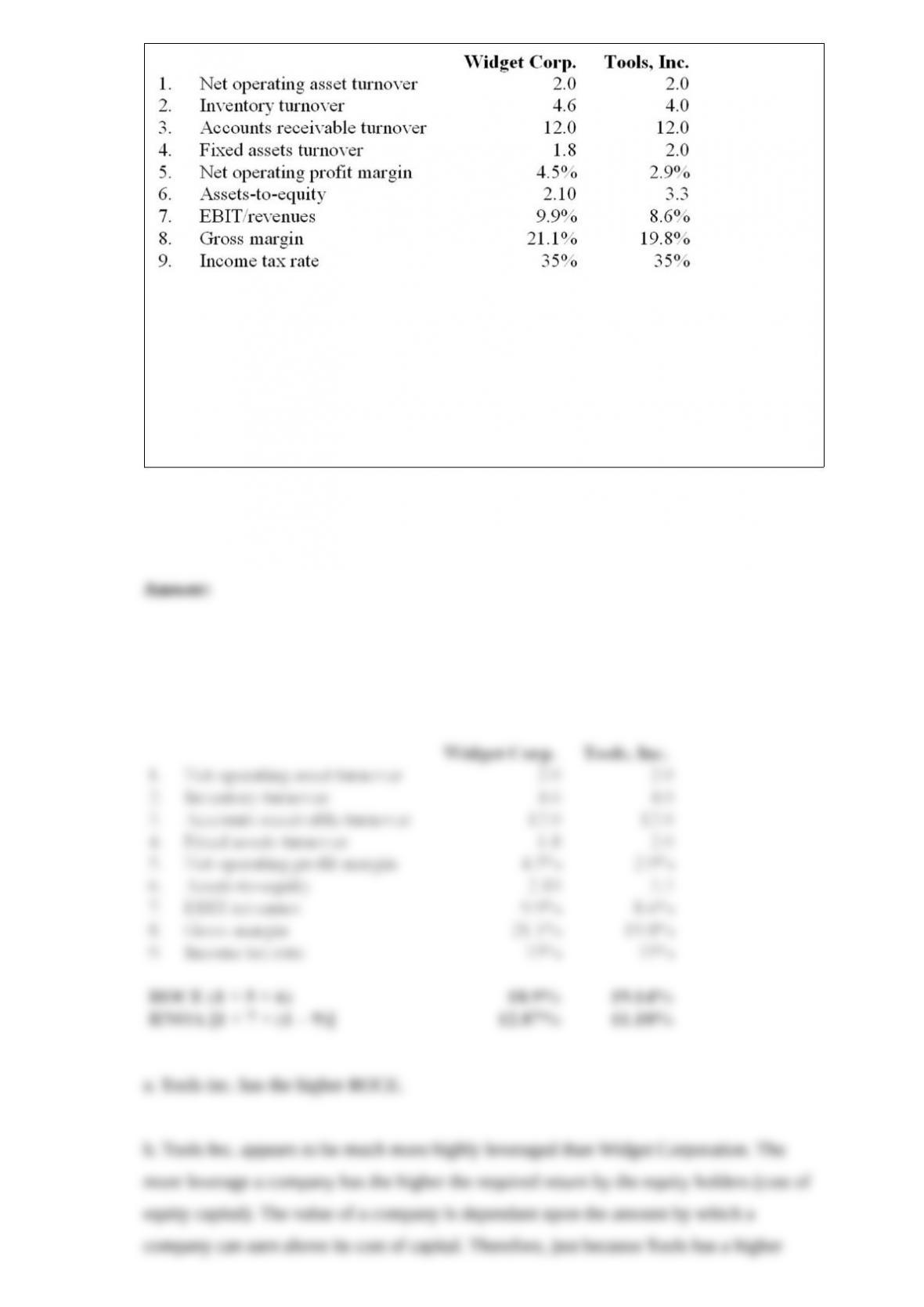

ROCE and Components

Below are selected ratios for Widget Corporation and Tools Inc. Use this information to

answer the following questions.

a. Which company has a higher return on equity?

b. We know from the residual income method of valuation that, all other things equal,

the company with the higher ROCE will have a higher intrinsic value. Why are all other

things not likely to be equal in this instance (hint: look at components of ROCE)?

c. Which company has better operating performance (that is, ignoring capital structure).

From the above information, you can infer that:

A. rate of sales growth has decreased.

B. net income to sales (return on sales) is increasing over time.

C. asset turnover is decreasing over time.

D. None of the above

When an acquisition is made and accounted for using the purchase method, the

post-acquisition retained earnings account:

A. is the sum of the pre-acquisition retained earnings accounts of the two combining

companies.

B. is the pre-acquisition retained earnings account of the acquiring company only.

C. is the pre-acquisition retained earnings accounts of the acquiring company plus net

income of acquired company in year of acquisition.

D. is the pre-acquisition retained earnings accounts of the acquiring company less

treasury stock of the acquired company.

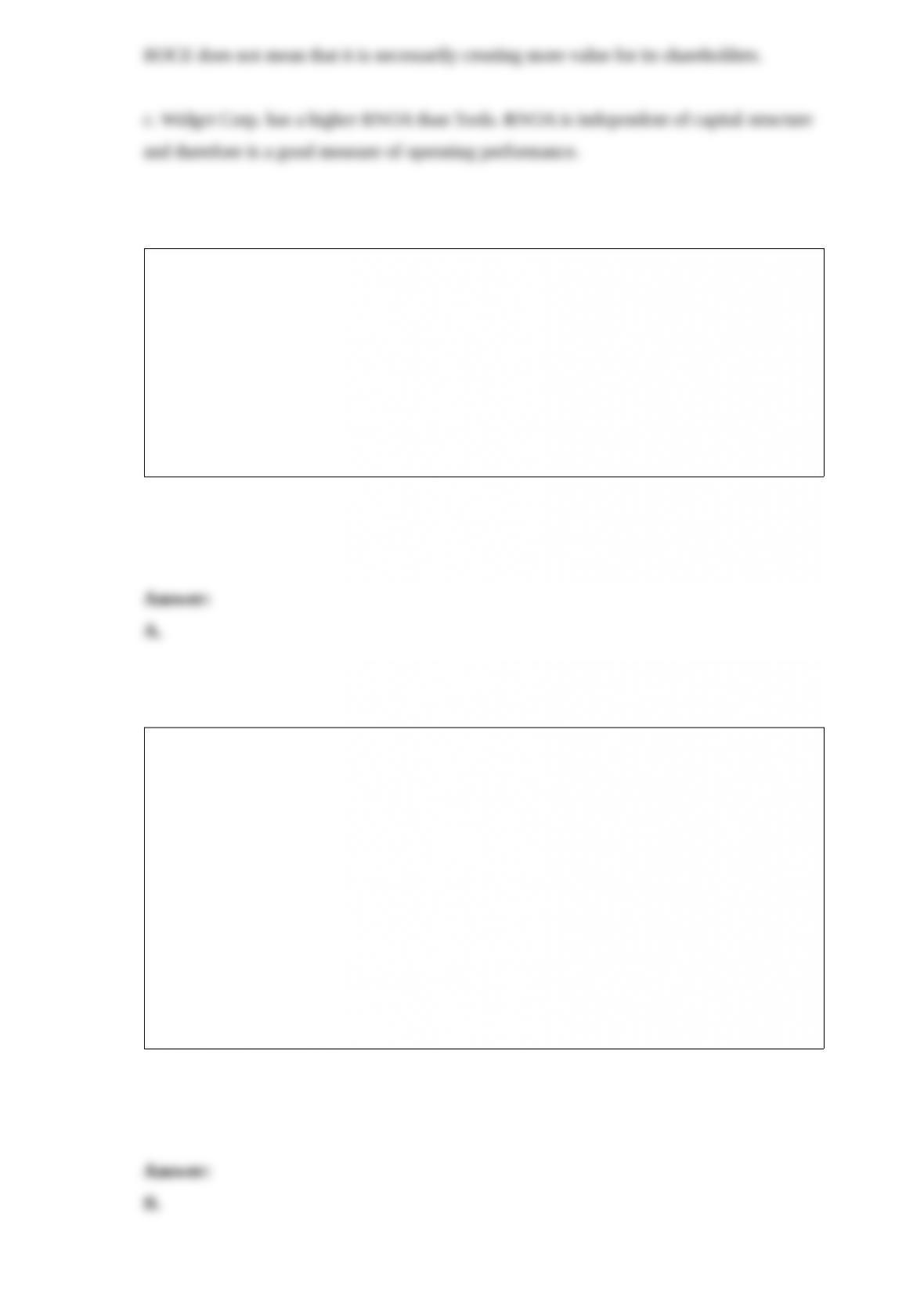

Alexas Corporation reports the following:

If price-to-book ratio at the end of 2005 equals 1.00, and return on beginning of year

equity is expected to remain constant, then cost of equity (to nearest percent) equals:

A. 15%.

B. 21%.

C. 24%.

D. Not determinable

Pro Formas

a. Developing pro forma financial statements and cash flow forecasts depends heavily

upon sales forecasts. Imagine you are a financial analyst working for a major

stockbroker, and you are trying to develop a one-year sales forecast for a major national

department store. List five pieces of information you want to obtain to aid you in your

forecast, explaining why this will aid you in your forecast.

b. Now you have made your best prediction of next year’s sales, you want to estimate

next year’s cost of goods sold. Pick two pieces of information you definitely want to

obtain in order to help you with this task, being sure to explain why they will be

helpful.

On a statement of cash flows that uses the indirect approach, calculation of cash flow

from operations treats depreciation as an adjustment to reported net income because:

A. depreciation is a direct source of cash.

B. depreciation is an outflow of cash to a reserve account for the replacement of assets.

C. depreciation reduces net income and involves an outflow of cash.

D. depreciation reduces net income but does not involve an outflow of cash.

Eyster Corporation reported $10 million in earnings and paid dividends of $3 million

for fiscal 2005. Return on equity and dividend payout are expected to remain constant

for the foreseeable future. Net book value at the end of fiscal 2004 was 100 million.

Cost of equity is 10%. Using the residual income method, the intrinsic value of Eyster’s

stock at the end of 2005 should be:

A. $110 million.

B. $107 million.

C. $101 million.

D. not determinable.

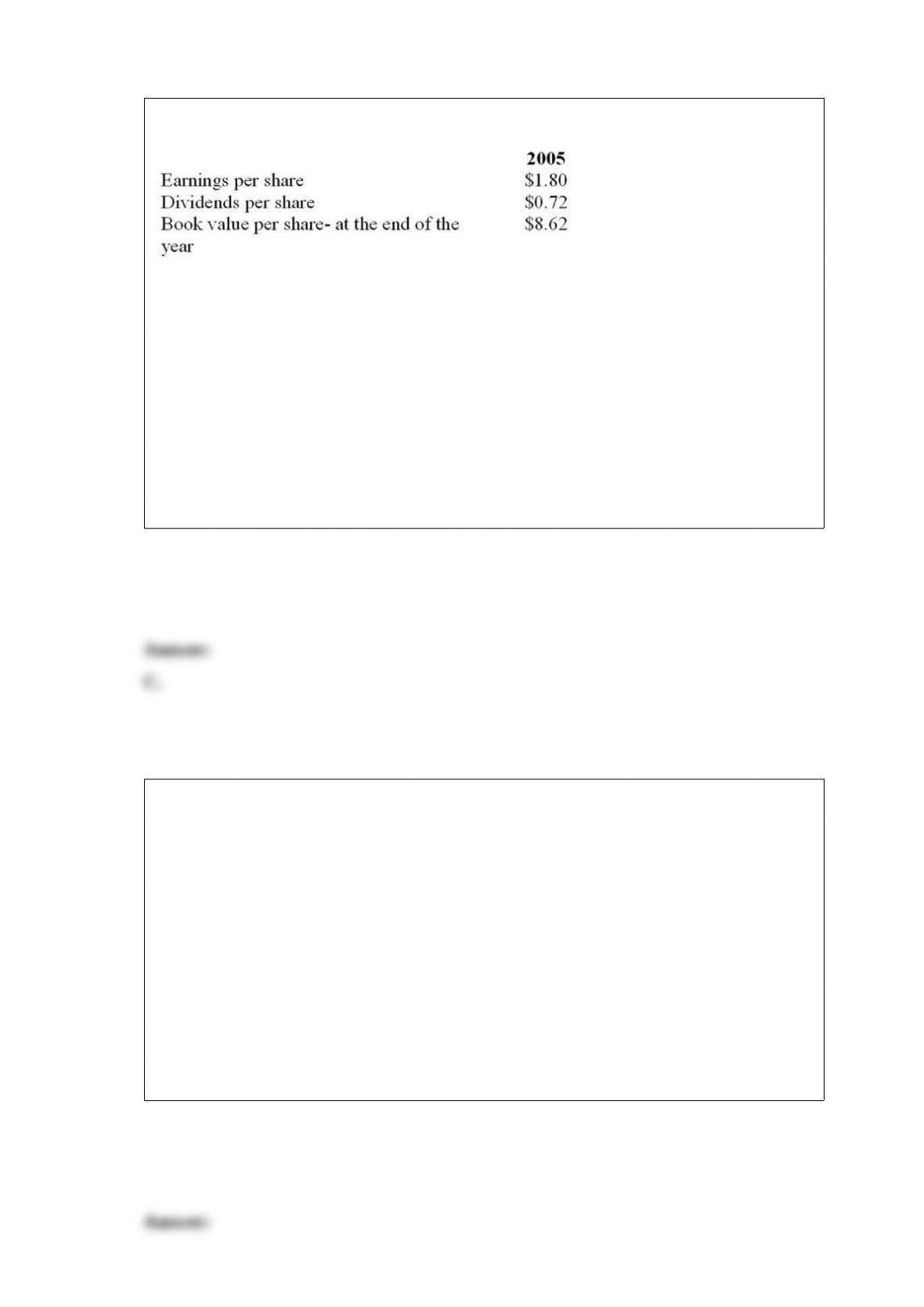

Hiruit company’s sales in December were $5,500. It expects sales to increase 10% in

January and February and 15% in March. All of its sales are made on credit. The typical

collection pattern is:

Gross margin is 30%. Inventory levels at the end of December are $900 and are

expected to grow at the same rate as sales. Purchases are paid for the month after they

are made. Net accounts receivable at the end of December are $400.

In March, Hiruit should collect:

A. $7,653.25 cash from sales made in March and previous months.

B. $7,342.50 cash from sales made in March and previous months.

C. $7,030.10 cash from sales made in March and previous months.

D. $6,331.30 cash from sales made in March and previous months.

Gupta Corporation has forecasted its need for external funding in the following year. It

needs to raise $2 million in either debt or equity. It would like to minimize its need for

external funding without decreasing its projected growth. Which of the following would

reduce its need for additional funding?

A. An increase in the dividend payout ratio

B. An increase in days’ sales outstanding

C. An increase in accounts payable

D. A decrease in inventory turnover

What is Dell’s profit margin for 2005?

A. 6.27%

B. 6.18%

C. 6.38%

D. 6.86%

What is Dell’s price-to-earnings ratio for 2006?

A. 27.63

B. 12.81

C. 23.65

D. 9.70

Foreign Currency Translation

Company ABC, an American company, has a 100% owned foreign subsidiary. The

foreign subsidiary’s local currency, functional currency and reporting currency are all

different. The subsidiary accounts for inventories using the first-in, first-out (FIFO)

method.

A. Assume the functional currency is appreciating relative to the reporting currency.

Compare each of the following ratios for the foreign subsidiary in the reporting

currency after translation to the same ratios in the functional currency before

translation. Explain why the ratios do or do not differ.

i. Gross profit margin percentage

ii. Current ratio

B. Assume the local currency is appreciating relative to the functional currency.

Compare each of the following ratios for the foreign subsidiary in the functional

currency after remeasurement to the same ratios in the local currency before

remeasurement. Explain why the ratios do or do not differ.

i. Gross profit margin percentage

ii. Operating profit margin

iii. Net profit margin

What were the cash proceeds from the sale?

A. $38,000

B. $18,000

C. $10,000

D. $8,000

Which of the following statistics would be the most useful in determining the efficiency

of a car rental company?

A. Inventory turnover

B. Number of employees per car rental

C. Average length of car rental

D. Number of days cars are rented as a percentage of number of days available for rent

What will be the retained earnings for 2005 if ABC used FIFO valuation?

A. $3,205,271

B. $3,566,918

C. $3,893,000

D. $4,096,430

What is your estimate of price per share using the dividend discount model at 12/31/05?

A. $20.62

B. $21.65

C. $23.56

D. $24.74

On January 1, a company entered into a capital lease resulting in an obligation of

$20,000 being recorded on the balance sheet. Estimated economic life of the leased

asset is ten years with an expected salvage value of zero at the end of ten years. The

company will depreciate this asset on a straight-line basis over its economic life. The

lessor’s implicit interest was 10 percent. At the end of the first year of the lease, the cash

flow from financing activities section of the lessee’s statement of cash flows showed a

use of cash of $2,200 applicable to the lease. How much did the company pay the lessor

in the first year of the lease?

A. $2,000

B. $2,200

C. $4,200

D. $20,000

Postretirement Health Benefits

Warden Corp. has a postretirement health benefit plan for its employees. As of

December 31, 2006, the accumulated postretirement benefit obligation (APBO) is $250

million and the postretirement health benefit cost for the year was $23 million. The plan

assets are $10 million. Warden chose to recognize its unfunded liability immediately.

Warden also has a pension plan, which is fully funded.

a. What reasons are there for the minimal funding of the postretirement health benefits

plans versus the full funding of the pension plan?

b. In 2006 Warden makes the following changes.

– Increases its expected rate of return on plan assets.

– Increases the expected compensation growth rate.

– Increases its discount rate.

Explain the effect of each of these on

i. economic cost as of the end of 2007.

ii. reported cost for 2007.

Which of the following is not considered a monitoring mechanism?

A. The Securities and Exchange Commission (SEC)

B. Top level management

C. The board of director’s audit committee

D. The external auditors

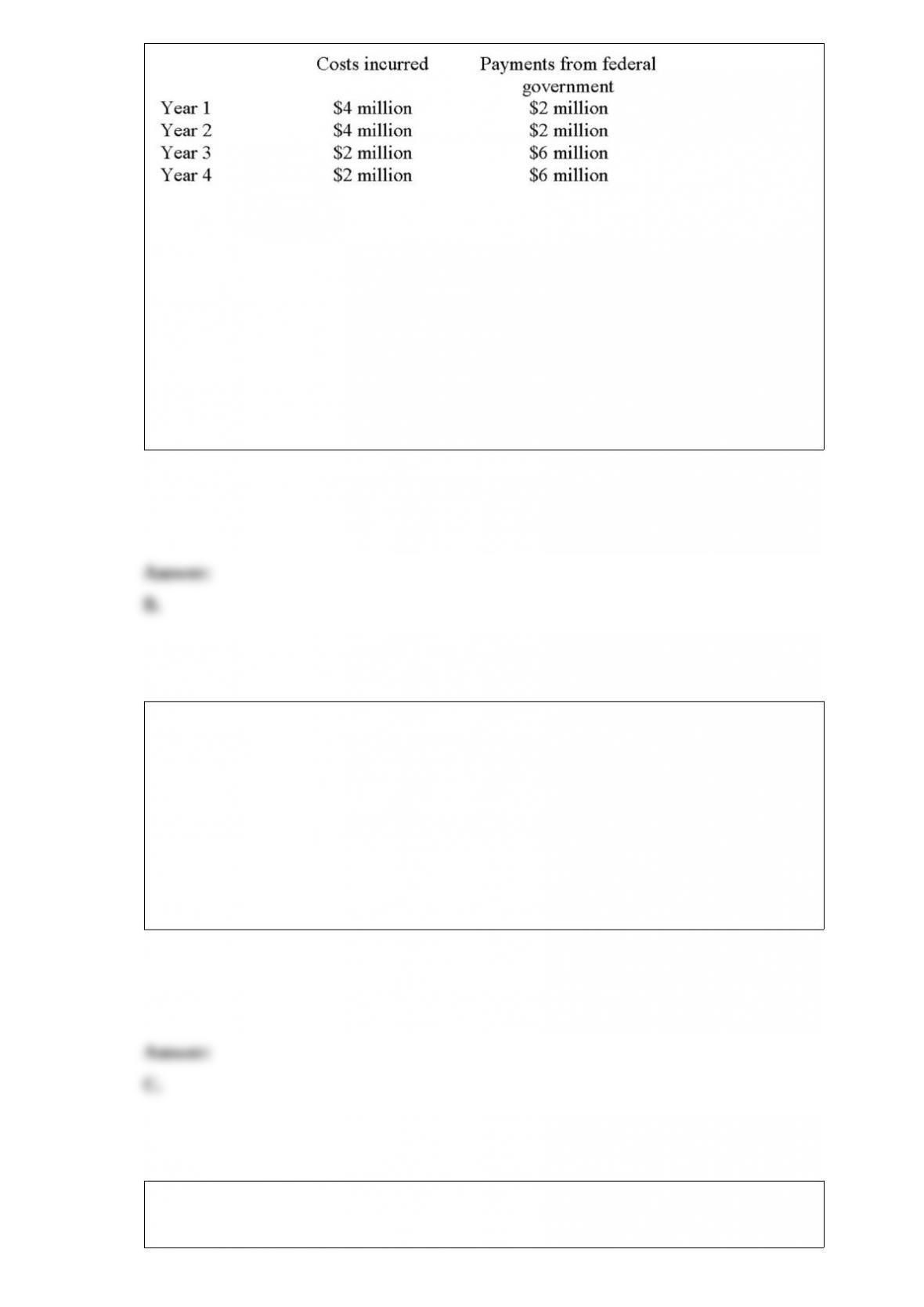

Brierton Company enters a contract at the beginning of year 1 to build a new federal

courthouse for a price of $16 million. Brierton estimates that total cost of the project

will be $12 million and will take four years to complete.

If Brierton used percentage-of-completion method to account for this project, what

would they have reported as profit in year 2?

A. $0

B. $1.33 million

C. $1.50 million

D. $0.67 million

Which of the following best describes the current ratio?

A. Debt ratio

B. Operating performance ratio

C. Liquidity ratio

D. Efficiency ratio

When calculating Acme’s return on net operating assets in Year 1, which of the

following adjustments to the asset base is most appropriate to consider?

A. Accumulated depreciation adjustment

B. Intangible asset adjustment

C. Non-operating asset adjustment

D. No asset adjustment

Which of the following is not a component of recognized OPEB cost?

A. Service cost

B. Amortization of prior service costs

C. Interest cost

D. Amortization of prior interest costs