Liquidity risk for an FI includes the possibility of an unexpected inflow of funds.

Answer:

During the financial crisis of 2008, there were large deposit inflows to the banking

system.

Answer:

The buyer of a loan participation benefits because the only risk exposure is to the

borrower.

Answer:

FDICIA required that banks and thrifts adopt the same capital requirements.

Answer:

For a given change in interest rates, fixed-rate liabilities with longer-term maturities

will have smaller changes in price than liabilities with shorter maturities.

Answer:

The Pension Benefit Guaranty Corporation (PBGC) insures pension benefits against the

under-funding of pension plans by corporations.

Answer:

Under Basel III, banks must hold a total capital to credit risk-adjusted assets equal to 8

percent to be adequately capitalized.

Answer:

One method of reducing the risk of a liquidity crisis for an FI to efficiently manage

liquid asset positions.

Answer:

Usury ceilings place caps on interest rates that FIs can charge on certain types of loans

and are established by federal regulatory authorities.

Answer:

The risk-based capital ratio fails to take into account the effects of diversification in the

credit portfolio.

Answer:

All credit unions are nationally chartered and regulated by the National Credit Union

Administration.

Answer:

Hedging the FI’s interest rate risk by buying a put option on a bond is an attractive

alternative to a manager.

Answer:

Banks increasingly have been susceptible to nonbank competition on both sides of the

balance sheet.

Answer:

The commercial paper market is an example of nonbank competition on the asset side

of the balance sheet that has become increasingly intense for banks.

Answer:

If a household invests in corporate securities and does not supervise how the funds are

invested or used by the corporation, the risk of not earning the desired return or not

having the funds returned increase.

Answer:

Decimalization involves making quotes in the equities markets in units of 1 cent ($0.01)

rather than in units of one-eights of a dollar ($0.125).

Answer:

In general, the interest rate spread (spread effect) between rate sensitive assets and rate

sensitive liabilities is positively related to the change in net interest income.

Answer:

Small banks make proportionately larger amounts of real estate loans than large banks.

Answer:

In the repricing gap model, assets or liabilities are rate sensitive within a given time

period if the dollar values of each are subject to receiving a different interest rate should

market rates change.

Answer:

In recent years, the proportion of savings and demand deposits have decreased and the

proportion of pension funds have increased in the financial assets held by U.S.

households.

Answer:

Market risk is present whenever an FI takes an open position and prices change in a

direction opposite to that expected.

Answer:

Credit derivatives allow FIs to reduce credit risks without removing loan assets from

their balance sheet.

Answer:

Buying a cap is like buying insurance against a decrease in interest rates.

Answer:

Investing in appropriate technology allows an FI to access lower-cost funding markets.

Answer:

The more costly it is to supervise the use of funds by a borrower, the less likely a saver

will encounter agency costs.

Answer:

The book value of bank equity is the present value of assets minus the present value of

liabilities.

Answer:

Finance companies generally charge lower interest rates on consumer loans than do

depository institutions.

Answer:

Because retail CDs have fixed maturities, FI managers always should have perfect

information regarding the scheduling of interest and principal payments.

Answer:

In the statistical modeling of the country risk analysis, the investment ratio is

considered to have a negative impact on the probability of rescheduling because the

larger expenditures on investment infrastructure leaves less funds for debt payment.

Answer:

Regulator forbearance is a policy of allowing economically insolvent FIs to continue in

operation.

Answer:

Which of the following observations concerning payday lenders is NOT TRUE?A.

They provide short-term cash advances.

B. Their advances are due when borrowers receive their next paycheck.

C. The industry originated from check cashing outlets.

D. The payday loan industry is regulated at the state level.

E. The demand for short-term loans has decreased considerably.

Answer:

The economic insolvency of many thrift institutions during the 1980s was due, at least

in part, to unexpected increases in interest rates.

Answer:

If the average maturity of assets is 4 years and the average maturity of liabilities is 4

years, then the FI has no interest rate risk exposure.

Answer:

The DEAR of a portfolio of assets is simply the weighted average of each individual

assets’ DEAR.

Answer:

In the life insurance model, morbidity risk differs from mortality risk by the

circumstances surrounding the actual death event.

Answer:

The determination of risk-adjusted on-balance-sheet assets under Basel III requires the

segregation of assets into nine categories of credit risk exposure.

Answer:

The discount effect and the prepayment effect are negatively correlated in their impact

on the value of a principal-only (PO) mortgage-backed strip security.

Answer:

A bank with a negative repricing (or funding) gap faces reinvestment risk.

Answer:

Surrender value is the amount of cash a life insurance policy holder can receive by

turning in the policy before it expires or matures.

Answer:

A U.S. bank agrees to a swap of making fixed-rate interest payments of $12 million to a

UK bank in exchange for floating-rate payments of LIBOR + 4 percent in British

pounds for a notional amount of £100 million. The current exchange rate is $1.50/£.

The interest payments will be exchanged at the end of the year at the prevailing rates.

At the end of the year, LIBOR is 4 percent and the exchange rate is $1.50/£. What is the

net payment paid or received in dollars by the U.S. bank? A. The U.S. bank paid $12

million and received $8 million for a net payment of $4 million.

B. The U.S. bank paid $12 million and received $10 million for a net payment of $2

million.

C. The U.S. bank paid $12 million and received $12 million for a net receipt of $0

million.

D. The U.S. bank paid $12 million and received $14 million for a net receipt of $2

million.

E. The U.S. bank paid $12 million and received $16 million for a net receipt of $4

million.

Answer:

What is the duration of this Treasury note? A. 1.500 years.

B. 1.371 years.

C. 1.443 years.

D. 2.882 years.

E. 1.234 years.

Answer:

A bank has assets of $500,000,000 and equity of $40,000,000. The assets have an

average duration of 5.5 years, and the liabilities have an average duration of 2.5 years.

An 8-year fixed-rate T-bond with the same coupon as the fixed-rate on the swap has a

duration of 6 years, and the duration of a floating-rate bond that reprices annually is one

year. The bank wishes to hedge its balance sheet with swap contracts that have notional

contracts of $100,000. What is the optimal number of swap contracts into which the

bank should enter? A. 2,500 contracts.

B. 2,760 contracts.

C. 13,800 contracts.

D. 3,200 contracts.

E. None of the above.

Answer:

Credit spread call options are useful becauseA. its value increases as the risk premium

on a specified benchmark bond of the borrower increases above some exercise spread.

B. an increase in the value of the call option will tend to offset the decreasing value of

an FI’s loan and net worth as the credit quality of the borrower decreases.

C. they will always cause a loss at least equal to the required premium on the option.

D. All of the above.

E. Answers A and B only.

Answer:

Banks and other FIs sell loans because of all of the following EXCEPT A. loan

diversification benefits.

B. reduction in reserve requirements.

C. lowering of capital costs.

D. reduction of liquid assets of the institution.

E. increase in fee income through brokerage functions.

Answer:

What is the bank’s leverage adjusted duration gap? A. 6.73 years

B. 0.29 years

C. 6.44 years

D. 6.51 years

E. 0 years.

Answer:

Use the following two choices to identify whether each intermediary or entity is a net

buyer or net seller of credit derivative securities.

a. Net buyer (typically)

b. Net seller (typically)

Corporations

Answer:

Given the expected one-year rates in one year, what are the possible bond prices in one

year? A. $85.22 and $86.25.

B. $85.73 and $86.69.

C. $85.22 and $86.69.

D. $85.73 and $86.25.

E. $83.35 and $84.65.

Answer:

This risk of default is associated with general economy-wide or macro conditions

affecting all borrowers. A. Systematic credit risk.

B. Firm-specific credit risk.

C. Refinancing risk.

D. Liquidity risk.

E. Sovereign risk.

Answer:

Which of the following was not an operating characteristic of foreign banks operating

in the U.S. prior to the International Banking Act of 1978? A. They had no access to

the Federal Reserve’s discount window.

B. They were not subject to the Federal Reserve’s audits and exams.

C. They had special rates on FDIC deposit insurance.

D. They could not use the Fedwire or the fed funds market.

E. They were not subject to the Glass-Steagall Act.

Answer:

As interest rates increase, the buyer of a bond put option stands to A. make limited

gains.

B. incur limited losses.

C. incur unlimited losses.

D. lose the entire premium amount.

E. Answers A and D only.

Answer:

Another method that may be employed by banks to lower required reserves is to A.

transfer deposits to another domestic bank on Friday and transfer them back on the

following Monday.

B. sweep demand deposits into higher interest-bearing accounts on Friday with a return

sweep the following Monday.

C. rely more heavily on zero explicit interest-rate deposits.

D. delay posting deposits made on Friday until the following Monday.

E. do nothing, because reserve requirements cannot be avoided.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation separated commercial and investment banking.

Answer:

The federal safety net to minimize bank failures includes all of the following EXCEPT

A. deposit insurance.

B. reserve requirements.

C. contagious runs.

D. minimum capital requirements.

E. the discount window of the Federal Reserve Bank.

Answer:

Policies established by The International Swaps and Derivatives Association (ISDA)

forbid swap contracts to be made between parties of different credit standing.

Answer:

Overseas bank is pooling 50 similar and fully amortized mortgages into a pass-through

security. The face value of each mortgage is $100,000 paying 180 monthly interest and

principal payments at a fixed rate of 9 percent per annum.

For the first monthly payment, what are the interest and principal portions of the

payment? A. $37,500 principal and $13,213 principal.

B. $37,500 interest and $13,213 principal.

C. $37,500 principal and $7,809 interest.

D. $37,500 interest and $7,809 principal.

E. $37,500 interest and $17,756 principal.

Answer:

A reason for the use of market risk management (MRM) for the purpose of identifying

potential misallocations of resources caused by prudential regulation is which of the

following? A. Regulation.

B. Resource allocation.

C. Management information.

D. Setting limits.

E. Performance evaluation.

Answer:

The contagion effect A. stems from the positive correlation in FI returns.

B. results when interest rate risk increases credit risk and liquidity risk exposures.

C. occurs when liquidity risk problems at bad banks damages well-run banks.

D. occurs when a computer virus infects the computerized electronics payments

systems Fedwire and CHIPS.

E. is completely eliminated by government provided deposit insurance against bank

runs.

Answer:

Holding corporate bonds with fixed interest rates involves A. default risk only.

B. interest rate risk only.

C. liquidity risk and interest rate risk only.

D. default risk and interest rate risk.

E. default and liquidity risk only.

Answer:

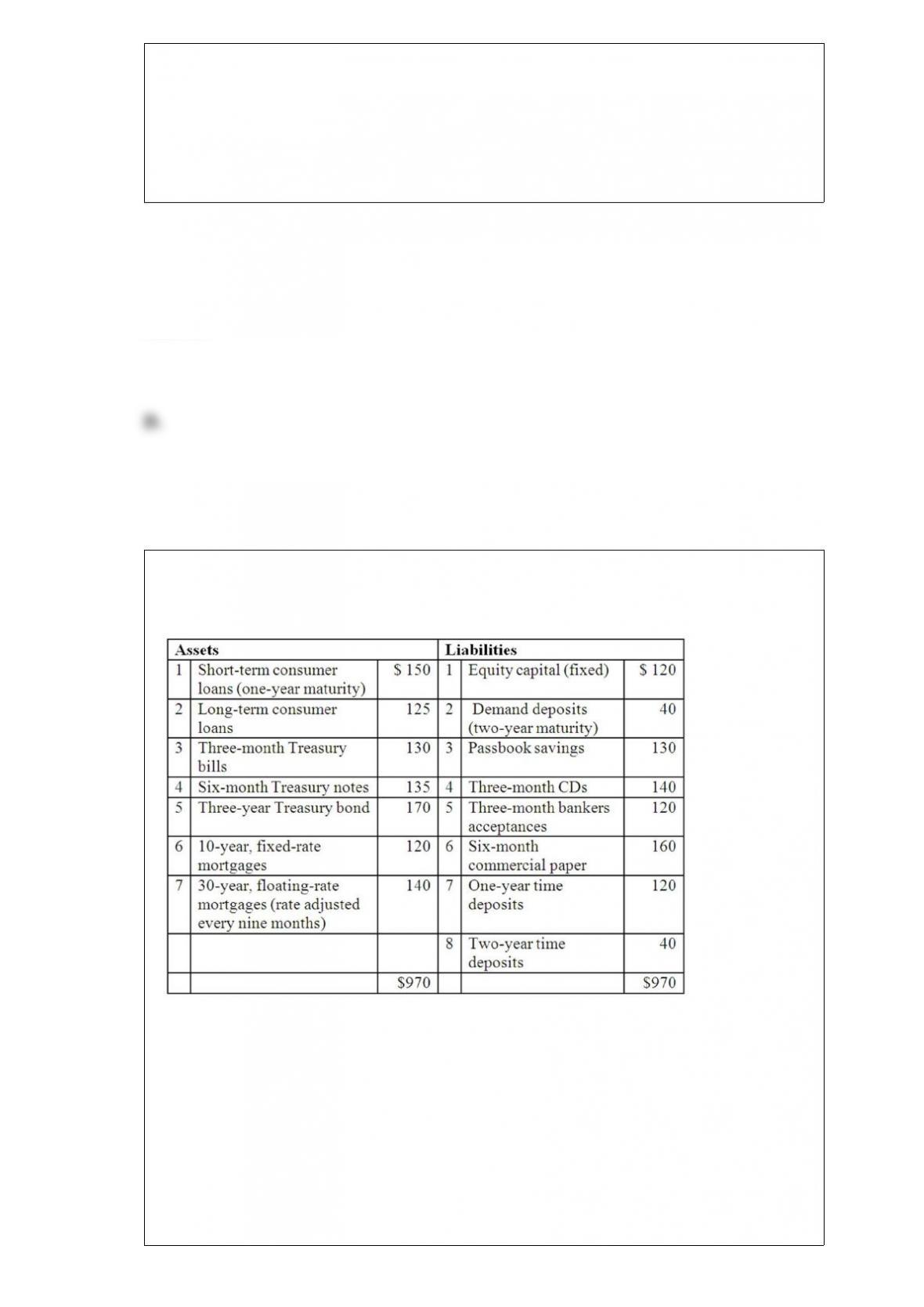

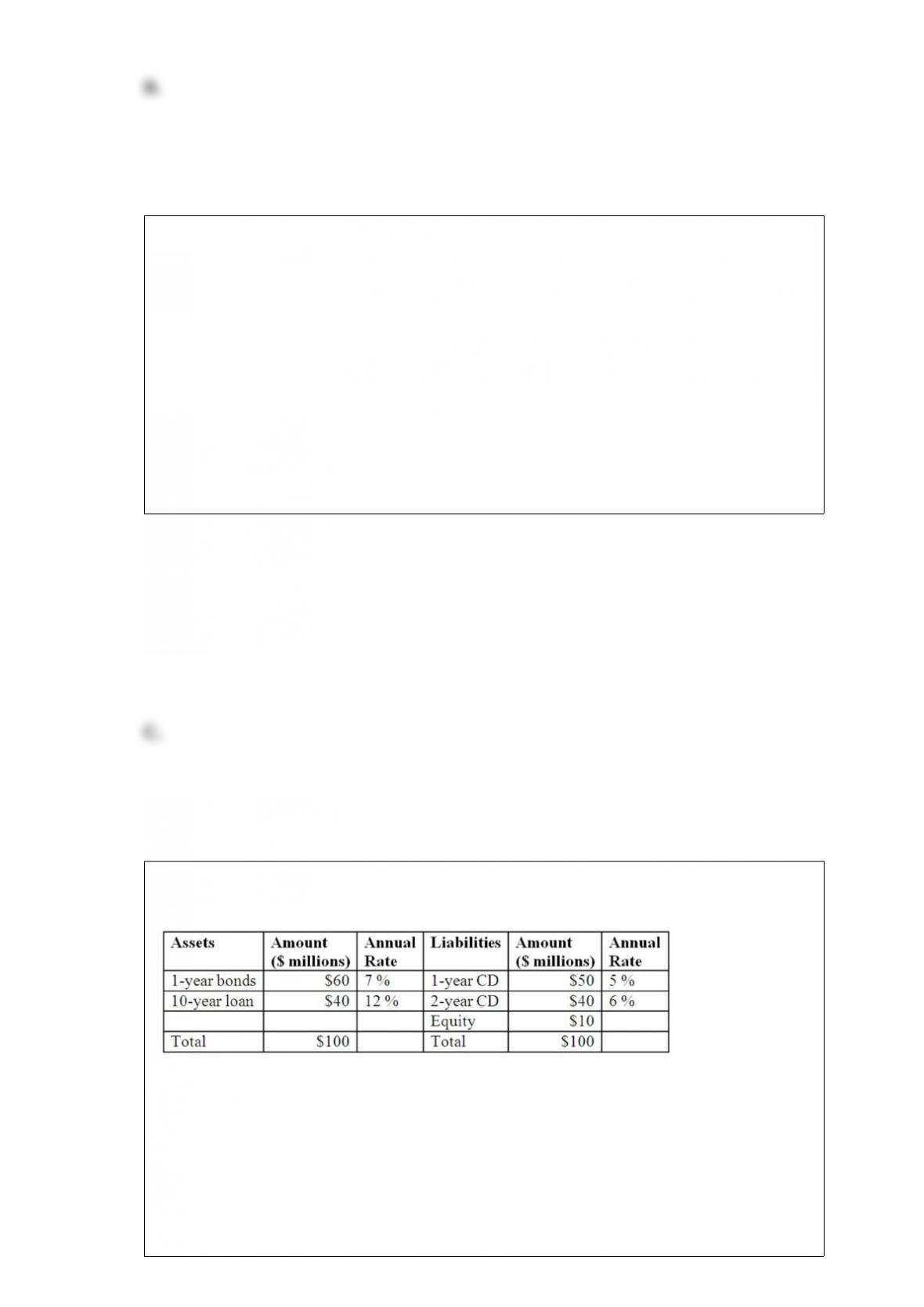

The balance sheet of XYZ Bank appears below. All figures in millions of US Dollars.

Suppose that

interest rates rise by 2 percent on both RSAs and RSLs. The expected annual change in

net interest income of the bank isA. -$300,000.

B. $500,000.

C. -$2,800,000.

D. -$3,000,000.

E. $300,000.

Answer:

Use the duration model to approximate the change in the market value (per $100 face

value) of two-year loans if interest rates increase by 100 basis points. A. -$1.756

B. -$1.775

C. +$98.24

D. -$1.000

E. +$1.924

Answer:

Which of the following is not included in the Common Equity Tier I capital under Basel

III? A. Retained earnings.

B. Par value of common shares issued by the bank.

C. Par value of noncumulative perpetual preferred stock.

D. Paid-in excess (surplus) of common stock.

E. Common shares issued by consolidated subsidiaries of the bank.

Answer:

Which of the following is NOT a reason for a FI to sell loans with recourse? A. To

reduce capital requirements.

B. To avoid credit risk exposure.

C. To control interest rate risk exposure.

D. To avoid regulatory scrutiny.

E. To make it possible to lend large amounts to an individual borrower.

Answer:

If in one year there is no change to either interest rates or exchange rates, what is the

end-of-year profit or loss for the bank? (Hint: Annual interest is paid on both the

Canadian bonds and the CD on the date of liquidation in exactly one year.) A. Profit of

US $20,000.

B. Loss of C $224,000.

C. Profit of US $50,000.

D. Profit of C $63,700.

E. Profit of US $313,000.

Answer:

Identify the correct observation. A. Most loan sales are completed in less than 30 days.

B. Up to 50 percent of loan sales eventually fail to be completed at all.

C. There is no incentive to renege on a loan sales contract.

D. The tendency to renege on a loan sales contract decrease as market prices move

away from those originally agreed.

E. Contractual problems, trading frictions, and costs rarely affect loan sales.

Answer:

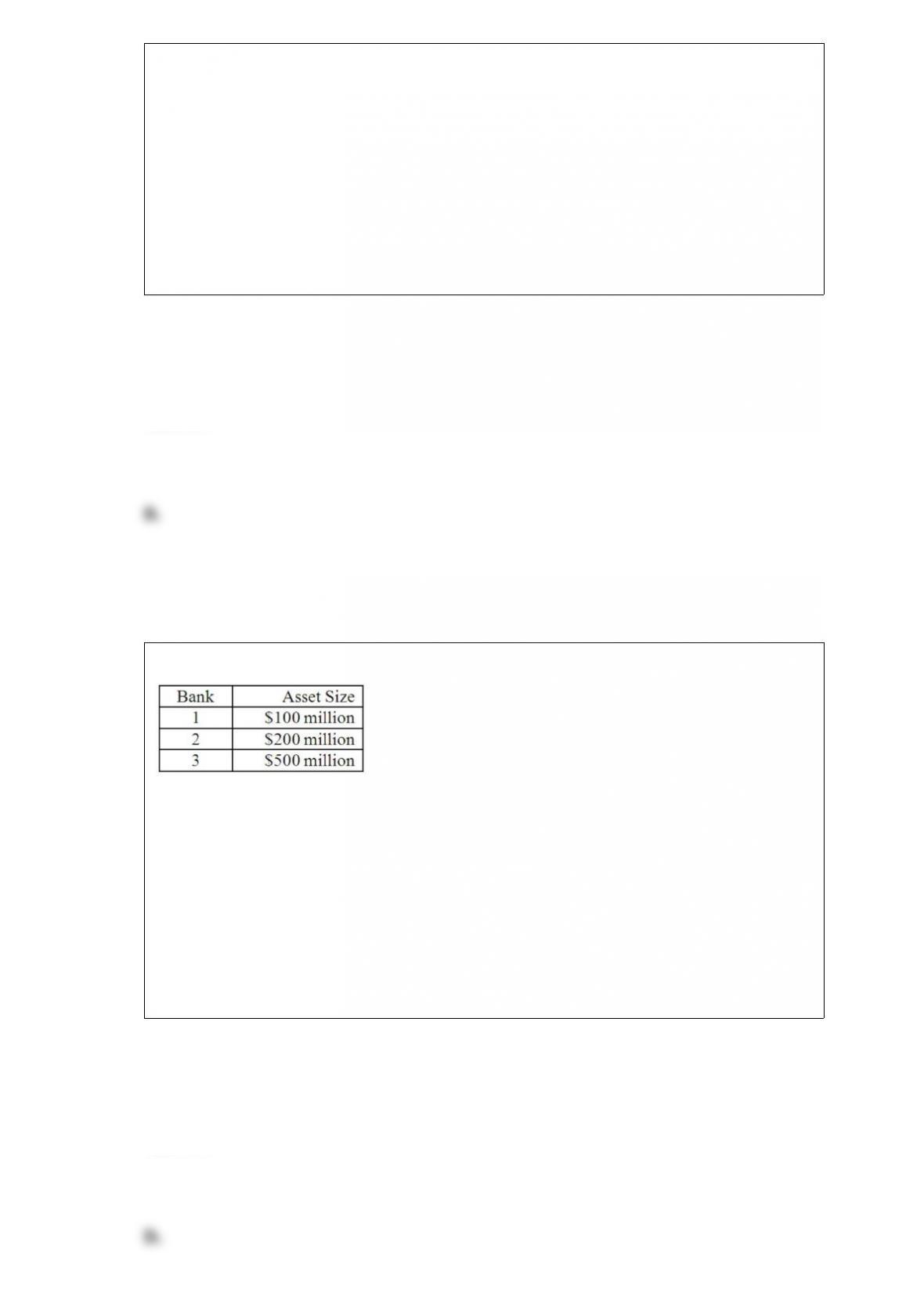

What is the market share of Bank 3? A. 12.5 percent.

B. 37.5 percent.

C. 25.0 percent.

D. 62.5 percent.

E. 50.0 percent.

Answer:

Which of the following arises in policies in which the insured event occurs during a

coverage period but a claim is not filed or reported until many years later? A. Short-tail

losses.

B. Adverse selection.

C. Moral hazard.

D. Long-tail losses.

E. Social inflation.

Answer:

An agreement between a buyer and a seller at time 0 to exchange a pre-specified asset

for cash at a specified later date is the characteristic of a A. spot contract.

B. forward contract.

C. futures contract.

D. put options contract.

E. call options contract.

Answer:

Which of the following identifies the primary function of the Office of the Comptroller

of the Currency? A. Manage the deposit insurance fund and carry out bank

examinations.

B. Regulate and examine bank holding companies as well as individual commercial

banks.

C. Charter national banks and approve their merger activity.

D. Determine permissible activities for state chartered banks.

E. Stand as the “lender of last resort” for troubled banks.

Answer:

Hadbucks National Bank current balance sheet appears below. All assets and liabilities

are currently priced at par and pay interest annually.

What is the

weighted average maturity of liabilities? A. 5.50 years.

B. 6.40 years.

C. 1.44 years.

D. 1.30 years.

E. 1.10 years.

Answer:

In the derivatives markets, the instrument with the longest potential maturity is A.

options.

B. futures.

C. forwards.

D. swaps.

E. currencies.

Answer:

If Bank 1 is acquired by Bank 2, what is the impact on the market’s HHI? A. An

increase in the HHI of 1600.

B. An increase in the HHI of 625.

C. An increase in the HHI of 1563.

D. A decrease in the HHI of 222.

E. A decrease in the HHI of 360.

Answer:

“Matching the book” or trying to match the maturities of assets and liabilities is

intended to protect the FI from A. liquidity risk.

B. interest rate risk.

C. credit risk.

D. foreign exchange risk.

E. off-balance-sheet risk.

Answer:

An agreement between a buyer and a seller at time 0 where the seller of an asset agrees

to deliver an asset immediately and the buyer agrees to pay for the asset immediately is

the characteristic of a A. spot contract.

B. forward contract.

C. futures contract.

D. put options contract.

E. call options contract.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation limited thrift investments in non-residential real estate.

Answer: