1) a zero coupon bond has a duration equal to its maturity and a convexity equal to

zero.

2) a securities subsidiary of a bank holding company that engages in investment

banking is called a riegle-neal affiliate.

3) households are the largest owner of money market mutual funds.

4) a macro hedge is a hedge of a particular asset or liability exposure to a change in a

macroeconomic variable.

5) four seats on the fomc are allocated to federal reserve bank presidents on an annual

rotating basis.

6) there are more credit unions than other types of thrifts, but credit unions are

generally smaller than other types of thrifts.

7) the structure of a bank’s balance sheet as evidenced by its repricing gap and its

duration gap affects a bank’s sensitivity to interest rate changes. which one of the

following statements about the two types of gaps is true?

a.the repricing gap immunizes the present value of all future cash flows, whereas

managing the duration gap can stabilize future cash flows, but not their present value

b.the duration gap considers all cash flows up to and including maturity, whereas the

repricing gap really only considers how cash flows will change within the maturity

bucket

c.if a bank could only manage one type of gap, the bank would limit its interest rate risk

the most by managing its repricing gap instead of its duration gap

d.the repricing gap is superior to the duration gap since the repricing gap has a

well-defined maturity bucket

e.it is virtually impossible for an institution to have both a positive duration gap and a

negative repricing gap at the same time

8) a policyholder wishes to annuitize the cash value of her insurance policy at

retirement. the cash value is $725,000. what payment (to the nearest dollar) can he

expect if he wishes to receive 15 years of payments (starting next year) and interest

rates are 5.25%?

a.$43,333

b.$55,555

c.$71,033

d.$60,524

e.$29,250

9) runs on insurance firms are more likely to occur than runs on banks even in states

with guaranty funds for insurers because these funds generally

a.lack a permanent reserve fund

b.do not repay insurance policyholders immediately

c.lack federal government backing

d.all of the above

10) insolvency risk at a financial intermediary (fi) is the risk

a.that promised cash flows from loans and securities held by fis may not be paid in full

b.incurred by an fi when the maturities of its assets and liabilities do not match

c.that a sudden surge in liability withdrawals may require an fi to liquidate assets

quickly at fire sale prices

d.incurred by an fi when its investments in technology do not result in cost savings or

revenue growth

e.risk that an fi may not have enough capital to offset a sudden decline in the value of

its assets

11) which of the following requires daily cash flow settlements between the parties?

a.forward contract

b.futures contract

c.purchased options contract

d.swap contract

e.collars

12) with ____________ voting, all directors up for election are voted on by the

shareholders at the same time in one general election.

a.straight

b.participating

c.nonparticipating

d.proxy

e.cumulative

13) a time draft payable to a seller of goods, with payment guaranteed by a bank is a

a.commercial paper security

b.t-bill

c.repurchase agreement

d.negotiable cd

e.banker’s acceptance

14) with respect to private placements of bonds, which of the following is correct?

i. issuers of privately placed bonds tend to be less well known than public bond issues.

ii. interest rates on privately placed debt tend to be higher than for similar public issues.

iii. purchasers of privately placed debt have assets of at least $100 million.

iv. once bonds have been privately placed, the original buyers must hold the bonds until

maturity.

a.i only

b.i and iii only

c.i, ii, and iii only

d.i, iii, and iv only

e.i, ii, iii, and iv

15) a 6-year annual payment corporate bond has a required return of 9.5% and an 8%

coupon. its market value is $20 over its pv. what is the bond’s err?

a.8.00%

b.10.21%

c.9.98%

d.9.03%

e.3.53%

16) property and casualty insurers hold _____________ short-term assets than life

insurers because property and casualty loss rates are _____________ predictable than

life insurance loss rates.

a.more; more

b.more; less

c.less; less

d.less; more

17) if you were a loan officer evaluating a small business credit application for a loan

and you wanted to ensure that the applicant had more than sufficient cash flow to pay

off its existing debt, the applicant’s cash flow to debt ratio would have to be greater than

a.one

b.zero

c.the tie ratio

d.the interest rate on the debt

e.peer average ratio

18) why has securitization progressed most rapidly for home mortgages?

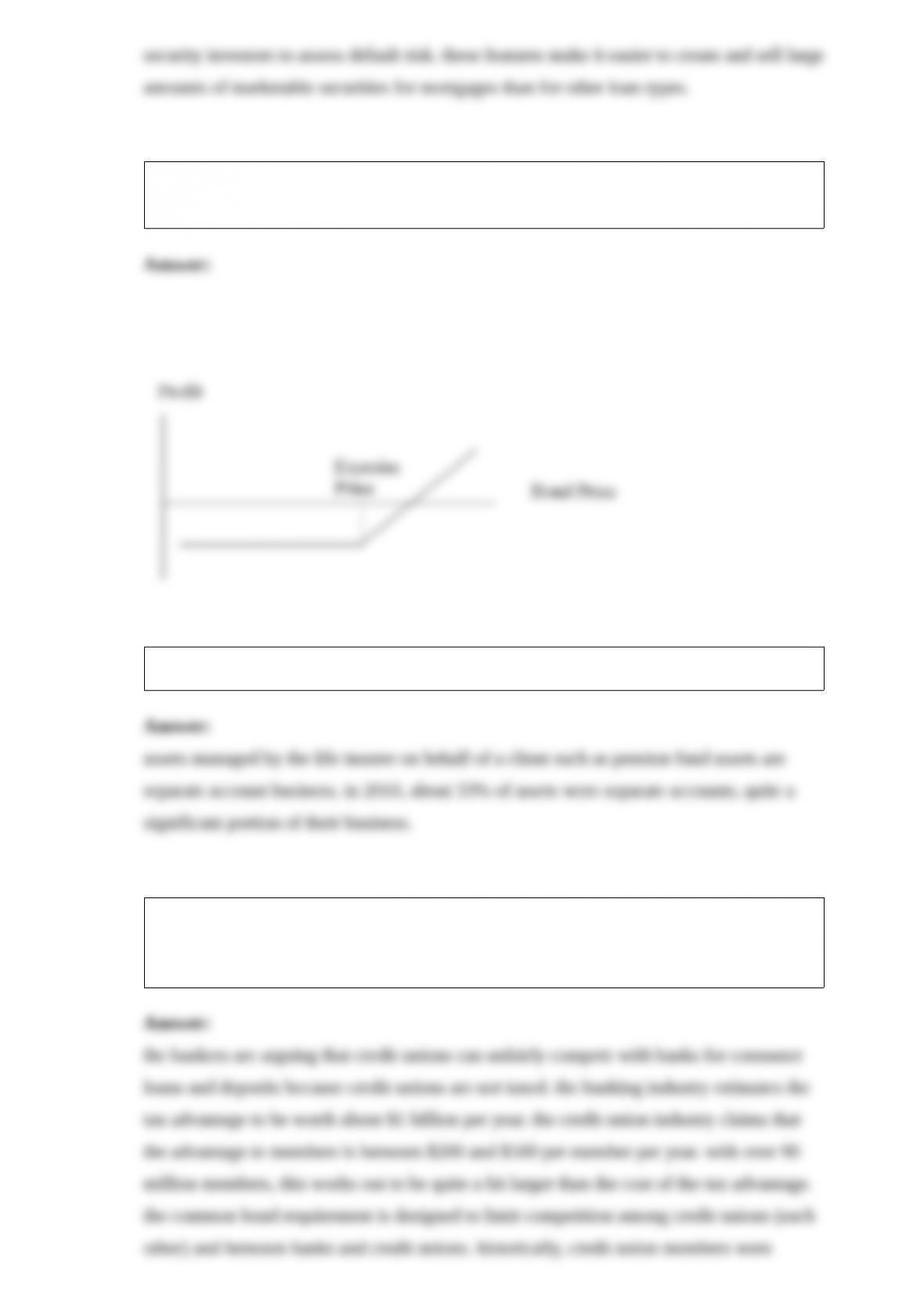

19) draw a graph of the gains and losses from owning a bond and simultaneously

buying a put on the bond.

20) what is separate account business? how important is it to life insurers?

21) the american bankers association and others are seeking to limit growth of credit

unions. what is the basis for the bankers’ concern? what does the credit union industry

argue? what kind of limits on credit unions are the bankers seeking?

22) what are weak form, semi-strong form, and strong form efficiency? does one form

of efficiency imply another?

23) in october 1987 stock prices fell 22% in one day and bond rates fell also. use the

loanable funds theory to explain what happened.

24) how does a repo differ from a fed funds transaction? how do their rates compare?

25) what are the advantages of a finance company or a bank leasing equipment to a

small business customer rather than financing the customer’s purchase of the

equipment?

26) in what ways are hedge funds different from mutual funds?