A company’s trial balance included the following account balances at year-end:

The amount of net sales reported on the income statement would be:

A) $114,400.

B) $128,400.

C) $112,000.

D) $111,400.

Which of the following will happen if the accrual adjusting entry is not made for

revenue earned but not yet recorded?

A) Assets will be understated and revenues will be overstated.

B) Revenues will be understated and assets will be overstated.

C) Both revenues and assets will be overstated.

D) Both revenues and assets will be understated.

A company started the year with $1,500 of supplies on hand. During the year the

company purchased additional supplies of $800 and recorded them as increase to the

supplies asset. At the end of the year the company determined that only $300 of

supplies are still on hand. What is the adjusting journal entry to be made at the end of

the period?

A) Debit Supplies Expense and credit Supplies for $2,000

B) Debit Supplies and credit Supplies Expense for $300

C) Debit Supplies Expense and credit Supplies for $1,200

D) Debit Supplies and credit Supplies Expense for $1,000

Which of the following represents a cash inflow from financing activities?

A) Issuing stock in exchange for another company’s stock.

B) Paying a bond’s face value at maturity.

C) Issuing long-term bonds at a discount.

D) Receiving interest on promissory notes.

A company has $72,500 of inventory at the beginning of the year and $65,500 at the

end of the year. Sales revenue is $986,400, cost of goods sold is $572,700, and net

income is $124,200 for the year. The inventory turnover ratio is closest to:

A) 1.8.

B) 8.3.

C) 6.0.

D) 14.3.

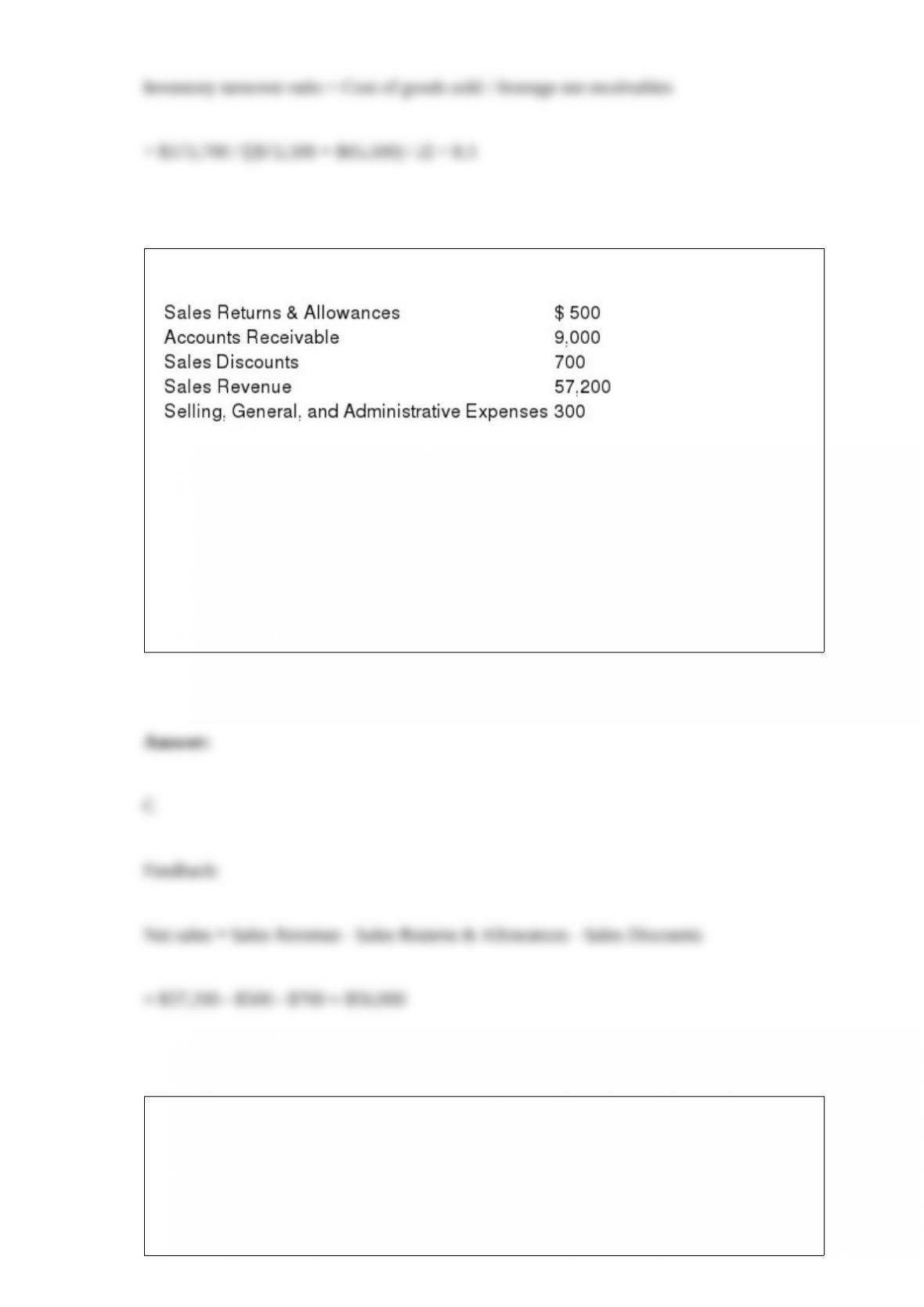

The following account balances appeared on the company’s trial balance at year-end:

The amount of net sales reported on the income statement would be:

A) $57,200.

B) $64,200.

C) $56,000.

D) $55,700.

All other things being equal, a company is better off when its receivable turnover ratio:

A) and its days-to-collect measure are both low.

B) is high and its days-to-collect measure is low.

C) and its days-to-collect measure are both high.

D) is low and its days-to-collect measure is high.

A company has net sales of $612,850 and cost of goods sold of $441,252. The

company’s gross profit percentage is:

A) 72%.

B) 0.28%.

C) 38.9%.

D) 28%.

Company X has net sales revenue of $780,000, cost of goods sold of $343,200, and all

other expenses of $327,600. The net profit margin is closest to:

A) 0.32.

B) 0.56.

C) 0.86.

D) 0.14.

Jim’s Gymnastics Training’s operations for the month of October are summarized as

follows:

A. Provided $5,000 of training to students on account.

B. Received $4,000 cash from students for training provided in October.

C. Received $1,000 cash for training to be provided in November.

D. Received $3,000 cash from students on account for training provided in September.

E. Paid September’s gym rental bill on account in the amount of $1,000.

F. Received October’s rental bill of $1,500; set it aside.

Required:

Part a. Determine the net income for October using the cash basis of accounting.

Part b. Determine the net income for October using the accrual basis of accounting.

Your company sells $50,000 of bonds for an issue price of $48,000. Which of the

following statements is correct?

A) The bond sold at a price of 96, implying a discount of $4,000.

B) The bond sold at a price of 48, implying a premium of $2,000.

C) The bond sold at a price of 48, implying a premium of $4,000.

D) The bond sold at a price of 96, implying a discount of $2,000.

When a company sells equipment for cash on a date other than the last day of the

accounting period, it must:

A) record Depreciation Expense for the entire accounting period during which the

equipment is sold.

B) record the disposal by reducing the Equipment account and increasing a revenue

account; a gain or loss is reported if the decrease and increase are not equal.

C) first record Depreciation Expense for the period up to the date of sale, and then

record the disposal by increasing Cash and decreasing both Equipment and

Accumulated Depreciation; a gain or loss is reported if the proceeds from the sale do

not equal the asset’s book value.

D) record Accumulated Depreciation for the entire current accounting period.

A company issues 100,000 shares of preferred stock for $40 a share. The stock has

fixed annual dividend rate of 5% and a par value of $3 per share. If sufficient dividends

are declared, preferred stockholders can anticipate receiving dividends of:

A) $5,000 each year.

B) $15,000 each year.

C) 5% of net income each year.

D) $3 per share.