A trader who has a __________ position in oil futures believes the price of oil will

__________ in the future.

A. short; increase

B. long; increase

C. short; stay the same

D. long; stay the same

Dividend discount models and P/E ratios are used by __________ to try to find

mispriced securities.

A. technical analysts

B. statistical analysts

C. fundamental analysts

D. dividend analysts

E. psychoanalysts

If the economy is shrinking, firms with low operating leverage will experience

A. larger decreases in profits than firms with high operating leverage.

B. similar decreases in profits as firms with high operating leverage.

C.-smaller decreases in profits than firms with high operating leverage.

D. no change in profits.

International investing

A. cannot be measured against a passive benchmark, such as the S&P 500.

B. can be measured against a widely-used index of non-U.S. stocks, the EAFE Index

(Europe, Australia, Far East).

C. can be measured against international indexes.

D. can be measured against a widely-used index of non-U.S. stocks, the EAFE Index

(Europe, Australia, Far East), and against international indexes.

E. None of the options are correct.

As the number of securities in a portfolio is increased, what happens to the average

portfolio standard

deviation?

A. It increases at an increasing rate.

B. It increases at a decreasing rate.

C. It decreases at an increasing rate.

D. It decreases at a decreasing rate.

E. It first decreases, then starts to increase as more securities are added.

Security selection refers to

A. choosing which securities to hold based on their valuation.

B. investing only in “safe” securities.

C. the allocation of assets into broad asset classes.

D. top-down analysis.

You write one JNJ February 70 put for a premium of $5. Ignoring transactions costs,

what is the break-even price of this position?

A.$65

B.$75

C. $5

D. $70

A hybrid strategy is one where the investor

A. uses both fundamental and technical analysis to select stocks.

B. selects the stocks of companies that specialize in alternative fuels.

C. selects some actively-managed mutual funds on their own and uses an investment

advisor to select other actively-managed funds.

D. maintains a passive core and augments the position with an actively-managed

portfolio.

The elasticity of a stock call option is always

A. greater than one.

B. smaller than one.

C. negative.

D. infinite.

E. None of the options are correct.

Normal backwardation

A. maintains that, for most commodities, there are natural hedgers who desire to shed

risk.

B. maintains that speculators will enter the long side of the contract only if the futures

price is below the expected spot price.

C. assumes that risk premiums in the futures markets are based on systematic risk.

D. maintains that, for most commodities, there are natural hedgers who desire to shed

risk, and that speculators will enter the long side of the contract only if the futures price

is below the expected spot price.

E. maintains that speculators will enter the long side of the contract only if the futures

price is below the expected spot price and assumes that risk premiums in the futures

markets are based on systematic risk.

In the mean-standard deviation graph, the line that connects the risk-free rate and the

optimal risky portfolio, P,

is called

A. the security market line.

B. the capital allocation line.

C. the indifference curve.

D. the investor’s utility line.

The weak form of the efficient-market hypothesis contradicts

A. technical analysis but supports fundamental analysis as valid.

B. fundamental analysis but supports technical analysis as valid.

C. both fundamental analysis and technical analysis.

D. technical analysis but is silent on the possibility of successful fundamental analysis.

In 2016, the proportion of mutual funds (based on total assets) specializing in bonds

was

A. 21.8%.

B. 28.0%.

C. 54.1%.

D. 73.4%.

E. 63.5%.

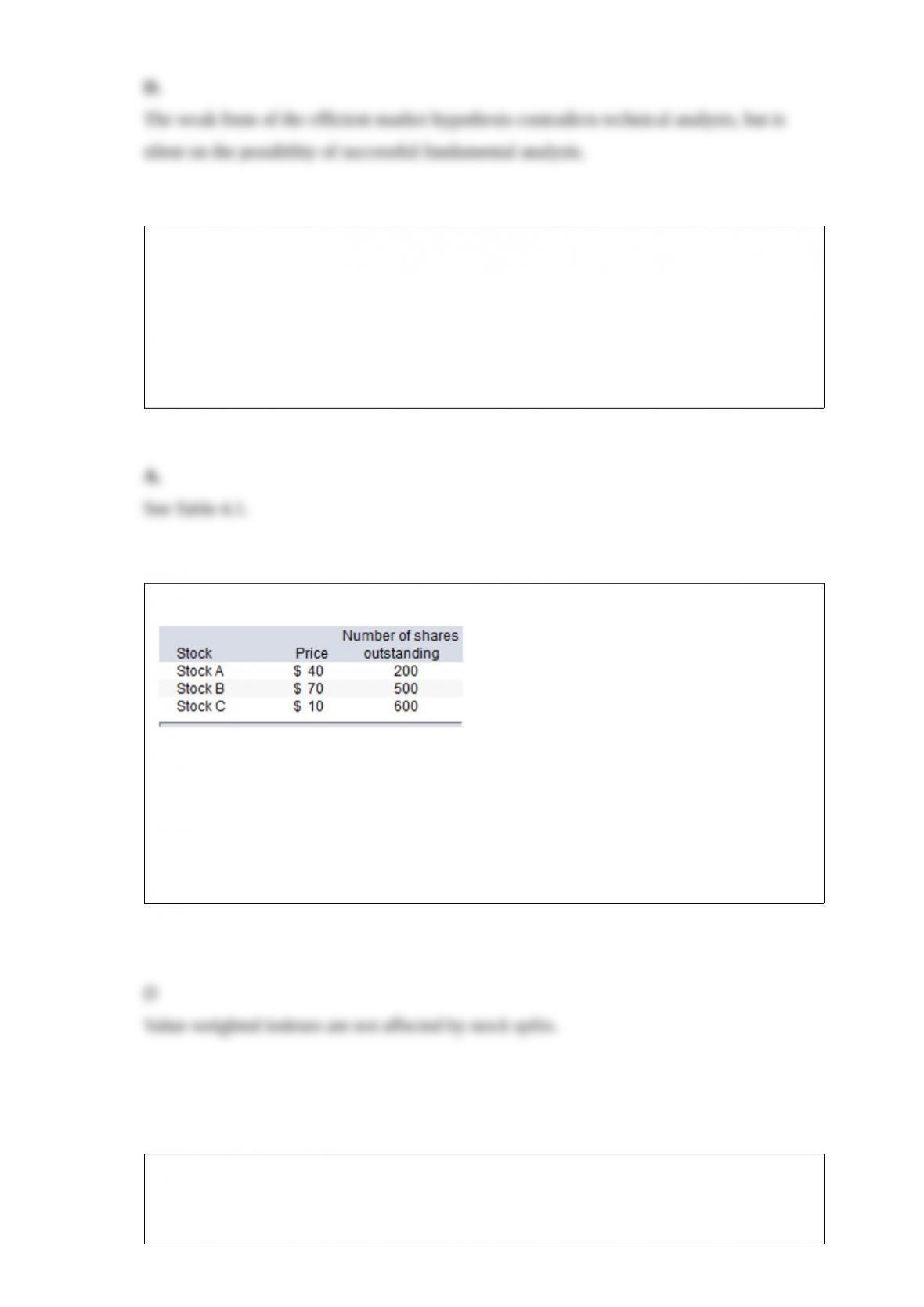

Consider the following three stocks:

Assume at these prices that the value-weighted index constructed with the three stocks

is 490. What would the index be if stock B is split 2 for 1 and stock C 4 for 1?

A. 265

B. 430

C. 355

D. 490

E. 1000

If a trader holding a long position in oil futures fails to meet the obligations of a futures

contract, the party that is hurt by the failure is

A. the offsetting short trader.

B. the oil producer.

C. the clearinghouse.

D. the broker.

E. the commodities dealer.

You invest $1,000 in a risky asset with an expected rate of return of 0.17 and a standard

deviation of 0.40 and a

T-bill with a rate of return of 0.04.

What percentages of your money must be invested in the risk-free asset and the risky

asset, respectively, to

form a portfolio with a standard deviation of 0.20?

A. 30% and 70%

B. 50% and 50%

C. 60% and 40%

D. 40% and 60%

E. Cannot be determined.

The “break-even” interest rate for year n that equates the return on an n-period

zero-coupon bond to that of an n 1 period zero-coupon bond rolled over into a one-year

bond in year n is defined as

A. the forward rate.

B. the short rate.

C. the yield to maturity.

D. the discount rate.

E. None of the options are correct.

Basu (1977, 1983) found that firms with low P/E ratios

A. earned higher average returns than firms with high P/E ratios.

B. earned the same average returns as firms with high P/E ratios.

C. earned lower average returns than firms with high P/E ratios.

D. had higher dividend yields than firms with high P/E ratios.

An American call-option buyer on a nondividend-paying stock will

A. always exercise the call as soon as it is in the money.

B. only exercise the call when the stock price exceeds the previous high.

C. never exercise the call early.

D. buy an offsetting put whenever the stock price drops below the strike price.

E. None of the options are correct.

A bond that can be retired prior to maturity by the issuer is a(n) ____________ bond.

A. convertible

B. secured

C. unsecured

D. callable

E. Yankee

You invest $1,000 in a risky asset with an expected rate of return of 0.17 and a standard

deviation of 0.40 and a

T-bill with a rate of return of 0.04.

What percentages of your money must be invested in the risky asset and the risk-free

asset, respectively, to

form a portfolio with an expected return of 0.11?

A. 53.8% and 46.2%

B. 75% and 25%

C. 62.5% and 37.5%

D. 46.2% and 53.8%

E. Cannot be determined.

According to the Capital Asset Pricing Model (CAPM), underpriced securities have

A. positive betas.

B. zero alphas.

C. negative betas.

D. positive alphas.

E. None of the options are correct.

An upward-sloping yield curve

A. may be an indication that interest rates are expected to increase.

B. may incorporate a liquidity premium.

C. may reflect the confounding of the liquidity premium with interest rate expectations.

D. All of the options are correct.

E. None of the options are correct.

A portfolio consists of 225 shares of stock and 300 calls on that stock. If the hedge ratio

for the call is 0.4, what would be the dollar change in the value of the portfolio in

response to a $1 decline in the stock price?

A. −$345

B. +$500

C. −$580

D. −$520

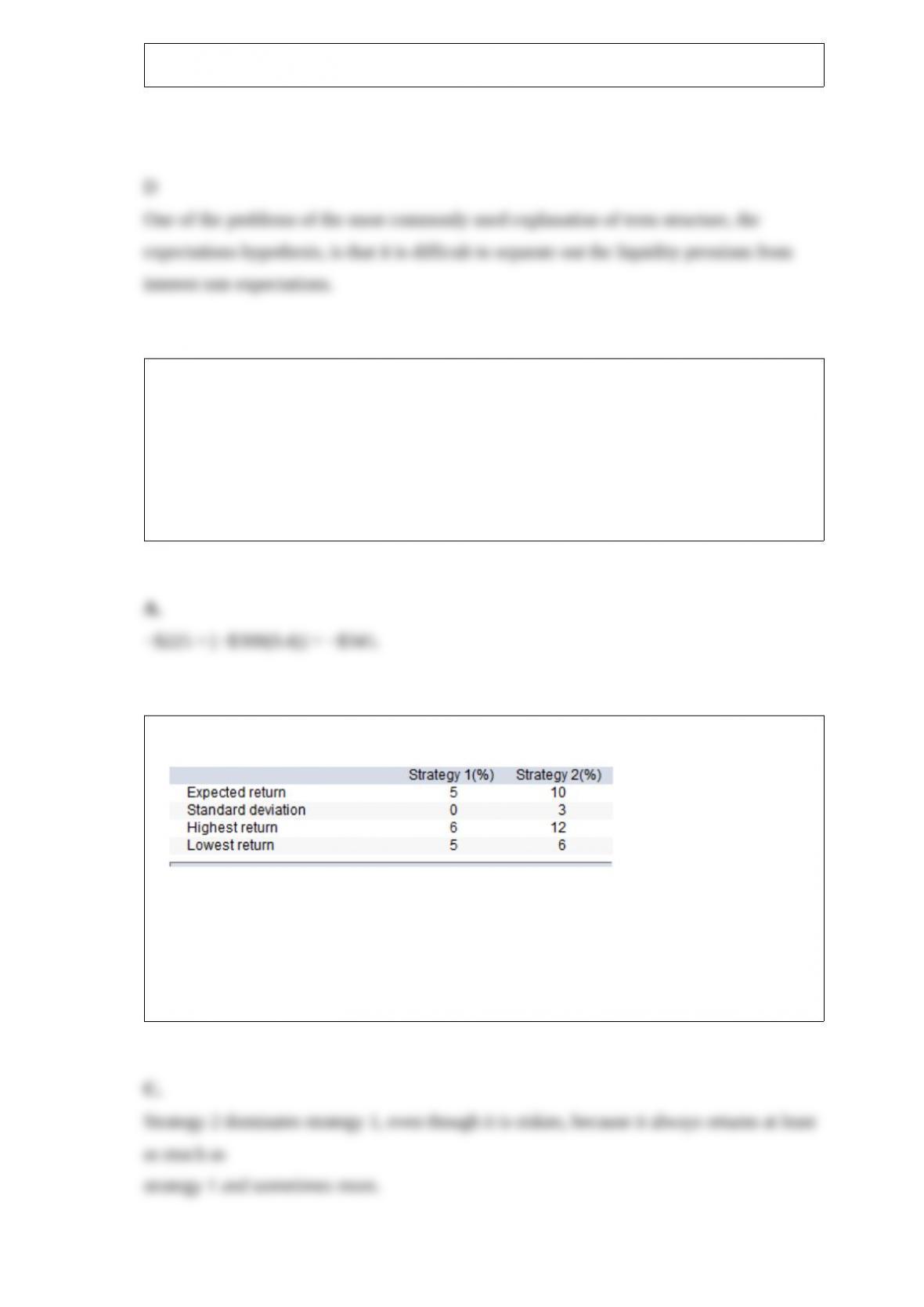

Consider these two investment strategies:

Strategy __________ is the dominant strategy because __________.

A. 1; it is riskless

B. 1; it has the highest reward/risk ratio

C.2; its return is greater than or equal to the return of Strategy 1

D. 2; it has the highest reward/risk ratio

E. Both strategies are equally preferred.

Other things equal, the price of a stock put option is positively correlated with the

following factors except

A. the stock price.

B. the time to expiration.

C. the stock volatility.

D. the exercise price.

Which of the following determine(s) the level of real interest rates?

I) The supply of savings by households and business firms

II) The demand for investment funds

III) The government’s net supply and/or demand for funds

A. I only

B. II only

C. I and II only

D. I, II, and III

You invest $600 in a security with a beta of 1.2 and $400 in another security with a beta

of 0.90. The beta of the

resulting portfolio is

A. 1.40.

B. 1.00.

C. 0.36.

D. 1.08.

E. 0.80.

A futures contract

A. is an agreement to buy or sell a specified amount of an asset at the spot price on the

expiration date of the contract.

B. is an agreement to buy or sell a specified amount of an asset at a predetermined price

on the expiration date of the contract.

C. gives the buyer the right, but not the obligation, to buy an asset sometime in the

future.

D. is a contract to be signed in the future by the buyer and the seller of the commodity.

E. None of the options are correct.

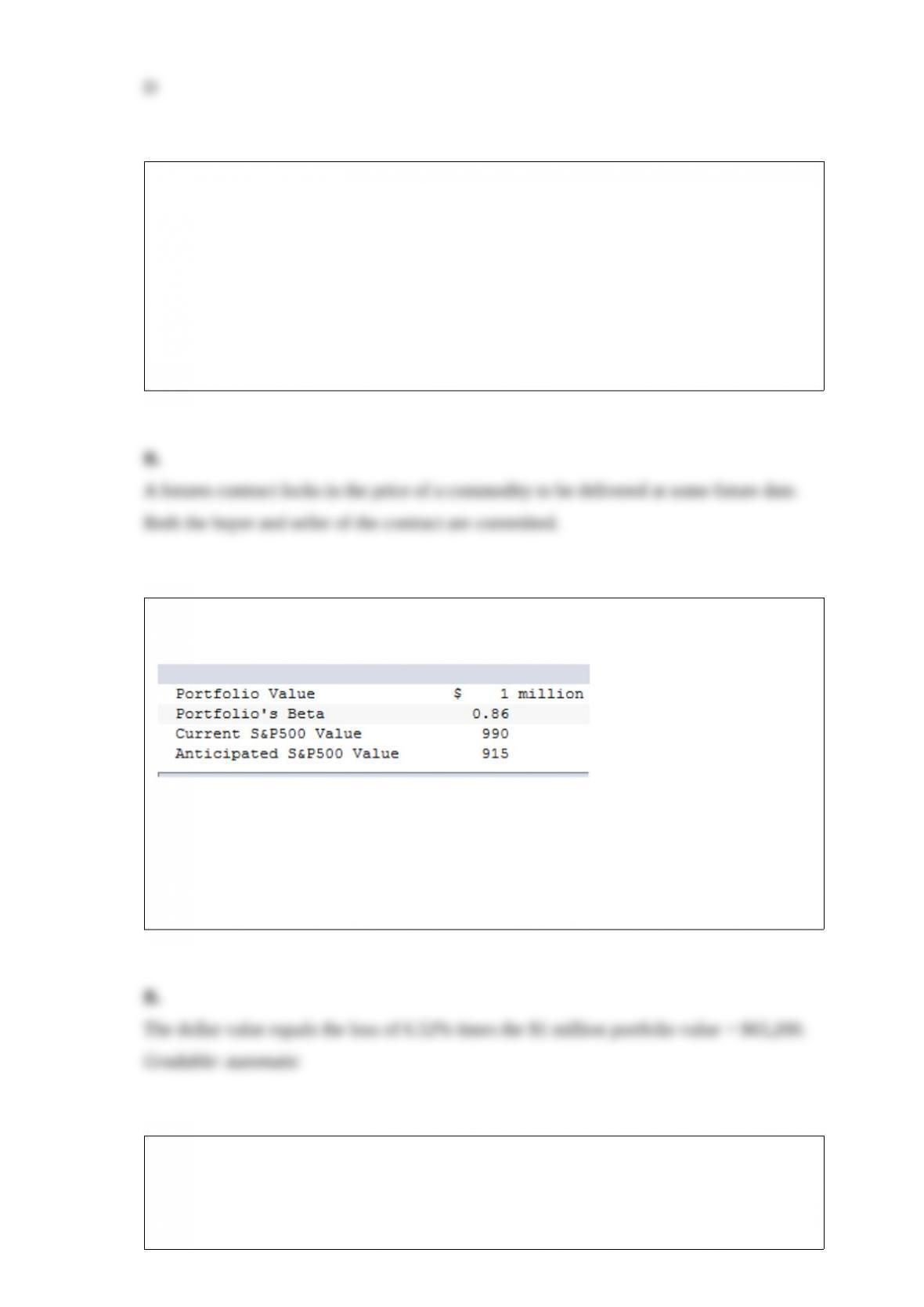

You are given the following information about a portfolio you are to manage. For the

long term, you are bullish, but you think the market may fall over the next month.

What is the dollar value of your expected loss?

A. $142,900

B. $65,200

C. $85,700

D. $30,000

E. $64,200

The duration of a bond is a function of the bond’s

A. coupon rate.

B. yield to maturity.

C. time to maturity.

D. All of the options are correct.

E. None of the options are correct.

The intrinsic value of an at-the-money put option is equal to

A. the stock price minus the exercise price.

B. the put premium.

C. zero.

D. the exercise price minus the stock price.

E. None of the options are correct.

The Treynor-Black model

A.considers both macroeconomic and microeconomic risks.

B. considers security selection only.

C. is nearly impossible to implement.

D. considers both macroeconomic and microeconomic risks and is nearly impossible to

implement.

E. considers security selection only and is nearly impossible to implement.

The preliminary prospectus is referred to as a(n)

A. red herring.

B. indenture.

C. greenmail.

D. tombstone.

E. headstone.