1) in germany the corporate board is

a.legally charged with representing the interests of shareholders exclusively

b.legally charged with looking after the interests of stakeholders (e.g., workers,

creditors, etc.) in general, not just shareholders

c.legally charged as a supervisory board only

d.legally charged as a management board only

2) for most countries and most firms, the domestic country beta

a.can be no lower than its world beta

b.is normally much smaller than the world beta

c.is normally much much higher than the world beta

d.is exactly equal to the world beta

3) assume the time from acceptance to maturity on a $10,000,000 banker’s acceptance is

90 days. further assume that the importing bank’s acceptance commission is 1 percent

and that the market rate for 90-day b/as is 3.0 percent. the bond equivalent yield that the

bank earns in holding the b/a to maturity is:

a.22.87%

b.1.02%

c.4.06%

d.none of the above

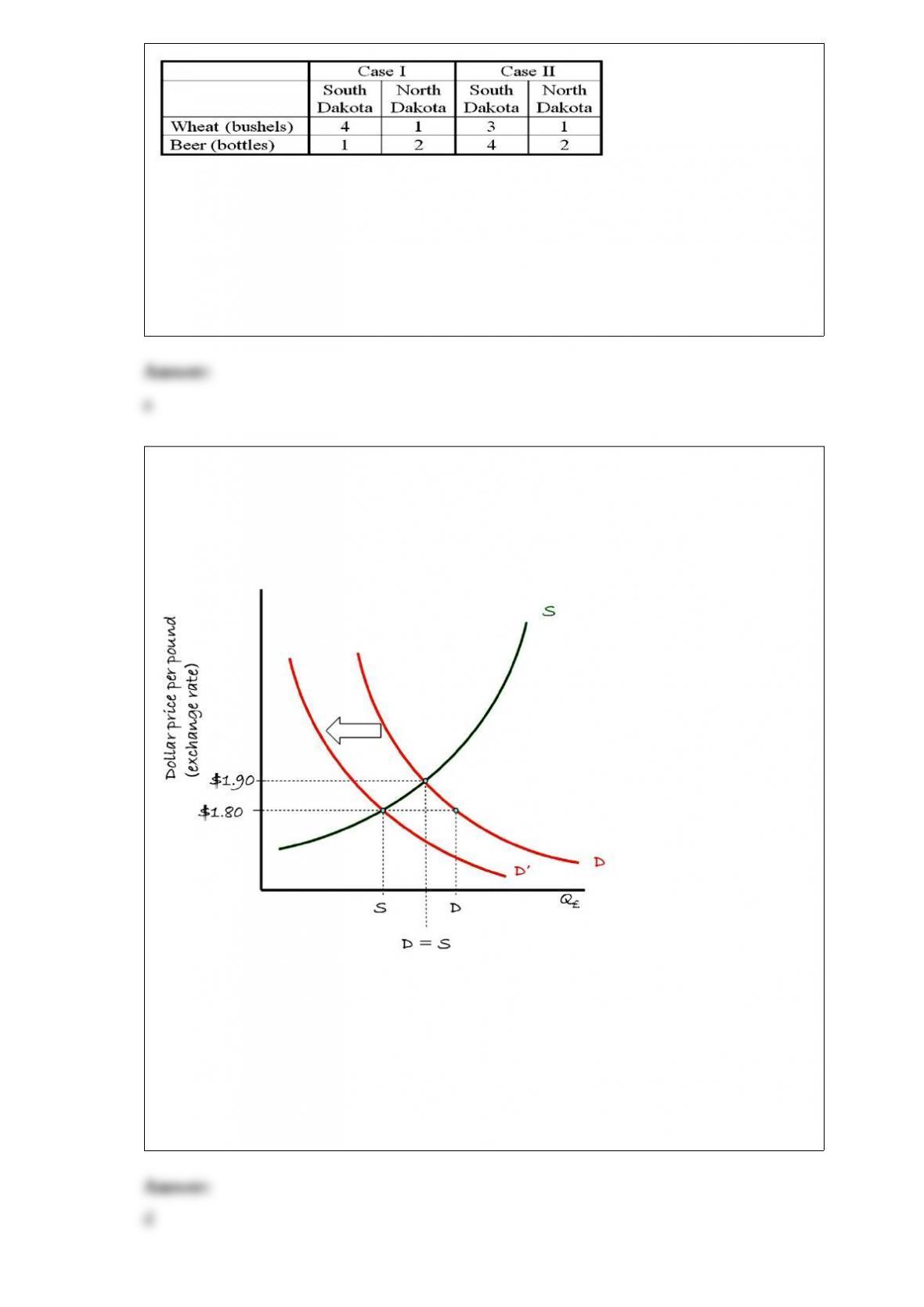

4) the table below shows the bushels of wheat and the bottles of beer that north and

south dakota can produce per day of labor under two different hypothetical situations

(cases i and ii).

which state has a comparative advantage in wheat production in case ii?

a.south dakota

b.north dakota

c.neither state

5) consider the supply-demand framework for the british pound relative to the u.s.

dollar shown in the nearby chart. the exchange rate is currently $1.80 = £1.00. which of

the following is correct?

a.at an exchange rate of $1.80 = £1.00, demand for british pounds exceeds supply

b.at an exchange rate of $1.80 = £1.00, supply for british pounds exceeds demand

c.under a flexible exchange rate regime, the u.s. dollar will depreciate to an exchange

rate of $1.90 = £1.00

d.a and c are correct

6) the monetary system of bimetallism is unstable. due to the fluctuation of the

commercial value of the metals,

a.the metal with a commercial value lower than the currency value tends to be used as

metal and is withdrawn from circulation as money (gresham’s law)

b.the metal with a commercial value higher than the currency value tends to be used as

money (gresham’s law)

c.the metal with a commercial value higher than the currency value tends to be used as

metal and is withdrawn from circulation as money (gresham’s law)

d.none of the above

7) your firm has just issued five-year floating-rate notes indexed to six-month u.s. dollar

libor plus 1/4 percent. what is the amount of the first coupon payment your firm will

pay per u.s. $1,000 of face value, if six-month libor is currently 7.2 percent?

a.$36.00

b.$37.25

c.$74.50

d.none of the above

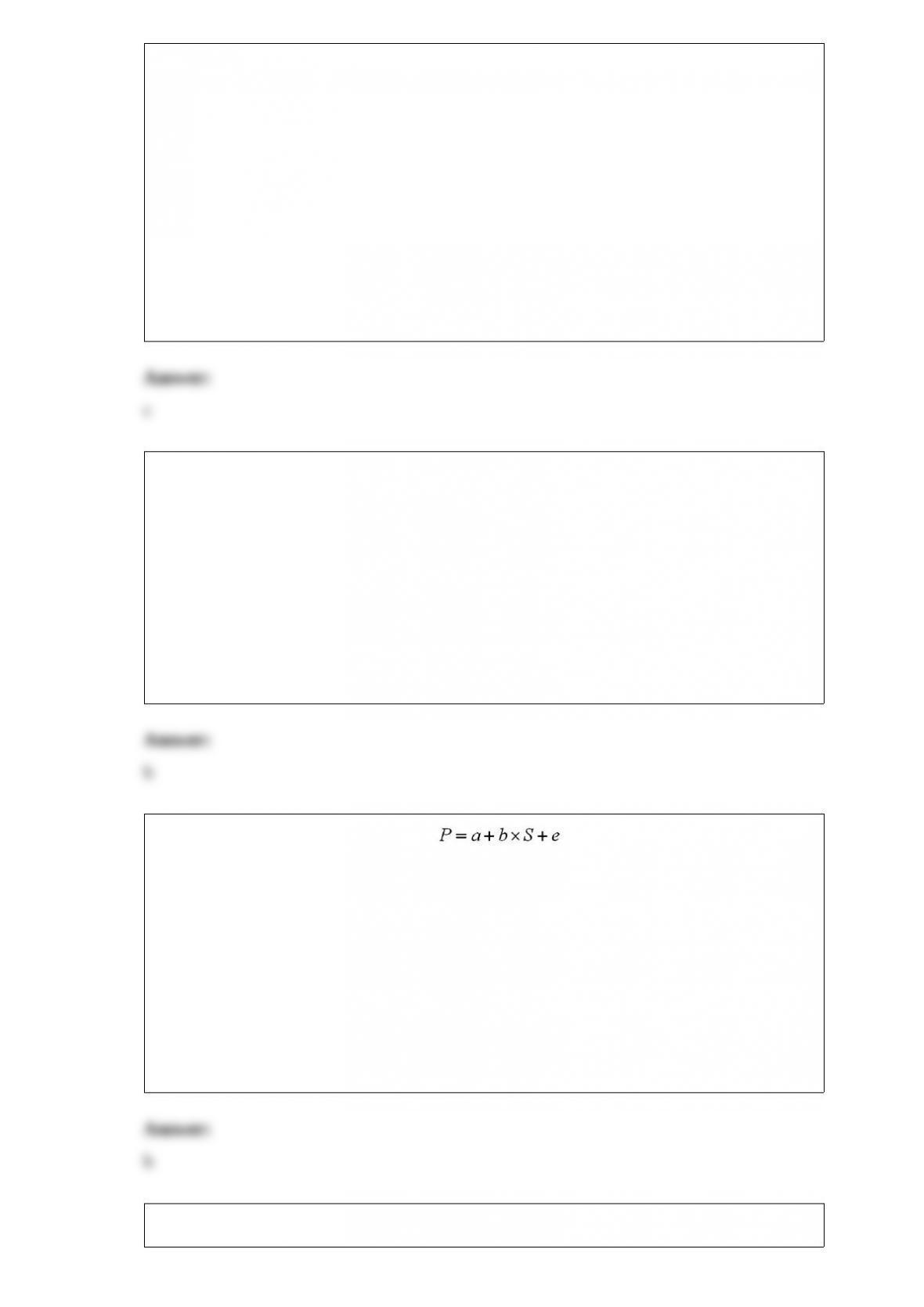

8) on the basis of regression equation we can decompose the variability

of the dollar value of the asset, var(p), into two separate components var(p) = b2 var(s)

+ var(e).

the second term in the right-hand side of the equation, var(e) represents.

a.the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate

b.captures the residual part of the dollar value variability that is independent of

exchange rate movements

c.none of the above

9) the purpose of a withholding tax

a.is to assure the local tax authority that it will receive the tax due on the active income

earned within its tax jurisdiction

b.is to assure the local tax authority that it will receive the tax due on the passive

income earned within its tax jurisdiction

c.is to assure the local tax authority that it will receive the tax due on all income earned

within its tax jurisdiction

d.none of the above

10) a market order

a.is an instruction from a customer to a broker to buy or sell at the best price available

when the order is received (immediately)

b.is an instruction from a customer to a broker to buy or sell in a particular market (e.g.

nyse)

c.is always and everywhere “fill or kill”

d.is always and everywhere “good till cancelled”

11) the entries in the “current account” and the “capital account”, combined together,

can be outlined (in alphabetic order) as:

(i) – direct investment

(ii) – factor income

(iii) – merchandise

(iv) – official transfer

(v) – other capital

(vi) – portfolio investment

(vii) – private transfer

(viii) – services

current account includes

a.(i), (ii), and (iii)

b.(ii), (iii), and (vii)

c.(iv), (v), and (vii)

d.(i), (v), and (vi)

12) the united states withholds ___ of passive income from taxpayers that reside in

countries with which it does not have withholding tax treaties.

a.10%

b.20%

c.30%

d.40%

e.50%

13) which of the following is correct?

a.european options can be exercised early

b.american options can be exercised early

c.asian options can be exercised early

d.all of the above

14) capital export neutrality

a.is the criterion that an ideal tax should be effective in raising revenue of the

government and not have any negative effects on the economic decision-making

process of the taxpayer

b.requires that taxable income is taxed in the same manner by the taxpayer’s national

tax authority regardless of where in the world it is earned

c.implies that the tax burden a host country imposes on the foreign subsidiary of the

mnc should be the same regardless of which country the mnc is incorporated and the

same as that placed on domestic firms

d.none of the above

15) developing multiple production sites in a variety of countries,

a.can create an excess capacity problem

b.can lead to underutilization of domestic plants

c.can lead to domestic job losses

d.all of the above

16) the less correlated the securities in a portfolio,

a.the lower the portfolio risk

b.the higher the portfolio risk

c.the lower the unsystematic risk

d.the higher the diversifiable risk

17) assume that a country is on the gold standard. in order to support unrestricted

convertibility into gold, banknotes need to be backed by a gold reserve of some

minimum stated ratio. in addition,

a.the domestic money stock should rise and fall as gold flows in and out of the country

b.the central bank can control the money supply by buying or selling the foreign

currencies

c.both a and b

18) which term correctly describes the following situation? when a country imposes

exchange restrictions on its own currency, limiting conversion to other currencies, a

mnc’s frustrated remittance of profits from a subsidiary would be

a.blocked funds

b.stopped funds

c.constipated funds

d.money down the toilet

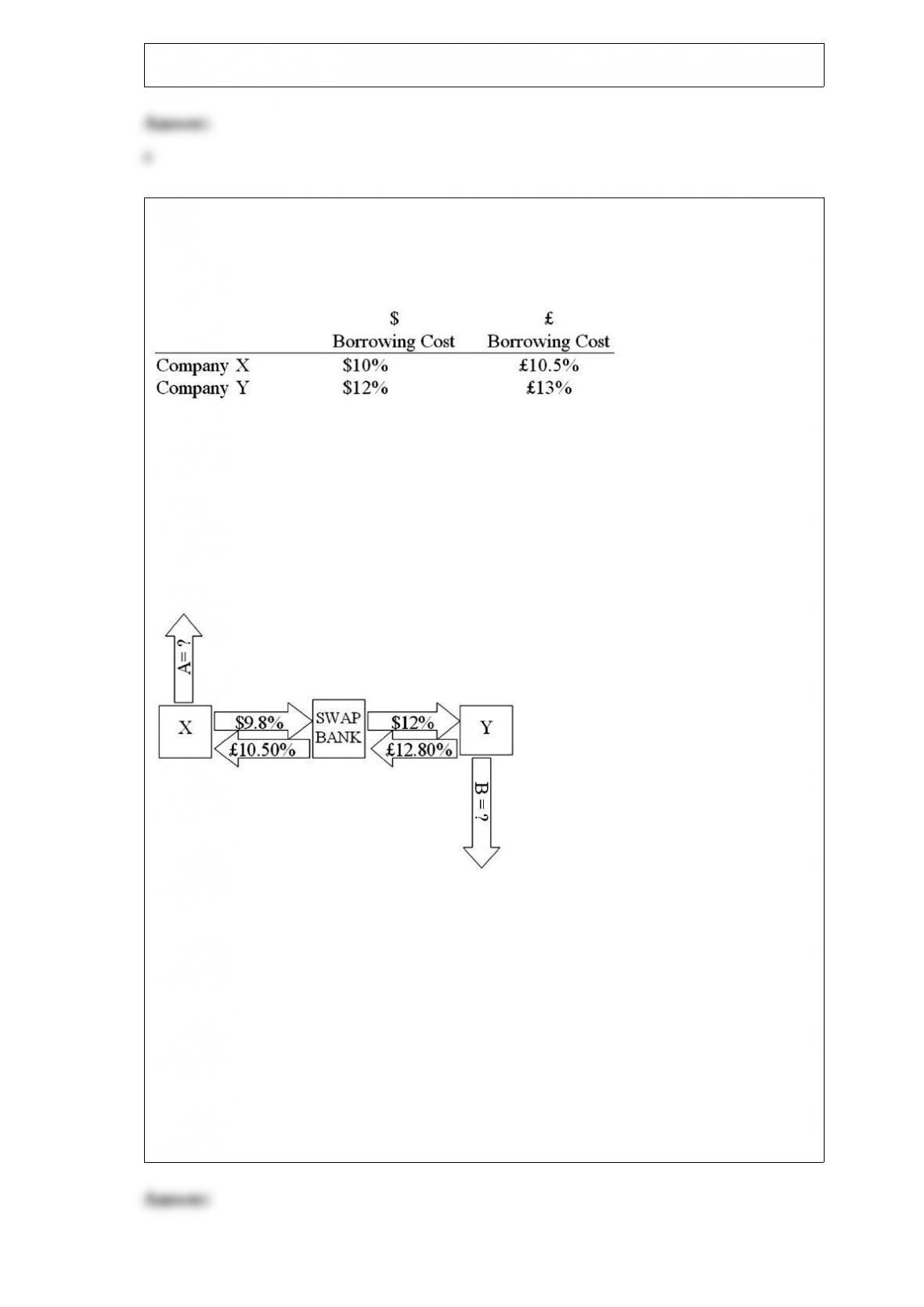

19) company x wants to borrow $10,000,000 floating for 5 years; company y wants to

borrow £5,000,000 fixed for 5 years. the exchange rate is $2 = £1 and is not expected to

change over the next 5 years. their external borrowing opportunities are:

a swap bank proposes the following interest-only swap: company x will pay the swap

bank annual payments on $10,000,000 at an interest rate of $9.80%; in exchange the

swap bank will pay to company x interest payments on £5,000,000 at a fixed rate of

10.5%. y will pay the swap bank interest payments on £5,000,000 at a fixed rate of

12.80% and the swap bank will pay y annual payments on $10,000,000 with the coupon

rate of 12%.

if company x takes on the swap, what external actions should they engage in?

a.they should borrow $10,000,000 at $10%

b.they should borrow £5,000,000 at 10.50% interest-only for five years; translate

pounds to dollars at the spot rate

c.they should borrow £5,000,000 at £10.50% interest-only for five years; translate

pounds to dollars at the spot rate; enter long position in a forward contract to buy

£5,000,000 in five years

d.none of the above

20) the singapore dollaru.s. dollar (s$/$) spot exchange rate is s$1.60/$, the canadian

dollaru.s. dollar (cd/$) spot rate is cd1.33/$ and the s$/cd1.15. determine the triangular

arbitrage profit that is possible if you have $1,000,000.

a.$44,063 profit

b.$46,093 loss

c.no profit is possible

d.$46,093 profit