The advantage to the lender (purchaser) of a Brady bond versus a loan to a foreign

country is that U.S. Treasury bonds serve as collateral for Brady bonds.

Answer:

An FI that sells a loan with recourse retains ownership of the loan.

Answer:

Wholesale loans are loan agreements between corporations and their customers at

reduced interest rates.

Answer:

The Commodity Futures Trading Commission (CFTC) has jurisdiction over swaps.

Answer:

Because investment banks typically buy and sell securities on a regular basis; they have

no need for a liability management plan.

Answer:

In the event of a bank run, depositor claims on the bank are satisfied on a pro rata

basis.

Answer:

U.S. pension funds invest approximately one percent (1%) of their portfolios in foreign

securities.

Answer:

A positive repricing gap implies that a decrease in interest rates will cause interest

expense to decrease more than the decrease in interest income.

Answer:

Noninterest expense has increased faster than interest expense for all U.S. insured

commercial banks in recent years.

Answer:

Which of the following statements is TRUE?A. The optimal duration gap is zero.

B. Duration gap measures the impact of changes in interest rates on the market value of

equity.

C. The shorter the maturity of the FI’s securities, the greater the FI’s interest rate risk

exposure.

D. The duration of all floating rate debt instruments is equal to the time to maturity.

E. The duration of equity is equal to the duration of assets minus the duration of

liabilities.

Answer:

Interest rate parity implies that the discounted spread between interest rates in two

currencies should equal the percentage spread between forward and spot exchange

rates.

Answer:

Full amortization of a thirty-year fixed rate mortgage means that monthly payments are

equal and include both principal and interest.

Answer:

Insured depositors can be covered for more than $250,000 at any given FI under current

FDIC regulations.

Answer:

Short-term mutual funds invest solely in tax-exempt securities.

Answer:

The payoff on a catastrophe futures contract is adjusted for the actual loss ratio of the

insurer.

Answer:

Currently in the U.S., deposit insurance premiums increase with the amount of risk of

the institution.

Answer:

Which of the following statements is TRUE?A. Closed-end funds issue an unlimited

number of shares as liabilities.

B. Open-end funds supply limited number of shares to investors.

C. Open-end funds need not stand ready to buy back previously issued shares from

investors at the current market price for the fund’s shares.

D. At a given market price, the supply of open-end fund shares is perfectly inelastic.

E. The number of outstanding shares of a closed-ended fund may change when the

issuing fund chooses to repurchase them.

Answer:

If not done by FIs, the process of monitoring the actions of borrowers would reduce the

attractiveness and increase the risk of investing in corporate debt and equity by

individuals.

Answer:

Mutual funds are financial intermediaries that invest in diversified portfolios of assets.

Answer:

A pure credit swap will reduce interest rate risk.

Answer:

Matching the maturities of assets and liabilities is not a perfect method of immunizing

the balance sheet because the timing of the cash flows is likely to differ between the

assets and liabilities.

Answer:

The establishment of minimum required reserves by regulators is a method of

extracting taxes from FIs.

Answer:

A major advantage of discriminant models is the stability of the coefficient weights

over time.

Answer:

The negotiable instrument characteristic of large wholesale CDs effectively eliminates

the adverse withdrawal risk for the bank.

Answer:

A change from commercial bank deposits to money market mutual funds typically

allows an investor to benefit from higher yields, but with the cost of losing deposit

insurance coverage.

Answer:

The Financial Services Modernization Act of 1999 has provided for more standardized

relationships among financial service sectors and commerce.

Answer:

The advantage to a lender in a repurchase agreement transaction versus a fed funds sale

is the collateral of government securities or other acceptable liquid assets provided by

the borrowing FI.

Answer:

The availability of a liquid secondary market for asset-backed securities provided an

incentive for FIs to follow an originate-to-distribute strategy of loan origination.

Answer:

Moral hazard provides an incentive for bank owners to accept greater asset risks

because they have less to lose, and potentially more to gain.

Answer:

Daily earnings at risk (DEAR) is defined as the dollar value of a position times price

sensitivity.

Answer:

The fastest growing group of swaps in recent years has been those designed to help FIs

manage interest rate risk.

Answer:

Securitization of assets increases the FI’s capital requirements.

Answer:

The growth in off-balance-sheet activities during the decade of the 1990s was due, in

large part, to the use of derivative contracts.

Answer:

Duration is the weighted-average present value of the cash flows using the timing of the

cash flows as weights.

Answer:

Which of the following shows the change in the value of a put option for each $1

change in the underlying bond? A. Open interest.

B. Volatility.

C. Delta.

D. Basis.

E. Sigma.

Answer:

What is this bank’s interest rate risk exposure, if any? A. The bank is exposed to

decreasing interest rates because it has a negative duration gap of -0.21 years.

B. The bank is exposed to increasing interest rates because it has a negative duration

gap of -0.21 years.

C. The bank is exposed to increasing interest rates because it has a positive duration

gap of +0.21 years.

D. The bank is exposed to decreasing interest rates because it has a positive duration

gap of +0.21 years.

E. The bank is not exposed to interest rate changes since it is running a matched book.

Answer:

Consider a five-year, 8 percent annual coupon bond selling at par of $1,000.

What is the duration of this bond?A. 5 years.

B. 4.31 years.

C. 3.96 years.

D. 5.07 years.

E. Not enough information to answer.

Answer:

What is the FI’s net exposure in the Japanese yen? A. +30,000.

B. +40,600.

C. -19,400.

D. -40,600.

E. +20,600.

Answer:

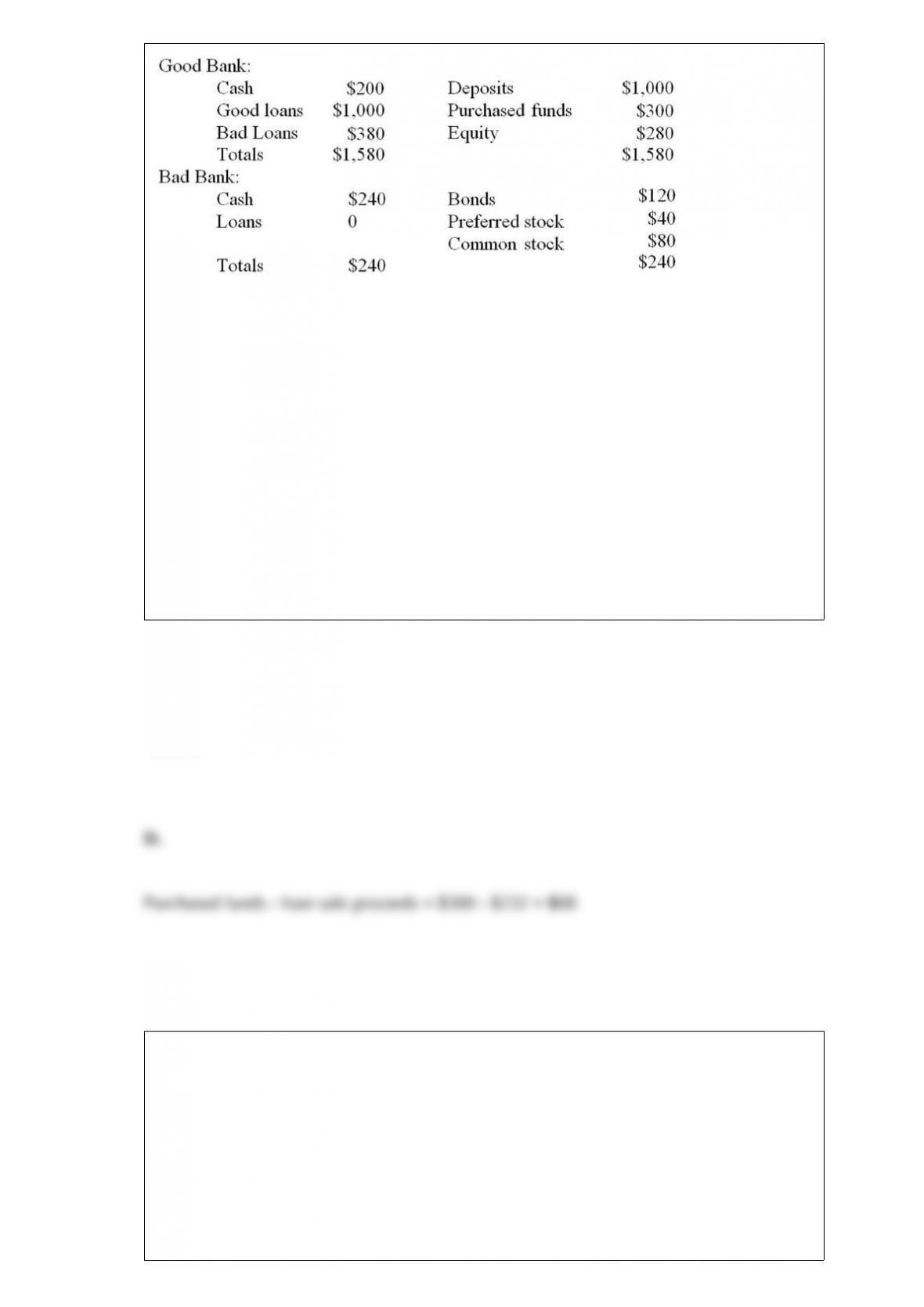

Bad Bank buys the bad loans for $232. The proceeds of the loan sale are used by Good

Bank to pay off purchased funds.

If the proceeds of the loan sale are used to pay off purchased funds, what will be the

balance of the purchased funds for Good Bank after the transaction? A. $1,200.

B. $232.

C. $132.

D. $68.

E. $0.

Answer:

To measure market risk at the 1 percent level of risk, what is the the scaling factor for

the value at risk (VAR) and the expected shortfall (ES) respectively?A. 2.33 and 2.665

B. 1.65 and 2.063

C. 1.65 and 2.665

D. 2.33 and 2.063

E. none of the above is the correct scaling factor.

Answer:

Which of the following is NOT a reason that a swap may have less credit risk than an

individual loan? A. Netting of payments.

B. Payment flows are interest and not principal.

C. Standby letters of credit are available.

D. Swaps can be cancelled, individual loans cannot.

E. None of the above.

Answer:

What are the possible ways that the bank can meet an expected net deposit drain of +4

percent using stored liquidity management techniques? A. Liquidate all cash holdings.

B. Utilize further the Fed funds market.

C. Liquidate some securities and/or loans.

D. Liquidate all cash and use more Fed funds.

E. All of the above are suitable techniques.

Answer:

The risk that an FI may not have enough capital to offset a sudden decline in the value

of its assets relative to its liabilities is referred to as A. currency risk.

B. sovereign risk.

C. insolvency risk.

D. liquidity risk.

E. interest rate risk.

Answer:

Which of the following assets is deducted from Common Equity Tier I capital? A.

Trademarks.

B. Goodwill.

C. Patents.

D. Bank premises.

E. None of the above.

Answer:

What should be the price of a three-year 6 percent floor if the current (spot) rates are

also 6 percent? The face value is $5,000,000, and time periods are zero, one, and two.

A. $44,060.

B. $66,030.

C. $22,462.

D. $21,598.

E. $25,000.

Answer:

A risk manager could restructure assets and liabilities to reduce interest rate exposure

for this example by A. increasing the average duration of its assets to 9.56 years.

B. decreasing the average duration of its assets to 4.00 years.

C. increasing the average duration of its liabilities to 6.78 years.

D. increasing the average duration of its liabilities to 9.782 years.

E. increasing the leverage ratio, k, to 1.

Answer:

Which of the following 2 firms survived as investment banks following the most recent

financial crisis? A. Morgan Stanley and Bear Stearns.

B. Goldman Sachs and Merrill Lynch.

C. Lehman Brothers and Morgan Stanley.

D. Merrill Lynch and Lehman Brothers.

E. None of the above.

Answer:

Any model that seeks to estimate an efficient frontier for loans, and thus the optimal

proportions in which to hold loans made to different borrowers, needs to determine and

measure the A. expected return on each loan to a borrower.

B. risk of each loan made to a borrower.

C. correlation of default risks between loans made to borrowers.

D. expected return of the entire loan portfolio

E. All of the above.

Answer:

Which of the following might lead a consumer to seek a loan from a subprime lender?

A. Inability to document their income.

B. Have previously filed for bankruptcy.

C. Has never had a loan before.

D. Lack of savings for a down payment.

E. All of the above.

Answer:

How can noninterest operating expenses of an FI be reduced by improved technological

efficiency? A. By improving the efficiency of management of information flows.

B. By obtaining access to low cost sources of funds.

C. By linking services to the quality of the FI’s technology.

D. By innovating new interest earning products.

E. By complying with all government regulations.

Answer:

The following information is for a collateralized mortgage obligation (CMO). Tranche

A has a face value of $110 million and pays 5 percent annually. Tranche B has a face

value of $90 million and pays 7 percent annually.

What are the annual coupon payments promised to each tranche? (Assume no

prepayments and non-amortization of principal.) A. $5.5 million on Tranche A and $6.3

million on Tranche B.

B. $5.5 million on Tranche B and $6.3 million on Tranche A.

C. A total of $12 million on both Tranche A and B.

D. $4.5 million on Tranche A and $7.7 million on Tranche B.

E. $4.5 million on Tranche B and $7.7 million on Tranche A.

Answer:

During 2006, originations of new subprime mortgages totaled approximately

__________, which was ________ of new mortgages originated that year. A. $600

billion; one-fifth

B. $400 billion; one-tenth

C. $100 billion; one-half

D. $400 billion; one-third

E. $600 billion; one-half

Answer:

Which type of financial intermediary is more highly exposed to liquidity risk? A.

Property-casualty insurance companies.

B. Life insurance companies.

C. Mutual funds.

D. Depository institutions.

E. Pension funds.

Answer:

Which of the following is NOT included as high-quality liquid assets when computing a

liquidity coverage ratio? A. Sovereign debt.

B. Bank capital.

C. Government guaranteed mortgage-backed securities.

D. Central bank reserves.

E. Cash.

Answer:

What type of risk focuses upon mismatched asset and liability maturities and durations?

A. Liquidity risk.

B. Interest rate risk.

C. Credit risk.

D. Foreign exchange rate risk.

E. Off-balance sheet risk.

Answer:

The average duration of the loans is 10 years. The average duration of the deposits is 3

years.

What is the leveraged-adjusted duration gap of the bank’s portfolio? A. 10 years.

B. 7.3 years.

C. 7 years.

D. 7.18 years.

E. 3 years.

Answer:

What is the market’s Herfindahl Hirschman Index (HHI)? A. 4,688.

B. 3,600.

C. 548.

D. 8.

E. 0.

Answer:

Which of the following is most typical of broker-dealers? A. They assist in

underwriting of new securities.

B. They assist in trading of existing securities.

C. They assist in issuing new securities.

D. They assist in underwriting and distribution of new securities.

E. All of the above.

Answer:

Customer deposits are classified on a DI’s balance sheet as A. assets, because the DI

uses deposit funds to earn profits.

B. liabilities, because the DI uses deposits as a source of funds.

C. assets, because customers view deposits as assets.

D. liabilities, because the DI must meet reserve requirements on customer deposits.

E. liabilities, because DIs are required to serve depositors.

Answer:

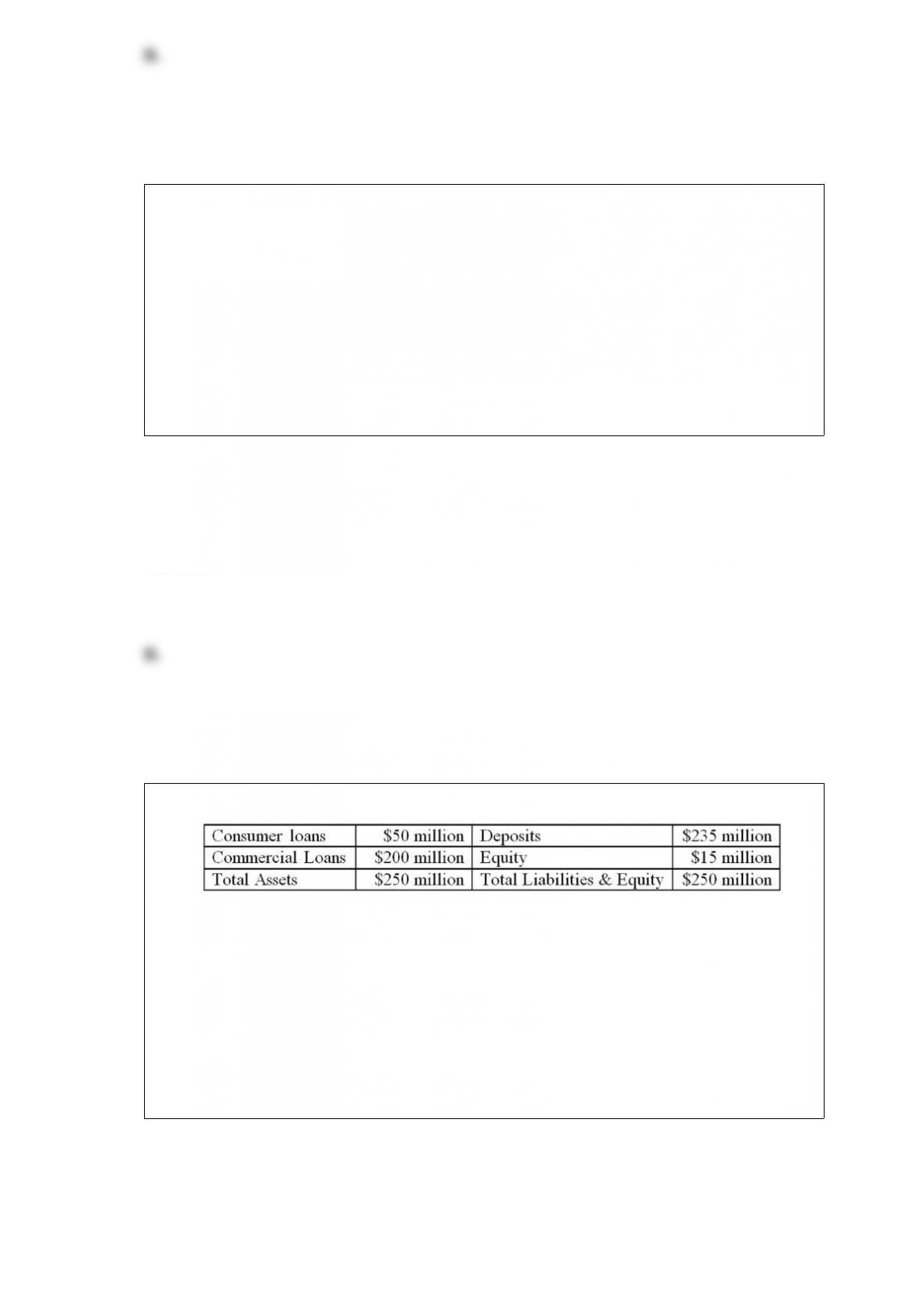

Given that 25 percent of the loans have been identified as problem loans, and if

historical cost accounting methods allow the bank to write down only 10 percent of the

problem loans, what will be the book value of capital? A. $35 million.

B. -$155 million.

C. $16 million.

D. -$7 million.

E. $0.

Answer:

What is a swap?A. An agreement between two parties to exchange assets or a series of

cash flows for a specific period of time at a specified interval.

B. An agreement between a buyer and a seller at time 0 to exchange a nonstandardized

asset for cash at some future date.

C. A contract that gives the holder the right, but not the obligation to buy or sell the

underlying asset at a specified price within a specified period of time.

D. Trading in securities prior to their actual issue.

E. Contractual commitment to make a loan up to a stated amount at a given interest

rate in the future.

Answer:

The primary function of insurance companies is toA. generate fees for the banks that

sell insurance products.

B. sell a variety of consumer investment products.

C. protect policyholders from adverse events.

D. assist in the transfer of wealth into the future.

E. provide contracts that encourage policyholders to save current income.

Answer:

How many institutions are currently listed as Global Systematically Important Banks

(G-SIBs)? A. 12.

B. 18.

C. 29.

D. 32.

E. 35.

Answer:

Nonbank institutions have NOT gained competitive momentum for which of the

following financial products? A. Commercial paper.

B. Money market mutual funds.

C. Annuities.

D. Business credit market.

E. Savings accounts.

Answer:

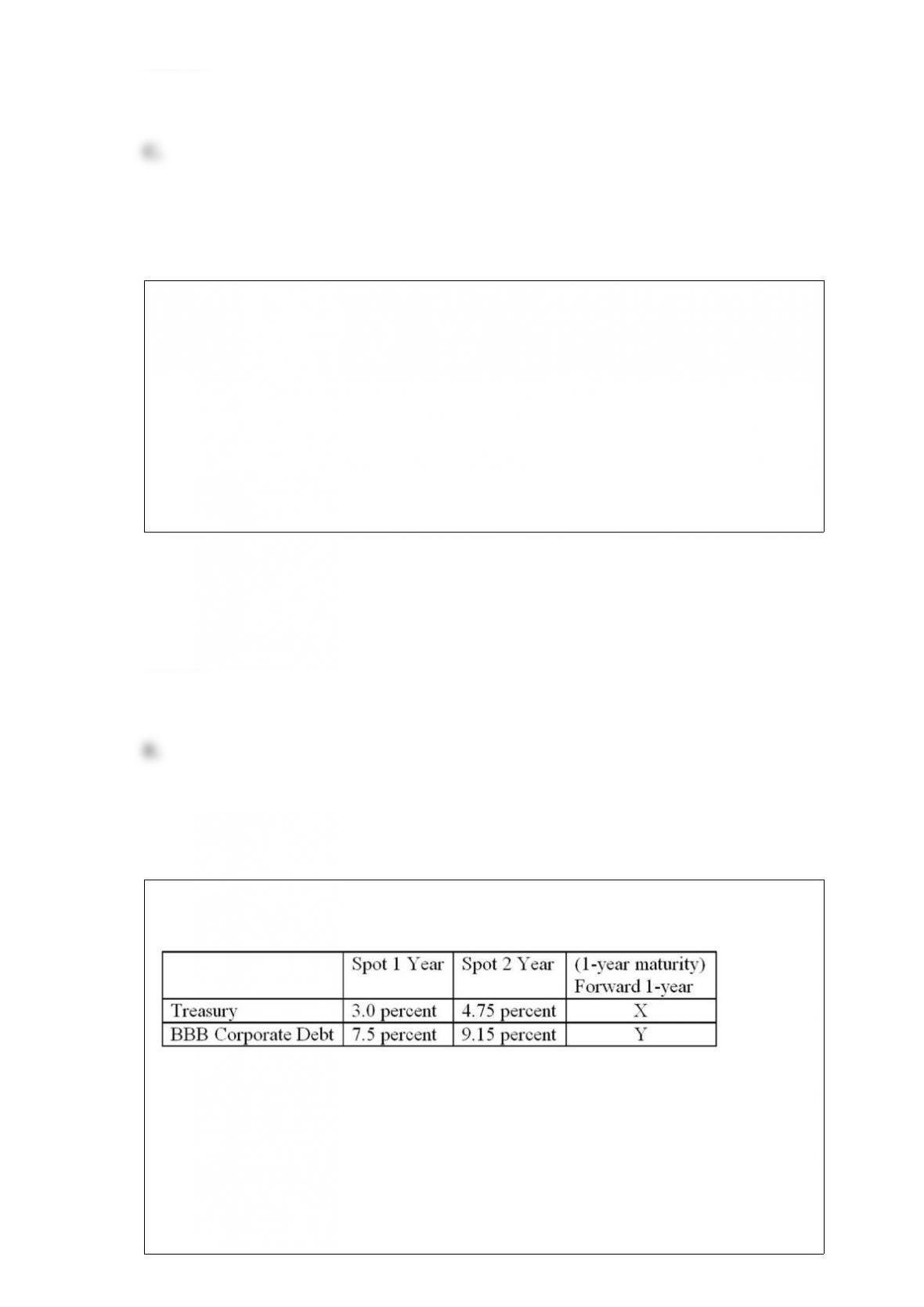

The following is information on current spot and forward term structures (assume the

corporate debt pays interest annually):

Calculate

the value of x (the implied forward rate on one-year maturity Treasuries to be delivered

in one year). A. 6.53 percent.

B. 10.83 percent.

C. 5.75 percent.

D. 6.925 percent.

E. 1.017 percent.

Answer: