1) Which of the following statements about the business cycle is false?

a. Toward the end of a recession, financial stocks typically increase in value as

investment and borrowing activities accelerate.

b. Once the economy hits a trough and begins to recover, consumer durable stocks

become attractive investments.

c. Once the economy has recovered and current levels of consumption are sustainable,

businesses may consider modernizing or expanding, thus stocks of capital goods

industries become attractive investments.

d. As the business cycle reaches a peak, inflation rates decrease.

e. None of the above (that is, all are true statements)

2) A 4.75 percent coupon bond issued by the State of Washington sells for $1,000. What

coupon rate on a corporate bond selling at $1,000 par value would produce the same

after tax return to the investor as the municipal bond if the investor is in the 28 percent

marginal tax bracket?

a. 1.1%

b. 5.8%

c. 6.6%

d. 7.3%

e. 9.7%

3) The basis (Bt,T) at time t between the spot price (St) and a futures contract expiring at

time T (Ft,T) is

a. Bt,T= St+ Ft,T

b. Bt,T= St– Ft,T

c. Bt,T= Stx Ft,T

d. Bt,T= St/Ft,T

e. None of the above

4) Which of the following statements concerning historical investment risk and return is

false?

a.The geometric mean of the rates of return was always lower than the arithmetic mean

of the rates of return.

b.The rates of return on long-term U.S. government bonds were lower than on stocks.

c.Real estate investments consistently provide higher rates of return than those provided

by common stock.

d.Stocks and bonds experienced results in the middle of the art and antiques series.

e.none of the above (that is, all are true statements)

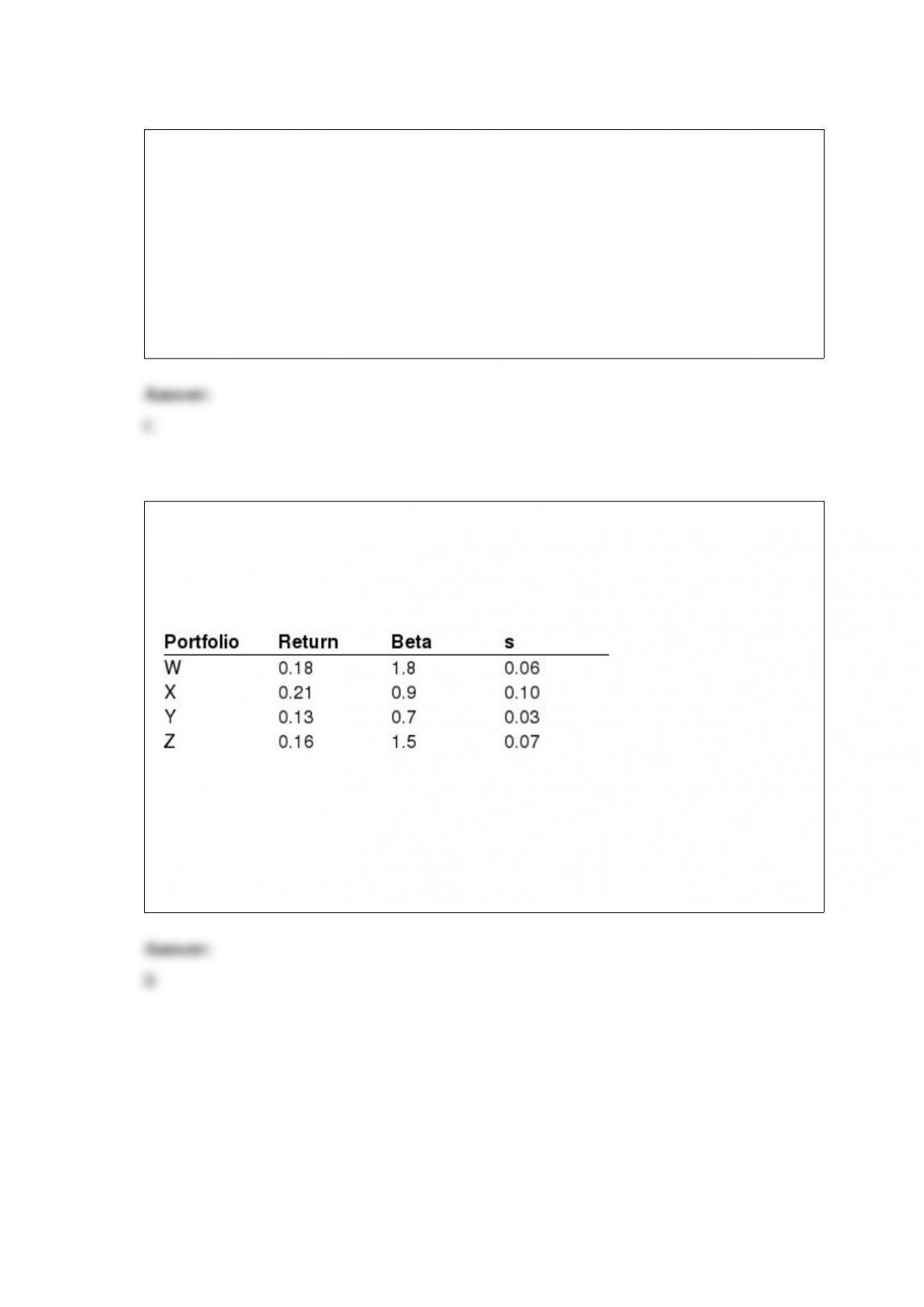

5) Exhibit 25.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The portfolios identified below are being considered for investment. Assume that

during the period under consideration Rf= .04.

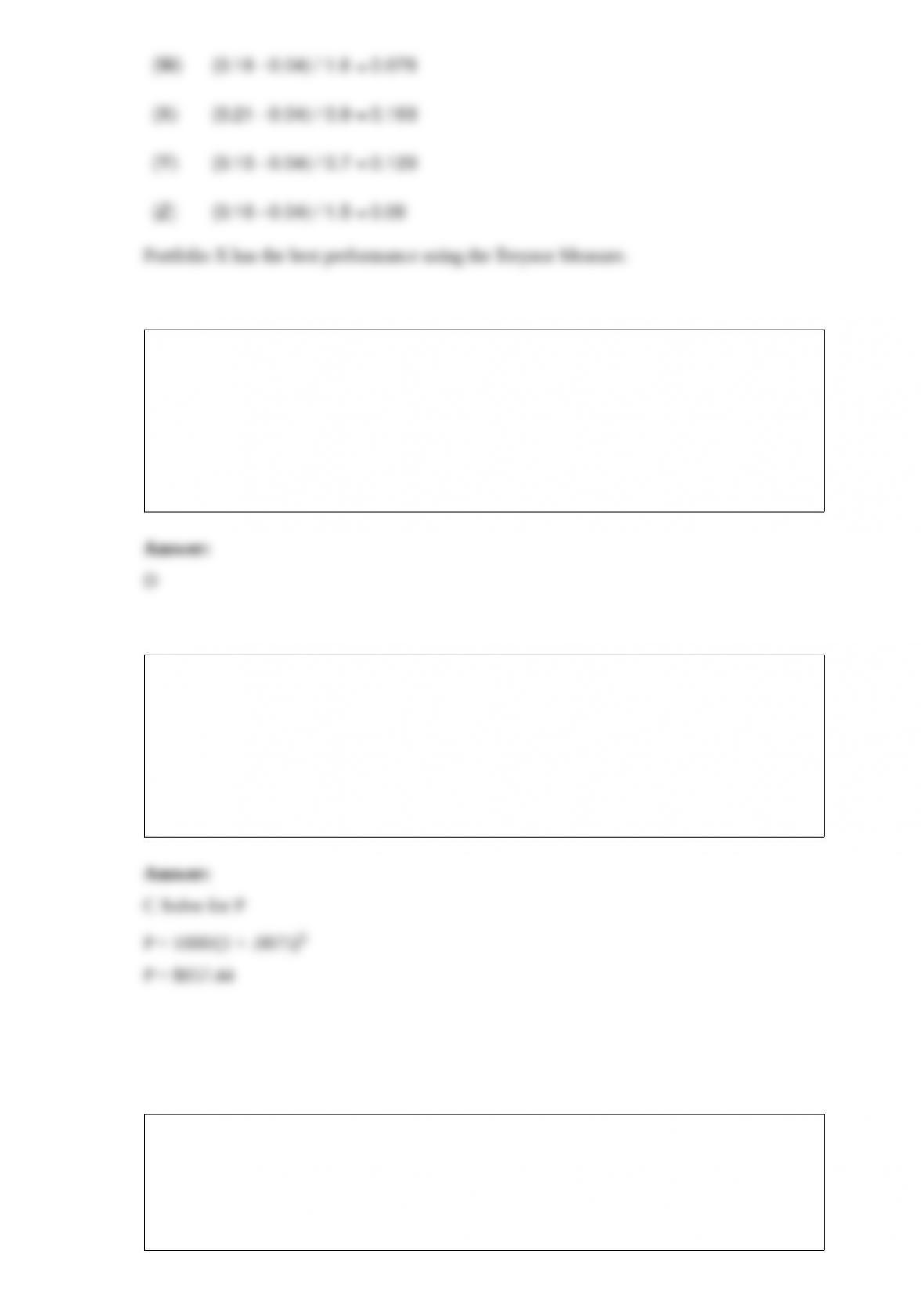

According to the Treynor Measure, which portfolio performed best?

a. W

b. X

c. Y

d. Z

e. Two portfolios are tied

6) Which of the following statements about the correlation coefficient is false?

a. The values range between –1 to +1.

b. A value of +1 implies that the returns for the two stocks move together in a

completely linear manner.

c. A value of –1 implies that the returns move in a completely opposite direction.

d. A value of zero means that the returns are independent.

e. None of the above (that is, all statements are true)

7) Calculate the price of a zero coupon bond with yield to maturity of 8.75%, a face

value of $1000, and maturing in 5 years.

a. $1000

b. $756.43

c. $675.44

d. $435.12

e. $875.14

8) Horizon matching is a combination of

a. Cash-matching dedication and interest rates swaps.

b. Cash-matching dedication and immunization.

c. Interest rate swaps and immunization.

d. Enhanced indexing and immunization.

e. Enhanced indexing and interest rate swaps.

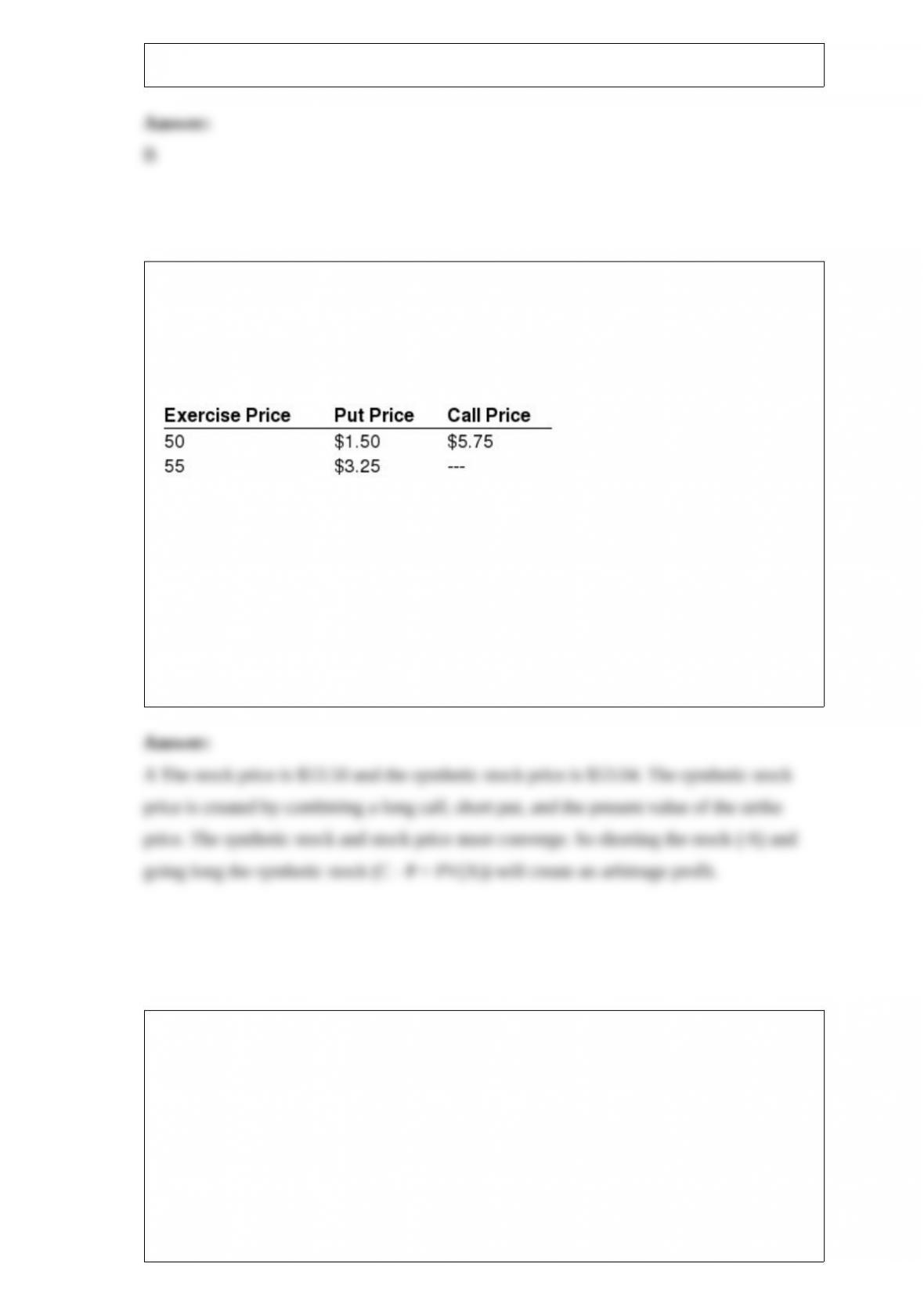

9) Exhibit 20.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The current stock price of ABC Corporation is $53.50. ABC Corporation has the

following put and call option prices that expire 6 months from today. The risk-free rate

of return is 5% and the expected return on the market is 11%.

How could an investor create arbitrage profits?

a. Sell the stock short, write a put, buy a call and invest the proceeds at the risk-free

rate.

b. Buy the stock, write a put, buy a call and invest the proceeds at the risk-free rate.

c. Sell the stock short, buy a put, write a call and invest the proceeds at the risk-free

rate.

d. Buy the stock, write a put, buy a call and borrow the strike price at the risk-free rate.

e. Sell the stock short, write a put, buy a call and borrow the strike price at the risk-free

rate.

10) Exhibit 23.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

An international investment firm buys an interest rate cap that pays the difference

between LIBOR and 6% if LIBOR exceeds 6%. Current LIBOR is 5%. The amount of

the option is $1,500,000, and the settlement is every 3 months. Assume a 360 day year.

Find the payoff if LIBOR closes at 6.3%.

a. -$45,000

b. -$11,250

c. $0

d. $11,250

e. $45,000

11) Like future contracts, all forward contracts are processed by a clearing corporation.

12) In a binomial option pricing model the initial value of the call can be determined by

working backward through the tree and solving for each of the remaining intermediate

option values.

13) It is a violation of the securities laws to combine option contracts to achieve a

customized payoff.

14) A strip is a call option on a stock that is written by someone that owns the stock.

15) An equity investor’s required rate of return is influenced by the economy’s real

risk-free rate, the expected rate of inflation, and a risk premium.

16) Government agency securities are issued by local government entities as either

general obligation or revenue bonds.

17) Over the last 20 years, increases in the return on equity for the S&P Index has been

associated with decreases in return of assets.

18) A relative valuation technique is appropriate to consider when you have a good set

of comparable entities.

19) The Jensen measure requires that each period’s rates of return and risk-free rate be

measured, rather than using the long-term averages as in the Treynor and Sharpe

measures.

20) Since many of the assumptions made by the capital market theory are unrealistic,

the theory is not applicable in the real world.