Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

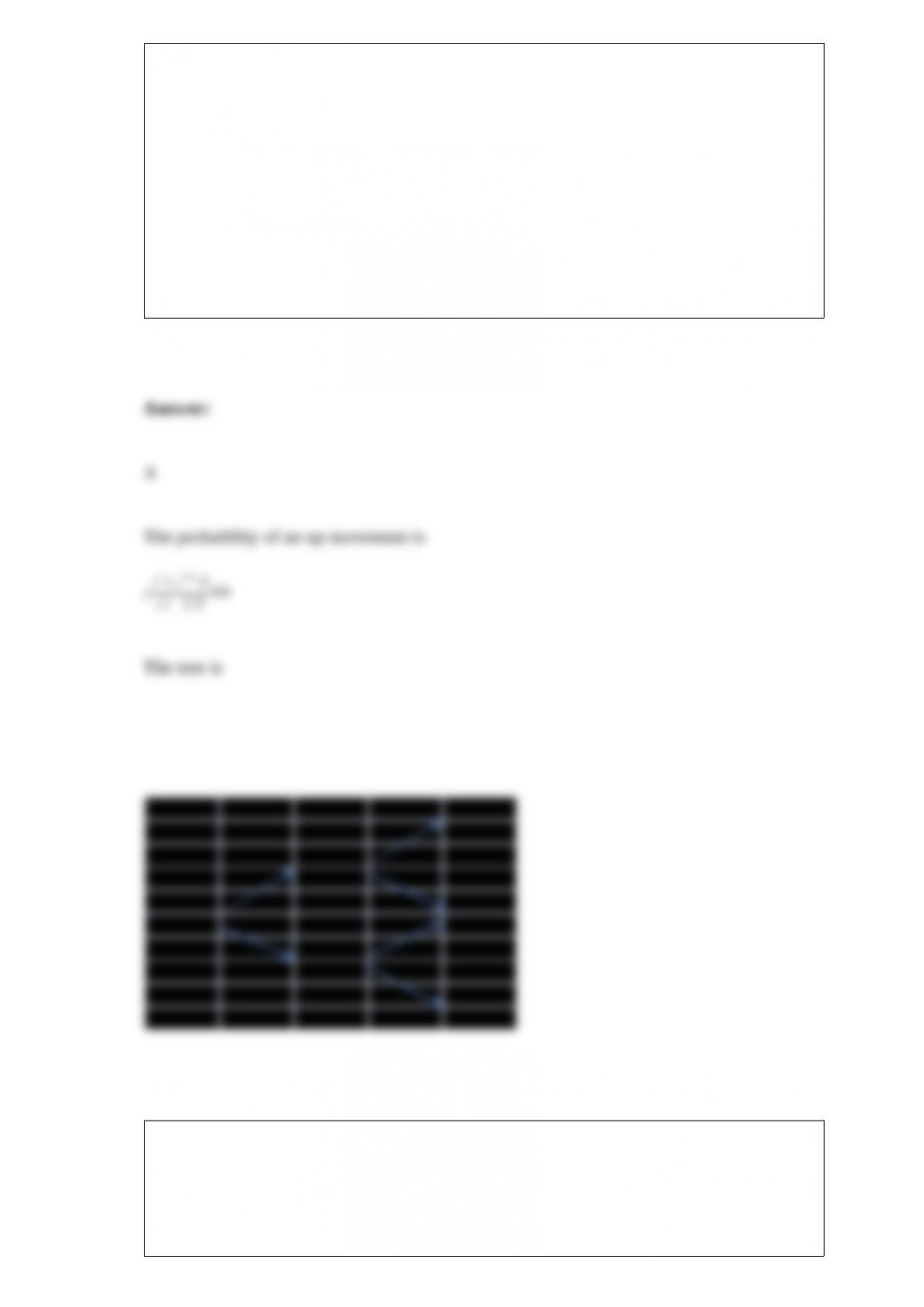

The current price of a non-dividend paying stock is $30. Use a two-step tree to value a

European put option on the stock with a strike price of $32 that expires in 6 months

with u = 1.1 and d = 0.9. Each step is 3 months, the risk free rate is 8%.

A. $2.24

B. $2.44

C. $2.64

D. $2.84

A stock price (which pays no dividends) is $50 and the strike price of a two year

European put option is $54. The risk-free rate is 3% (continuously compounded).

Which of the following is a lower bound for the option such that there are arbitrage

opportunities if the price is below the lower bound and no arbitrage opportunities if it is

above the lower bound?

A. $4.00

B. $3.86

C. $2.86

D. $0.86

A fixed lookback put option pays off which of the following

A. The amount by which the final stock price exceeds the minimum stock price

B. The amount by which the maximum stock price exceeds the final stock price

C. The amount by which the strike price exceeds the minimum stock price

D. The amount by which the maximum stock price exceeds the strike price

Which of the following is true of a covariance matrix?

A. The numbers on the diagonal are variances

B. The numbers on the diagonal are standard deviations

C. The numbers on the diagonal are all one.

D. The numbers on the diagonal are all zero

Which of the following is a definition of the covariance between X and Y?

A. Correlation between X and Y times variance of X times variance of Y

B. Variance of X times the variance of Y

C. Correlation between X and Y divided by the product of the standard deviation of X

and the standard deviation of Y

D. Correlation between X and Y times standard deviation of X times standard deviation

of Y

A stock is expected to return 10% when the risk-free rate is 4%. What is the correct

discount rate to use for the expected payoff on an option in the real world?

A. 4%

B. 10%

C. More than 10%

D. It could be more or less than 10%

Suppose that OIS rates of all maturities are 6% per annum, continuously compounded.

The one-year LIBOR rate is 6.4%, annually compounded and the two-year swap rate

for a swap where payments are exchanged annually is 6.8%, annually compounded.

Which of the following is closest to the LIBOR forward rate for the second year when

LIBOR discounting is used and the rate is expressed with annual compounding

A. 7.199%

B. 7.221%

C. 7.229%

D. 7.225%

Which of the following is usually used to define the recovery rate of a bond?

A. The value of the bond immediately after default as a percent of its face value

B. The value of the bond immediately after default as a percent of the sum of the bond's

face value and accrued interest

C. The amount finally realized by a bondholder as a percent of face value

D. The amount finally realized by a bondholder as a percent of the sum of the bond's

face value and accrued interest

Which of the following is measured by the VIX index

A. Implied volatilities for stock options trading on the CBOE

B. Historical volatilities for stock options trading on CBOE

C. Implied volatilities for options trading on the S&P 500 index

D. Historical volatilities for options trading on the S&P 500 index

In which of the following cases is an asset NOT considered constructively sold?

A. The owner shorts the asset

B. The owner buys an in-the-money put option on the asset

C. The owner shorts a forward contract on the asset

D. The owner shorts a futures contract on the stock

Which of the following is NOT a property of a Wiener process?

A. The change during a short period of time dt has a variance dt

B. The changes in two different short periods of time are independent

C. The mean change in any time period is zero

D. The standard deviation over two consecutive time periods is the sum of the standard

deviations over each of the periods

If the volatility of a non-dividend paying stock is 20% per annum and a risk-free rate is

5% per annum, which of the following is closest to the Cox, Ross, Rubinstein parameter

u for a tree with a three-month time step?

A. 1.05

B. 1.07

C. 1.09

D. 1.11

A binary option pays off $100 if a non-dividend-paying stock price is greater than its

current value in three months. The risk-free rate is 3% and the volatility is 40%. Which

of the following is its value?

A. 99.25N(-0.1375)

B. 99.25N(0.1375)

C. 99.25N(-0.0625)

D. 99.25N(0.0625)

A portfolio manager in charge of a portfolio worth $10 million is concerned that the

market might decline rapidly during the next six months and would like to use put

options on an index to provide protection against the portfolio falling below $9.5

million. The index is currently standing at 500 and each contract is on 100 times the

index. What position is required if the portfolio has a beta of 0.5?

A. Short 200 contracts

B. Long 200 contracts

C. Short 100 contracts

D. Long 100 contracts

AIG lost money because

A. It bought tranches created from mortgages

B. It invested heavily in real estate

C. It invested heavily in the stock market

D. It insured AAA tranches of ABS CDOs

Which of the following describes a subprime mortgage?

A. The rate of interest is less than the prime rate of interest

B. The loan-to-value ratio is below average

C. The life of the mortgage is less than 25 years

D. The credit risk is high