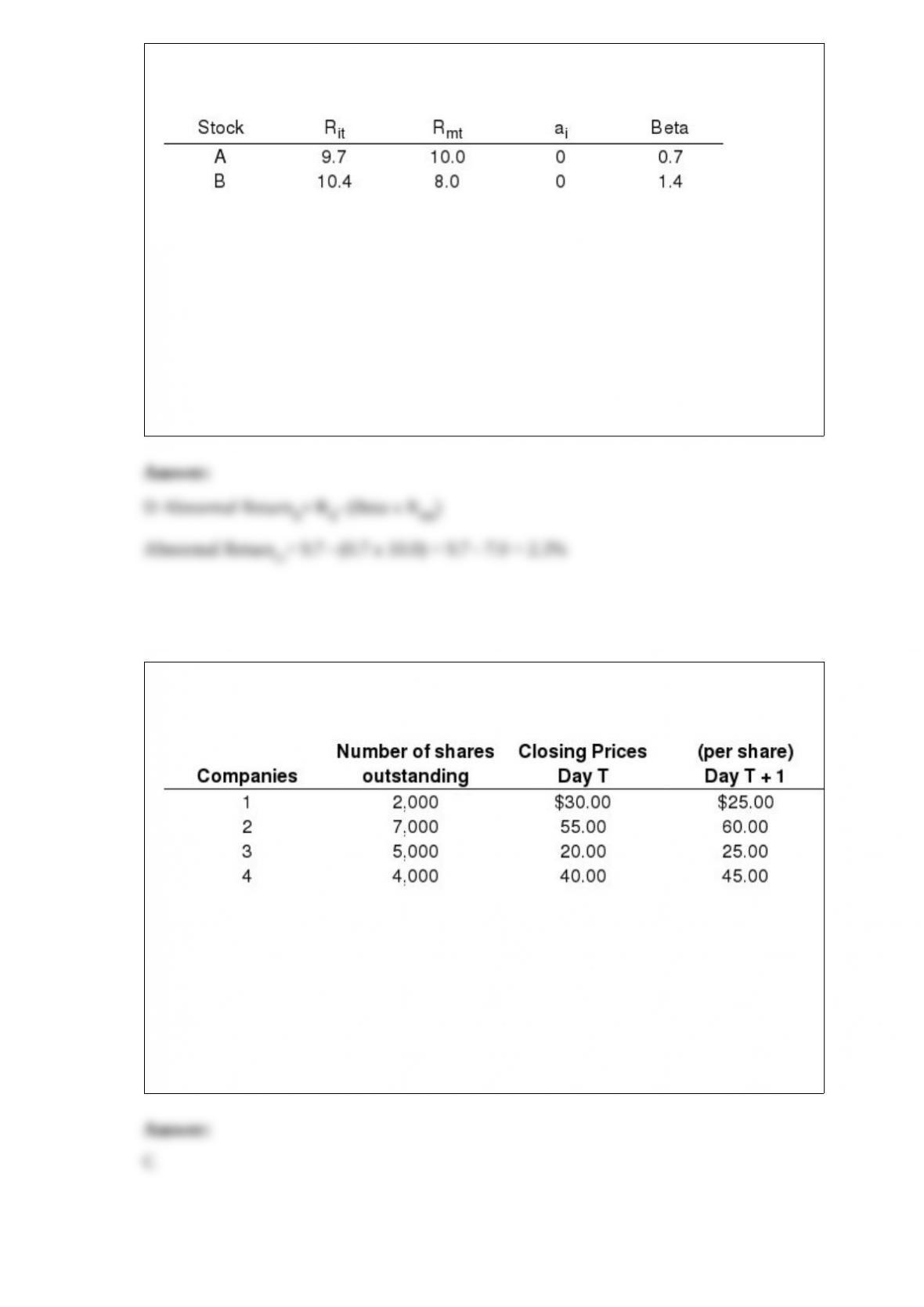

1) Exhibit 6.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Rit= return for stock i during period t

Rmt= return for the aggregate market during period t

Refer to Exhibit 6.6. What is the abnormal rate of return for Stock A when you consider

its systematic risk measure (beta)?

a.-2.3%

b.-0.3%

c.0.3%

d.2.3%

e.3.0%

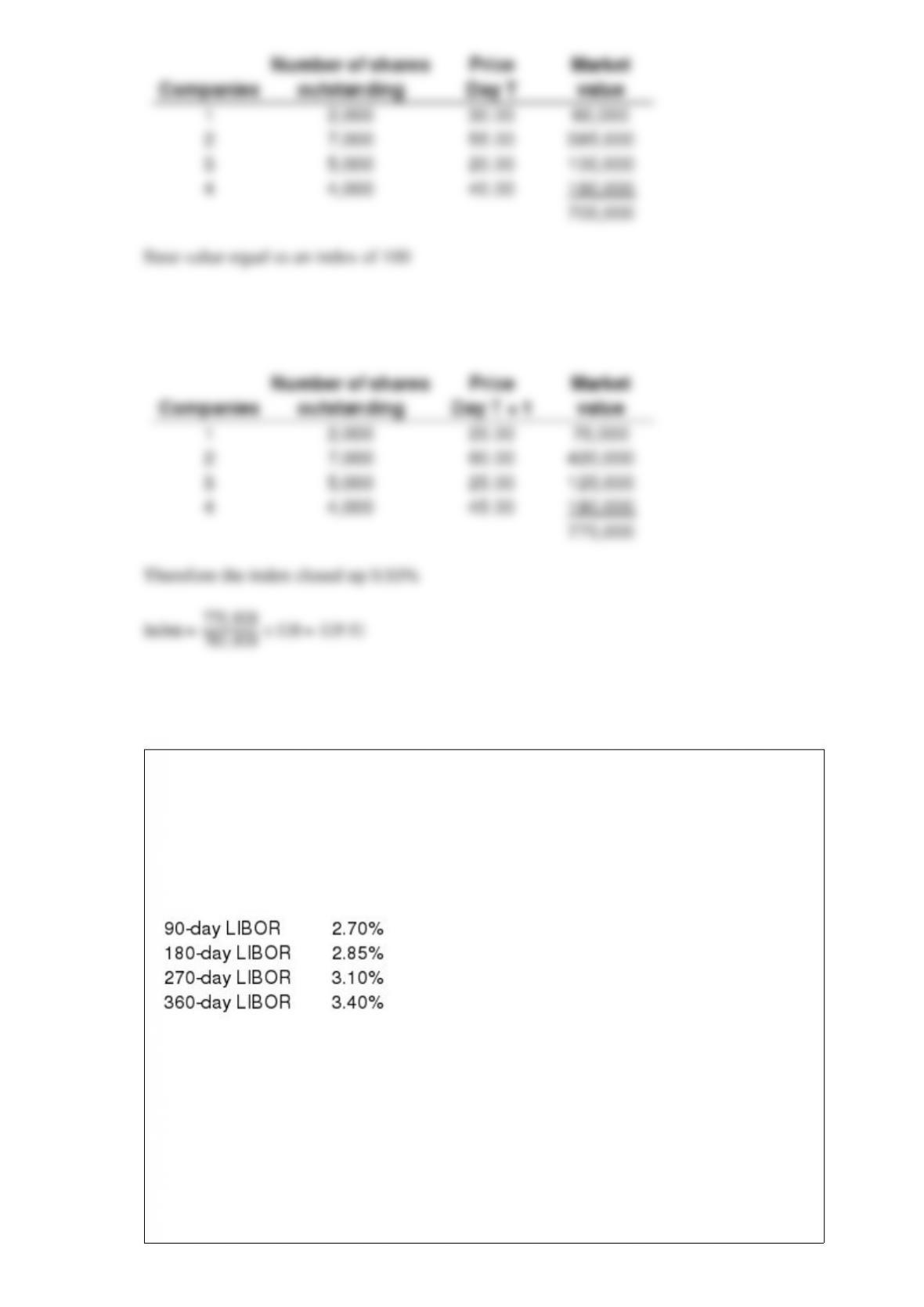

2) Exhibit 5.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 5.1. For a value-weighted series, assume that Day T is the base period

and the base value is 100. What is the new index value for Day T + 1 and what is the

percentage change in the index from Day T?

a.106.33, 6.33%

b.107.48, 7.48%

c.109.93, 9.93%

d.108.7, 8.7%

e.None of the above

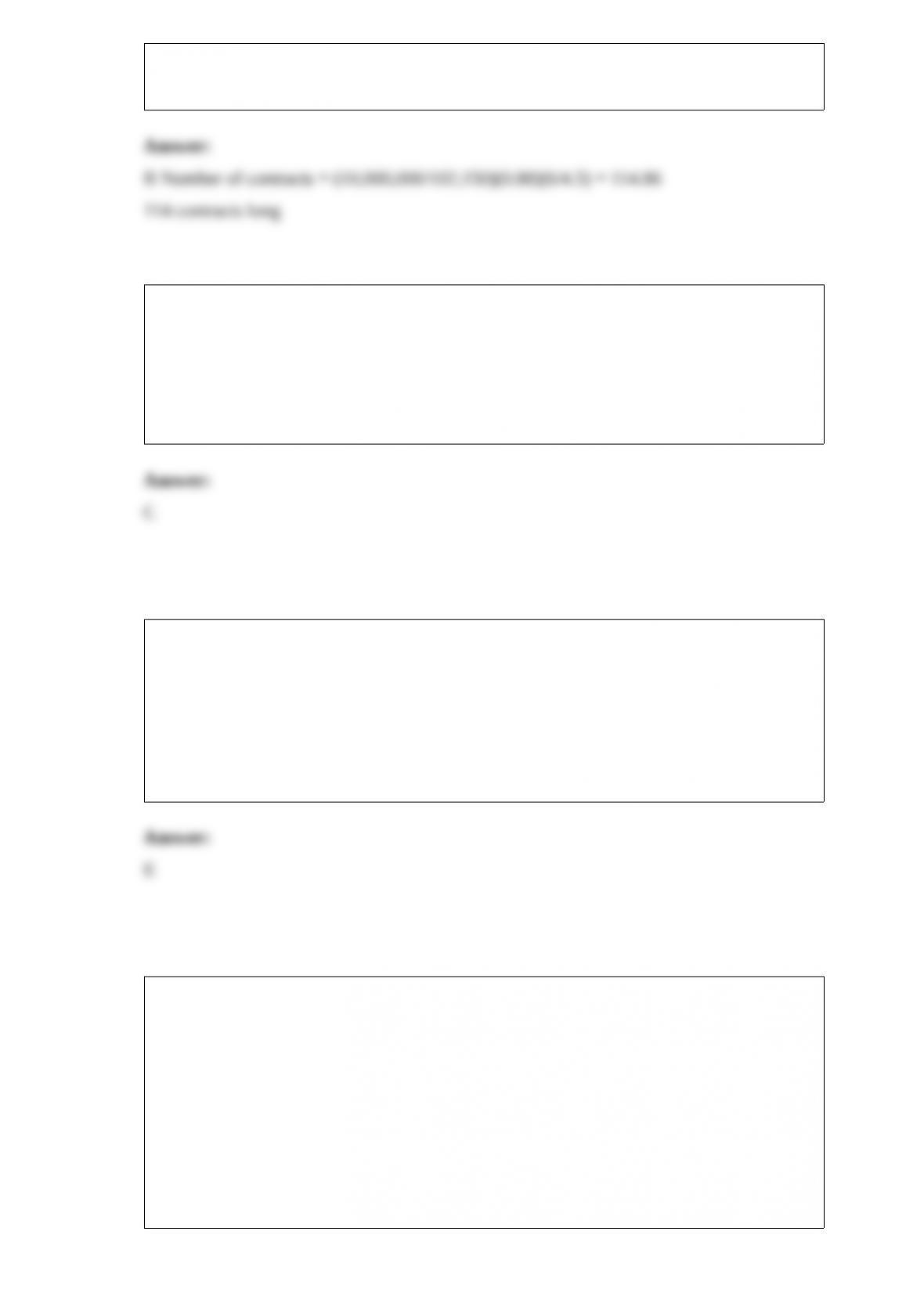

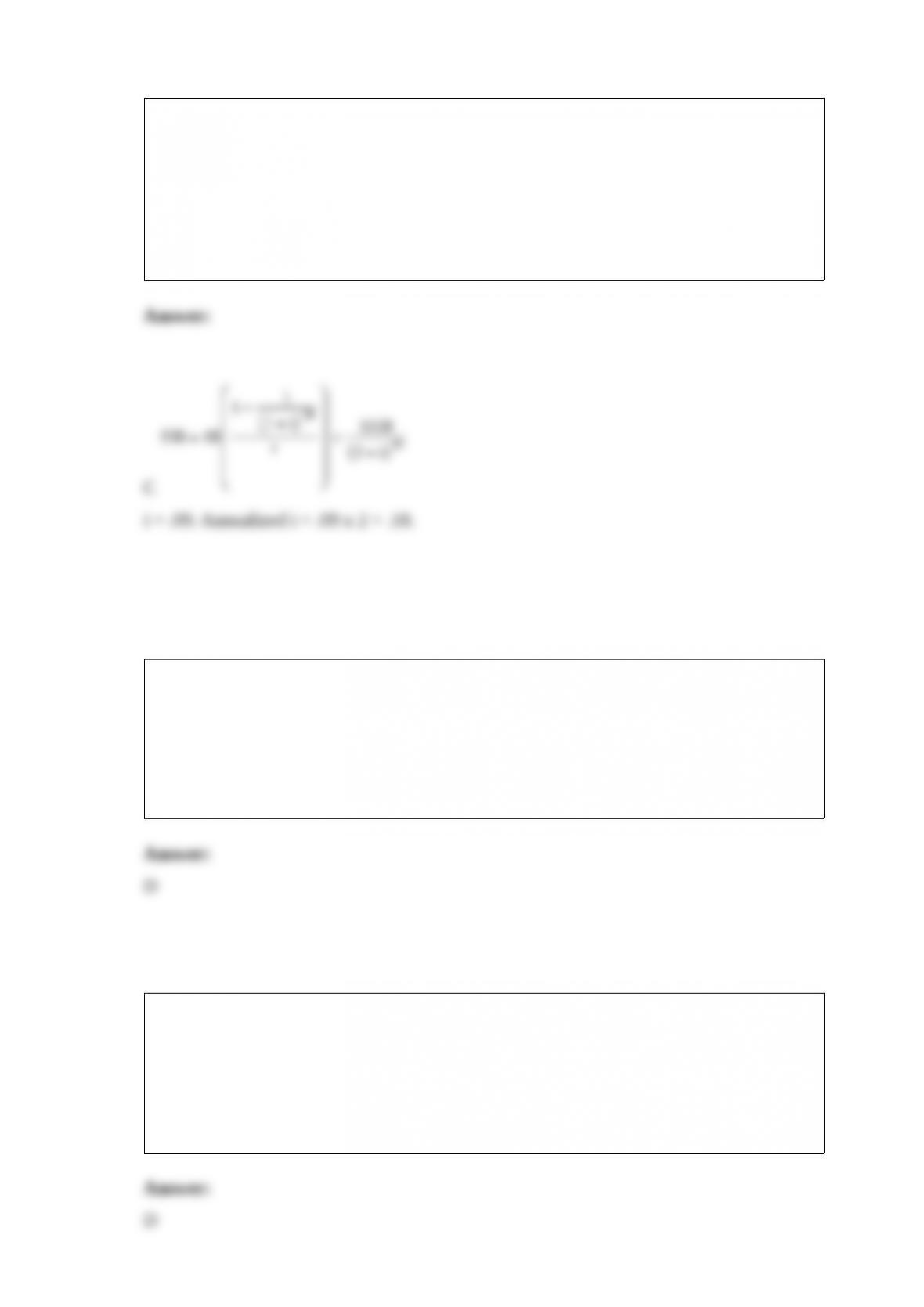

3) Exhibit 21.12

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Suppose you are a loan officer for a commercial bank and one of your clients has just

approached you about a one-year loan for $4,000,000. Interest on the new loan will be

paid at the end of each quarter based on the prevailing level of LIBOR at the beginning

of each quarter. The LIBOR yield curve in the cash market is as follows:

A bond portfolio manager expects a cash inflow of $10,000,000. The manager plans to

hedge potential risk with a Treasury futures contract with a value of $102,150. The

conversion factor between the CTD and the bond specified in the Treasury futures

contract is 0.88. The duration of bond portfolio is 6 years, and the duration of the CTD

bond is 4.5 years. Indicate the number of contracts required and whether the position to

be taken is short or long.

a. 114 contracts short

b. 114 contracts long

c. 60 contract short

d. 60 contracts long

e. None of the above

4) A real option is a reference to

a. Options on physical assets.

b. Options on commodity futures.

c. The value of flexibility embedded in a real asset.

d. a and b.

e. b and c.

5) Treynor showed that rational, risk averse investors always prefer portfolio possibility

lines that have

a. Zero slopes.

b. Slightly negative slopes.

c. Highly negative slopes.

d. Slightly positive slopes.

e. Highly positive slopes.

6) Exhibit 12.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The aggregate market currently has a retention ratio of 60 percent, a required rate of

return of 12 percent, and an expected growth rate for dividends of 4 percent.

What is the current earnings multiplier?

a. 2.5

b. 5.0

c. 7.5

d. 10.0

e. 12.5

7) Exhibit 14.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following information on Kayray Corporation. Your ultimate

objective is to calculate the EVA for the firm.

Calculate the firm’s EVA.

a. 85.2

b. 72.3

c. 65.8

d. 89.5

e. 78.2

8) A foreign currency option contract traded on U.S. exchanges allows for the sale or

purchase of a set amount of

a. U.S. currency at a floating exchange rate

b. U.S. currency at a fixed exchange rate

c. Foreign currency at a floating exchange rate

d. Foreign currency at a fixed exchange rate

e. None of the above

9) Suppose you buy a round lot of HS Inc. stock on 55% margin when it is selling at

$40 a share. The broker charges a 10 percent annual interest rate and commissions are 4

percent of the total stock value on both the purchase and the sale. If at year end you

receive a $0.90 per share dividend and sell the stock for 35 5/8, what is your rate of

return on the investment?

a.-35.17%

b.-21.84%

c.14.74%

d.21.84%

e.35.17%

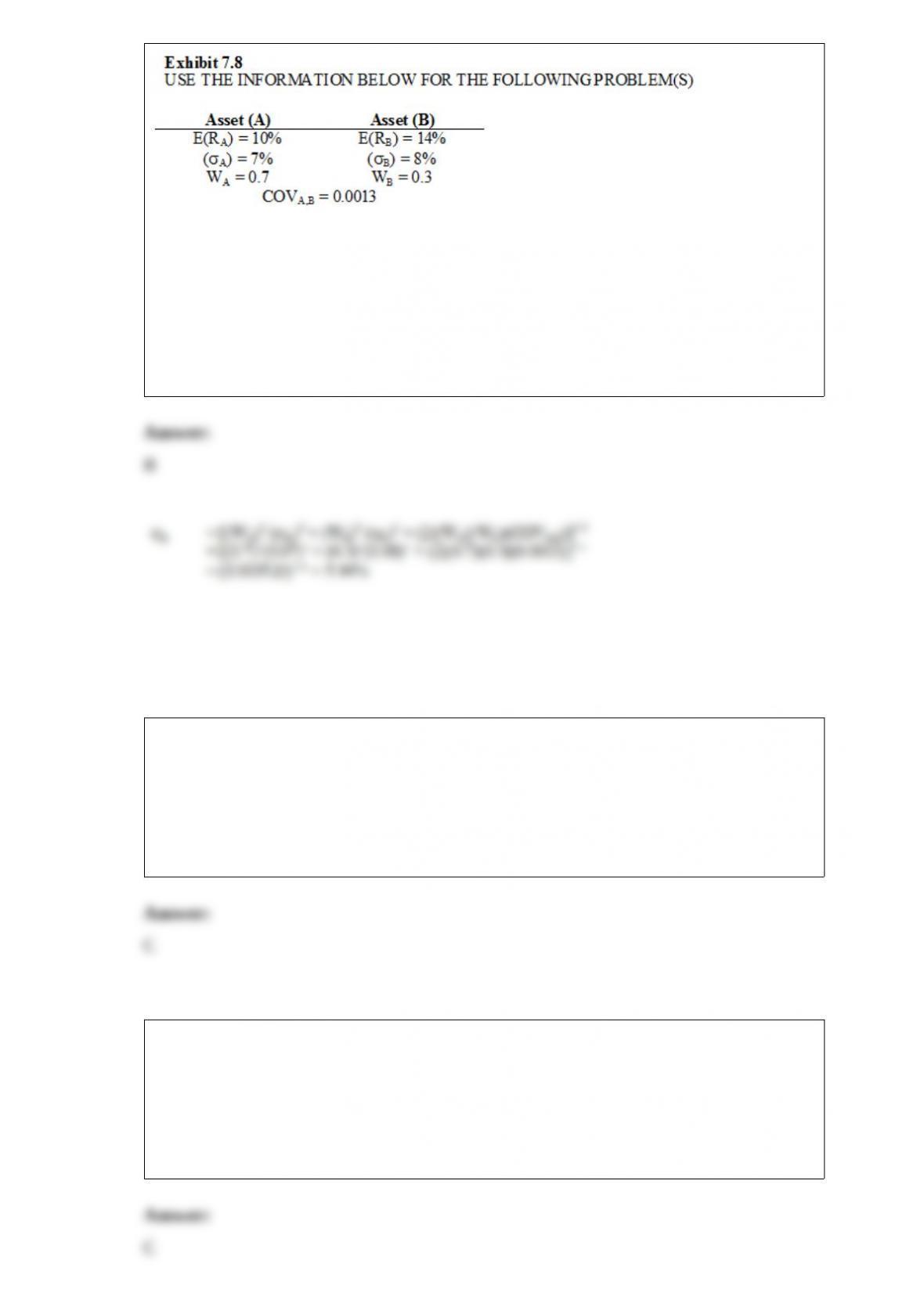

10)

Refer to Exhibit 7.8. What is the standard deviation of this portfolio?

a. 4.51%

b. 5.94%

c. 6.75%

d. 7.09%

e. 8.62%

11) Which of the following is not true regarding defined contribution pension plans?

a. Employees make regular contributions to the plan.

b. Employers make regular contributions to the plan.

c. The employer bears all of the investment risk.

d. Benefits are directly related to the earnings of the funds investments.

e. The number of defined contribution plans is increasing.

12) A block trade is one which involves a minimum of

a.1,000 shares.

b.5,000 shares.

c.10,000 shares.

d.100,000 shares.

e.1,000,000 shares.

13) Suppose you have a 12%, 20 year bond traded at $850. If it is callable in 5 years at

$1,100, what is the bond’s yield to call? Interest is paid semiannually.

a. 8%

b. 9.0%

c. 18.0%

d. 9.4%

e. 16.5%

14) A contrary opinion technician would buy stock when mutual funds

a. Are at the market peak

b. Are fully invested

c. Have a cash ratio approaching 4 percent

d. Have a cash ratio approaching 11 percent

e. None of the above

15) Which of the following is not a value added performance measure?

a. Economic Value Added (EVA)

b. Market Value Added (MVA)

c. Franchise Factor

d. Company Value Added (CVA)

e. None of the above (that is, all are value added performance measures)

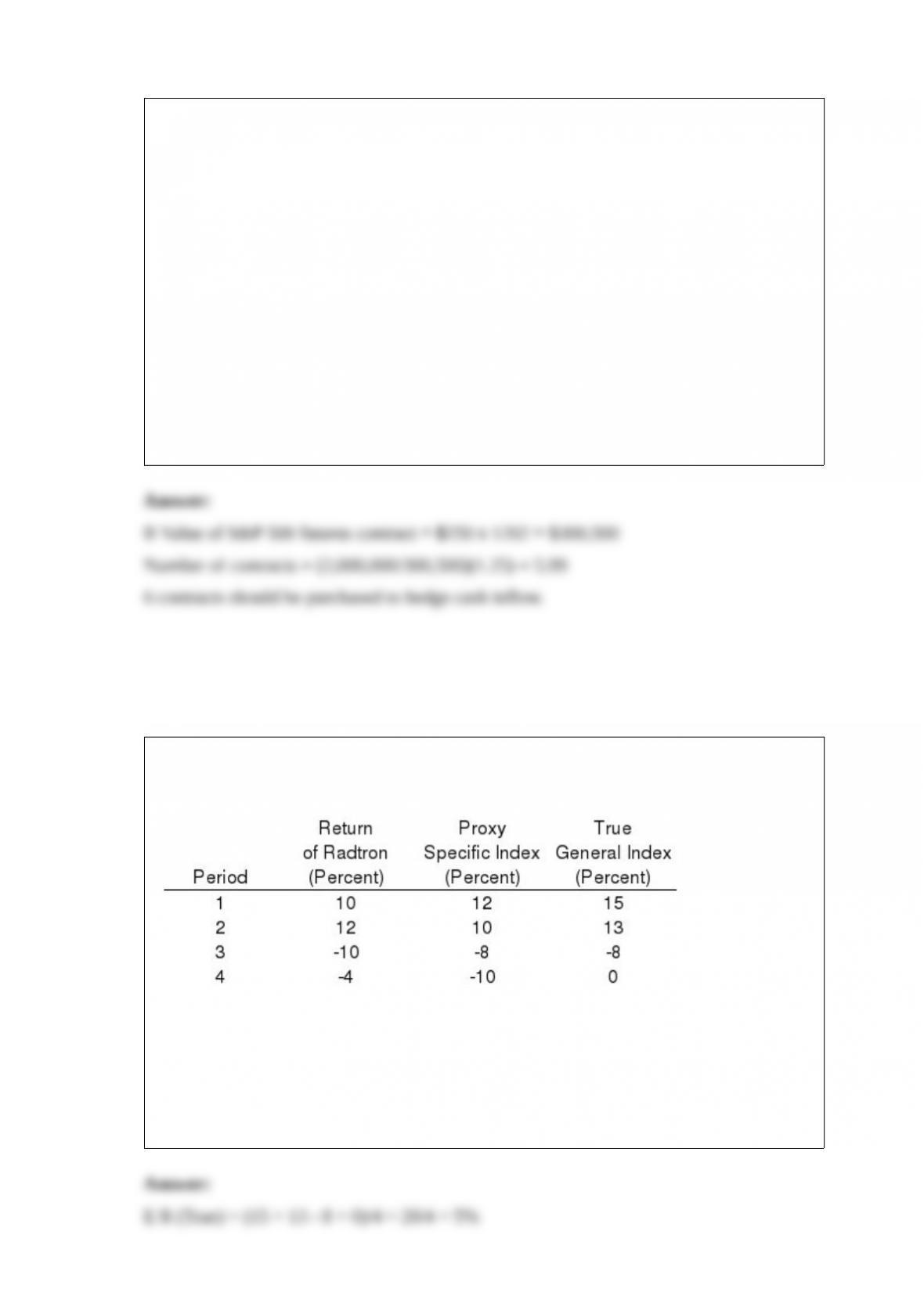

16) Exhibit 21.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

As a portfolio manager, you are responsible for a $150 million portfolio, 90 percent of

which is invested in equities, with a portfolio beta of 1.25. You are utilizing the S&P

500 as your passive benchmark. Currently the S&P 500 is valued at 1202. The value of

the S&P 500 futures contract is equal to $250 times the value of the index. The beta of

the futures contract is 1.0.

If you anticipate a cash inflow of $2 million next week, how many futures contracts

should you buy or sell in order to mitigate the effect of this inflow on the portfolio’s

performance (rounded to the nearest integer)?

a. Sell 6 contracts

b. Buy 6 contracts

c. Sell 8 contracts

d. Buy 8 contracts

e. None of the above

17) Exhibit 8.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 8.3. The average true return is

a. 1%

b. 2%

c. 3%

d. 4%

e. 5%

18) Consider a bond with a duration of 6 years having a yield to maturity of 8% and

interest rates are expected to rise by 50 basis points. What is the percentage change in

the price of the bond?

a. 2.88%

b. 3.45%

c. -3.89%

d. -3.45%

e. -2.88%

19) For an investor with a time horizon of 6 to 10 years and lower risk tolerance, an

appropriate asset allocation strategy would be

a.100% stocks

b.100% cash

c.30% cash, 50% bonds, and 20% stocks

d.10% cash, 30% bonds, and 60% stocks

e.100% bonds

20) The sustainable growth rate can be calculated by taking the dividend payout ratio

time return on equity (ROE).

21) The correlation coefficient between the market return and a risk-free asset would

22) Convexity is a measure of how much a bond’s price-yield curve deviates from the

linear approximation of that curve.

23) The current ratio, receivables turnover and total asset turnover are measures of

internal liquidity.

24) In a three asset portfolio the standard deviation of the portfolio is one third of the

square root of the sum of the individual standard deviations.

25) A floor agreement is a series of cash settlement interest rate options, typically based

on LIBOR.

26) An offensive competitive strategy involves positioning the firm to deflect the effect

of the competitive forces in the industry.

27) A futures contract is an agreement between a trader and the clearinghouse of the

exchange for delivery of an asset in the future.

28) Investment planning is complicated by the tax code.