Which of the following funds are usually most tax-efficient?

A. equity funds

B. bond Funds

C. ETFs

D. specialized-sector funds

The term investment horizon refers to __________.

A. the proportion of short-term to long-term investments held in an investor’s portfolio

B. the planned liquidation date of an investment

C. the average maturity date of investments held in a portfolio

D. the maturity date of the longest investment in the portfolio

The divergence between an option’s intrinsic value and its market value is usually

greatest when ___________________.

A. the option is deep in the money

B. the option is approximately at the money

C. the option is far out of the money

D. time to expiration is very low

A bond has a maturity of 12 years and a duration of 9.5 years at a promised yield rate of

8%. What is the bond’s modified duration?

A. 12 years

B. 11.1 years

C. 9.5 years

D. 8.8 years

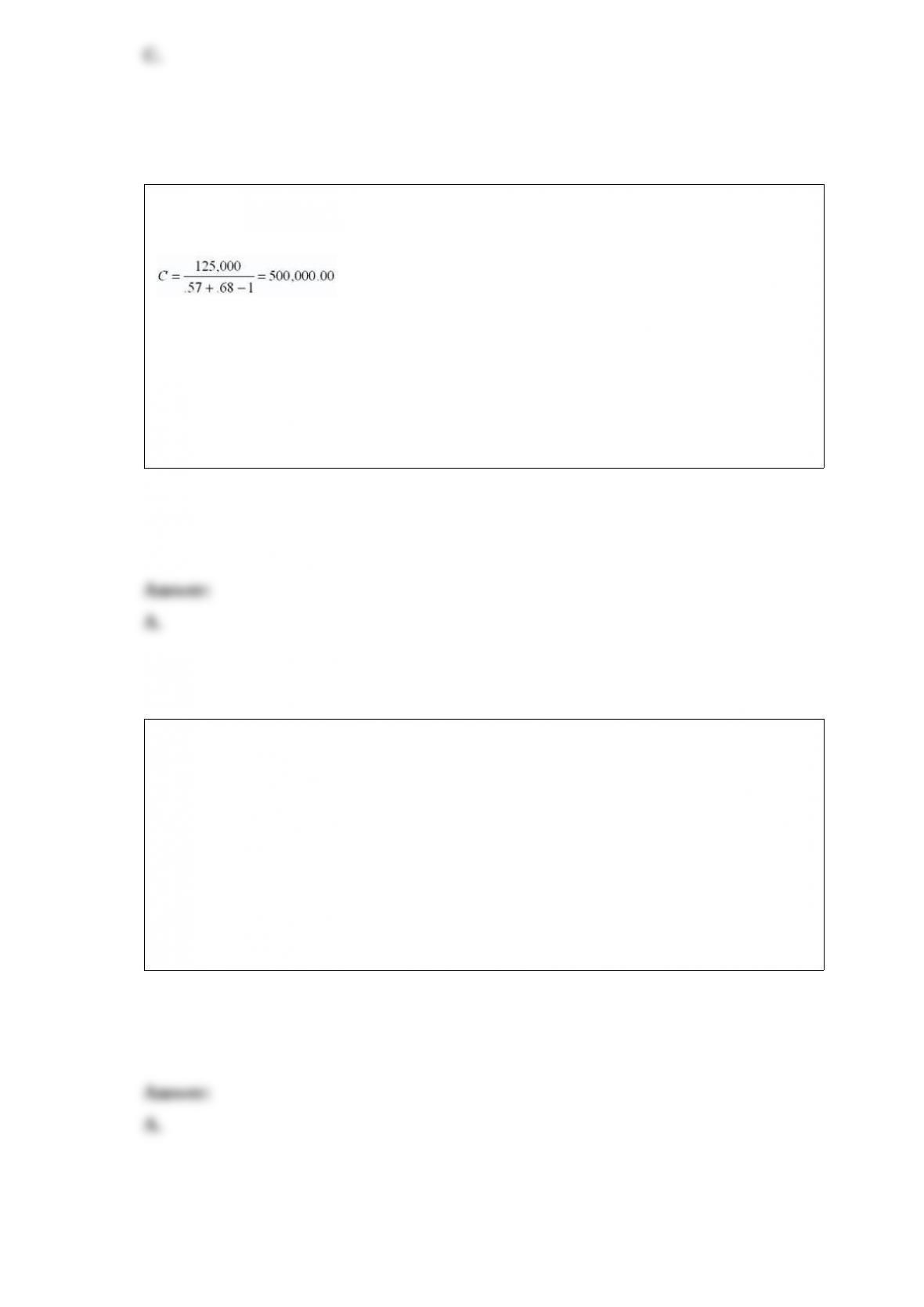

Douglass, an imperfect forecaster, correctly predicts 57% of all bull markets and 68%

of all bear markets. Simmonds is a perfect forecaster. If Douglass is able to charge a fee

of $125,000, the fee that Roy Simmonds should charge is __________. Assume that

both forecasters manage similar-size funds.

A. $31,250

B. $200,000

C. $500,000

D. $625,000

A wheat farmer should __________ in order to reduce his exposure to risk associated

with fluctuations in wheat prices.

A. sell wheat futures

B. buy wheat futures

C. buy a contract for delivery of wheat now and sell a contract for delivery of wheat at

harvest time

D. sell wheat futures if the basis is currently positive and buy wheat futures if the basis

is currently negative

The accounting measure of a firm’s equity value generated by applying accounting

principles to asset and liability acquisitions is called ________.

A. book value

B. market value

C. liquidation value

D. Tobin’s q

An investor is looking at different retirement investment choices, and he is willing to

accept one with upside potential even if that means sacrificing certainty. Which of the

following will he most likely select?

A. fixed annuity

B. defined benefit plan

C. defined contribution plan

D. bonds invested in a retirement plan

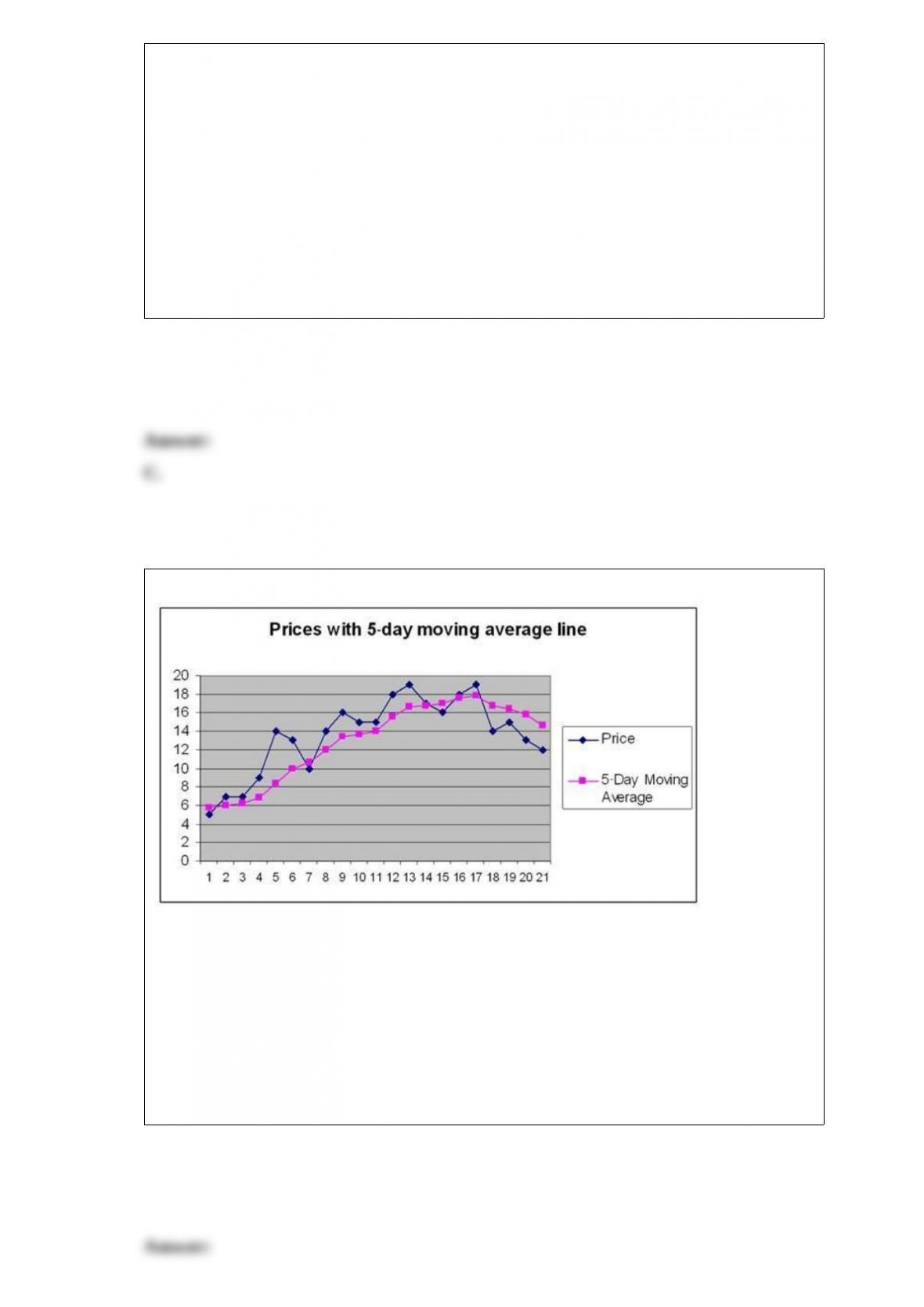

The

moving average generates sell signals _____.

A. on days 3, 11, and 15

B. on days 7, 15, and 18

C. on days 5, 9, and 13

D. on day 16

Active portfolio managers try to construct a risky portfolio with _______.

A. a higher Sharpe ratio than a passive strategy

B. a lower Sharpe ratio than a passive strategy

C. the same Sharpe ratio as a passive strategy

D. very few securities

All else equal, call option values are _____ if the _____ is lower.

A. higher; stock price

B. higher; exercise price

C. lower; dividend payout

D. lower; stock volatility

The excess return is the _________.

A. rate of return that can be earned with certainty

B. rate of return in excess of the Treasury-bill rate

C. rate of return to risk aversion

D. index return

The primary measurement unit used for assessing the value of one’s stake in an

investment company is ___________________.

A. net asset value

B. average asset value

C. gross asset value

D. total asset value

The four largest economies in the world in 2010 were ____________.

A. United States, India, China, and Japan

B. United States, China, Canada, and Japan

C. United States, China, Japan, and Germany

D. China, United Kingdom, Canada, and United States

As of 2014, hedge funds had approximately _____ under management.

A. $.5 trillion

B. $1.6 trillion

c. $2.4 trillion

D. $3.2 trillion

The EBIT of a firm is $300, the tax rate is 35%, the depreciation is $20, capital

expenditures are $60, and the increase in net working capital is $30. What is the free

cash flow to the firm?

A. $85

B. $125

C. $185

D. $305

Bond prices are _______ sensitive to changes in yield when the bond is selling at a

_______ initial yield to maturity.

A. more; lower

B. more; higher

C. less; lower

D. equally; higher or lower

Management fees for hedge funds typically range between _____ and _____.

A. .5%; 1.5%

B. 1%; 2%

C. 2%; 5%

D. 5%; 8%

You own a stock portfolio worth $50,000. You are worried that stock prices may take a

dip before you are ready to sell, so you are considering purchasing either at-the-money

or out-of-the- money puts. If you decide to purchase the out-of-the-money puts, your

maximum loss is __________ than if you buy at-the-money puts and your maximum

gain is

__________.

A. greater; lower

B. greater; greater

C. lower; greater

D. lower; lower

Which of the following are true statements about T-bills?

I. T-bills typically sell in denominations of $10,000.

II. Income earned on T-bills is exempt from all federal taxes.

III. Income earned on T-bills is exempt from state and local taxes.

A. I only

B. I and II only

C. I and III only

D. I, II, and III

A market neutral hedge fund is likely to have ______________.

A. various derivative strategies designed to create stability

B. a low beta compared to other equity only investments

C. a beta well above 1.0 compared to other equity investments

D. a beta near 1.0

The SIPC was established by the ____.

A. Insider Trading Act of 1931

B. Securities Act of 1933

C. Securities Exchange Act of 1934

D. none of these options

Calculate the price of a call option using the Black Scholes model and the following

data: stock price = $47.30, exercise price = $50, time to expiration = 85 days, risk-free

rate = 3%, standard deviation = 35%.

A. $1.11

B. $2.22

C. $3.33

D. $4.44

A stock priced at $65 has a standard deviation of 30%. Three-month calls and puts with

an exercise price of $60 are available. The calls have a premium of $7.27, and the puts

cost $1.10. The risk-free rate is 5%. Since the theoretical value of the put is $1.525, you

believe the puts are undervalued.

If you want to construct a riskless arbitrage to exploit the mispriced puts, you should

____________.

A. buy the call and sell the put

B. write the call and buy the put

C. write the call and buy the put and buy the stock and borrow the present value of the

exercise price

D. buy the call and buy the put and short the stock and lend the present value of the

exercise price

The daily settlement of obligations on futures positions is called _____________.

A. a margin call

B. marking to market

C. a variation margin check

D. the initial margin requirement

What would you expect to have happened to the spread between yields on commercial

paper and Treasury bills immediately after September 11, 2001?

A. no change, as both yields will remain the same

B. increase, as the spread usually increases in response to a crisis

C. decrease, as the spread usually decreases in response to a crisis

D. no change, as both yields will move in the same direction

A firm is expected to produce earnings next year of $3 per share. It plans to reinvest

25% of its earnings at 20%. If the cost of equity is 11%, what should be the value of the

stock?

A. $27.27

B. $37.50

C. $66.67

D. $70

One feasible way to hedge labor income is to ____________________.

A. diversify your investment portfolio away from the industry in which you work

B. save for retirement only from investment income

C. change careers every 7 years

D. invest heavily in the stock options provided by your firm

An individual wants to have $95,000 per year to live on when she retires in 30 years.

The individual is planning on living for 20 years after retirement. If the investor can

earn 6% during her retirement years and 10% during her working years, how much

should she be saving during her working life? (Hint: Treat all calculations as annuities.)

A. $9,872

B. $8,234

C. $7,908

D. $6,624

__________ often accompany short sales and are used to limit potential losses from the

short position.

A. Limit orders

B. Restricted orders

C. Limit loss orders

D. Stop-buy orders

The fastest-growing category of hedge funds is feeder funds. These funds invest in

________.

A. other hedge funds

B. convertible securities and preferred stock

C. equities and bonds

D. managed futures and options