Historically, the best asset for the long-term investor wanting to fend off the threats of

inflation and taxes while making his money grow has been

____.

A. stocks

B. bonds

C. money market funds

D. Treasury bills

Which of the following assets is most liquid?

A. cash equivalents

B. receivables

C. inventories

D. plant and equipment

The holding-period return on a stock was 25%. Its ending price was $18, and its

beginning price was $16. Its cash dividend must have been

_________.

A. $.25

B. $1

C. $2

D. $4

If investors are too slow to update their beliefs about a stock’s future performance when

new evidence arises, they are exhibiting _______.

A. representativeness bias

B. framing error

C. conservatism

D. memory bias

Exercise prices for listed stock options usually occur in increments of ____ and bracket

the current stock price.

A. $1

B. $5

C. $20

D. $25

The ________ is equal to the square root of the systematic variance divided by the total

variance.

A. covariance

B. correlation coefficient

C. standard deviation

D. reward-to-variability ratio

A firm purchases goods on credit worth $90. The same firm pays off $100 in old credit

purchases. An investment is made via the purchase of a new facility, and equity is

issued in the amount of $180 to pay for the purchase. What is the change in net cash

provided by investments?

A. $10 decrease

B. $90 decrease

C. $180 decrease

D. $190 decrease

When a company sets up a defined contribution pension plan, the __________ bears all

the risk and the __________ receives all the return from the plan’s assets.

A. employee; employee

B. employee; employer

C. employer; employee

D. employer; employer

Assuming all other factors remain unchanged, __________ would increase a firm’s

price-earnings ratio.

A. an increase in the dividend payout ratio

B. a reduction in investor risk aversion

C. an expected increase in the level of inflation

D. an increase in the yield on Treasury bills

You manage a $15 million hedge fund portfolio with beta = 1.2 and alpha = 2% per

quarter. Assume the risk-free rate is 2% per quarter and the current value of the S&P

500 Index is 1,200. You want to exploit the positive alpha, but you are afraid that the

stock market may fall and you want to hedge your portfolio by selling 3-month S&P

500 future contracts. The S&P contract multiplier is $250.

How much is the portfolio expected to be worth 3 months from now?

A. $15,000,000

B. $15,450,000

C. $15,600,000

D. $16,000,000

A red herring becomes a prospectus when ____.

A. the preliminary registration statement is approved by the SEC

B. the IPO is complete

C. the offering is seasoned

D. the lockup period expires

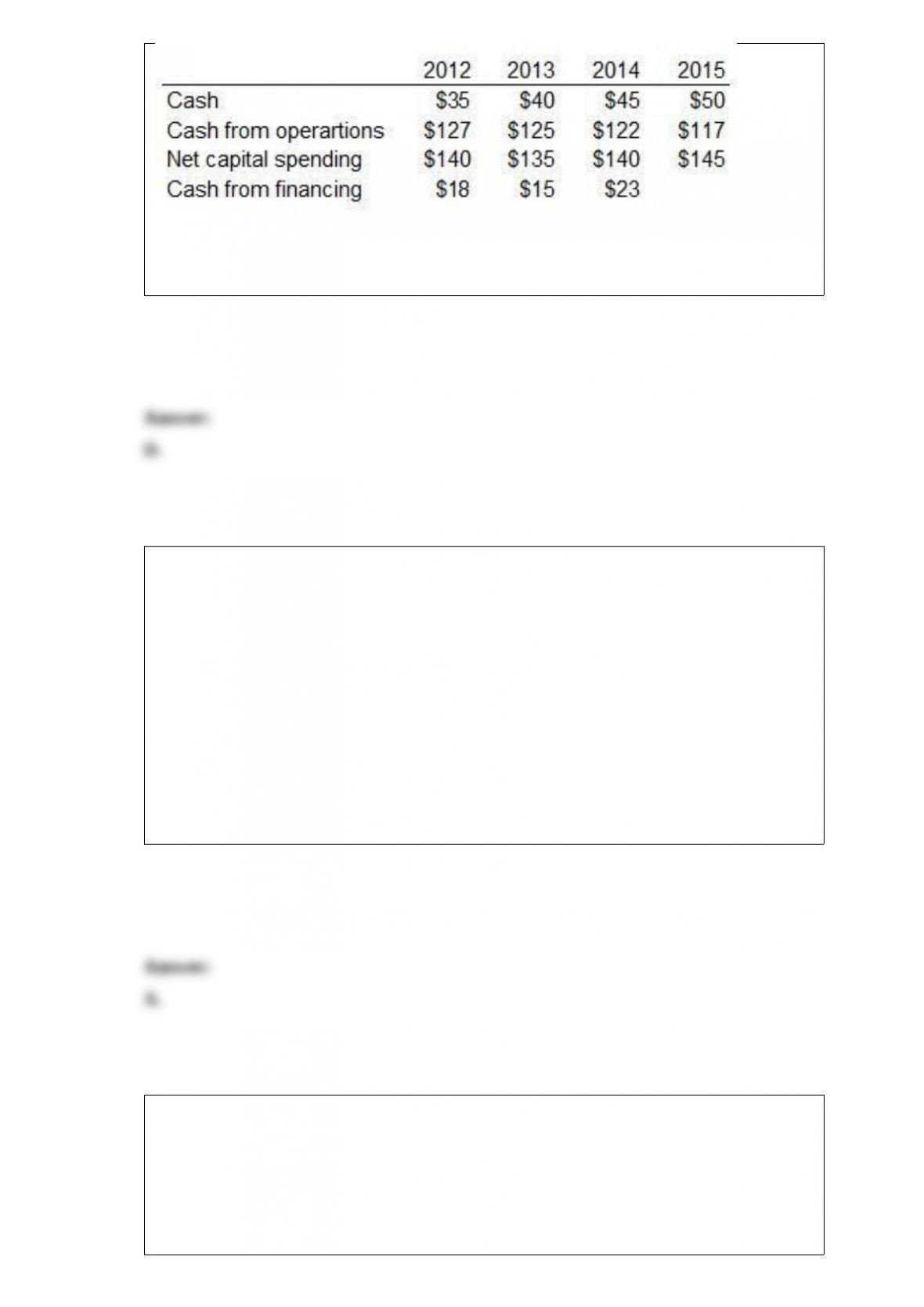

Cash Flow Data for Interceptors, Inc.

What must cash flow from financing have been in 2008 for Interceptors, Inc.?

A. $5

B. $28

C. $30

D. $33

You calculate the Black-Scholes value of a call option as $3.50 for a stock that does not

pay dividends, but the actual call price is $3.75. The most likely explanation for the

discrepancy is that either the option is _________ or the volatility you input into the

model is too _________.

A. overvalued and should be written; low

B. undervalued and should be written; low

C. overvalued and should be purchased; high

D. undervalued and should be purchased; high

The common stock of the Avalon Corporation has been trading in a narrow range

around $40 per share for months, and you believe it is going to stay in that range for the

next 3 months. The price of a 3-month put option with an exercise price of $40 is $3,

and a call with the same expiration date and exercise price sells for $4.

How can you create a position involving a put, a call, and riskless lending that would

have the same payoff structure as the stock at expiration?

A. Buy the call, sell the put; lend the present value of $40.

B. Sell the call, buy the put; lend the present value of $40.

C. Buy the call, sell the put; borrow the present value of $40.

D. Sell the call, buy the put; borrow the present value of $40.

A worker plans to retire in 30 years. He hopes to receive $65,000 per year in retirement

income. If inflation is forecast at 2.5% per year, what annual income should he plan to

receive in the first year of retirement in order to maintain the purchasing power on

$65,000?

A. $65,000

B. $76,159

C. $98,398

D. $136,342

The cumulative tally of the number of advancing stocks minus declining stocks is called

the ______________.

A. market breadth

B. market volume

C. trin ratio

D. relative strength ratio

Statistics show that life expectancy at age 66 for males is about _____ additional years

and for females is about _____ additional years.

A. 15; 20

B. 16; 19

C. 18; 22

D. 19; 24

The two-factor model on a stock provides a risk premium for exposure to market risk of

9%, a risk premium for exposure to interest rate risk of (-1.3%), and a risk-free rate of

3.5%. The beta for exposure to market risk is 1, and the beta for exposure to interest

rate risk is also 1. What is the expected return on the stock?

A. 8.7%

B. 11.2%

C. 13.8%

D. 15.2%

Which of the following set of conditions will result in a bond with the greatest price

volatility?

A. a high coupon and a short maturity

B. a high coupon and a long maturity

C. a low coupon and a short maturity

D. a low coupon and a long maturity

In 1980 the dollar-yen exchange rate was about $.0045. In 2012 the yen-dollar

exchange rate was about 80 yen per dollar. A Japanese producer would have had to

increase the dollar price of a good sold in the United States by approximately _____ to

maintain the same yen price in 2012.

A. 178%

B. 79.5%

C. 265.4%

D. 36%

An investor who goes long in a futures contract will _____ any increase in value of the

underlying asset and will _____ any decrease in value in the underlying asset.

A. pay; pay

B. pay; receive

C. receive; pay

D. receive; receive

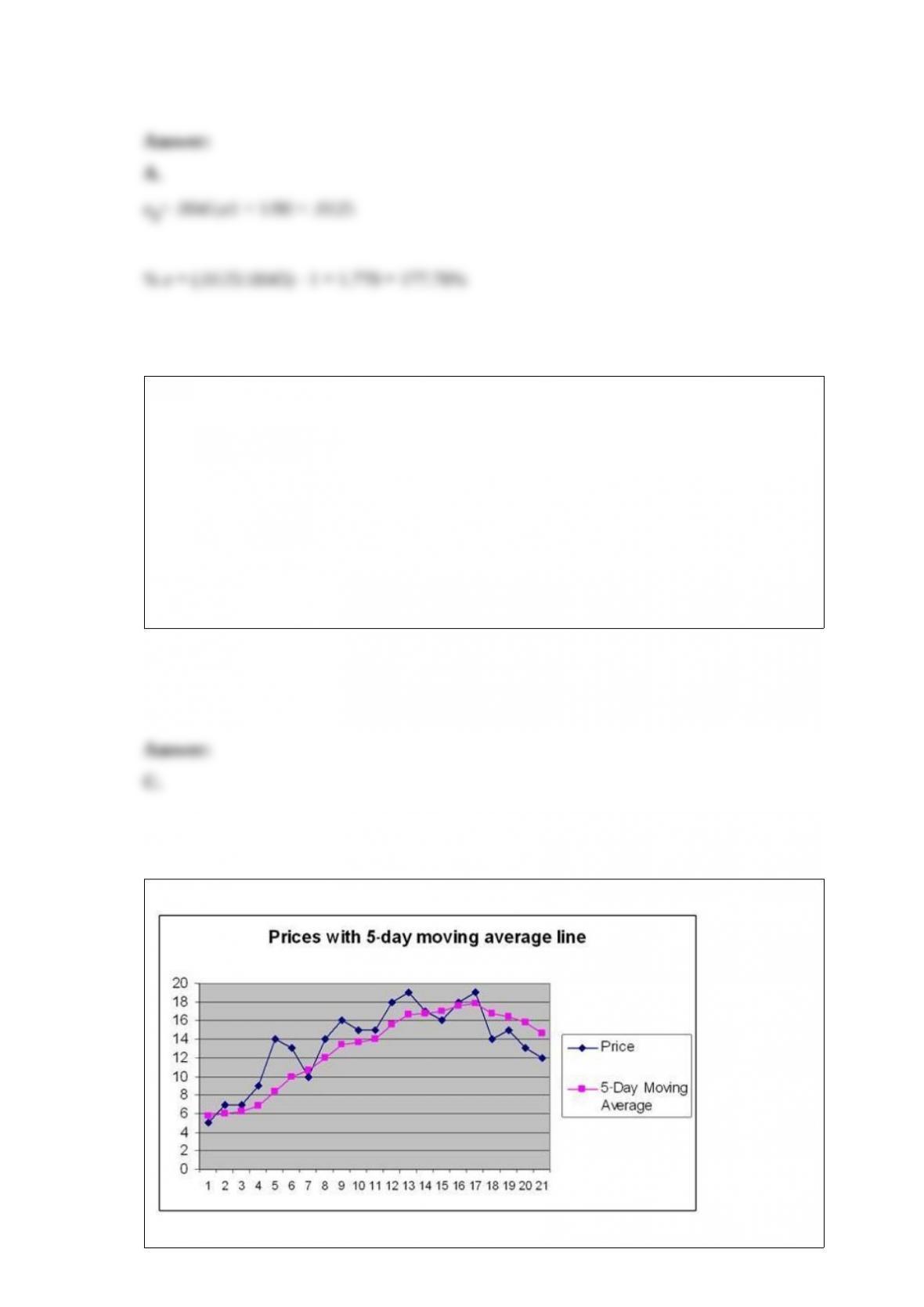

The

moving average generates buy signal(s) _____.

A. on days 3, 11, and 15

B. on days 2 and 16

C. on days 5, 9, and 13

D. on no days

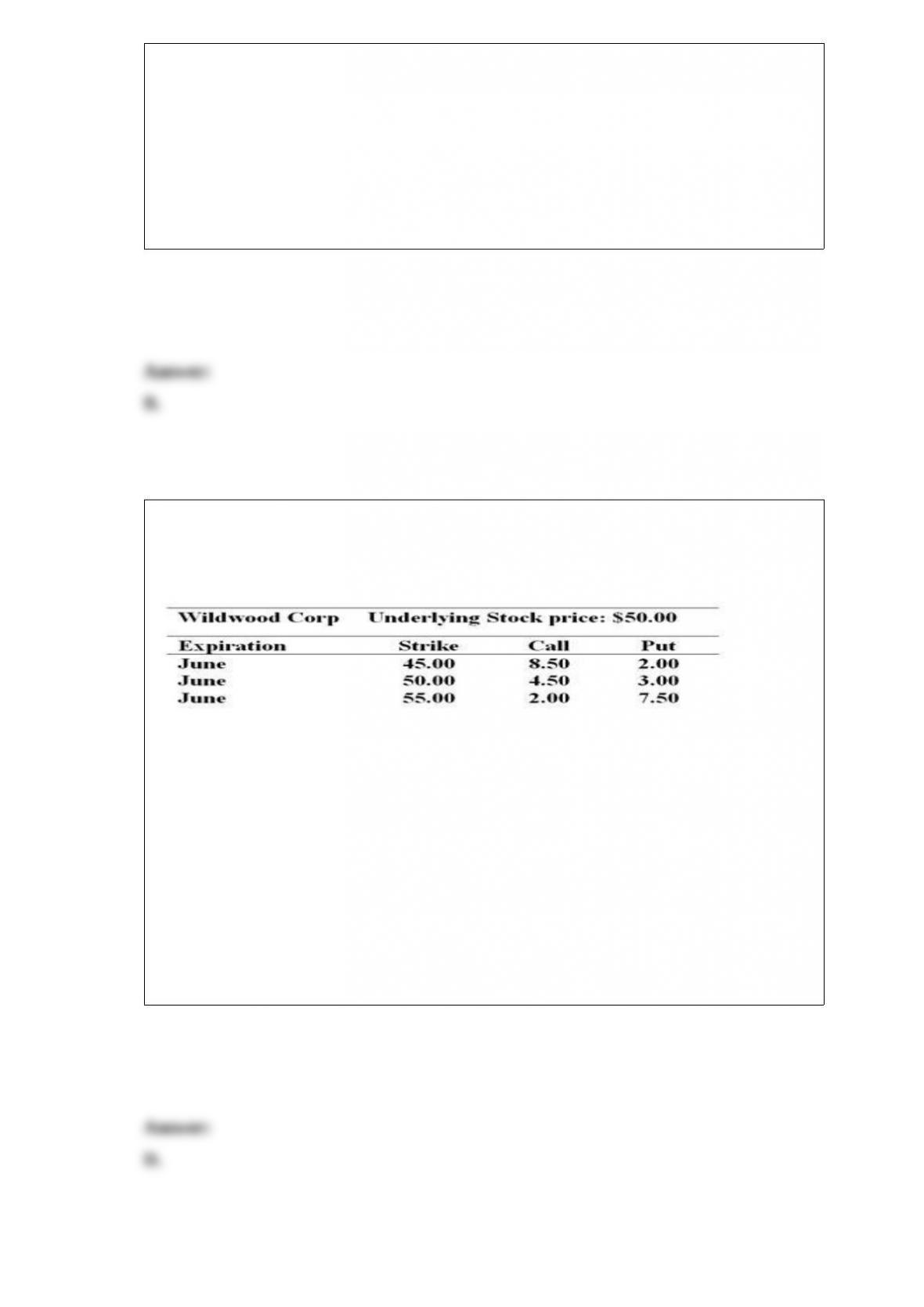

You are cautiously bullish on the common stock of the Wildwood Corporation over the

next several months. The current price of the stock is $50 per share. You want to

establish a bullish money spread to help limit the cost of your option position. You find

the following option quotes:

Suppose you establish a bullish money spread with the puts. In June the stock’s price

turns out to be $52. Ignoring commissions, the net profit on your position is

_______________.

A. $500

B. $700

C. $200

D. $250

The delta of a put option on a stock is always __________.

A. between 0 and -1

B. between -1 and 1

C. positive but less than 1

D. greater than 1

A stock has an intrinsic value of $15 and an actual stock price of $13.50. You know that

this stock ________.

A. has a Tobin’s q value < 1

B. will generate a positive alpha

C. has an expected return less than its required return

D. has a beta > 1

Which of the following correlation coefficients will produce the most diversification

benefits?

A. -.6

B. -.9

C. 0

D. .4

The fact that the U.S. government provides deposit insurance to banks creates a form of

___________, which is at least partially offset by requiring banks to hold more capital

if they are riskier.

A. moral hazard

B. adverse selection

C. risk aversion

D. interest rate risk

The Hydro Index is a price weighted stock index based on the 5 largest boat

manufacturers in the nation. The stock prices for the five stocks are $10, $20, $80, $50

and $40. The price of the last stock was just split 2 for 1 and the stock price was halved

from $40 to $20. What is the new divisor for a price weighted index?

A. 5.00

B. 4.85

C. 4.50

D. 4.75

Which of the following is not a liquidity ratio?

A. inventory turnover ratio

B. current ratio

C. quick ratio

D. cash ratio

The yield to maturity on a bond is:

I. Above the coupon rate when the bond sells at a discount and below the coupon rate

when the bond sells at a premium II. The discount rate that will set the present value of

the payments equal to the bond price

III. Equal to the true compound return on investment only if all interest payments

received are reinvested at the yield to maturity

A. I only

B. II only

C. I and II only

D. I, II, and III

Higher returns of equity hedge funds as compared to the S&P 500 Index reflect positive

compensation for __________ risk.

A. market

B. liquidity

C. systematic

D. interest rate

The expected return on the market is the risk-free rate plus the _____________.

A. diversified returns

B. equilibrium risk premium

C. historical market return

D. unsystematic return