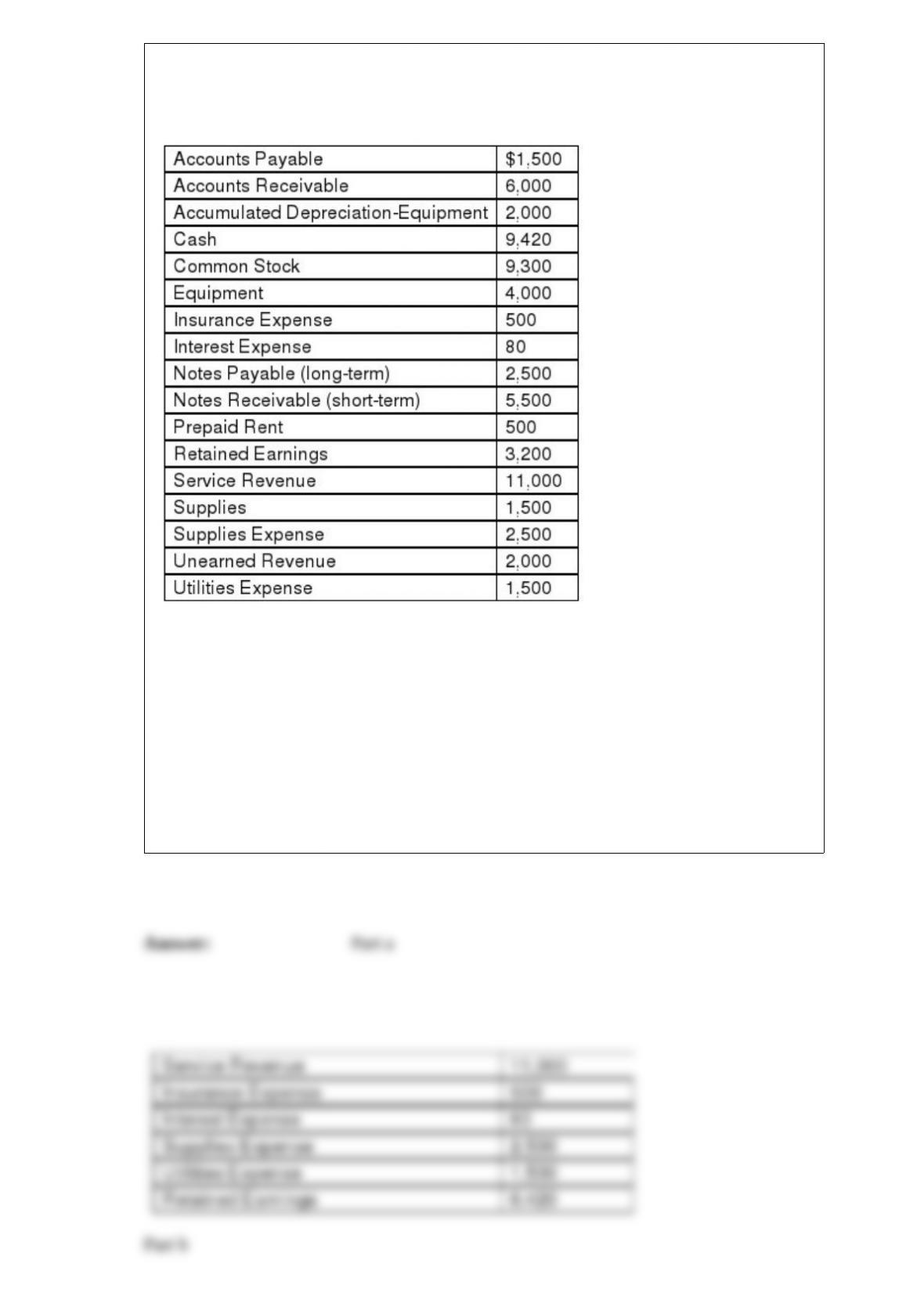

The following information was summarized from the adjusted trial balance of Reliance

Yacht Repair, Inc. as of September 30, 2015, the end of the company’s fiscal year.

Required:

Part a. Prepare the closing entry for the company for the year ended September 30,

2015.

Part b. Draw a T-account for the Retained Earnings account. Enter the beginning

balance into the T-account, post the closing entry, and then determine the ending

balance.

Part c. Prepare a post-closing trial balance at September 30, 2015.

A company started the year with a normal balance of $68,000 in the Inventory account.

During the year, debits totaling $45,000 and credits totaling $55,000 were posted to the

Inventory account. Which of the following statements about the Inventory account is

correct?

A) The normal balance of the Inventory account is a credit balance.

B) After these amounts are posted, the balance in the Inventory account is a credit

balance of $58,000.

C) The Inventory account is decreased by debits.

D) The debits and credits posted to the Inventory account caused it to decrease by

$10,000.

Choose the appropriate letter to match the term and the definition. There are more

definitions than terms.

Term

1) ____ FOB Destination

2) ____ FOB Shipping Point

3) ____ Merchandising Company

4) ____ Periodic Inventory System

5) ____ Perpetual Inventory System

6) ____ Service Company

Definition

A. Sells services rather than physical goods.

B. Assets acquired for resale to customers.

C. Inventory records are updated every time inventory is bought, sold, or returned.

D. A term of sale indicating that goods are owned by the seller until they are delivered

to the buyer.

E. Sells goods that have been obtained from a supplier.

F. The sum of beginning inventory and purchases for the period.

G. Inventory records are updated at the end of the accounting period. To determine how

much merchandise has been sold, periodic systems require that inventory be physically

counted at the end of the period.

H. A term of sale indicating that goods are owned by the buyer the moment they leave

the seller’s premises.

I. A sales price reduction given to customers for prompt payment of their account

balance.

J. Presents important subtotals, such as gross profit, to help distinguish core operating

results from other, less significant items that affect net income.

Assume that the custodian of a $450 petty cash fund has $62.50 in currency and coins

plus $387.50 in receipts at the end of the month. The entry to replenish the petty cash

fund will include a:

A) debit to Cash for $387.50.

B) debit to Petty Cash for $387.50.

C) credit to Petty Cash for $387.50.

D) credit to Cash for $387.50.

Revenues:

A) decrease assets.

B) increase stockholders’ equity.

C) increase liabilities.

D) decrease expenses.

Which of the following would be in the finished goods inventory of a company making

cheese?

A) Milk and cream used to make the cheese

B) Cheese that has been made but is curing before being ready to sell

C) Cured cheese that is waiting to be shipped to customers

D) Cured cheese that has been sold to customers

Which of the following statements about adjustments is not correct?

A) When making an adjustment to recognize supplies used in a period, total assets will

not change.

B) Accrued wages are wages owed, but not yet paid, to employees; the accrued wages

will need to be recorded with an adjusting entry that increases expenses.

C) Deferral adjustments are used to update amounts that have been previously deferred

on the balance sheet.

D) Depreciation is an example of a deferral adjustment.

A company sells three different products. Model A costs $8 and sells for $16, Model B

costs $18 and sells for $45, and Model C costs $36 and sells for $120.

Required:

Part a. Calculate the gross profit per unit for each of the three products.

Part b. Calculate the gross profit percentage for each of the three products.

Company X paid Company Y $1.35 million for a new plant. During the same

accounting period, Company X experienced the following changes in its balance sheet:

Cash decreased by $350,000, Accounts Receivable increased by $321,300, Inventory

increased by $275,800, Property, Plant, and Equipment increased by $752,900, and

Bonds Payable increased by $1 million. The net cash flow provided by financing

activities is:

A) An inflow of $1.35 million.

B) An outflow of $350,000.

C) An inflow of $1 million.

D) An inflow of $752,900.

Which of the following statements about net profit margin is not correct?

A) If a company’s net profit margin increases from 15% to 20% this would be

considered an improvement in profitability.

B) A company with a net profit margin of 10% is using 90% of each dollar of revenue

to cover costs and expenses.

C) Net profit margin indicates how much net income is earned for every dollar of

revenue.

D) A company with a net profit margin of 10% may be evaluated differently depending

upon which industry it is in.

A company incurred $2,000 for utilities for the last month of Year 2. The company paid

the bill during the first month of Year 2. Which of the following statements is correct?

A) The related $2,000 should be reported on the income statement for Year 1 as Utilities

Expense.

B) Since it has not been paid, this utility bill would not be reported in the financial

statements for Year 1.

C) The related $2,000 should be included in Accounts Receivable on the balance sheet

at the Year 1.

D) The related $2,000 should be included in Utilities Expense on the balance sheet at

the end Year 1.

The attitude that people in the organization hold regarding internal control is referred to

as the:

A) control environment.

B) control atmosphere.

C) risk assessment.

D) monitoring activities.

Which of the following statements about revenue and expense accounts is correct?

A) Revenue accounts are a subset of assets, and expense accounts are subcategories of

liabilities.

B) Both revenue accounts and expense accounts are subcategories of assets.

C) Both revenue accounts and expense accounts are subcategories of Retained

Earnings.

D) Revenue accounts are a subcategory of Cash and expense accounts are a subcategory

of Accounts Payable.

An adjustment to accrue the amount of salaries and wages owed was recorded on

December 31. These salaries and wages were paid on the following January 5. The

entry on January 5 would include a debit to:

A) Salaries and Wages Expense and Credit to Cash.

B) Salaries and Wages Payable and Credit to Cash.

C) Cash and Credit to Salaries and Wages Payable.

D) Cash and Credit to Salaries and Wages Expense.

Which of the following would a company be most likely to overstate if the company

was trying to mislead potential creditors as to its ability to pay debts as they become

due?

A) Accounts Receivable

B) Notes Payable

C) Salaries Expense

D) Accounts Payable

Which of the following is not a term for the value at which an asset is reported on a

financial statement?

A) Carrying value

B) Book value

C) Equipment, net

D) Accrual value

Interest Receivable:

A) is an asset reported on the balance sheet.

B) is a temporary account reported on the income statement.

C) is a permanent account reported on the income statement.

D) represents the amount of interest the company has received on promissory notes.

Use the information above to answer the following question. What journal entry will be

recorded by Flynn Company on November 15?

A) Debit Accounts Payable and credit Cash for $4,900

B) Debit Accounts Payable for $5,000, credit Purchase Discount for $100, and credit

Cash for $4,900

C) Debit Accounts Payable for $5,000, credit Inventory for $100, and credit Cash for

$4,900

D) Debit Accounts Payable for $4,900, credit Inventory for $100, and credit Cash for

$4,800

On the declaration date, the company:

A) debits Dividends and credits Dividends Payable for the amount of the dividend.

B) debits Dividend Expense and credits Cash for the dividend amount.

C) debits Dividends Payable and credits Cash for the dividend amount.

D) establishes who will receive the dividend payment.

Contingent liabilities must be recorded if the:

A) future event is reasonably possible.

B) amount owed cannot be reasonably estimated.

C) future event is probable and the amount owed can be reasonably estimated.

D) future event is remote.