1) The largest asset on the typical securities firms’ balance sheet in 2012 was

A.securities purchased under agreements to resell.

B.long positions in securities and commodities.

C.reverse repurchase agreements.

D.repurchase agreements.

E.cash.

2) For a nine-month maturity bucket, the bank has _________________ in fixed-rate

assets and _________________ in fixed-rate liabilities.

A.$425; $285

B.$285; $425

C.$285; $359

D.$359; $285

E.$250; $66

3) Altman’s Z-score model is Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + 1.0X5

X1 = Working Capital/Total Assets

X2 = Retained Earnings/Total Assets

X3 = EBIT/Total Assets

X4 = Market Value Equity/Book Value Long-Term Debt

X5 = Sales/Total Assets

Using the Altman’s Z model, Big Valley’s Z-score is

A.3.22.

B.2.88.

C.2.65.

D.2.11.

E.1.85.

4) The main advantage of a profit sharing Keogh plan over a money sharing Keogh plan

is that profit sharing plans

A.are eligible for PBGC insurance and money sharing plans are not.

B.have higher maximum contributions than money sharing plans.

C.can have contributions that vary from year to year with profits, while money sharing

plan contributions are fixed.

D.profit sharing Keogh plans are eligible for PBGC insurance and money sharing plans

are not, and they have higher maximum contributions than money sharing plans.

E.none of the options

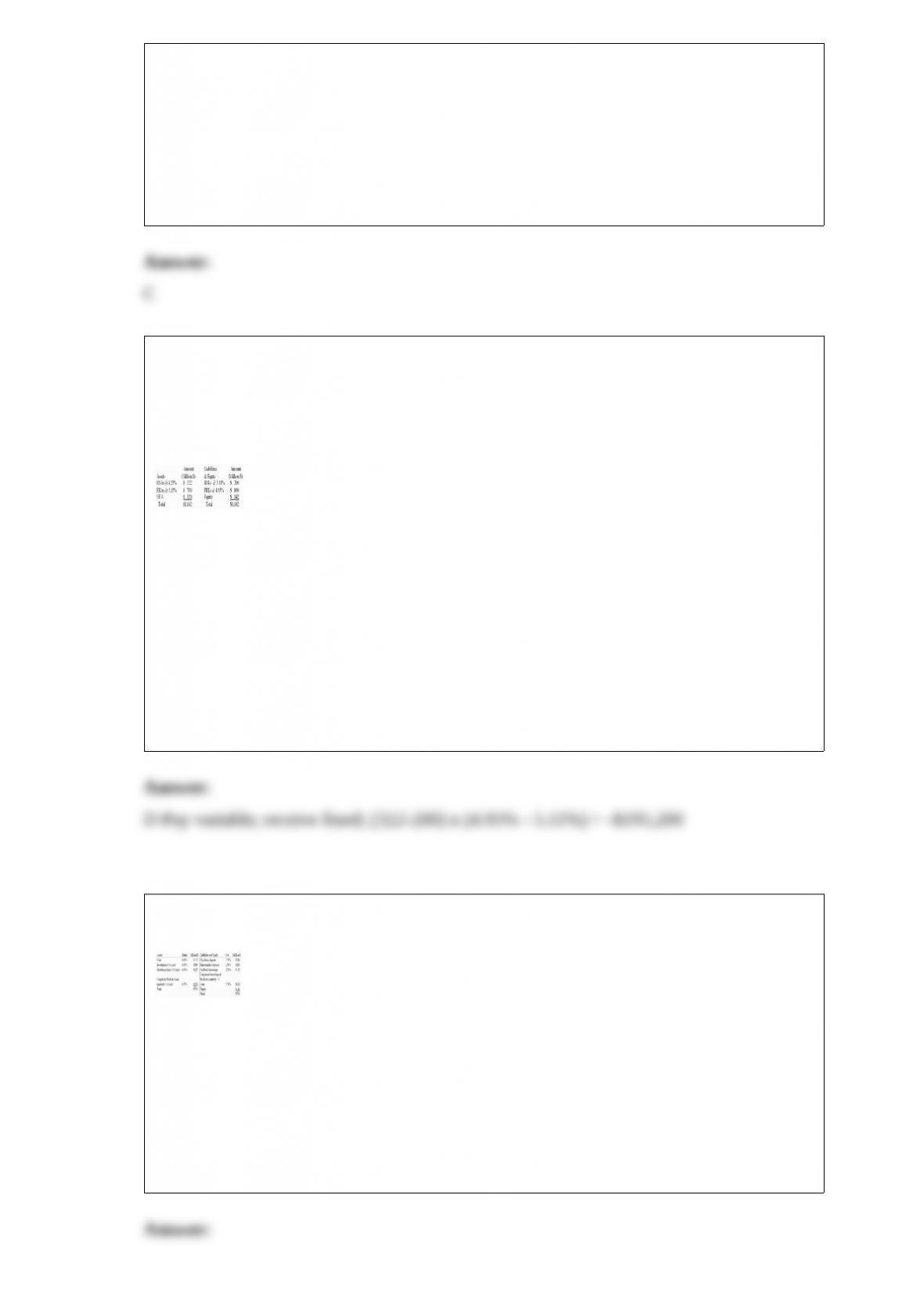

5) After conducting a rate-sensitive analysis, a bank finds itself with the following

amounts of rate-sensitive assets and liabilities (RSAs and RSL) and fixed-rate assets

and liabilities (FRAs and FRLs); the rate of return and cost rates on the accounts are

also given:

Suppose the institution wishes to fully hedge the interest rate risk with a swap. A swap

is available with whatever notional principal is needed that pays fixed at 4.95 percent

and pays variable at LIBOR. LIBOR is currently 5.11 percent. By how much would

profits change right now if the bank engages in the swap?

A.$202,600

B.-$202,600

C.$300,000

D.-$195,200

E.$195,200

6) A bank has the following balance sheet:

If the spread effect is zero and all interest rates decline 50 basis points, the bank’s NII

will change by ________________ over the year.

A.$0

B.$400,000

C.-$400,000

D.$700,000

E.-$700,000

7)

If FNBNA is expecting a $15 million net deposit drain and the securities liquidity index

is 0.98, how many securities would have to be liquidated if the bank used only its

securities to fund the expected deposit drain?

A.$15,000,000

B.$16,444,331

C.$15,600,000

D.$15,306,122

E.$16,772,345

8) Darby Minerals wants to hire an investment banker to sell two million shares of

stock to the public. Darby is considering using either a firm commitment or a best

efforts offering.

9) A three-class (Class A, B, and C) sequential pay CMO starts with an $80 million

principal amount in each class. The mortgages in the pool have a 7 percent interest rate.

The CMO classes receive monthly payments. During the first month, $1 million in

interest is received from mortgage holders and $1.5 million in principal. What principal

amounts are outstanding for each class during the second month? How will this affect

the total payment each class receives? Explain.