1) consider the position of a treasurer of a mnc, who has $20,000,000 that his firm will

not need for the next 90 days.

a.he could borrow the $20,000,000 in the money market

b.he could take a long position in the eurodollar futures contract

c.he could take a short position in the eurodollar futures contract

d.none of the above

2) under the bretton woods system, each country was responsible for maintaining its

exchange rate within 1 percent of the adopted par value by

a.buying or selling foreign exchanges as necessary

b.buying or selling gold as necessary

c.expanding or contracting the supply of loanable funds as necessary

d.increasing or decreasing their money supply as necessary

3) assume that you have invested $100,000 in british equities. when purchased, the

stock’s price and the exchange rate were £50 and £0.50/$1.00 respectively. at selling

time, one year after purchase, they were £60 and £0.60/$1.00. if the investor had sold

£50,000 forward at the forward exchange rate of £0.55/$1.00. the dollar rate of return

would be:

a.10.90%

b.7.58%

c.28.00%

d.9.09%

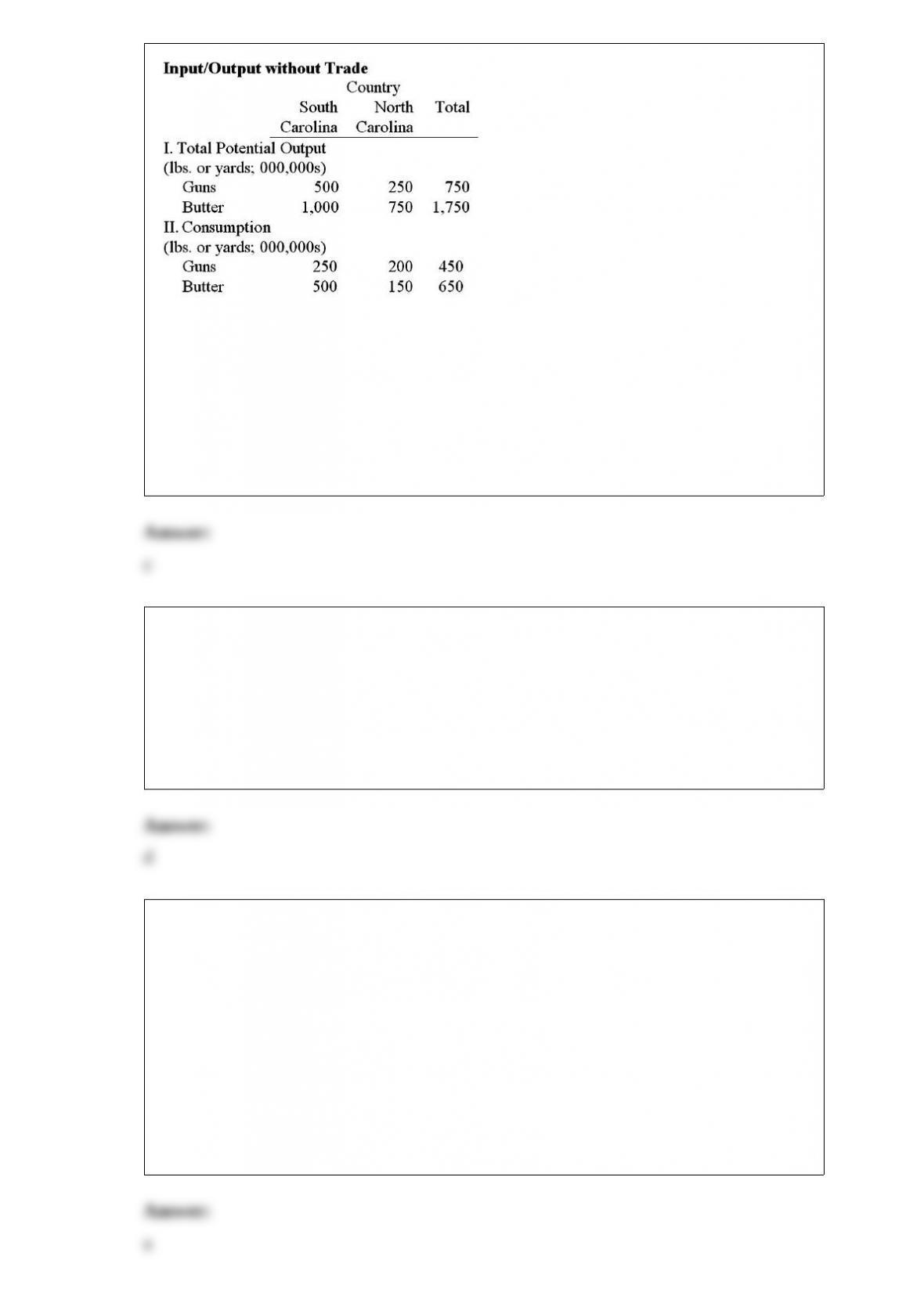

4) consider the no-trade input/output situation presented in the following table and

graph for south and north carolina. assume that free trade is legal.

what is the relative price of a gun in terms of butter in south carolina?

a.1 gun costs 3 butters

b.3 guns costs 1 butter

c.1 gun costs 2 butters

d.2 guns costs 1 butter

5) suppose that $2 = £1, $1.60 = 1, and the cross exchange rate is 1.25 = £1.00. if you

own a call option on £10,000 with a strike price of $1.50, you would exercise this

option at maturity if

a.the $/£ exchange rate is at least $1.60/£

b.the $/ exchange rate is at least $1.60/

c.the /£ exchange rate is at least 1.25/£

d.none of the above

6) for firms with free cash flows,

a.debt can be a stronger mechanism than stocks for credibly bonding managers to

release cash flows to investors

b.equity dividends can be a stronger mechanism than bonds for credibly bonding

managers to release cash flows to investors

c.preferred stock dividends can be a stronger mechanism than bonds for credibly

bonding managers to release cash flows to investors

d.none of the above

7) outside the united states and the united kingdom,

a.concentrated ownership of the company is more the exception than the rule

b.diffused ownership of the company is more the exception than the rule

c.partnerships are more important than corporations

d.none of the above

8) a currency dealer has good credit and can borrow either $1,000,000 or 800,000 for

one year. the one-year interest rate in the u.s. is i$ = 2% and in the euro zone the

one-year interest rate is i = 6%. the one-year forward exchange rate is $1.20 = 1.00;

what must the spot rate be to eliminate arbitrage opportunities?

a.$1.2471 = 1.00

b.$1.20 = 1.00

c.$1.1547 = 1.00

d.none of the above

9) the secondary market for eurobonds

a.is an over-the-counter market

b.is an organized exchange

c.has never developedthere is only a primary market for eurobonds

10) deregulation of world financial markets

a.provided a natural environment for financial innovations, like currency futures and

options

b.has promoted competition among market participants

c.has encouraged developing countries such as chile, mexico, and korea to liberalize by

allowing foreigners to directly invest in their financial markets

d.all of the above

11) following the introduction of the euro, the national central banks of the euro-12

nations

a.disbanded

b.formed the escb, which is analogous to the federal reserve system in the u.s

c.continue to perform important functions in their jurisdictions

d.b and c are correct

12) to hedge a foreign currency payable,

a.buy call options on the foreign currency

b.buy put options on the foreign currency

c.sell call options on the foreign currency

d.sell put options on the foreign currency

13) the international monetary system can be defined as the institutional framework

within which

a.international payments are made

b.movement of capital is accommodated

c.exchange rates among currencies are determined

d.all of the above

14) the stock market of country a has an expected return of 5%, and standard deviation

of expected return of 8%. the stock market of country b has an expected return of 15%

and standard deviation of expected return of 10%.

is it reasonable to conclude that your portfolio is on the efficient frontier? if not, then

prove your point by finding just one portfolio weighting between a and b that offers

more return with less risk. if you think it is on the efficient frontier, why do you think

this? no points for guessing.

15) your firm is based in southern ireland (and thereby operates in euro, not pounds)

and is considering an investment in the united states.

the project involves selling widgets: you project a sales volume of 50,000 widgets per

year, sales price of $20 per widget with a contribution margin of $15 per widget.

the project will last for 5 years, require an investment of $1,000,000 at time zero (which

will be depreciated straight-line to $10,000 over the 5 years). salvage value for the

equipment is projected to be $10,000. the project will operate in rented quarters:

$300,000 rent is due at the start of each year.

the corporate tax rate is 12% in ireland and 40% in the u.s.

for simplicity, assume that taxes are paid like sales taxes: immediately.

the spot exchange rate is $1.50 = 1.00. the cost of capital to the irish firm for a domestic

project of this risk is 8%. the u.s. risk-free rate is 3%; the irish risk-free rate is 2%.

what is the euro-denominated irr?

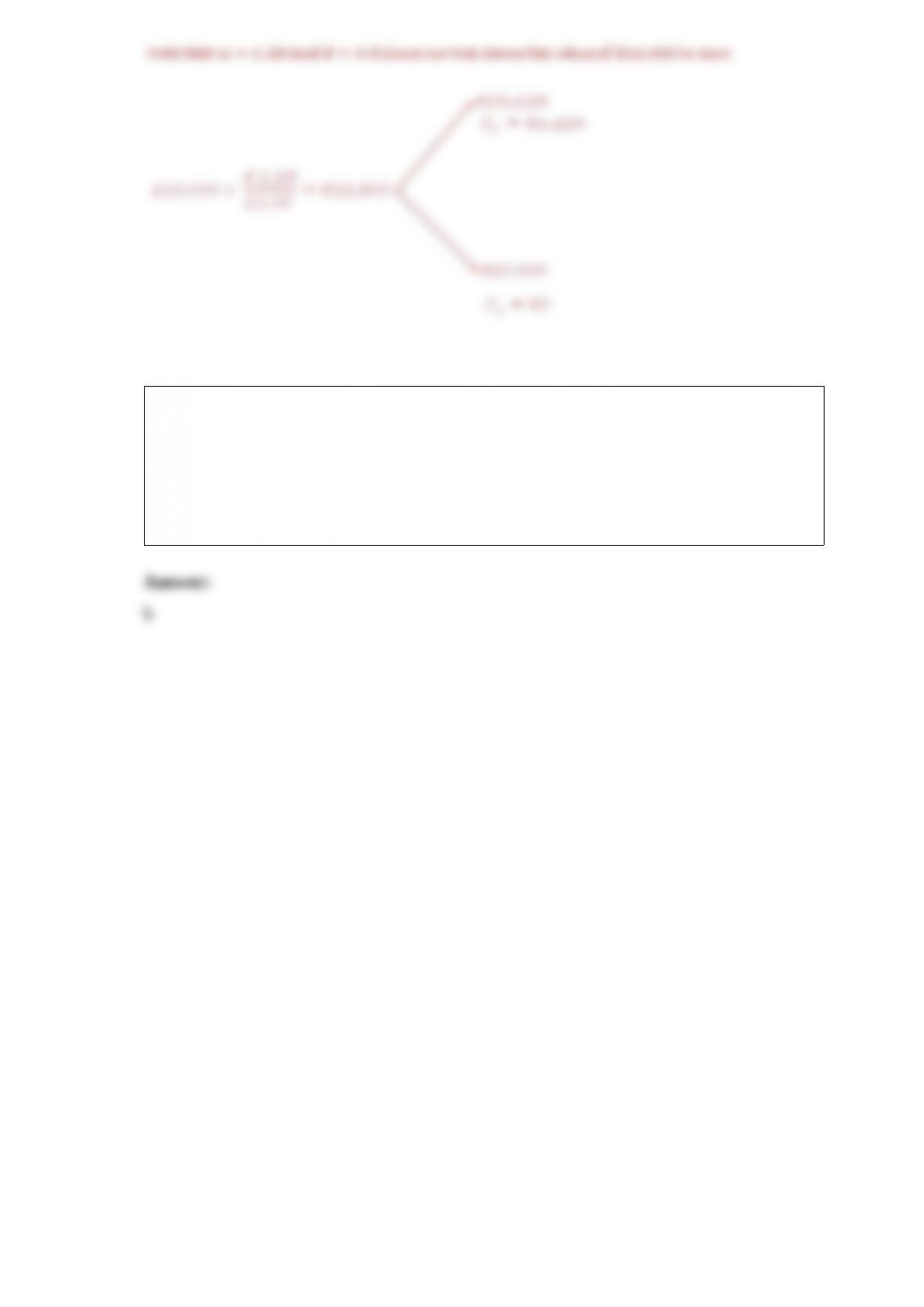

16) consider an option to buy £10,000 for 12,500. in the next period, if the pound

appreciates against the dollar by 37.5 percent then the euro will appreciate against the

dollar by ten percent. on the other hand, the euro could depreciate against the pound by

20 percent.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

if the call finishes out-of-the-money what is your replicating portfolio cash flow?

17) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock. one year after investment, the stock pays a £1 dividend,

and sells for £54 the exchange rate has changed from 1.25 per pound to 1.30 per pound,

although he sold £10,000 forward at the forward rate of 1.28 per pound.

18) a country that gives foreign aid to another country can be viewed as

a. importing goodwill from the latter

b. exporting goodwill to the latter

19) in 1963, president john kennedy imposed the interest equalization tax (iet) on u.s.

purchases of foreign securities. the iet was designed to

a.decrease the cost of foreign borrowing in the u.s. bond market

b.increase the cost of foreign borrowing in the u.s. bond market

20) the criteria of tax neutrality: capital export neutrality, capital import neutrality and

national neutrality

21) consider an option to buy £10,000 for 12,500. in the next period, if the pound

appreciates against the dollar by 37.5 percent then the euro will appreciate against the

dollar by ten percent. on the other hand, the euro could depreciate against the pound by

20 percent.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

if the call finishes in-the-money what is your replicating portfolio cash flow?

22) consider an option to buy £10,000 for 12,500. in the next period, if the pound

appreciates against the dollar by 37.5 percent then the euro will appreciate against the

dollar by ten percent. on the other hand, the euro could depreciate against the pound by

20 percent.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

draw the binomial tree for this option.

23) consider an 8.5 percent swiss franc/u.s. dollar dual-currency bonds that pays

$666.67 at maturity per sf1,000 of par value. if the bond sells at par, what is the implicit

sf/$ exchange rate at maturity? will the investor be better or worse off at maturity if the

actual sf/$ exchange rate is sf1.35/$1.00?

a. sf1.5/$1.00; better off

b. sf1.5/$1.00; worse off