Suppose that the average P/E multiple in the oil industry is 16. Shell Oil is expected to

have an EPS of $4.50 in the coming year. The intrinsic value of Shell Oil stock should

be

A. $28.12.

B. $35.55.

C. $63.00.

D. $72.00.

E. None of the options are correct.

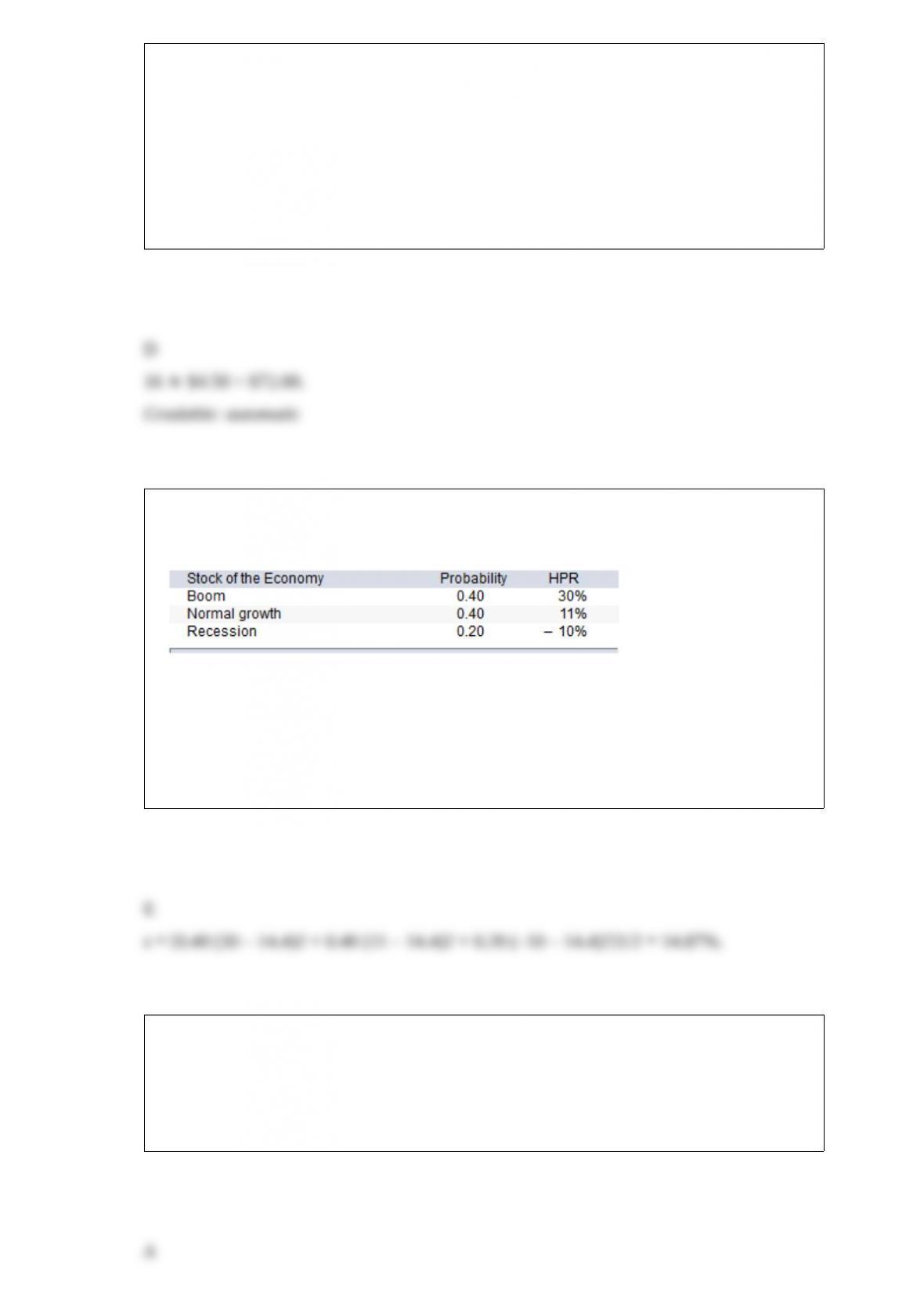

You have been given this probability distribution for the holding-period return for GM

stock:

What is the expected standard deviation for GM stock?

A. 16.91%

B. 16.13%

C. 13.79%

D. 15.25%

E. 14.87%

The duration of a perpetuity with a yield of 8% is

A. 13.50 years.

B. 12.11 years.

C. 6.66 years.

D. Cannot be determined

Which of the following statement(s) is(are) false regarding the variance of a portfolio of

two risky securities?

I) The higher the coefficient of correlation between securities, the greater the reduction

in the portfolio variance.

II) There is a linear relationship between the securities’ coefficient of correlation and the

portfolio variance.

III) The degree to which the portfolio variance is reduced depends on the degree of

correlation between

securities.

A. I only

B. II only

C. III only

D. I and II

E. I and III

If a portfolio had a return of 11%, the risk-free asset return was 6%, and the standard

deviation of the portfolio’s

excess returns was 25%, the risk premium would be

A. 14%.

B. 6%.

C. 35%.

D. 21%.

E. 5%.

In their multifactor model, Chen, Roll, and Ross found

A. that two market indexes, the equally weighted NYSE and the value weighted NYSE,

were not significant predictors of security returns.

B. that the value weighted NYSE index had the incorrect sign, implying a negative

market risk premium.

C. expected changes in inflation predicted security returns.

D. that two market indexes, the equally weighted NYSE and the value weighted NYSE,

were not significant predictors of security returns and that the value weighted NYSE

index had the incorrect sign, implying a negative market risk premium.

E. All of the options are correct.

An inverted yield curve is one

A. with a hump in the middle.

B. constructed by using convertible bonds.

C. that is relatively flat.

D. that plots the inverse relationship between bond prices and bond yields.

E. that slopes downward.

__________ are mutual funds that invest in one country only.

A. ADRs

B. ECUs

C. Single-country funds

D. All of the options are correct.

E. None of the options are correct.

A collar with a net outlay of approximately zero is an options strategy that

A. combines a put and a call to lock in a price range for a security.

B. uses the gains from sale of a call to purchase a put.

C. uses the gains from sale of a put to purchase a call.

D.combines a put and a call to lock in a price range for a security and uses the gains

from sale of a call to purchase a put.

E. combines a put and a call to lock in a price range for a security and uses the gains

from sale of a put to purchase a call.

An investor who wishes to form a portfolio that lies to the right of the optimal risky

portfolio on the capital

allocation line must

A. lend some of her money at the risk-free rate.

B. borrow some money at the risk-free rate and invest in the optimal risky portfolio.

C. invest only in risky securities.

D. borrow some money at the risk-free rate, invest in the optimal risky portfolio, and

invest only in risky

securities

E. Such a portfolio cannot be formed.

Management fees and other expenses of mutual funds may include

A. front-end loads.

B. back-end loads.

C. 12b-1 charges.

D. front-end and back-end loads.

E. front-end loads, back-end loads, and 12b-1 charges.

Relative to European puts, otherwise identical American put options

A. are less valuable.

B. are more valuable.

C. are equal in value.

D. will always be exercised earlier.

E. None of the options are correct.

A U.S. dollar-denominated bond that is sold in Singapore is a(n)

A. Eurobond.

B. Yankee bond.

C. Samurai bond.

D. Bulldog bond.

When borrowing and lending at a risk-free rate are allowed, which capital allocation

line (CAL) should the

investor choose to combine with the efficient frontier?

I) The one with the highest reward-to-variability ratio.

II) The one that will maximize his utility.

III) The one with the steepest slope.

IV) The one with the lowest slope.

A. I and III

B. I and IV

C. II and IV

D. I only

E. I, II, and III

If the hedge ratio for a stock call is 0.60, the hedge ratio for a put with the same

expiration date and exercise price as the call would be

A. 0.60.

B. 0.40.

C. −0.60.

D. −0.40.

E. −0.17.

Bond analysts might be more interested in a bond’s yield to call if

A. the bond’s yield to maturity is insufficient.

B. the firm has called some of its bonds in the past.

C. the investor only plans to hold the bond until its first call date.

D. interest rates are expected to rise.

E. interest rates are expected to fall.

Consider a well-diversified portfolio, A, in a two-factor economy. The risk-free rate is

6%, the risk premium on the first factor portfolio is 4%, and the risk premium on the

second factor portfolio is 3%. If portfolio A has a beta of 1.2 on the first factor and .8 on

the second factor, what is its expected return?

A. 7.0%

B. 8.0%

C. 9.2%

D. 13.0%

E. 13.2%

What is the expected return of a zero-beta security?

A. The market rate of return

B. Zero rate of return

C. A negative rate of return

D. The risk-free rate

Given a stock index with a value of $1,500, an anticipated dividend of $62 and a

risk-free rate of 5.75%, what should be the value of one futures contract on the index?

A. $1,343.40

B. $62.00

C. $1,418.44

D. $1,524.25

Closed-end funds are frequently issued at a ______ to NAV and subsequently trade at a

__________ to NAV.

A. discount; discount

B. discount; premium

C. premium; premium

D. premium; discount

E. No consistent relationship has been observed.

A remainderman is

A. a stockbroker who remained working on Wall Street after the 1987 crash.

B. an employee of a trustee.

C. one who receives interest and dividend income from a trust during their lifetime.

D. one who receives the principal of a trust when it is dissolved.

If the yield on mortgage-backed securities was abnormally low compared to Treasury

bonds, a hedge fund pursuing a relative value strategy would

A. short sell the Treasury bonds and short sell the mortgage-backed securities.

B. short sell the Treasury bonds and buy the mortgage-backed securities.

C. buy the Treasury bonds and buy the mortgage-backed securities.

D. buy the Treasury bonds and short sell the mortgage-backed securities.

Which one of the following portfolios cannot lie on the efficient frontier as described by

Markowitz?

A. Only portfolio A cannot lie on the efficient frontier.

B. Only portfolio B cannot lie on the efficient frontier.

C. Only portfolio C cannot lie on the efficient frontier.

D. Only portfolio D cannot lie on the efficient frontier.

E. Cannot be determined from the information given.

A mutual fund had average daily assets of $4.0 billion in 2016. The fund sold $1.5

billion worth of stock and purchased $1.6 billion worth of stock during the year. The

fund’s turnover ratio is

A. 37.5%.

B. 22%.

C. 15%.

D. 45%.

E. 20%.

In the consolidation stage of the industry life cycle,

A. it is difficult to predict which firms will succeed and which firms will fail.

B. industry growth is very rapid.

C.-the performance of firms will more closely track the performance of the overall

industry.

D. it is difficult to predict which firms will succeed and which firms will fail, and

industry growth is very rapid.

E. industry growth is very rapid, and the performance of firms will more closely track

the performance of the overall industry.

The premise of behavioral finance is that

A. conventional financial theory ignores how real people make decisions and that

people make a difference.

B. conventional financial theory considers how emotional people make decisions, but

the market is driven by rational utility maximizing investors.

C. conventional financial theory should ignore how the average person makes decisions

because the market is driven by investors who are much more sophisticated than the

average person.

D. conventional financial theory considers how emotional people make decisions, but

the market is driven by rational utility maximizing investors and should ignore how the

average person makes decisions because the market is driven by investors who are

much more sophisticated than the average person.

E. None of the options are correct.

The premise of behavioral finance is that conventional financial theory ignores how real

people make decisions and that people make a difference.

The Fama and French three factor model uses ___, ___, and ___ as factors.

A. industrial production; term spread; default spread

B. industrial production; inflation; default spread

C. firm size; book to market ratio; market index

D. firm size; book to market ratio; default spread

E. None of the options are correct.

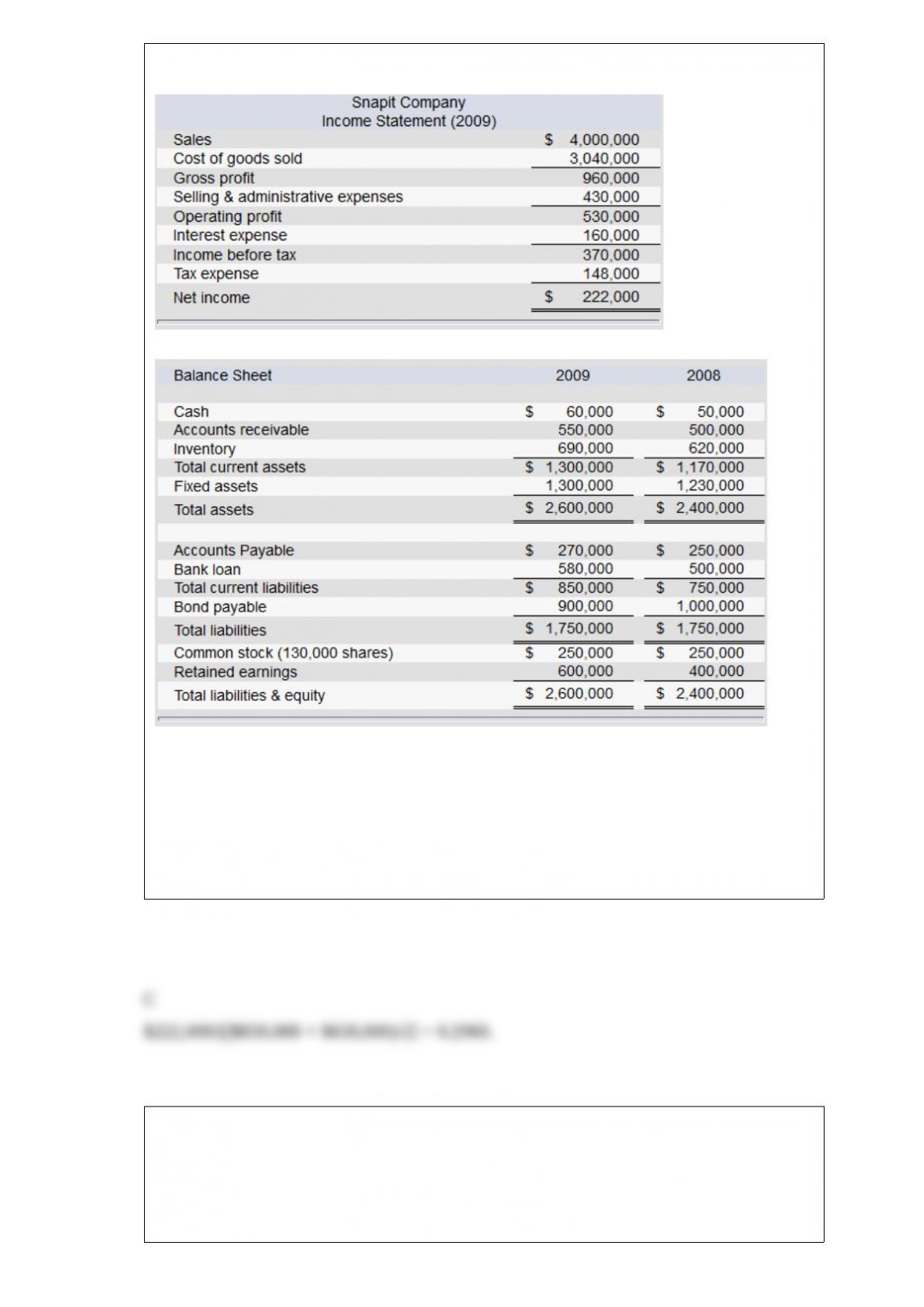

The financial statements of Snapit Company are given below.

Note: The common shares are trading in the stock market for $100 each.

Refer to the financial statements of Snapit Company. The firm’s return on equity ratio

for 2009 is

A. 0.1235.

B. 0.0296.

C. 0.2960.

D. 2.2960.

You purchased a share of CSCO stock for $20. One year later, you received $2 as a

dividend and sold the

share for $31. What was your holding-period return?

A. 45%

B. 50%

C. 60%

D. 40%

E. None of the options are correct.

A hedge fund pursuing a ______ strategy is attempting to exploit temporary

misalignments in relative pricing.

A. directional

B. nondirectional

C. stock or bond

D. arbitrage or speculation

E. None of the options are correct.

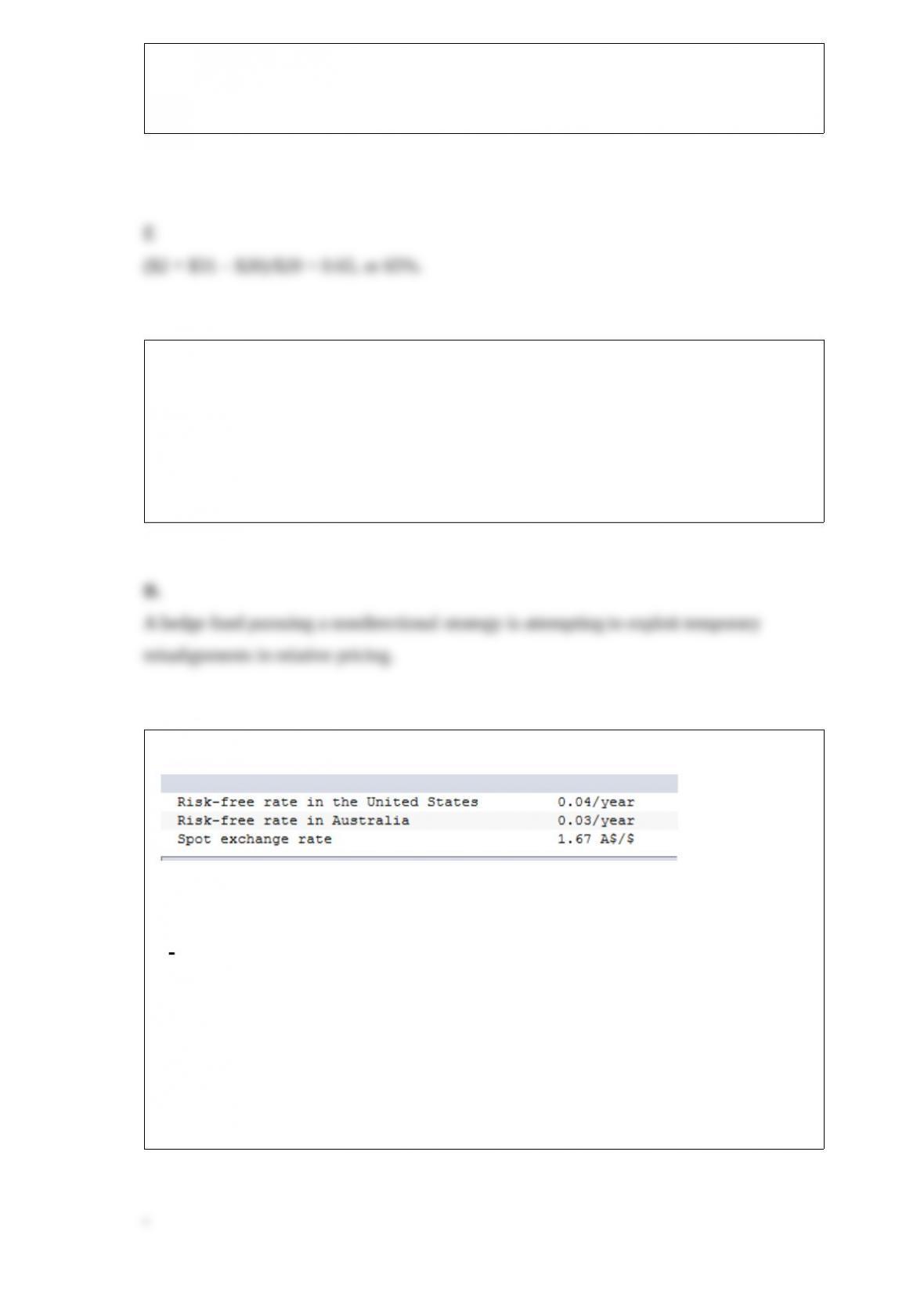

Consider the following:

If the market futures price is 1.69 A$/$, how could you arbitrage?

A. Borrow Australian dollars in Australia, convert them to dollars, lend the proceeds in

the United States, and . enter futures positions to purchase Australian dollars at the

current futures price.

B. Borrow U.S. dollars in the United States, convert them to Australian

dollars, lend the proceeds in Australia, . and enter futures positions to sell Australian

dollars at the current futures price.

C. Borrow U.S. dollars in the United States, invest them in the U.S., and enter futures

positions to purchase Australian dollars at the current futures price.

D. Borrow Australian dollars in Australia and invest them there, then convert back to

U.S. dollars at the spot price.

E. There is no arbitrage opportunity.

If a portfolio had a return of 15%, the risk-free asset return was 5%, and the standard

deviation of the portfolio’s

excess returns was 30%, the Sharpe measure would be

A. 0.20.

B. 0.35.

C. 0.45.

D. 0.33.

E. 0.25.

Rubinstein (1994) observed that the performance of the Black-Scholes model had

deteriorated in recent years, and he attributed this to

A. investor fears of another market crash.

B. higher-than-normal dividend payouts.

C. early exercise of American call options.

D. decreases in transaction costs.

E. None of the options are correct.

Consider a one-year maturity call option and a one-year put option on the same stock,

both with striking price $100. If the risk-free rate is 5%, the stock price is $103, and the

put sells for $7.50, what should be the price of the call?

A. $17.50

B.$15.26

C. $10.36

D. $12.26

E. None of the options.