1) for european currency options written on euro with a strike price in dollars, what of

the effect of an increase in r$ relative to r?

a.decrease the value of calls and puts ceteris paribus

b.increase the value of calls and puts ceteris paribus

c.decrease the value of calls, increase the value of puts ceteris paribus

d.increase the value of calls, decrease the value of puts ceteris paribus

2) assume the time from acceptance to maturity on a $4,000,000 banker’s acceptance is

180 days. further assume that the importing bank’s acceptance commission is 1.25

percent and that the market rate for 90-day b/as is 3.0 percent. calculate the amount the

exporter will receive if he discounts the b/a with the importer’s bank.

a.$3,993,750

b.$3,915,000

c.$3,975,000

d.$3,009,375

3) publicly traded yankee bonds must

a.meet the same regulations as u.s. domestic bonds

b.meet the same regulations as eurobonds if sold to europeans

c.meet the same regulations as samurai bonds if sold to japanese

d.none of the above

4) floating-rate notes (frn)

a.experience very volatile price changes between reset dates

b.are typically medium-term bonds with coupon payments indexed to some reference

rate (e.g. libor)

c.appeal to investors with strong need to preserve the principal value of the investment

should they need to liquidate prior to the maturity of the bonds

d.both b and c

5) the volume of otc currency options trading is

a.much smaller than that of organized-exchange currency option trading

b.much larger than that of organized-exchange currency option trading

c.larger, because the exchanges are only repackaging otc options for their customers

d.none of the above

6) adler and simon (1986) examined the exposure of a sample of foreign equity and

bond index returns to exchange rate changes. they found that

a.changes in exchange rates generally explained a smaller portion of the variability of

foreign bond indexes than foreign equity indexes

b.changes in exchange rates generally explained none of the variability of foreign bond

indexes but completely explained the variability in foreign equity indexes

c.changes in exchange rates generally explained a larger portion of the variability of

foreign equity indexes than foreign bond indexes

d.changes in exchange rates generally explained a larger portion of the variability of

foreign bond indexes than foreign equity indexes

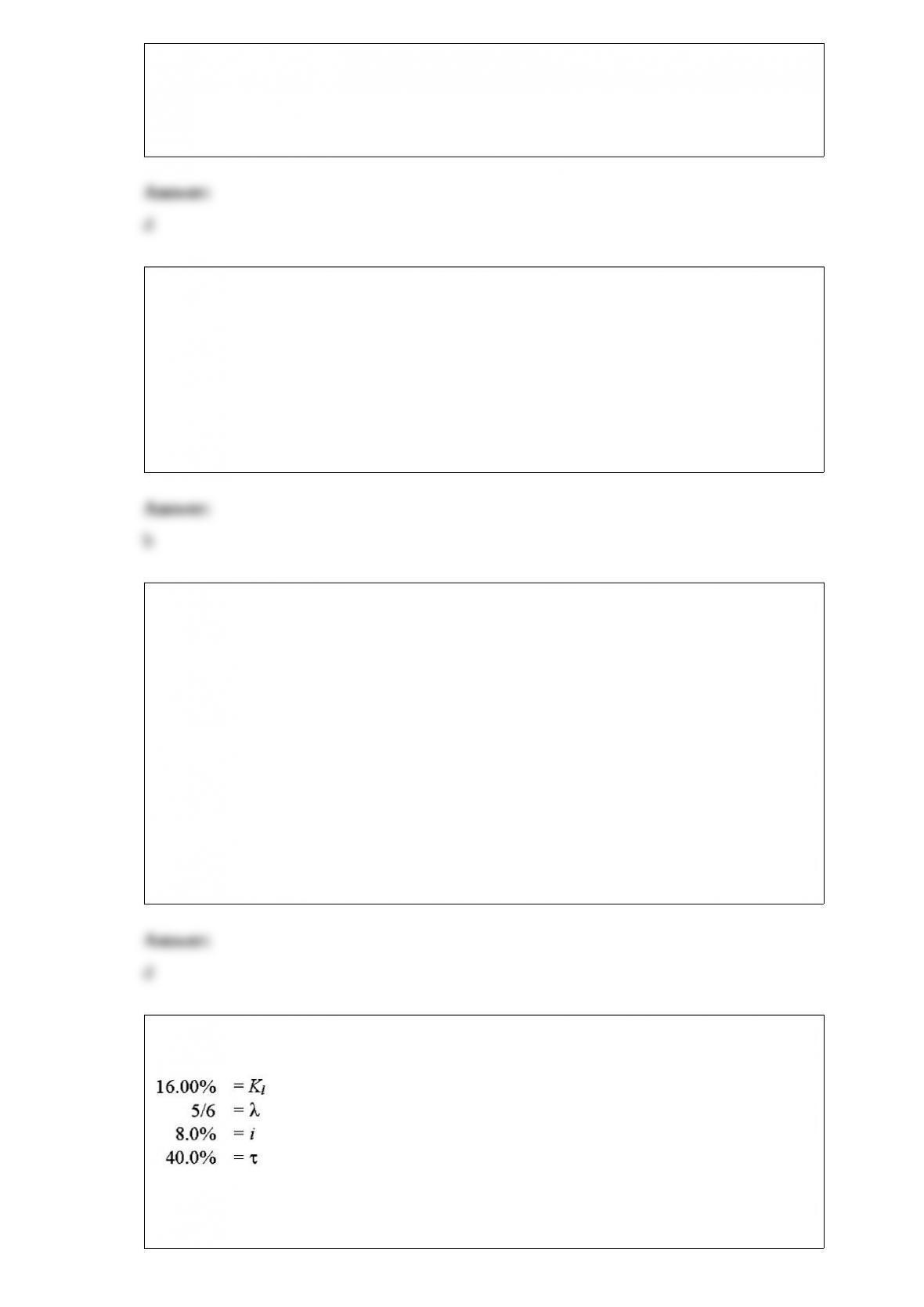

7) solve for the weighted average cost of capital:

a.7.00%

b.6.89%

c.6.73%

d.6.67%

e.6.57%

8) recently, financial markets have become highly integrated. this development

a.allows investors to diversify their portfolios internationally

b.allows minority investors to buy and sell stocks

c.has increased the cost of capital for firms

d.answers a and c are both correct

9) when an interest-only swap is established on an amortizing basis

a.the debt service exchanges decrease periodically through time as the hypothetical

notational principal is amortized

b.the debt service exchanges are the same each year, but the level of interest and

principal changes as the loans amortize

c.there is no such thing as an amortizing interest-only swap

d.none of the above

10) swap transactions

a.involve the simultaneous sale (or purchase) of spot foreign exchange against a

forward purchase (or sale) of approximately an equal amount of the foreign currency

b.account for about half of interbank fx trading

c.involve trades of one foreign currency for another without going through the u.s.

dollar

d.all of the above

11) with any successful hedge

a.you are guaranteed to lose money on one side

b.you can avoid the accounting ramifications of a loss on one side by keeping it off the

books

c.both a and b

d.none of the above

12) the financial manager’s responsibility involves

a.increasing the per share price of the company’s stock at any cost and by any means,

ways and fashion that is possible

b.the shareholder wealth maximization

c.which capital projects to select

d.both b and c

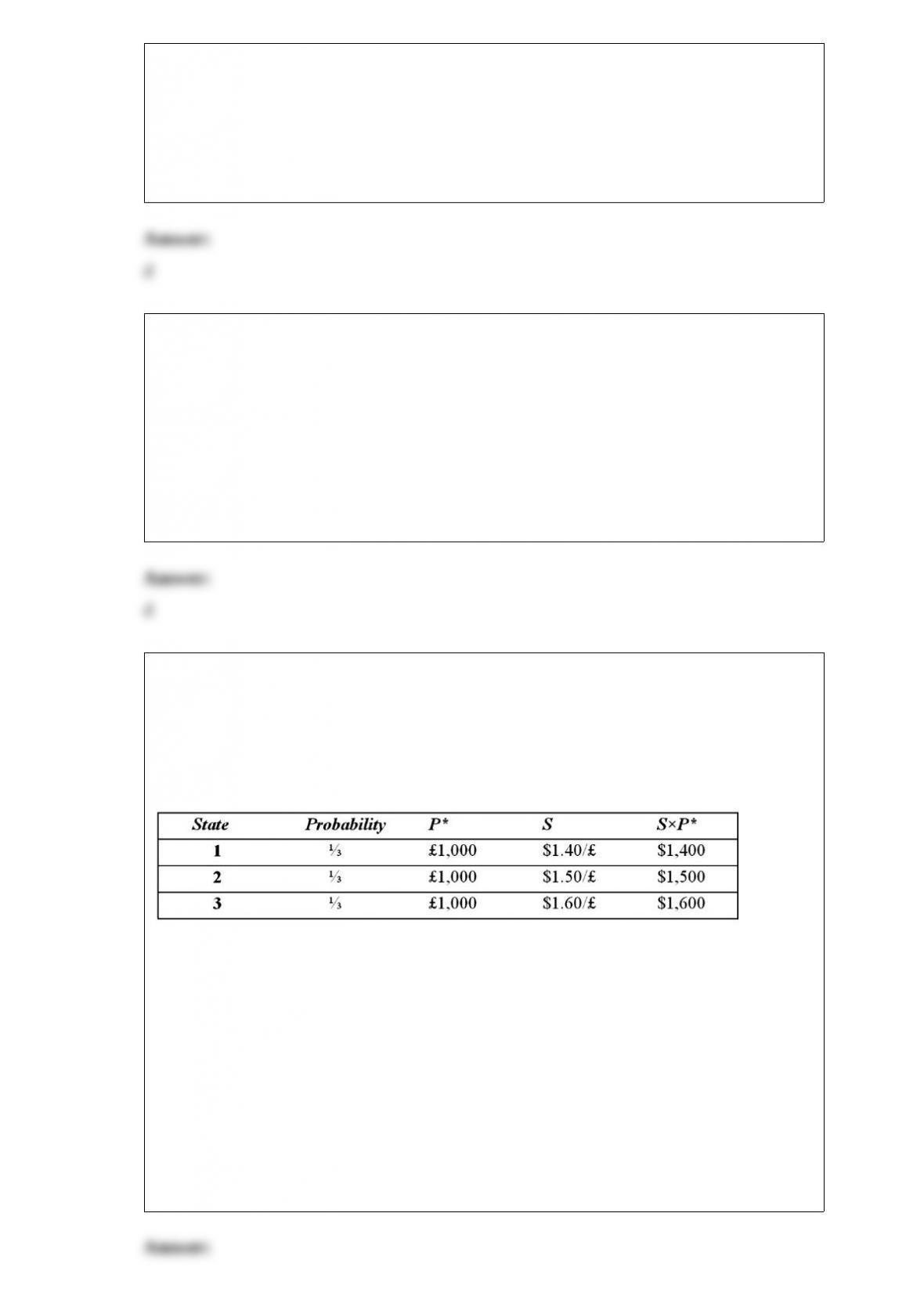

13) suppose a u.s. firm has an asset in britain whose local currency price is random. for

simplicity, suppose there are only three states of the world and each state is equally

likely to occur. the future local currency price of this british asset (p*) as well as the

future exchange rate (s) will be determined, depending on the realized state of the

world.

which of the following statements is most correct?

a.the firm faces no exchange rate risk since the local currency price of the asset and the

exchange rate are negatively correlated

b.the firm faces substantial exchange rate risk since the local currency price of the asset

and the exchange rate are positively correlated

c.the firm’s exchange rate exposure can be completely hedged with derivatives written

on the british pound

d.since randomness is involved, no hedging is possible

14) which of the following are true?

a.some items that are a source of transaction exposure are also a source of translation

exposure

b.some items that are a source of transaction exposure are not also a source of

translation exposure

c.both a and b

d.none of the above

15) under the bretton woods system each country established a par value for its

currency in relation to the dollar. and the u.s. dollar was pegged to gold at

a.$1 per ounce

b.$35 per ounce

c.$350 per ounce

d.$900 per ounce

16) eurodollars refers to dollar deposits when the depository bank is located in

a.europe

b.europe, and the caribbean

c.outside the united states

d.united states

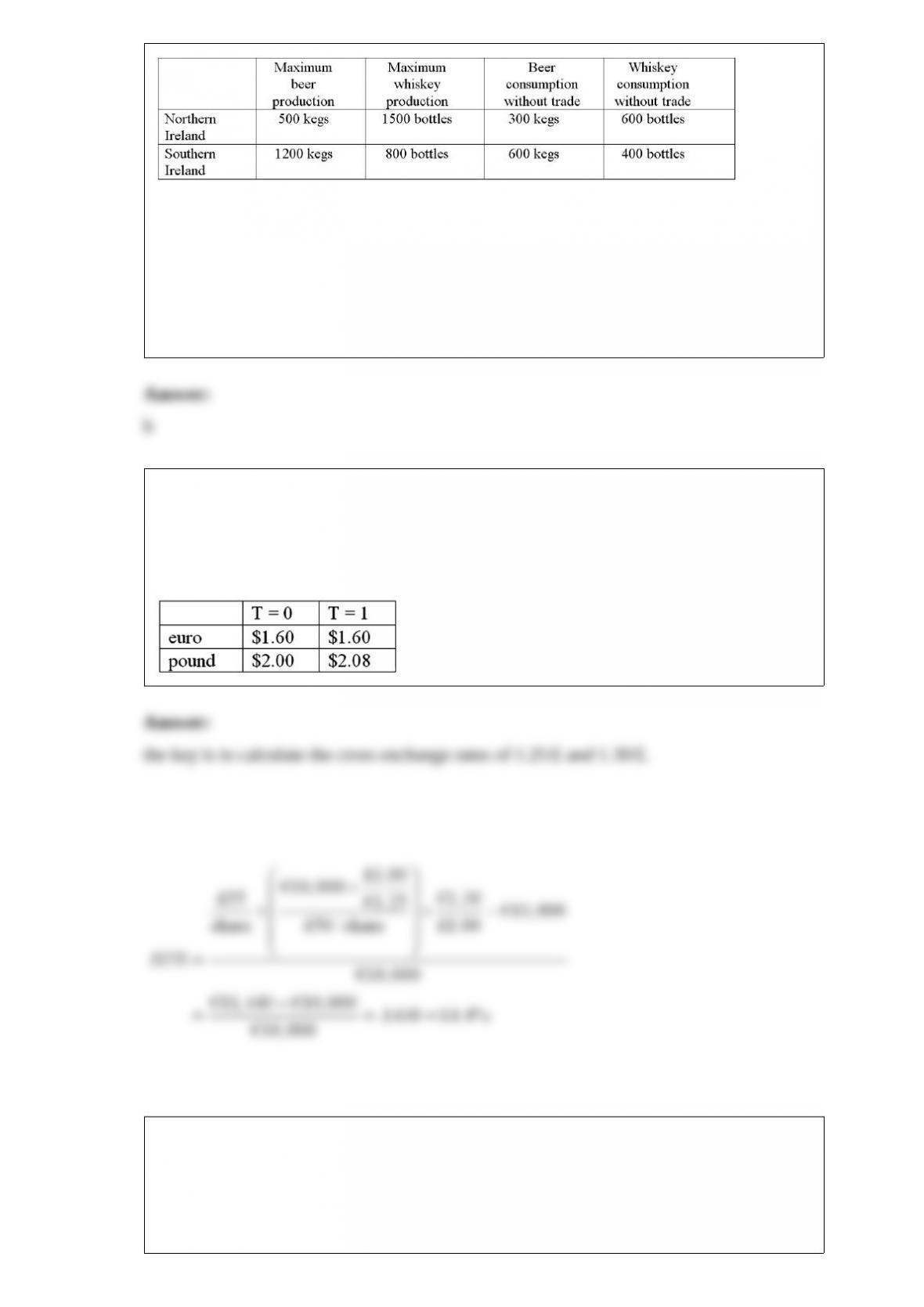

17) the first two columns give the maximum daily amounts of beer and whiskey that

southern ireland and northern ireland can produce when they completely specialize in

one or other product. the last two columns give each country’s consumption without

trade.

in which product does northern ireland have a comparative advantage?

a.beer

b.whiskey

c.neither

18) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock. one year after investment, the stock pays a £1 dividend,

and sells for £54. spot exchange rates at the start and end of the year are shown in the

table.

19) consider the situation of firm a and firm b. the current exchange rate is $1.50/. firm

a is a u.s. mnc and wants to borrow 40 million for 2 years. firm b is a french mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown;

both firms have aaa credit ratings.

explain how this opportunity affects which swap firm a will be willing to participate in.

20) the time from acceptance to maturity on a $50,000 banker’s acceptance is 180 days.

the importing bank’s acceptance commission is 2.50 percent and that the market rate for

180-day b/as is 2 percent.

determine the bond equivalent yield the importer’s bank will earn from discounting the

b/a with the exporter.

21) the time from acceptance to maturity on a $300,000 banker’s acceptance is 30 days.

the importing bank’s acceptance commission is 3 percent and that the market rate for

30-day b/as is 4 percent.

if the exporter’s opportunity cost of capital is 11 percent, should he discount the b/a or

hold it to maturity?

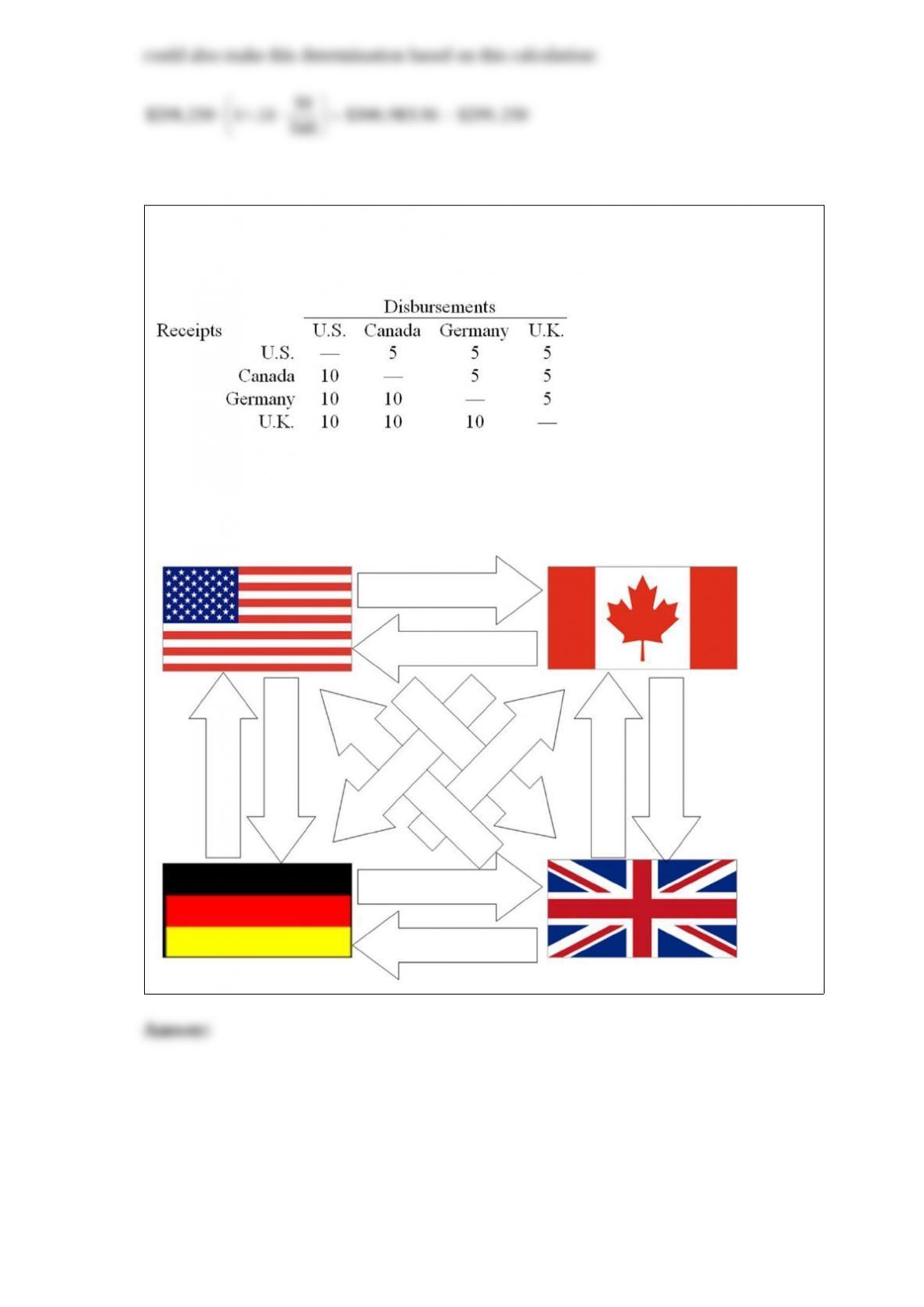

22) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

using your results to the last question, use bilateral netting to simplify.

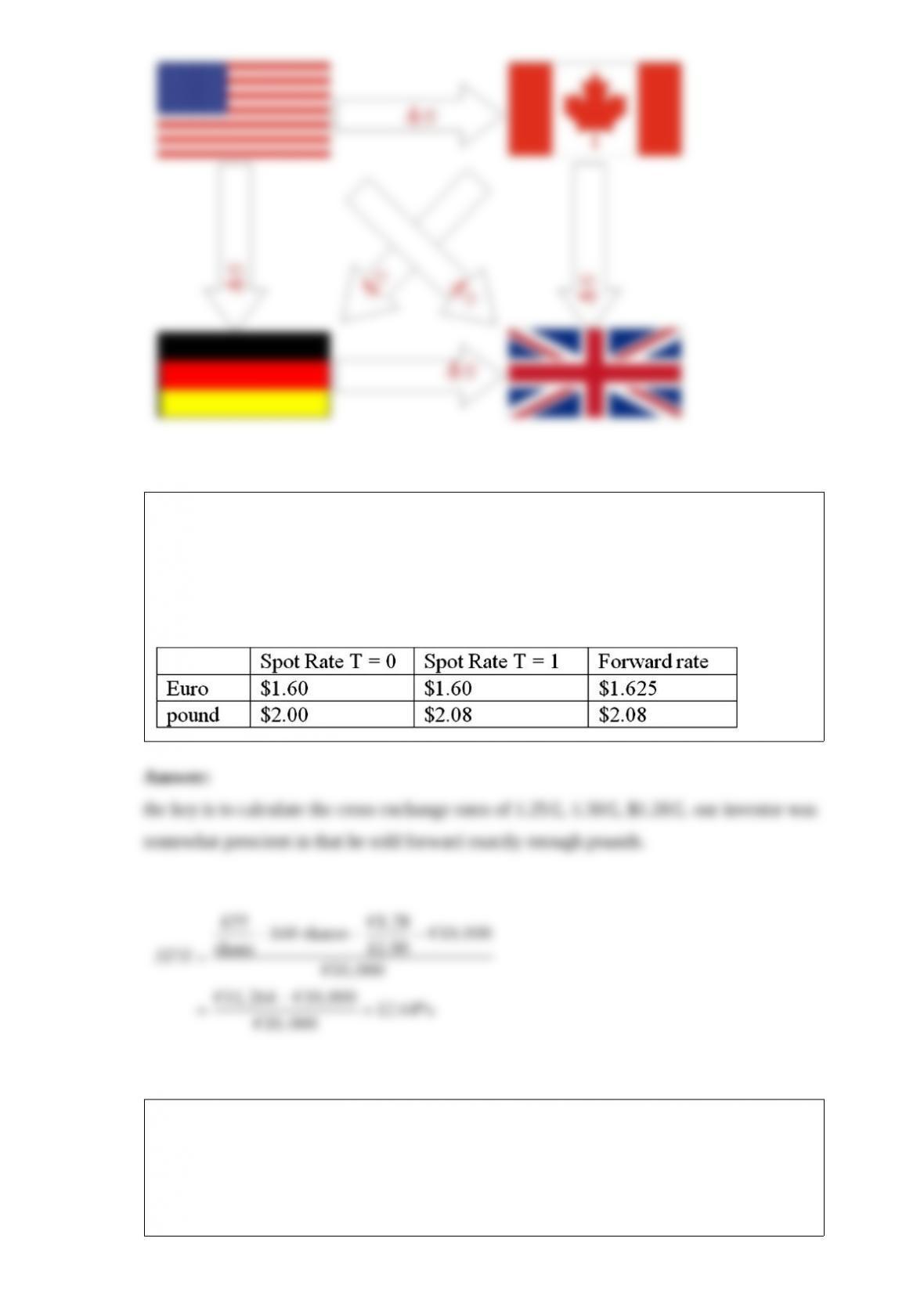

23) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock. one year after investment, the stock pays a £1 dividend,

and sells for £54 the exchange rate has changed from 1.25 per pound to 1.30 per pound,

although he sold £8,800 forward at the forward rate of 1.28 per pound.

spot exchange rates at the start and end of the year are shown in the table.

24) suppose that the swap that you proposed in question 2 is now 4 years old (i.e. there

is exactly one year to go on the swap). if the spot exchange rate prevailing in year 4 is

$1.8778 = 1 and the 1-year forward exchange rate prevailing in year 4 is $1.95 = 1,

what is the value of the swap to the party paying dollars? if the swap were initiated

today the correct rates would be as shown:

25) the time from acceptance to maturity on a $1,000,000 banker’s acceptance is 60

days.

the importing bank’s acceptance commission is 1.00 percent and that the market rate for

60-day b/as is 5 percent.

calculate the amount the banker will receive if the exporter discounts the b/a with the

importer’s bank.