1) Exhibit 23.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Darden Industries has decided to borrow $25,000,000.00 for six months in two

three-month issues. As the Treasurer, you are concerned that interest rates will rise over

the next three months and the rate upon which the second payment will be based will be

undesirable. (The amount of Darden’s first payment will be known at origination.) To

reduce the company’s interest rate exposure, you decide to purchase a 3 – 6 FRA

whereby you pay the dealer’s quoted fixed rate of 4.5% in exchange for receiving

3-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys

LIBOR from McIntire Industries at its bid rate of 4%. (Assume a notional principal of

$25,000,000.00 and that there are 60 days between month 3 and month 6.)

Assuming that 3-month LIBOR is 5.00% on the rate determination day, and the contract

specified settlement in arrears at month 6, describe the transaction that occurs between

the dealer and Darden.

a. The dealer is obligated to pay Darden $19,500

b. The dealer is obligated to pay Darden $31,250

c. Darden is obligated to pay the dealer $19,500

d. Darden is obligated to pay the dealer $31,250

e. None of the above

2) Institutional investors typically account for about

a. 90 to 95 percent of bond market trading.

b. 40 to 50 percent of bond market trading.

c. 10 to 15 percent of bond market trading.

d. Less than 5% of bond market trading.

e. None of the above.

3) In a value weighted index

a.Exchange rate fluctuations have a large impact.

b.Exchange rate fluctuations have a small impact.

c.Large companies have a disproportionate influence on the index.

d.Small companies have an exaggerated effect on the index.

e.None of the above

4) A properly selected sample for use in constructing a market indicator series will

consider the sample’s source, size and

a.Breadth.

b.Average beta.

c.Value.

d.Variability.

e.Dividend record.

5) Which of the following factors would be indicative of a high quality balance sheet?

a. Book value is greater than market value.

b. The presence of off-balance sheet liabilities

c. Market value is greater than book value.

d. Very little unused borrowing capacity.

e. None of the above.

6) The price at which a futures contract is set at the end of the day is the

a. Stock price.

b. Strike price.

c. Maintenance price.

d. Settlement price.

e. Parity price.

7) Issues that provide funds to retire another issue early are known as

a. Bearer bonds

b. Secured debentures

c. Unsecured debentures

d. Revenue bonds

e. Refunding bonds

8) A 1994 study concluded dealers were colluding to maintain wide bid/ask spreads by

concentrating market quotes in quarters instead of eighths. This study eventually led to

new order handling rules that required quotes to be available to the public through:

a.NASDAQ market

b.Electronic communications networks (ECN)

c.High frequency trading (HFT)

d.Algorithmic trading (AT)

e.Intermarket trading system (ITS)

9) Which of the following is correct?

a. If estimated value > Market price, you should buy.

b. If estimated value > Market price, you should sell.

c. If estimated value < Market price, you should sell.

d. If estimated value < Market price, you should buy.

e. Choices a and c.

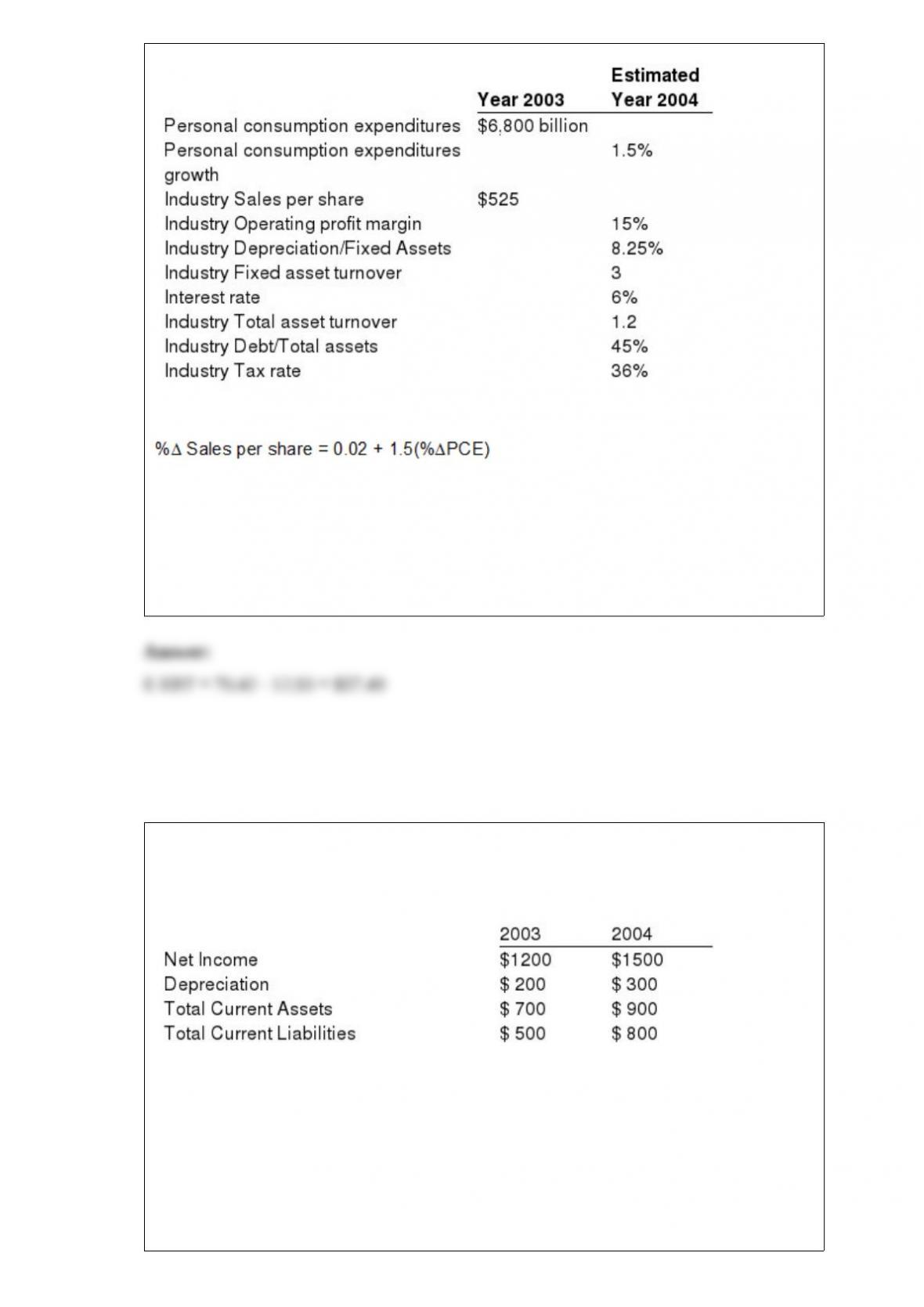

10) Exhibit 13.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that you are an analyst for the U.S. Autoparts Industry. Consider the following

information that you propose to use to obtain an estimate of year 2002 EPS for the U.S.

Autoparts Industry:

In addition a regression analysis indicates the following relationship between growth in

industry sales per share and personal consumption expenditures (PCE) growth is

Calculate the industry EBT per share for the year 2004.

a. $53.29

b. $67.89

c. $68.75

d. $59.63

e. $57.49

11) Exhibit 10.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following information for the Klandy Corporation.

During 2004 Klandy Corp. made capital expenditures totaling $500 and disposed

property worth $400.

The firm’s cash flow from operating activities for the year 2004 is

a. $2100

b. $1900

c. $1800

d. $1700

e. $1600

12) In the case of investment companies

a. Investors deal with a fund company and do not have separate accounts tailored to

their specific needs.

b. Investors deal with a fund company and have separate accounts tailored to their

specific needs.

c. Investors deal with an asset manager and do not have separate accounts tailored to

their specific needs.

d. Investors deal with an asset manager have separate accounts tailored to their specific

needs.

e. None of the above.

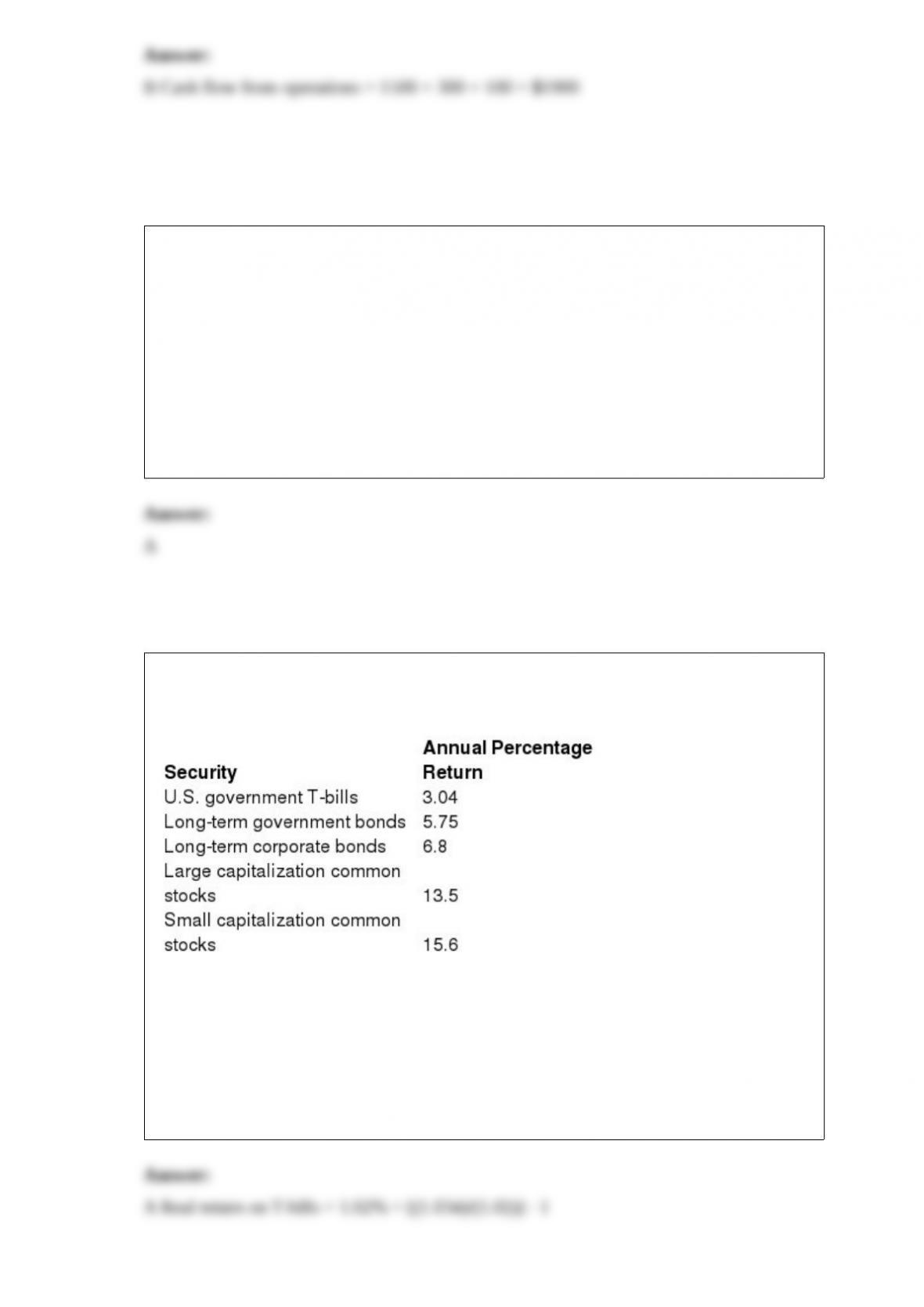

13) Exhibit 3.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The annual rate of inflation is 2%.

Refer to Exhibit 3.1. What is the real return on T-bills?

a.1.02%

b.3.68%

c.4.71%

d.11.27%

e.13.33%

14) The Dow Jones Industrial Average is a value weighted average.

15) A bond’s price is determined by the issue’s coupon rate, length to maturity, and the

prevailing yield in the market.

16) The goal of a passive portfolio is to track the index as closely as possible.

17) Historically the correlation between stocks and bonds has consistently remained

between 0.20 and 0.45.

18) The components of interest rate risk are: price risk and maturity risk.

19) Defined contribution pension plans promise to pay retirees a specific income stream

after retirement.