Tender offers always consist of an offer to exchange acquirer shares for shares in the

target firm. True or False

Answer:

The extremely high leverage associated with leveraged buyouts significantly increases

the riskiness of the cash flows available to equity investors as a result of the increase in

fixed interest and principal repayments that must be made to lenders. Consequently, the

cost of equity should be adjusted for the increased leverage of the firm. True or False

Answer:

Trend extrapolation, which entails extending present trends into the future using

historical growth rates or multiple regression techniques, is rarely used to forecast cash

flow. True or False

Answer:

Shell corporations may be attractive for investors interested in capitalizing on the

intangible value associated with the existing corporate shell. This could include name

recognition; licenses, patents, and other forms of intellectual properties; and

underutilized assets such as warehouse space and fully depreciated equipment with

some economic life remaining. True or False

Answer:

Market power is a theory that suggests that firms merge to improve their ability to set

product and service selling prices. True or False

Answer:

The Euroequity market reflects equity issues by a foreign firm tapping a larger investor

base than the firm’s home equity market. True or False

Answer:

The LBO that is initiated by the target firm’s incumbent management is called a

management buyout. True or False

Answer:

A newly merged company will often experience at least a 5-10% loss of current

customers during the integration effort. True or False

Answer:

A composition is an agreement in which creditors agree to settle for less than the full

amount they are owed. True or False

Answer:

M&A practitioners utilize nominal cash flows except in circumstances of high rates of

inflation, when real cash flows are preferable. True or False

Answer:

Appreciating foreign currencies relative to the dollar increase the overall cost of

investing in the U.S. True or False

Answer:

Firms with redundant assets and predictable cash flow are often good candidates for

leveraged buyouts. True or False

Answer:

Antitakeover laws do not exist at the state level. True or False

Answer:

Elaborate multimedia presentations made to potential lenders in an effort to ‘shop” for

the best financing are often referred to as the “road show.” True or False

Answer:

Using stock as a form of payment is generally less complicated than using cash from

the buyer’s point of view. True or False

Answer:

Acquisition plan objectives should be directly linked to key business plan objectives.

True or False

Answer:

Acquisitions involving companies of a certain size cannot be completed until certain

information is supplied to the federal government and until a specific waiting period has

elapsed.

True or False

Answer:

Federal law prohibits trading in a bankrupt firm’s securities. True or False

Answer:

Empirical studies show that the desire by parent firms to increase strategic focus is an

important motive for exiting businesses. True or False

Answer:

Co-locating employees from the acquiring and target firms is rarely a good idea early in

the integration period because of the inevitable mistrust that will arise. True or False

Answer:

Equity carve-outs are similar to divestitures and spin-offs in that they provide a cash

infusion to the parent. True or False

Answer:

ESOP structures are rarely used vehicles for transferring the owner’s interest in the

business to the employees in small, privately owned firms. True or False

Answer:

Newly merged firms frequently experience a loss of existing customers as a direct

consequence of the merger. True or False

Answer:

The market or markets in which a firm chooses to compete should reflect the fit

between the firm’s primary strengths and its ability to satisfy customers needs better

than the competition. True or False

Answer:

If the selling price of the failing firm is less than the going concern and liquidation

value, the firm should sell the firm to another party.

Answer:

In choosing how to manage an acquisition in a new country, a manager with an in-depth

knowledge of the acquirer’s priorities, decision-making processes, and operations is

appropriate, especially when the acquirer expects to make very large new investments.

True or False

Answer:

LBO investors will often use the target firm’s cash in excess of normal working capital

requirements to finance the transaction. True or False

Answer:

A joint venture is rarely an independent legal entity such as a corporation or

partnership.

True or False

Answer:

A three-month Treasury bill rate is not free of risk for a five- or ten-year period, since

interest and principal received at maturity must be reinvested at three month intervals.

True or False

Answer:

Business alliances often receive favorable antitrust regulatory treatment. True or False

Answer:

Asset based lenders will usually lend up to 100% if the book value of the LBO target’s

receivables. True or False

Answer:

Rumors of impending acquisition can have a substantial deleterious impact on the target

firm. True or False

Answer:

Borrowers often prefer term loans because they do not have to be concerned that these

loans will have to be renewed. True or False

Answer:

The cost of equity can also be viewed as an opportunity cost. True or False

Answer:

Most M&A transactions in the United States are hostile or unfriendly takeover attempts.

True or False

Answer:

When buyers and sellers cannot reach agreement on price, other mechanisms can be

used to close the gap. These include balance sheet adjustments, earn-outs, rights to

intellectual property, and licensing fees. True or False

Answer:

In a public solicitation, a firm can announce publicly that it is putting itself, a

subsidiary, or a product line up for sale. Either potential buyers contact the seller or the

seller actively solicits bids from potential buyers or both. True or False

Answer:

Relative valuation methods are often described as market-based, as they reflect the

amounts investors are willing to pay for each dollar of earnings, cash flow, sales, or

book value at a moment in time. True or False

Answer:

LBO analyses are similar to DCF valuations in that they require projected cash flows,

present values, and discount rates; however, LBO models do not require the estimation

of terminal values. True or False

Answer:

Both public and private firms always attempt to maximize earnings growth. True or

False

Answer:

Avoiding the Merger Blues: American Airlines Integrates TWA

Trans World Airlines (TWA) had been tottering on the brink of bankruptcy for several

years, jeopardizing a number of jobs and the communities in which they are located.

Despite concerns about increased concentration, regulators approved American’s

proposed buyout of TWA in 2000 largely on the basis of the “failing company doctrine.”

This doctrine suggested that two companies should be allowed to merge despite an

increase in market concentration if one of the firms can be saved from liquidation.

American, now the world’s largest airline, has struggled to assimilate such smaller

acquisitions as AirCal in 1987 and Reno Air in 1998. Now, in trying to meld together

two major carriers with very different and deeply ingrained cultures, a combined

workforce of 113,000 and 900 jets serving 300 cities, American faced even bigger

challenges. For example, because switches and circuit breakers are in different locations

in TWA’s cockpits than in American’s, the combined airlines must spend millions of

dollars to rearrange cockpit gear and to train pilots how to adjust to the differences.

TWA’s planes also are on different maintenance schedules than American’s jets. For

American to see any savings from combining maintenance operations, it gradually had

to synchronize those schedules. Moreover, TWA’s workers had to be educated in

American’s business methods, and the carrier’s reservations had to be transferred to

American’s computer systems. Planes had to be repainted, and seats had to be

rearranged (McCartney, 2001).

Combining airline operations always has proved to be a huge task. American has

studied the problems that plagued other airline mergers, such as Northwest, which

moved too quickly to integrate Republic Airlines in This integration proved to be one of

the most turbulent in history. The computers failed on the first day of merged

operations. Angry workers vandalized ground equipment. For 6 months, flights were

delayed and crews did not know where to find their planes. Passenger suitcases were

misrouted. Former Republic pilots complained that they were being demoted in favor of

Northwest pilots. Friction between the two groups of pilots continued for years. In

contrast, American adopted a more moderately paced approach as a result of the

enormity and complexity of the tasks involved in putting the two airlines together. The

model they followed was Delta Airline’s acquisition of Western Airlines in 1986. Delta

succeeded by methodically addressing every issue, although the mergers were far less

complex because they involved merging far fewer computerized systems.

Even Delta had its problems, however. In 1991, Delta purchased Pan American World

Airways’ European operations. Pan Am’s international staff had little in common with

Delta’s largely domestic-minded workforce, creating a tremendous cultural divide in

terms of how the combined operations should be managed. In response to the 19911992

recession, Delta scaled back some routes, cut thousands of jobs, and reduced pay and

benefits for workers who remained..

Before closing, American had set up an integration management team of 12 managers,

six each from American and TWA. An operations czar, who was to become the vice

chair of the board of the new company, directed the team. The group met daily by

phone for as long as 2 hours, coordinating all merger-related initiatives. American set

aside a special server to log the team’s decisions. The team concluded that the two

lynchpins to a successful integration process were successfully resolving labor

problems and meshing the different computer systems. To ease the transition, William

Compton, TWA’s CEO, agreed to stay on with the new company through the transition

period as president of the TWA operations.

The day after closing the team empowered 40 department managers at each airline to

get involved. Their tasks included replacing TWA’s long-term airport leases with

short-term ones, combining some cargo operations, changing over the automatic

deposits of TWA employees’ paychecks, and implementing American’s environmental

response program at TWA in case of fuel spills. Work teams, consisting of both

American and TWA managers, identified more than 10,000 projects that must be

undertaken before the two airlines can be fully integrated.

Some immediate cost savings were realized as American was able to negotiate new

lease rates on TWA jets that are $200 million a year less than what TWA was paying.

These savings were a result of the increased credit rating of the combined companies.

However, other cost savings were expected to be modest during the 12 months

following closing as the two airlines were operated separately. TWA’s union workers,

who would have lost their jobs had TWA shut down, have been largely supportive of the

merger. American has won an agreement from its own pilots’ union on a plan to

integrate the carriers’ cockpit crews. Seniority issues proved to be a major hurdle.

Getting the mechanics’ and flight attendants’ unions on board required substantial effort.

All of TWA’s licenses had to be switched to American. These ranged from the Federal

Aviation Administration operating certificate to TWA’s liquor license in all the states.

Discussion Questions:

1) In your opinion, what are the advantages and disadvantages of moving to integrate

operations quickly? What are the advantages and disadvantages of moving more slowly

and deliberately?

2) Why did American choose to use managers from both airlines to direct the

integration of the two companies? What are the specific benefits in doing so?

3) How did the interests of the various stakeholders to the merger affect the complexity

of the integration process?

Answer:

In determining whether a proposed transaction is anti-competitive, U.S. regulators look

at all of the following except for

a. Market share of the combined businesses

b. Potential for price fixing

c. Ease of new competitors to enter the market

d. Potential for job loss among target firm’s employees

e. The potential for the target firm to fail without the takeover

Answer:

Which of the following is not true about mergers and acquisitions and taxes?

a. Tax considerations and strategies are likely to have an important impact on how a

deal is structured by affecting the amount, timing, and composition of the price offered

to a target firm.

b. Tax factors are likely to affect how the combined firms are organized following

closing, as the tax ramifications of a corporate structure are quite different from those of

a limited liability company or partnership.

c. Potential tax savings are often the primary motivation for an acquisition or merger.

d. Transactions may be either partly or entirely taxable to the target firm’s shareholders

or tax-free.

b. None of the above

Answer:

The form of acquisition refers to which of the following:

a. Tax status of the transaction

b. Acquisition vehicle

c. What is being acquired, i.e., stock or assets

d. Form of payment

e. How the transaction will be displayed for financial reporting purposes

Answer:

Developing staffing plans requires which of the following?

a. Identifying personnel requirements

b. Determining the availability of skilled employees to fill these requirements

c. Developing compensation plans

d. A and B only

e. A, B, and C

Answer:

Institutional investors in private companies often have considerable influence approving

or disapproving

proposed mergers. Which of the following are generally not considered institutional

investors?

a. Pension funds

b. Insurance companies

c. Bank trust departments

d. United States Treasury Department

e. Mutual funds

Answer:

Why would creditors be willing to give a portion of what they are owed by the debtor

firm for equity in the reorganized firm?

a. They are legally obligated to do so under U.S. bankruptcy law.

b. Ownership in a firm is inherently more valuable than being a creditor.

c. The value of the stock may in the long run far exceed the amount of debt the

creditors were willing to forgive.

d. Creditors understand that they can sue the firm at a later date for what they are owed.

e. None of the above.

Answer:

Which one of the following is not a commonly used method of valuing target firms?

a. Discounted cash flow

b. Comparable companies method

c. Recent transactions method

d. Asset oriented method

e. Share exchange ratio method

Answer:

In civil law countries (which include Western Europe, South America, Japan, and

Korea), the acquisition will generally be in the form of a share company or limited

liability company. True or False

Answer:

All of the following are true about product life cycles except for

a. Strong sales growth and low barriers to entry often characterize the early stages of a

product’s introduction

b. New entrants have substantially poorer cost positions, as a result of their small

market shares when compared to earlier entrants.

c. Later phases are characterized by slower market growth rates

d. During the high growth phases, firms usually experience high positive operating cash

flow

e. The introduction of product enhancements can extend a firm’s product life cycle

Answer:

Which of the following is not true about the constant growth valuation model?

a. The firm’s free cash flow is assumed to be unchanged in perpetuity

b. The firm’s free cash flow is assumed to grow at a constant rate in perpetuity

c. Free cash flow is discounted by the difference between the appropriate discount rate

and the expected growth rate of cash flow.

d. The constant growth model is sometimes referred to as the Gordon Growth Model.

e. If the analyst were using free cash flow to the firm, cash flow would be discounted by

the firm’s cost of capital less the expected growth rate in cash flow.

Answer:

Exxon and Mobil MergerThe Market Share Conundrum

Following a review of the proposed $81 billion merger in late 1998, the FTC decided to

challenge the ExxonMobil transaction on anticompetitive grounds. Options available to

Exxon and Mobil were to challenge the FTC’s rulings in court, negotiate a settlement,

or withdraw the merger plans. Before the merger, Exxon was the largest oil producer in

the United States and Mobil was the next largest firm. The combined companies would

create the world’s biggest oil company in terms of revenues. Top executives from Exxon

Corporation and Mobil Corporation argued that they needed to implement their

proposed merger because of the increasingly competitive world oil market. Falling oil

prices during much of the late 1990s put a squeeze on oil industry profits. Moreover,

giant state-owned oil companies are posing a competitive threat because of their access

to huge amounts of capital. To offset these factors, Exxon and Mobil argued that they

had to combine to achieve substantial cost savings.

After a year-long review, antitrust officials at the FTC approved the ExxonMobil

merger after the companies agreed to the largest divestiture in the history of the FTC.

The divestiture involved the sale of 15% of their service station network, amounting to

2400 stations. This included about 1220 Mobil stations from Virginia to New Jersey and

about 300 in Texas. In addition, about 520 Exxon stations from New York to Maine and

about 360 in California were divested. Exxon also agreed to the divestiture of an Exxon

refinery in Benecia, California. In entering into the consent decree, the FTC noted that

there is considerably greater competition worldwide. This is particularly true in the

market for exploration of new reserves. The greatest threat to competition seems to be

in the refining and distribution of gasoline.

Discussion Questions:

1) How does the FTC define market share?

2) Why might it be important to distinguish between a global and a regional oil and gas

market?

3) Why are the Exxon and Mobil executives emphasizing efficiencies as a justification

for this

merger?

4) Should the size of the combined companies be an important consideration in the

regulators’

analysis of the proposed merger?

5) How do the divestitures address perceived anti-competitive problems?

Answer:

JV and alliance agreements often limit how and to whom parties to the agreement can

transfer their interests. These limitations include which of the following mechanisms?

a. Tag-along provisions

b. Drag-along provisions

c. Put provisions

d. A, B, and C

e. A and B only

Answer:

Purchasing the target firm’s stock in the open market is a commonly used tactic to

achieve all of

the following except for

a. Acquiring a controlling interest in the target firm without making such actions public

knowledge.

b. Lowering the average cost of acquiring the target firm’s shares

c. Recovering the cost of an unsuccessful takeover attempt

d. Obtaining additional voting rights in the target firm

e. Strengthening the effectiveness of proxy contests

Answer:

The screening process represents a refinement of the search process and commonly

utilizes which of the following as selection criteria

a. Market share, product line, and profitability

b. Product line, profitability, and growth rate

c. Profitability, leverage, and growth rate

d. Degree of leverage, market share, and growth rate

e. All of the above

Answer:

Which of the following is true of the adjusted present value method of valuation?

a. Calculates the present value of tax benefits separately

b. Calculates the present value of the firm’s cash flow without debt

c. Adds A and B together

d. A, B, and C

e. A and B only

Answer:

Which of the following are not true about ESOPs?

a. An ESOP is a trust

b. Employer contributions to an ESOP are tax deductible

c. ESOPs can never borrow

d. Employees participating in ESOPs are immediately vested

e. C and D

Answer:

Which of the following is not true of exporting as a market entry strategy?

a. Exporting does not require the expense of establishing local operations

b. Exporters do not need to establish some means of marketing and distributing their

products at the local level

c. Exporters incur high transportation costs

d. Exporters may be adversely impacted by exchange rate fluctuations

e. Exporters may be adversely impacted by tariffs placed on imports into the local

country

Answer:

Which of the following represent common law countries?

a. United Kingdom

b. Australia

c. India

d. Pakistan

e. All of the above

Answer:

All of the following are true of antitrust lawsuits except for

a. The FTC files lawsuits in most cases they review.

b. The FTC reviews complaints that have been recommended by its staff and approved

by the FTC

c. FTC guidelines commit the FTC to make a final decision within 13 months of a

complaint

d. As an alternative to litigation, a company may seek to negotiate a voluntary

settlement of its differences with the FTC.

e. FTC decisions can be appealed in the federal circuit courts.

Answer:

Which of the following is not true about goodwill ?

a. Goodwill must be written off over 20 years.

b. Goodwill must be checked for impairment at least annually.

c. The loss of key customers could impair the value of goodwill.

d. Goodwill does not have to be amortized.

e. Goodwill is shown as an asset on the balance sheet.

Answer:

Which of the following represent alternative ways for businesses to reap some or all of

the advantages of M&As?

a. Joint ventures and strategic alliances

b. Strategic alliances, minority investments, and licensing

c. Minority investments, alliances, and licensing

d. Franchises, alliances, joint ventures, and licensing

e. All of the above

Answer:

Which of the following is true of the equity valuation model?

a. Discounts free cash flow to the firm by the weighted average cost of capital

b. Discounts free cash flow to equity by the cost of equity

c. Discounts free cash flow the firm by the cost of equity

d. Discounts free cash flow to equity by the weighted average cost of capital

e. None of the above

Answer:

Which of the following activities are likely to extend beyond what is normally

considered the conclusion of the post-closing integration period?

a. Developing communication plans

b. Cultural integration

c. Integration planning

d. Developing staffing plans

e. None of the above

Answer:

Which of the following are required for an acquisition to be considered tax-free?

a. Continuity of interest

b. A legitimate business purpose other than tax avoidance

c. The use of predominately acquirer shares to buy the target’s shares

d. An all cash acquisition of the target firm’s shares

e. A, B, and C only

Answer:

Termination provisions in alliances commonly include all but which of the following:

a. Buyout provisions enabling one party to purchase another’s ownership interests

b. Predetermined prices at which the buyouts may take place

c. Breakup payments payable to the remaining partners

d. How assets and liabilities will be divided among the partners

e. What will happen to patents and licenses owned by the alliance

Answer:

The enterprise value to EBITDA multiple relates the total book value of the firm from

the perspective of the liability side of the balance sheet (i.e., long-term debt plus

preferred and common equity), excluding cash, to EBITDA. True or False

Answer:

Certain post integration issues are best addressed prior to the closing. These include all

of the following except for

a. Who will pay for employee severance expenses

b. How will employee payroll be managed during ownership transition

c. What will be done with checks from customers that the seller continues to receive

after closing

d. How will the seller be reimbursed for monies owed to suppliers for products sold

prior to closing

e. Who will pay for health care and disability claims that often arise just before a

business is sold?

Answer:

Which of the following are not true about economies of scale?

a. Spreading fixed costs over increasing production levels

b. Improve the overall cost position of the firm

c. Most common in manufacturing businesses

d. Most common in businesses whose costs are primarily variable

e. Are common to such industries as utilities, steel making, pharmaceutical, chemical

and aircraft manufacturing

Answer:

Local country firms may be interested in alliances for which of the following reasons?

a. To gain access to the technology

b. To gain access to a widely recognized brand name

c. To gain access to innovative products

d. A, B, and C

e. A and B only

Answer:

Kraft Sweetens the Offer to Overcome Cadbury’s Resistance

Despite speculation that offers from U.S.-based candy company Hershey and the Italian

confectioner Ferreiro would be forthcoming, Kraft’s bid on January 19, 2010, was

accepted unanimously by Cadbury’s board of directors. Kraft, the world’s second (after

Nestle) largest food manufacturer, raised its offer over its initial September 7, 2009, bid

to $19.5 billion to win over the board of the world’s second largest candy and chocolate

maker. Kraft also assumed responsibility for $9.5 billion of Cadbury’s debt.

Kraft’s initial bid evoked a raucous response from Cadbury’s chairman Roger Carr, who

derided the offer that valued Cadbury at $16.7 billion as showing contempt for his

firm’s well-known brand and dismissed the hostile bidder as a low-growth

conglomerate. Immediately following the Kraft announcement, Cadbury’s share price

rose by 45 percent (7 percentage points more than the 38 percent premium implicit in

the Kraft offer). The share prices of other food manufacturers also rose due to

speculation that they could become takeover targets.

The ensuing four-month struggle between the two firms was reminiscent of the highly

publicized takeover of U.S. icon Anheuser-Busch in 2008 by Belgian brewer InBev.

The Kraft-Cadbury transaction stimulated substantial opposition from senior

government ministers and trade unions over the move by a huge U.S. firm to take over

a British company deemed to be a national treasure. However, like InBev’s takeover of

Anheuser-Busch, what started as a donnybrook ended on friendly terms, with the two

sides reaching final agreement in a single weekend.

Determined to become a global food and candy giant, Kraft decided to bid for Cadbury

after the U.K.-based firm spun off its Schweppes beverages business in the United

States in 2008. The separation of Cadbury’s beverage and confectionery units resulted

in Cadbury becoming the world’s largest pure confectionery firm following the spinoff.

Confectionery companies tend to trade at a higher value, so adding the Cadbury’s

chocolate and gum business could enhance Kraft’s attractiveness to competitors.

However, this status was soon eclipsed by Mars’s acquisition of Wrigley in 2008.

A takeover of Cadbury would help Kraft, the biggest food conglomerate in North

America, to compete with its larger rival, Nestle. Cadbury would strengthen Kraft’s

market share in Britain and would open India, where Cadbury is among the most

popular chocolate brands. It would also expand Kraft’s gum business and give it a

global distribution network. Nestle lacks a gum business and is struggling with

declining sales as recession-plagued consumers turned away from its bottled water and

ice cream products. Cadbury and Kraft fared relatively well during the 20082009 global

recession, with Cadbury’s confectionery business proving resilient despite price

increases in the wake of increasing sugar prices. Kraft had benefited from rising sales of

convenience foods because consumers ate more meals at home during the recession.

The differences in the composition of the initial and final Kraft bids reflected a series of

crosscurrents. Irene Rosenfeld, the Kraft CEO, not only had to contend with

vituperative comments from Cadbury’s board and senior management, but she also was

soundly criticized by major shareholders who feared Kraft would pay too much for

Cadbury. Specifically, the firm’s largest shareholder, Warren Buffett’s Berkshire

Hathaway with a 9.4 percent stake, expressed concern that the amount of new stock that

would have to be issued to acquire Cadbury would dilute the ownership position of

existing Kraft shareholders. In an effort to placate dissident Kraft shareholders while

acceding to Cadbury’s demand for an increase in the offer price, Ms. Rosenfeld

increased the offer by 7 percent by increasing the cash portion of the purchase price.

The new bid consisted of $8.17 of cash and 0.1874 new Kraft shares, compared to

Kraft’s original offer of $4.89 of cash and 0.2589 new Kraft shares for each Cadbury

share outstanding. The change in the composition of the offer price meant that Kraft

would issue 265 million new shares compared with its original plan to issue 370

million. The change in the terms of the deal meant that Kraft would no longer have to

get shareholder approval for the new share issue, since it was able to avoid the NYSE

requirement that firms issuing shares totaling more than 20 percent of the number of

shares currently outstanding must receive shareholder approval to do so.

Discussion Questions:

1) Which firm is the acquirer and which is the target firm?

2) Why did the Cadbury common share price close up 38% on the announcement date,

7% more than the premium built into the offer price?

3) Why did the price of other food manufacturers also increase following the

announcement of the attempted takeover?

4) After four months of bitter and often public disagreement, Cadbury’s and Kraft’s

management reached a final agreement in a weekend. What factors do you believe

might have contributed to this rapid conclusion?

5) Kraft appeared to take action immediately following Cadbury’s spin-off of

Schweppes making Cadbury a pure candy company. Why do you believe that Kraft

chose not to buy Cadbury and later divest such noncore businesses as Schweppes?

Answer:

Hughes Corporation’s Dramatic Transformation

In one of the most dramatic redirections of corporate strategy in U.S. history, Hughes

Corporation transformed itself from a defense industry behemoth into the world’s

largest digital information and communications company. Once California’s largest

manufacturing employer, Hughes Corporation built spacecraft, the world’s first working

laser, communications satellites, radar systems, and military weapons systems.

However, by the late 1990s, the firm had undergone substantial gut-wrenching change

to reposition the firm in what was viewed as a more attractive growth opportunity. This

transformation culminated in the firm being acquired in 2004 by News Corp., a global

media empire.

To accomplish this transformation, Hughes divested its communications satellite

businesses and its auto electronics operation. The corporate overhaul created a firm

focused on direct-to-home satellite broadcasting with its DirecTV service offering.

DirecTV’s introduction to nearly 12 million U.S. homes was a technology made

possible by U.S. military spending during the early 1980s. Although military spending

had fueled much of Hughes’ growth during the decade of the 1980s, it was becoming

increasingly clear by 1988 that the level of defense spending of the Reagan years was

coming to a close with the winding down of the cold war.

For the next several years, Hughes attempted to find profitable niches in the rapidly

consolidating U.S. defense contracting industry. Hughes acquired General Dynamics’

missile business and made 15 smaller defense-related acquisitions. Eventually, Hughes’

parent firm, General Motors, lost enthusiasm for additional investment in

defense-related businesses. GM decided that, if Hughes could not participate in the

shrinking defense industry, there was no reason to retain any interests in the industry at

all. In November 1995, Hughes initiated discussions with Raytheon, and two years

later, it sold its aerospace and defense business to Raytheon for $9.8 billion. The firm

also merged its Delco product line with GM’s Delphi automotive systems. What

remained was the firm’s telecommunications division. Hughes had transformed itself

from a $16 billion defense contractor to a svelte $4 billion telecommunications

business.

Hughes’ telecommunications unit was its smallest operation but, with DirecTV, its

fastest growing. The transformation was to exact a huge cultural toll on Hughes’

employees, most of whom had spent their careers dealing with the U.S. Department of

Defense. Hughes moved to hire people aggressively from the cable and broadcast

businesses. By the late 1990s, former Hughes’ employees constituted only 1520 percent

of DirecTV’s total employees.

Restructuring continued through the end of the 1990s. In 2000, Hughes sold its satellite

manufacturing operations to Boeing for $3.75 billion. This eliminated the last

component of the old Hughes and cut its workforce in half. In December 2000, Hughes

paid about $180 million for Telocity, a firm that provides digital subscriber line service

through phone lines. This acquisition allowed Hughes to provide high-speed Internet

connections through its existing satellite service, mainly in more remote rural areas, as

well as phone lines targeted at city dwellers. Hughes now could market the same

combination of high-speed Internet services and video offered by cable providers,

Hughes’ primary competitor.

In need of cash, GM put Hughes up for sale in late 2000, expressing confidence that

there would be a flood of lucrative offers. However, the faltering economy and stock

market resulted in GM receiving only one serious bid, from media tycoon Rupert

Murdoch of News Corp. in February 2001. But, internal discord within Hughes and GM

over the possible buyer of Hughes Electronics caused GM to backpedal and seek

alternative bidders. In late October 2001, GM agreed to sell its Hughes Electronics

subsidiary and its DirecTV home satellite network to EchoStar Communication for

$25.8 billion. However, regulators concerned about the antitrust implications of the deal

disallowed this transaction. In early 2004, News Corp., General Motors, and Hughes

reached a definitive agreement in which News Corp acquired GM’s 19.9 percent stake

in Hughes and an additional 14.1 percent of Hughes from public shareholders and GM’s

pension and other benefit plans. News Corp. paid about $14 per share, making the deal

worth about $6.6 billion for 34.1 percent of Hughes. The implied value of 100 percent

of Hughes was, at that time, $19.4 billion, about three fourths of EchoStar’s valuation

three years earlier.

Case Study Discussion Questions:

1) How did changes in Hughes’ external environment contribute to its dramatic 20-year

restructuring effort? Cite specific influences in answering this question. (Hint: Consider

some of the motivations discussed in this chapter for engaging in restructuring

activities.). Cite examples of how Hughes took advantage of their core competencies in

pursuing other alternatives?

2) Why did Hughes’ board and management seem to rely heavily on divestitures rather

than other restructuring

strategies discussed in this chapter to achieve the radical transformation of the firm? Be

specific.

3) What risks did Hughes face in moving completely away from its core defense

business and into a high-technology commercial business? In your judgment, did

Hughes move too quickly or too slowly? Explain your answer.

4) Why did Hughes move so aggressively to hire employees from the cable TV and

broadcast industry?

5) Speculate as to why News Corp, a major entertainment industry content provider,

might have been interested in acquiring Hughes. Be specific.

Answer:

Coca-Cola and Procter & Gamble’s Aborted Effort to Create a Global Joint

Venture Company

Coca-Cola (Coke), arguably the world’s best-known brand, manufactures and

distributes Coca-Cola as well as 230 other products in 200 countries through the world’s

largest distribution system. Procter & Gamble (P&G) sells 300 brands to nearly 5

billion consumers in 140 countries and holds more food patents than the three largest

U.S. food companies combined. Moreover, P&G has a substantial number of new food

and beverage products under development. Both firms have been competing in the

health and wellness segment of the food market for years. P&G spends about 5 percent

of its annual sales, about $1.9 billion, on R&D and holds more than 27,000 patents. The

firm employs about 6,000 scientists, including about 1,200 people with PhDs.

Both firms have extensive distribution systems. P&G uses a centralized selling and

warehouse distribution system for servicing high-volume outlets, such as grocery store

chains. With a warehouse distribution system, the retailer is responsible for in-store

presentations of the brands, including shelving, display, and merchandising. The

primary disadvantage of this type of distribution system is that it does not reach many

smaller outlets cost effectively, resulting in many lost opportunities. In contrast, Coke

uses three distinct systems. Direct store delivery consists of a network of independently

operated bottlers, which bottle and deliver the product directly to the outlet. The bottler

also is responsible for in-store merchandising. Coke’s warehouse distribution is similar

to P&G’s and is used primarily to distribute Minute Maid products. Coke also sells

beverage concentrates to distributors and food service outlets.

On February 21, 2001, Coca-Cola and Procter & Gamble announced, amid great

fanfare, plans to create a stand-alone joint venture corporation focused on developing

and marketing new juice and juice-based beverages as well as snacks on a global basis.

The new company expected to benefit from Coca-Cola’s worldwide distribution,

merchandising, and customer marketing skills and P&G’s R&D capabilities and wide

range of popular brands. The new company would focus on the health and wellness

segment of the food market. Less than nine months later, Coke and P&G released a

one-sentence joint statement on September 21, 2001, that they could achieve better

returns for their respective shareholders if they pursued this opportunity independently.

Although it is unclear what may have derailed what initially had seemed to the potential

partners like such a good idea, it is instructive to examine the initial rationale for the

proposed joint effort.

Each parent would own 50 percent of the new company. Because of the businesses each

partner was to contribute to the JV, the firm would have annual sales of $4 billion. The

new firm would be an LLC, having its own board of directors consisting of two

directors each from Coke and P&G. Moreover, the new firm would have its own

management and dedicated staff providing administrative and R&D services. Coke was

contributing a number of well-known brands including Minute Maid, Hi-C, Five Alive,

Cappy, Kapo, Sonfil, and Qoo; P&G contributed Pringles, Sunny Delight, and Punica

beverages. The new company would have had 15 manufacturing facilities and about

6,000 employees.

Although the new firm was to have access to all distribution systems of the parents, it

would have been free to choose the best route to market for each product. Although

Minute Maid was to continue to use Coke’s distribution channels, it also was to take

advantage of existing refrigerated distribution systems built for Sunny Delight. Pringles

was to use a variety of distribution systems, including the existing warehouse system.

The Pringles brand was expected to take full advantage of Coke’s global distribution

and merchandising capabilities. Minute Maid was to gain access to new outlets through

Coke’s fountain and direct store distribution system.

The new company’s sales were expected to grow from $4 billion during the first 12

months of operation to more than $5 billion within two years. The combination of

increasing revenue and cost savings was expected to contribute about $200 million in

pretax earnings annually by 2005. Specifically, Pringles’s revenue growth as a result of

enhanced distribution was expected to contribute about $120 million of this projected

improvement in pretax earnings. The importance of improved distribution is illustrated

by noting that Coke has access to 16 million outlets globally. In the United States alone,

that represents a 10-fold increase for Pringles, from its current 150,000 points of outlet.

Similarly, improved merchandising and distribution of Sunny Delight was expected to

contribute an additional $30 million in pretax income. The remaining $50 million in

pretax earnings was to come from lower manufacturing, distribution, and administrative

expenses and through discounts received on bulk purchases of foodstuffs and

ingredients. P&G and Coke were hoping to stimulate innovation by combining global

brands and distribution with talent from both firms in what was hoped would be a

highly entrepreneurial corporate culture. The parents also hoped that the stand-alone

firm would be able to achieve focus and economies of scale that could not have been

achieved by either firm separately.

The results of the LLC were not to be consolidated with those of the parents but rather

shown using the equity method of accounting. Under this method of accounting, each

parent’s proportionate share of earnings (or losses) is shown on its income statement,

and its equity interest in the LLC is displayed on its balance sheets. The new company

was expected to be nondilutive of the earnings of the parents during its first full year of

operations and contribute to earnings per share in subsequent years. The incremental

earnings were expected to improve the market value of the parents by at least $1.52.0

billion (Bachman, 2001).

Some observers suggested that P&G would stand to benefit the most from the JV. It

would have gained substantially by obtaining access to the growing vending machine

market. Historically, P&G’s penetration in this market had been miniscule. This

perceived disproportionate benefit accruing to P&G may have contributed to the

eventual demise of the joint venture effort. Coke may have sought additional benefits

from the JV that P&G was simply not willing to cede. Once again, we see that, no

matter how attractive the concept may seem to be on the surface, the devil is indeed in

the details when comes to making it happen.

Discussion Questions:

1) In your opinion, what were the motivating factors for the Coke and P&G business

alliance?

2) Why do you think the parents selected a limited liability company structure for the

new company? What are the advantages and disadvantages of this structure over

alternative legal structures?

3) The parents estimate that the new company will add at least $1.5-$2.0 billion to their

market values. How do you think this estimated incremental value was determined?

4) Why do you think the parents opted to form a 50/50 distribution of ownership? What

are some of the possible challenges of operating the new company with this type of an

ownership arrangement? What can the parents do to overcome these challenges?

5) Do you think it is likely that the new company will become highly entrepreneurial

and innovative? Why? / Why not? What can the parents do to stimulate the

development of this type of an environment within the new company?

6) What factors may have contributed to the decision to discontinue efforts to

implement the joint venture? Consider control, scope, financial, and resource

contribution issues.

Answer:

Answer:

Answer:

Additional Problems/Case Studies

The Importance of Distinguishing Between Operating and Nonoperating Assets

In 2006, Verizon Communications and MCI Inc. executives completed a deal in which

MCI shareholders received $6.7 billion for 100% of MCI stock. Verizon’s management

argued that the deal cost their shareholders only $5.3 billion in Verizon stock, with MCI

having agreed to pay its shareholders a special dividend of $1.4 billion contingent on

their approval of the transaction. The $1.4 billion special dividend reduced MCI’s cash

in excess of what was required to meet its normal operating cash requirements.

To understand the actual purchase price, it is necessary to distinguish between operating

and nonoperating assets. Without the special dividend, the $1.4 billion in cash would

have transferred automatically to Verizon as a result of the purchase of MCI’s stock.

Verizon would have had to increase its purchase price by an equivalent amount to

reflect the face value of this nonoperating cash asset. Consequently, the purchase price

would have been $6.7 billion. With the special dividend, the excess cash transferred to

Verizon was reduced by $1.4 billion, and the purchase price was $5.3 billion.

In fact, the alleged price reduction was no price reduction at all. It simply reflected

Verizon’s shareholders receiving $1.4 billion less in net acquired assets. Moreover, since

the $1.4 billion represents excess cash that would have been reinvested in MCI or paid

out to shareholders anyway, the MCI shareholders were simply getting the cash earlier

than they may have otherwise.

The Hunt for Elusive Synergy@Home Acquires Excite

Background Information

Prior to @Home Network’s merger with Excite for $6.7 billion, Excite’s market value

was about $3.5 billion. The new company combined the search engine capabilities of

one of the best-known brands (at that time) on the Internet, Excite, with @Home’s

agreements with 21 cable companies worldwide. @Home gains access to the nearly 17

million households that are regular users of Excite. At the time, this transaction

constituted the largest merger of Internet companies ever. At the time of the transaction,

the combined firms, called Excite @Home, displayed a P/E ratio in excess of 260 based

on the consensus earnings estimate of $0.21 per share. The firm’s market value was

$18.8 billion, 270 times sales. Investors had great expectations for the future

performance of the combined firms, despite their lackluster profit performance since

their inception. @Home provided interactive services to home and business users over

its proprietary network, telephone company circuits, and through the cable companies’

infrastructure. Subscribers paid $39.95 per month for the service.

Assumptions

Excite is properly valued immediately prior to announcement of the transaction.

Annual customer service costs equal $50 per customer.

Annual customer revenue in the form of @Home access charges and ancillary services

equals $500 per customer. This assumes that declining access charges in this highly

competitive environment will be offset by increases in revenue from the sale of

ancillary services.

None of the current Excite user households are current @Home customers.

New @Home customers acquired through Excite remain @Home customers in

perpetuity.

@Home converts immediately 2 percent or 340,000 of the current 17 million Excite

user households.

@Home’s cost of capital is 20 percent during the growth period and drops to 10

percent during the slower, sustainable growth period; its combined federal and state tax

rate is 40 percent.

Capital spending equals depreciation; current assets equal current liabilities.

FCFF from synergy increases by 15 percent annually for the next 10 years and 5

percent thereafter. Its cost of capital after the high-growth period drops to 10 percent.

The maximum purchase price @Home should pay for Excite equals Excite’s current

market price plus the synergy that results from the merger of the two businesses.

Discussion Questions

1) Use discounted cash flow (DCF) methods to determine if @Home overpaid for

Excite.

2) What other assumptions might you consider in addition to those identified in the case

study?

3) What are the limitations of the discounted cash flow method employed in this case?

Answers to Case Study Questions:

1) Did @Home overpay for Excite?

2) What other assumptions might you consider?

3) What are the limitations of the valuation methodology employed in this case?

Answer:

Daimler Acquires ChryslerAnatomy of a Cross-Border Transaction

The combination of Chrysler and Daimler created the third largest auto manufacturer in

the world, with more than 428,000 employees worldwide. Conceptually, the strategic fit

seemed obvious. German engineering in the automotive industry was highly regarded

and could be used to help Chrysler upgrade both its product quality and production

process. In contrast, Chrysler had a much better track record than Daimler in getting

products to market rapidly. Daimler’s distribution network in Europe would give

Chrysler products better access to European markets; Chrysler could provide parts and

service support for Mercedes-Benz in the United States. With greater financial strength,

the combined companies would be better able to make inroads into Asian and South

American markets.

Daimler’s product markets were viewed as mature, and Chrysler was under pressure

from escalating R&D costs and retooling demands in the wake of rapidly changing

technology. Both companies watched with concern the growing excess capacity of the

worldwide automotive manufacturing industry. Daimler and Chrysler had been in

discussions about doing something together for some time. They initiated discussions

about creating a joint venture to expand into Asian and South American markets, where

both companies had a limited presence. Despite the termination of these discussions as

a result of disagreement over responsibilities, talks were renewed in February Both

companies shared the same sense of urgency about their vulnerability to companies

such as Toyota and Volkswagen. The transaction was completed in April 1998 for $36

billion.

Enjoying a robust auto market, starry-eyed executives were touting how the two firms

were going to save billions by using common parts in future cars and trucks and by

sharing research and technology. In a press conference to announce the merger, Jurgen

Schrempp, CEO of DaimlerChrysler, described the merger as highly complementary in

terms of product offerings and the geographic location of many of the firms’

manufacturing operations. It also was described to the press as a merger of equals

(Tierney, 2000). On the surface, it all looked so easy.

The limitations of cultural differences became apparent during efforts to integrate the

two companies. Daimler had been run as a conglomerate, in contrast to Chrysler’s

highly centralized operations. Daimler managers were accustomed to lengthy reports

and meetings to review the reports. Under Schrempp’s direction, many top management

positions in Chrysler went to Germans. Only a few former Chrysler executives reported

directly to Schrempp. Made rich by the merger, the potential for a loss of American

managers within Chrysler was high. Chrysler managers were accustomed to a higher

degree of independence than their German counterparts. Mercedes dealers in the United

States balked at the thought of Chrysler’s trucks still sporting the old Mopar logo

delivering parts to their dealerships. All the trucks had to be repainted.

Charged with the task of finding cost savings, the integration team identified a list of

hundreds of opportunities, offering billions of dollars in savings. For example,

Mercedes dropped its plans to develop a battery-powered car in favor of Chrysler’s

electric minivan. The finance and purchasing departments were combined worldwide.

This would enable the combined company to take advantage of savings on bulk

purchases of commodity products such as steel, aluminum, and glass. In addition,

inventories could be managed more efficiently, because surplus components purchased

in one area could be shipped to other facilities in need of such parts. Long-term supply

contracts and the dispersal of much of the purchasing operations to the plant level

meant that it could take as long as 5 years to fully integrate the purchasing department.

The time required to integrate the manufacturing operations could be significantly

longer, because both Daimler and Chrysler had designed their operations differently and

are subject to different union work rules. Changing manufacturing processes required

renegotiating union agreements as the multiyear contracts expired. All of that had to

take place without causing product quality to suffer. To facilitate this process, Mercedes

issued very specific guidelines for each car brand pertaining to R&D, purchasing,

manufacturing, and marketing.

Although certainly not all of DaimlerChrysler’s woes can be blamed on the merger, it

clearly accentuated problems associated with the cyclical economic slowdown during

2001 and the stiffened competition from Japanese automakers. The firm’s top

management has reacted, perhaps somewhat belatedly to the downturn, by slashing

production and eliminating unsuccessful models. Moreover, the firm has pared its

product development budget from $48 billion to $36 billion and eliminated more than

26,000 jobs, or 20% of the firm’s workforce, by early 2002. Six plants in Detroit,

Mexico, Argentina, and Brazil were closed by the end of 2002. The firm also cut

sharply the number of Chrysler. car dealerships. Despite the aggressive cost cutting,

Chrysler reported a $2 billion operating loss in 2003 and a $400 million loss in 2004.

While Schrempp had promised a swift integration and a world-spanning company that

would dominate the industry, five years later new products have failed to pull Chrysler

out of a tailspin. Moreover, DaimlerChrysler’s domination has not extended beyond the

luxury car market, a market they dominated before the acquisition. The market

capitalization of DaimlerChrysler, at $38 billion at the end of 2004, was well below the

German auto maker’s $47 billion market cap before the transaction.

With the benefit of hindsight, it is possible to note a number of missteps

DaimlerChrysler has made that are likely to haunt the firm for years to come. These

include paying too much for some parts, not updating some vehicle models sooner,

falling to offer more high-margin vehicles that could help ease current financial strains,

not developing enough interesting vehicles for future production, and failing to be

completely honest with Chrysler employees. Although Daimler managed to take costs

out, it also managed to alienate the workforce.

Discussion Questions:

1) Identify ways in which the merger combined companies with complementary skills

and resources?

2) What are the major cultural differences between Daimler and Chrysler?

3) What were the principal risks to the merger?

4) Why might it take so long to integrate manufacturing operations and certain

functions such as purchasing?

5) How might Daimler have better managed the postmerger integration?

Answer:

FTC Prevents Staples from Acquiring Office Depot

As the leading competitor in the office supplies superstore market, Staples’ proposed

$3.3 billion acquisition of Office Depot received close scrutiny from the FTC

immediately after its announcement in September The acquisition would create a huge

company with annual sales of $10.7 billion. Following the acquisition, only one

competitor, OfficeMax with sales of $3.3 billion, would remain. Staples pointed out that

the combined companies would comprise only about 5% of the total office supply

market. However, the FTC considered the superstore market as a separate segment

within the total office supply market. Using the narrow definition of “market,” the FTC

concluded that the combination of Staples and Office Depot would control more than

three-quarters of the market and would substantially increase the pricing power of the

combined firms. Despite Staples’ willingness to divest 63 stores to Office Max in

markets in which its concentration would be the greatest following the merger, the FTC

could not be persuaded to approve the merger.

Staples continued its insistence that there would be no harmful competitive effects from

the proposed merger, because office supply prices would continue their long-term

decline. Both Staples and Office Depot had a history of lowering prices for their

customers because of the efficiencies associated with their ‘superstores.” The companies

argued that the merger would result in more than $4 billion in cost savings over 5 years

that would be passed on to their customers. However, the FTC argued and the federal

court concurred that the product prices offered by the combined firms still would be

higher, as a result of reduced competition, than they would have been had the merger

not taken place. The FTC relied on a study showing that Staples tended to charge higher

prices in markets in which it did not have another superstore as a competitor. In early

1997, Staples withdrew its offer for Office Depot.

Discussion Questions:

1) How important is properly defining the market segment in which the acquirer and

target

companies compete to determining the potential increased market power if the two are

permitted to combine? Explain your answer.

2) Do you believe the FTC was being reasonable in not approving the merger even

though?

Staples agreed to divest 63 stores in markets where market concentration would be the

greatest

following the merger? Explain your answer.

Answer:

Delta Airlines Rises from the Ashes

Key Points:

Once in Chapter 11, a firm may be able to negotiate significant contract concessions

with unions as well as its creditors.

A restructured firm emerging from Chapter 11 often is a much smaller but more

efficient operation than prior to its entry into bankruptcy.

______________________________________________________________________

________________

On April 30, 2007, Delta Airlines emerged from bankruptcy leaner but still an

independent carrier after a 19-month reorganization during which it successfully fought

off a $10 billion hostile takeover attempt by US Airways. The challenge facing Delta’s

management was to convince creditors that it would become more valuable as an

independent carrier than it would be as part of US Airways.

Ravaged by escalating jet fuel prices and intensified competition from low-fare,

low-cost carriers, Delta had lost $6.1 billion since the September 11, 2001, terrorist

attack on the World Trade Center. The final crisis occurred in early August 2005 when

the bank that was processing the airline’s Visa and MasterCard ticket purchases started

holding back money until passengers had completed their trips as protection in case of a

bankruptcy filing. The bank was concerned that it would have to refund the passengers’

ticket prices if the airline curtailed flights and the bank had to be reimbursed by the

airline. This move by the bank cost the airline $650 million, further straining the

carrier’s already limited cash reserves. Delta’s creditors were becoming increasingly

concerned about the airline’s ability to meet its financial obligations. Running out of

cash and unable to borrow to satisfy current working capital requirements, the airline

felt compelled to seek the protection of the bankruptcy court in late August 2005.

Delta’s decision to declare bankruptcy occurred about the same time as a similar

decision by Northwest Airlines. United Airlines and US Airways were already in

bankruptcy. United had been in bankruptcy almost three years at the time Delta entered

Chapter 11, and US Airways had been in bankruptcy court twice since the 9/11 terrorist

attacks shook the airline industry. At the time Delta declared bankruptcy, about one-half

of the domestic carrier capacity was operating under bankruptcy court oversight.

Delta underwent substantial restructuring of its operations. An important component of

the restructuring effort involved turning over its underfunded pilot’s pension plans to

the Pension Benefit Guaranty Corporation (PBGC), a federal pension insurance agency,

while winning concessions on wages and work rules from its pilots. The agreement with

the pilot’s union would save the airline $280 million annually, and the pilots would be

paid 14 percent less than they were before the airline declared bankruptcy. To achieve

an agreement with its pilots to transfer control of their pension plan to the PBGC, Delta

agreed to give the union a $650 million interest-bearing note upon terminating and

transferring the pension plans to the PBGC. The union would then use the airline’s

payments on the note to provide supplemental payments to members who would lose

retirement benefits due to the PBGC limits on the amount of Delta’s pension obligations

it would be willing to pay. The pact covers more than 6,000 pilots.

The overhaul of Delta, the nation’s third largest airline, left it a much smaller carrier

than the one that sought protection of the bankruptcy court. Delta shed about one jet in

six used by its mainline operations at the time of the bankruptcy filing, and it cut more

than 20 percent of the 60,000 employees it had just prior to entering Chapter 11. Delta’s

domestic carrying capacity fell by about 10 percent since it petitioned for Chapter 11

reorganization, allowing it to fill about 84 percent of its seats on U.S. routes. This

compared to only 72 percent when it filed for bankruptcy. The much higher utilization

of its planes boosted revenue per mile flown by 15 percent since it entered bankruptcy,

enabling the airline to better cover its fixed expenses. Delta also sold one of its “feeder”

airlines, Atlantic Southeast Airlines, for $425 million.

Delta would have $2.5 billion in exit financing to fund operations and a cost structure

of about $3 billion a year less than when it went into bankruptcy. The purpose of the

exit financing facility is to repay the company’s $2.1 billion debtor-in-possession credit

facilities provided by GE Capital and American Express, make other payments required

on exiting bankruptcy, and increase its liquidity position. With ten financial institutions

providing the loans, the exit facility consisted of a $1.6 billion first-lien revolving credit

line, secured by virtually all of the airline’s unencumbered assets, and a $900 million

second-lien term loan.

As required by the Plan of Reorganization approved by the Bankruptcy Court, Delta

cancelled its preplan common stock on April 30, 2007. Holders of preplan common

stock did not receive a distribution of any kind under the Plan of Reorganization. The

company issued new shares of Delta common stock as payment of bankruptcy claims

and as part of a postbankruptcy compensation program for Delta employees. Issued in

May 2007, the new shares were listed on the New York Stock Exchange.

Discussion Questions:

1) To what extent do you believe the factors contributing to the airline’s bankruptcy

were beyond the control of management? To what extent do you believe past airline

mismanagement may have contributed to the bankruptcy?

2) Comment on the fairness of the bankruptcy process to shareholders, lenders,

employees, communities, government, etc. Be specific.

3) Why would lenders be willing to lend to a firm emerging from Chapter 11? How did

the lenders attempt to manage their risks? Be specific.

4) In view of the substantial loss of jobs, as well as wage and benefit reductions, do you

believe that firms should be allowed to reorganize in bankruptcy? Explain your answer.

5) How does Chapter 11 potentially affect adversely competitors of those firms

emerging from bankruptcy? Explain your answer.

Answer:

Pepsi Buys Quaker Oats in a Highly Publicized Food Fight

On June 26, 2000, Phillip Morris, which owned Kraft Foods, announced its planned

$15.9 billion purchase of Nabisco, ranked seventh in the United States in terms of sales

at that time. By combining Nabisco with its Kraft operations, ranked number one in the

United States, Phillip Morris created an industry behemoth. Not to be outdone,

Unilever, the jointly owned BritishDutch giant, which ranked fourth in sales, purchased

Bestfoods in a $20.3 billion deal. Midsized companies such as Campbell’s could no

longer compete with the likes of Nestle, which ranked number three; Proctor &

Gamble, which ranked number two; or Phillip Morris. Consequently, these midsized

firms started looking for partners. Other companies were cutting back. The U.K.’s

Diageo, one of Europe’s largest food and beverage companies, announced the

restructuring of its Pillsbury unit by cutting 750 jobs10% of its workforce. PepsiCo,

ranked sixth in U.S. sales, spun off in 1997 its Pizza Hut, KFC, and Taco Bell restaurant

holdings. Also, eighth-ranked General Mills spun off its Red Lobster, Olive Garden,

and other brand-name stores in 1995. In 2001, Coca-Cola announced a reduction of

6000 in its worldwide workforce.

As one of the smaller firms in the industry, Quaker Oats faced a serious problem: it was

too small to acquire other firms in the industry. As a result, they were unable to realize

the cost reductions through economies of scale in production and purchasing that their

competitors enjoyed. Moreover, they did not have the wherewithal to introduce rapidly

new products and to compete for supermarket shelf space. Consequently, their revenue

and profit growth prospects appeared to be limited.

Despite its modest position in the mature and slow-growing food and cereal business,

Quaker Oats had a dominant position in the sports drink marketplace. As the owner of

Gatorade, it controlled 85% of the U.S. market for sports drinks. However, its

penetration abroad was minimal. Gatorade was the company’s cash cow. Gatorade’s

sales in 1999 totaled $1.83 billion, about 40% of Quaker’s total revenue. Cash flow

generated from this product line was being used to fund its food and cereal operations.

Gatorade’s management recognized that it was too small to buy other food companies

and therefore could not realize the benefits of consolidation.

After a review of its options, Quaker’s board decided that the sale of the company

would be the best way to maximize shareholder value. This alternative presented a

serious challenge for management. Most of Quaker’s value was in its Gatorade product

line. It quickly found that most firms wanted to buy only this product line and leave the

food and cereal businesses behind. Quaker’s management reasoned that it would be in

the best interests of its shareholders if it sold the total company rather than to split it

into pieces. That way they could extract the greatest value and then let the buyer decide

what to do with the non-Gatorade businesses. In addition, if the business remained

intact, management would not have to find some way to make up for the loss of

Gatorade’s substantial cash flow. Therefore, Quaker announced that it was for sale for

$15 billion. Potential suitors viewed the price as very steep for a firm whose businesses,

with the exception of Gatorade, had very weak competitive positions. Pepsi was the

first to make a formal bid for the firm, quickly followed by Coca-Cola and Danone.

By November 21, 2000, Coca-Cola and PepsiCo were battling to acquire Quaker. Their

interest stemmed from the slowing sales of carbonated beverages. They could not help

noticing the explosive growth in sports drinks. Not only would either benefit from the

addition of this rapidly growing product, but they also could prevent the other from

improving its position in the sports drink market. Both Coke and PepsiCo could boost

Gatorade sales by putting the sports drink in vending machines across the country and

selling it through their worldwide distribution network.

PepsiCo’s $14.3 billion fixed exchange stock bid consisting of 2.3 shares of its stock for

each Quaker share in early November was the first formal bid Quaker received.

However, Robert Morrison, Quaker’s CEO, dismissed the offer as inadequate. Quaker

wanted to wait, since it was expecting to get a higher bid from Coke. At that time, Coke

seemed to be in a better financial position than PepsiCo to pay a higher purchase price.

Investors were expressing concerns about rumors that Coke would pay more than $15

billion for Quaker and seemed to be relieved that PepsiCo’s offer had been rejected.

Coke’s share price was falling and PepsiCo’s was rising as the drama unfolded. In the

days that followed, talks between Coke and Quaker broke off, with Coke’s board

unwilling to support a $15.75 billion offer price.

After failing to strike deals with the world’s two largest soft drink makers, Quaker

turned to Danone, the manufacturer of Evian water and Dannon yogurt. Much smaller

than Coca-Cola or PepsiCo, Danone was hoping to hype growth in its healthy nutrition

and beverage business. Gatorade would complement Danone’s bottled-water brands.

Moreover, Quaker’s cereals would fit into Danone’s increasing focus on breakfast

cereals. However, few investors believed that the diminutive firm could finance a

purchase of Quaker. Danone proposed using its stock to pay for the acquisition, but the

firm noted that the purchase would sharply reduce earnings per share through 2003.

Danone backed out of the talks only 24 hours after expressing interest, when its stock

got pummeled on the news.

Nearly 1 month after breaking off talks to acquire Quaker Oats because of

disagreements over price, PepsiCo once again approached Quaker’s management. Its

second proposal was the same as its first. PepsiCo was now in a much stronger position

this time, especially because Quaker had run out of suitors. Under the terms of the

agreement, Quaker Oats would be liable for a $420 million breakup fee if the deal was

terminated, either because its shareholders didn’t approve the deal or the company

entered into a definitive merger agreement with an alternative bidder. Quaker also

granted PepsiCo an option to purchase 19.9% of Quaker’s stock, exercisable only if

Quaker is sold to another bidder. Such a tactic sometimes is used in conjunction with a

breakup fee to discourage other suitors from making a bid for the target firm.

With the purchase of Quaker Oats, PepsiCo became the leader of the sports drink

market by gaining the market’s dominant share. With more than four-fifths of the

market, PepsiCo dwarfs Coke’s 11% market penetration. This leadership position is

widely viewed as giving PepsiCo, whose share of the U.S. carbonated soft drink market

is 31.4% as compared with Coke’s 44.1%, a psychological boost in its quest to

accumulate a portfolio of leading brands.

Discussion Questions:

1) What factors drove consolidation within the food manufacturing industry? Name

other industries that are currently undergoing consolidation?

2) Why did food industry consolidation prompt Quaker to announce that it was for sale?

3) Why do you think Quaker wanted to sell its consolidated operations rather than to

divide the company into the food/cereal and Gatorade businesses?

4) Under what circumstances might the Quaker shareholder have benefited more if

Quaker had sold itself in pieces (i.e., food/cereal and Gatorade) rather than in total?

5) Do you think PepsiCo may have been willing to pay such a high price for Quaker for

reasons other than economics? Do you think these reasons make sense? Explain your

answer.

Answer:

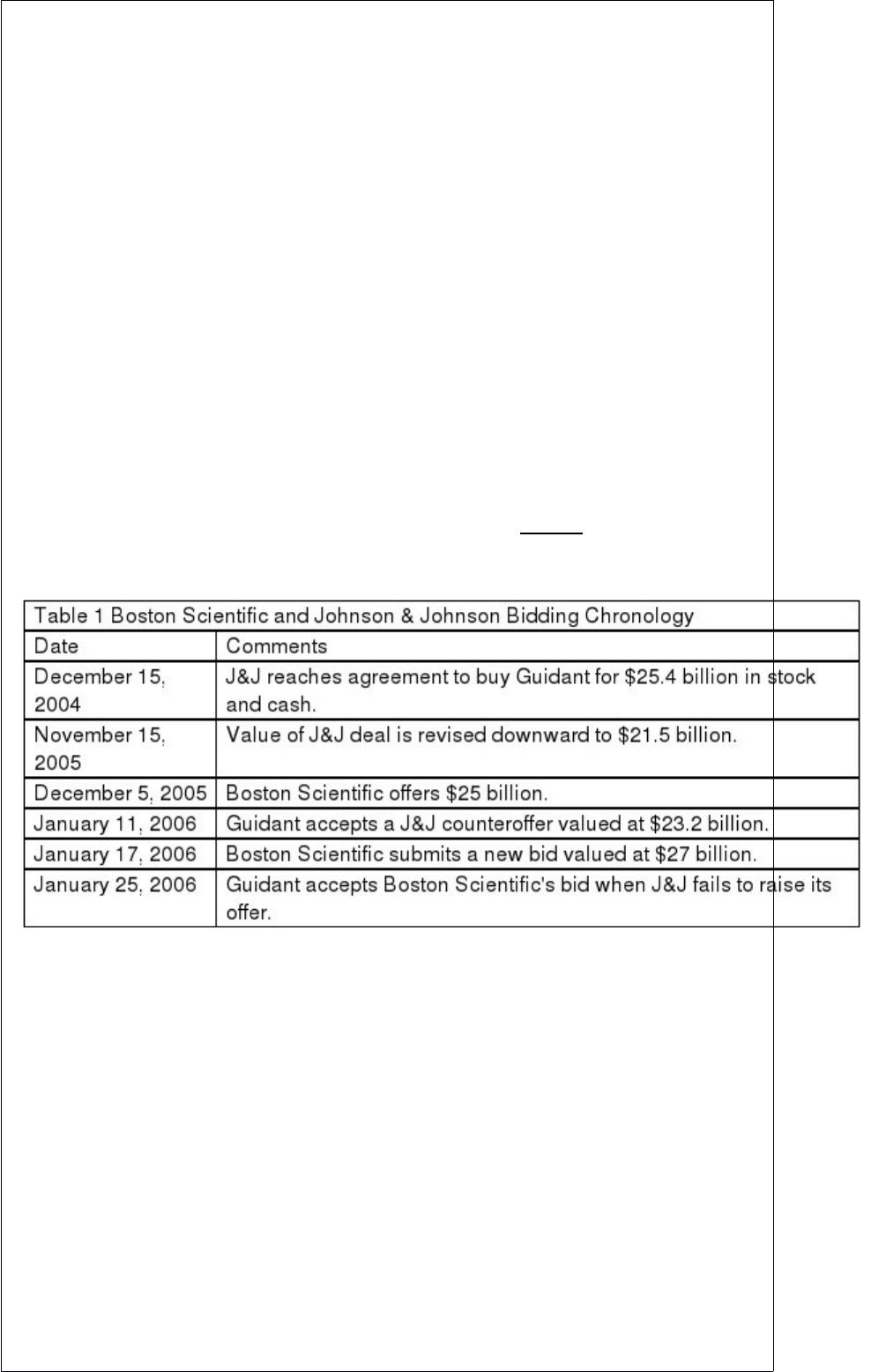

Boston Scientific Overcomes Johnson & Johnson to Acquire GuidantA Lesson in

Bidding Strategy

Johnson & Johnson, the behemoth American pharmaceutical company, announced an

agreement in December 2004 to acquire Guidant for $76 per share for a combination of

cash and stock. Guidant is a leading manufacturer of implantable heart defibrillators

and other products used in angioplasty procedures. The defibrillator market has been

growing at 20 percent annually, and J&J desired to reenergize its slowing growth rate

by diversifying into this rapidly growing market. Soon after the agreement was signed,

Guidant’s defibrillators became embroiled in a regulatory scandal over failure to inform

doctors about rare malfunctions. Guidant suffered a serious erosion of market share

when it recalled five models of its defibrillators.

The subsequent erosion in the market value of Guidant prompted J&J to renegotiate the

deal under a material adverse change clause common in most M&A agreements. J&J

was able to get Guidant to accept a lower price of $63 a share in mid-November.

However, this new agreement was not without risk.

The renegotiated agreement gave Boston Scientific an opportunity to intervene with a

more attractive informal offer on December 5, 2005, of $72 per share. The offer price

consisted of 50 percent stock and 50 percent cash. Boston Scientific, a leading supplier

of heart stents, saw the proposed acquisition as a vital step in the company’s strategy of

diversifying into the high-growth implantable defibrillator market.

Despite the more favorable offer, Guidant’s board decided to reject Boston Scientific’s

offer in favor of an upwardly revised offer of $71 per share made by J&J on January 11,

2005. The board continued to support J&J’s lower bid, despite the furor it caused among

big Guidant shareholders. With a market capitalization nine times the size of Boston