1) Which of the following ratios is least likely to be impacted by accounting

manipulation?

a. P/E

b. ROE

c. ROI

d. P/S

e. PM

2) All of the following are considered fixed income securities except

a.Debentures.

b.Eurobonds.

c.Preferred stock.

d.Mutual funds.

e.Yankee bonds.

3) Options embedded in real assets owned by firms are known as

a. Asset options.

b. Binomial options.

c. Company options.

d. Warrant options.

e. Real options.

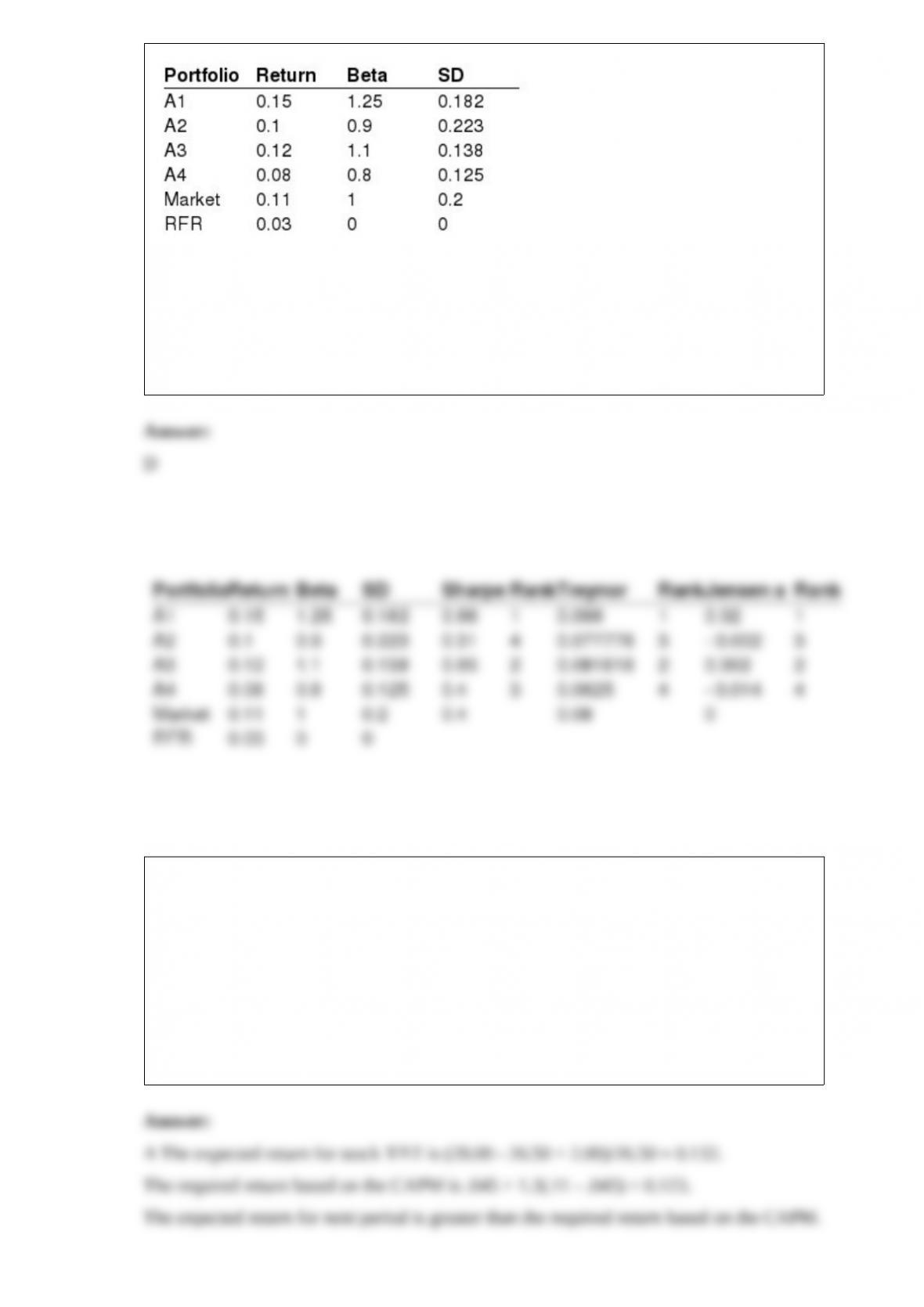

4) Exhibit 25.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information for four portfolios, the market and the risk free rate

(RFR):

Calculate the Sharpe Measure for each portfolio.

a. A1 = 0.40, A2 = 0.31, A3 = 0.65, A4 = 0.66

b. A1 = 0.31, A2 = 0.66, A3 = 0.65, A4 = 0.40

c. A1 = 0.66, A2 = 0.65, A3 = 0.31, A4 = 0.40

d. A1 = 0.66, A2 = 0.31, A3 = 0.65, A4 = 0.40

e. None of the above

5) Assume the risk-free rate is 4.5% and the expected return on the market is 11%. You

anticipate Stock XYZ to sell for $28 at the end of next year and pay a dividend of $2.

The stock is currently selling for $26.50 with a beta of 1.2. You currently hold stock

XYZ in a well-diversified portfolio. Assuming you have money to invest, you should:

a. Buy stock XYZ.

b. Sell stock XYZ.

c. Do nothing because it is properly valued.

d. Invest your money in the risk-free rate of return.

e. Both b and d above.

6) Which bond provision would be considered the most risky for an investor who is

concerned that market interest rates will drop dramatically over the life of the bond?

a. Sinking fund

b. Deferred call

c. Freely callable

d. Non-callable

e. None of the above

7) Exhibit 6.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Rit= return for stock i during period t

Rmt= return for the aggregate market during period t

Refer to Exhibit 6.3. What is the abnormal rate of return for Elliot when you consider

its systematic risk measure (beta)?

a.-2.10%

b.-2.00%

c.5.20%

d.14.10%

e.None of the above

8) Exhibit 23.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The WallMal Company has entered into a 4-year interest rate swap, with semiannual

settlement, to pay a fixed rate of 8% per year and receive 6-month LIBOR. The notional

principal is $50,000,000.

Indicate the market value of the swap to the WallMal Company.

a. $5,786,345

b. -$3,575,987

c. $1,289,450

d. -$1,514,900

e. $1,250,075

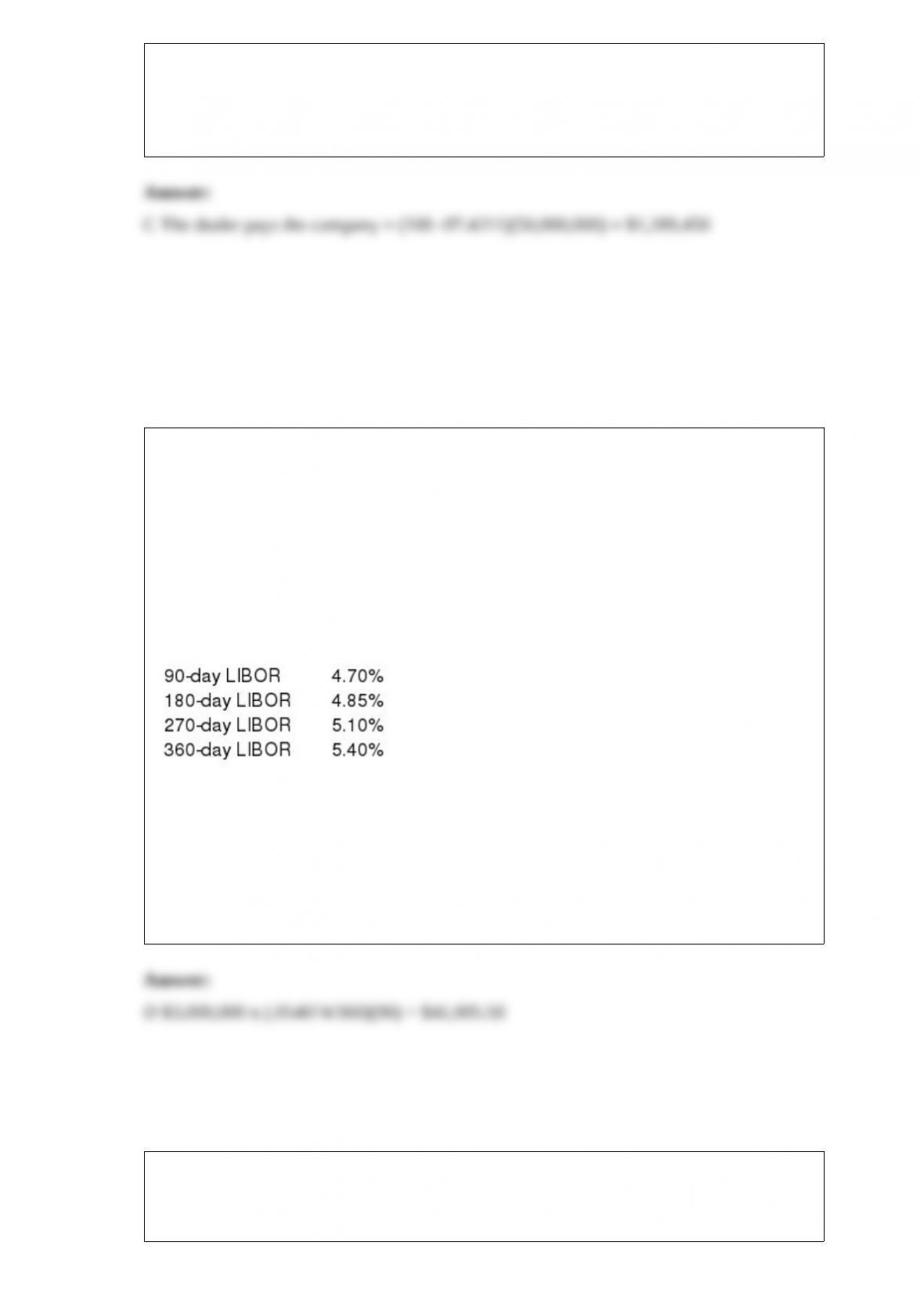

9) Exhibit 21.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

As a relationship officer for a money-center commercial bank, one of your corporate

accounts has just approached you about a one-year loan for $3,000,000. The customer

would pay a quarterly interest expense based on the prevailing level of LIBOR at the

beginning of each quarter. As is the bank’s convention on all such loans, the amount of

the interest payment would then be paid at the end of the quarterly cycle when the new

rate for the next cycle is determined. You observe the following LIBOR yield curve in

the cash market:

If 90-day LIBOR rises to the levels “predicted” by the implied forward rates, what will

the dollar level of the bank’s interest receipt be at the end of the third quarter?

a. $35,250.00

b. $36,375.00

c. $38,250.00

d. $41,005.50

e. None of the above

10) Exhibit 18.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

A $1000 par value bond with 4 years to maturity and a 5% coupon has a yield to

maturity of 6%. Interest is paid annually.

Estimate the percentage price change for this 4-year $1,000 par value bond, with annual

5% coupon, if the yield falls from 6% to 5.5%.

a. -3.50%

b. -1.75%

c. 1.75%

d. 3.50%

e. None of the above

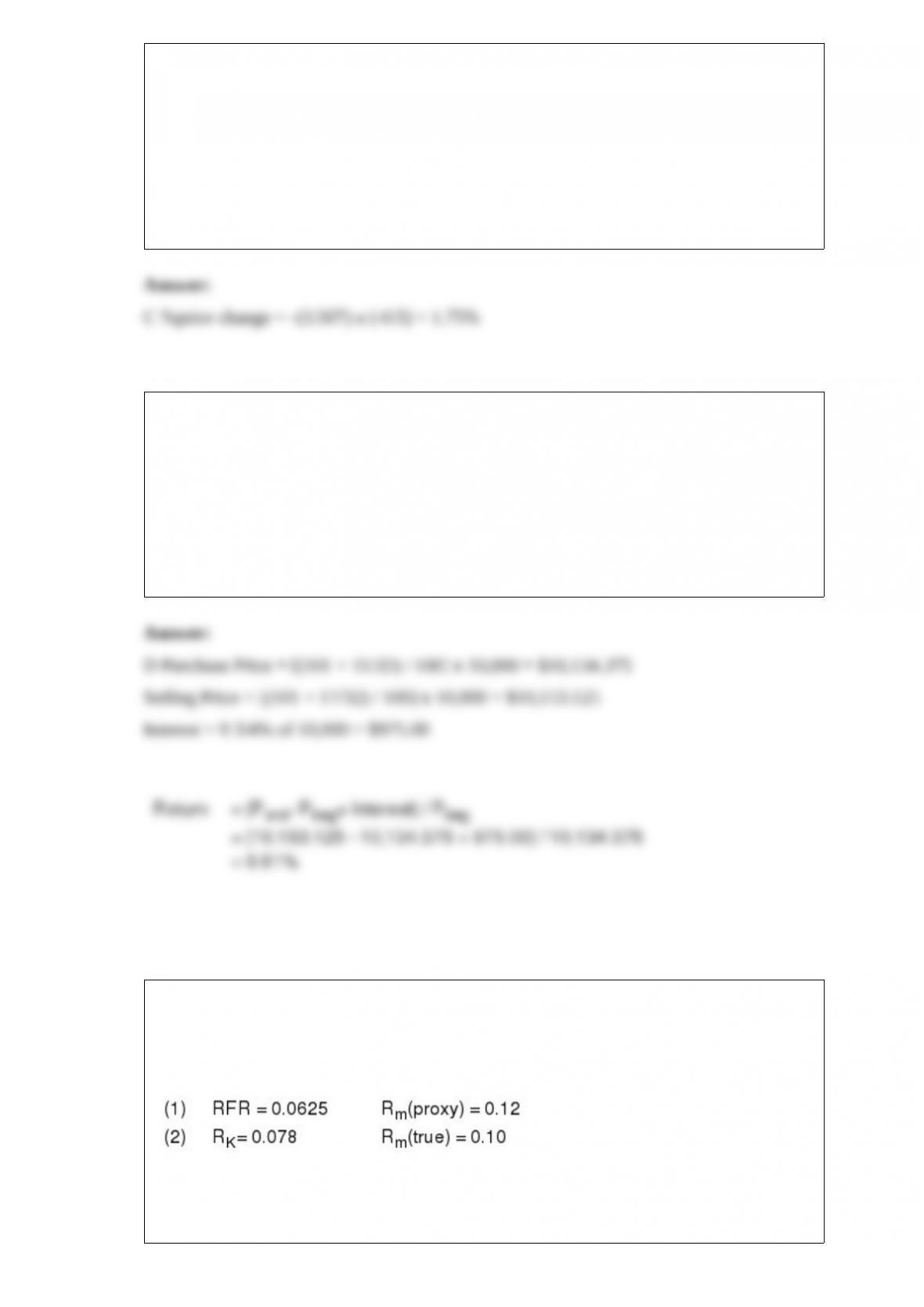

11) You purchase a 9 3/4s February $10,000 par Treasury Note at 101:11 and hold it for

exactly one year at which time you sell it. What is your rate of return if your selling

price is 101:17?

a. 8.14%

b. 8.75%

c. 9.75%

d. 9.81%

e. 10.47%

12) Assume that as a portfolio manager the beta of your portfolio is 1.15 and that your

performance is exactly on target with the SML data under condition 1. If the true SML

data is given by condition 2, how much does your performance differ from the true

SML?

a. 2.53% lower

b. 3.85% lower

c. 2.53% higher

d. 4.4% higher

e. 3.85% higher

13) The betas of those companies compiled by Value Line Investment Services tend to

be almost identical to those compiled by Merrill Lynch.

14) A rise in the Confidence Index published by Barron’s is an indication investors will

purchase more lower-quality bonds.

15) A nonrefunding provision prohibits a call and premature retirement of an issue from

the proceeds of a lower-coupon refunding bond.

16) An example of a relative valuation technique is the Price/Cash Flow ratio.

17) A pure auction market is also referred to as a quote-driven market.

18) Banks have high liquidity needs and therefore, have a short time horizon.

19) Combining assets that are not perfectly correlated does affect both the expected

return of the portfolio as well as the risk of the portfolio.

20) A cyclical stock’s rate of return is not expected to decline during an overall market

decline.

21) The goal of a hedge transaction is to increase expected returns of a fundamental

holding.

22) The most difficult part of valuing a bond is determining the required rate of return

on this investment.