Average daily turnover in the FX market has recently been over $4 trillion.

Answer:

The extremely high growth of OBS activities since the early 1990s has caused

regulators to recognize the potential risk exposure to FIs from their use.

Answer:

The difference between the changes in the market value of the assets and market value

of liabilities for a given change in interest rates is, by definition, the change in the FI’s

net worth.

Answer:

In the LCD and EM debt markets, sovereign bonds must be collateralized by

domestically-issued government bonds.

Answer:

FNMA securitizes conventional mortgage loans as well as FHA/VA insured loans.

Answer:

Counterparty credit risk is more prevalent for exchange-traded derivatives than

over-the-counter (OTC) contracts because the bank has more control of its OTC

contracts.

Answer:

Federal funds are excess reserves held by the Federal Reserve Banks that are loaned to

banks that have liquidity needs.

Answer:

Profits in foreign exchange trading have grown despite the decreased volatility in FX

rates in European countries.

Answer:

The market value of a fixed-rate liability will increase as interest rates rise, although the

market value of a fixed-rate asset will decrease as interest rates rise.

Answer:

The Financial Accounting Standards Board requires that all derivatives be

marked-to-market with any losses and gains transparent on FI’s financial statements.

Answer:

One reason FIs such as depository institutions and life insurance companies are exposed

to liquidity risk is the relatively illiquid nature of their liabilities.

Answer:

Because deposit insurance premiums were not priced in an actuarially fair manner

during the period from 1933-1980s, instability was created in the credit and monetary

system.

Answer:

As of 2012, chartering of life insurance companies can be done only at the state level.

Answer:

In a public offering of a new security, an investment banker places a new issue of

securities with a handful of private, usually large, investors.

Answer:

The objective of the investment function of securities firms (funds management) is to

allocate assets so that they outperform relative risk-return performance benchmark.

Answer:

The cumulative repricing gap position of an FI for a given extended time period is the

sum of the repricing gap values for the individual time periods that make up the

extended time period.

Answer:

One method of changing the positive leverage adjusted duration gap for the purpose of

immunizing the net worth of a typical depository institution is to increase the duration

of the assets and to decrease the duration of the liabilities.

Answer:

For situations in which probability distributions exhibit fat tail losses, expected shortfall

(ES) may look relatively small, but value at risk (VAR) may be very large.

Answer:

The rate of growth in the annuities market is increasing primarily because of the recent

changes in the capital gains tax rates.

Answer:

Which of the following observations is TRUE of the contemporaneous reserve

accounting system?A. The reserve computation and reserve maintenance periods do

not overlap.

B. The maintenance period does not begin until seventeen days after the end of the

computation period.

C. It results in a two-day window during which required reserves are known with

certainty.

D. It increases the accuracy of information on aggregate required reserve balances.

E. It may be used instead of the lagged reserve accounting system.

Answer:

Investors in a Structured Investment Vehicle (SIV) have no direct right to the cash flows

on the underlying portfolio of the SIV.

Answer:

The introduction of prompt corrective action capital zones by FDICIA was an attempt

to place greater decision-making power at the discretion of regulators rather than on

objective, measurable rules.

Answer:

Which of the following observations is NOT TRUE?A. The settlement risk that an FI is

exposed to within-day appears on its balance sheet.

B. Settlement Risk is a form of OBS risk that FIs participating on private wholesale

wire transfer system networks face.

C. A holding company is a corporation that owns more than 25 percent of the shares of

other corporations.

D. Failure of an affiliated firm or bank imposes affiliate risk on another bank in a

holding company structure in a number of ways.

E. Investors do not distinguish between the failing corporation and its surviving

affiliate because of name similarity.

Answer:

An FI is net long in foreign assets if it holds more foreign liabilities than foreign assets.

Answer:

The qualified thrift lender test is utilized to determine whether an institution can serve

as an FI.

Answer:

An FI can immunize its portfolio by matching the maturity of its asset with its

liabilities.

Answer:

The Basic Indicator Approach in calculating capital to cover operational risk requires

banks to hold 12 percent of total assets in capital to cover operational risk exposure.

Answer:

General diversification limits established by life and property and casualty insurance

regulators are based on the concepts of modern portfolio theory.

Answer:

As of 2011, ordinary life accounted for approximately 80% of policies in force.

Answer:

The purpose of guaranty funds in safety and soundness regulation is to protect

claim-holders when an FI collapses or fails.

Answer:

The U.S. Treasury has recently proposed that banks carry a capital cushion against

losses resulting from operational risk.

Answer:

A best-efforts offering of a security is more risky for an investment bank than a firm

commitment offering.

Answer:

During the financial crisis of 2008, liquidity problems were avoided as banks continued

to provide lending to each other.

Answer:

Unfairly excluding some potential financial service consumers from the financial

services marketplace is a reason why FIs must absorb net regulatory burden.

Answer:

In a credit forward agreement hedge, the loss on the balance sheet cash position is offset

completely by the gain on the off-balance-sheet credit forward agreement if the

characteristics of the benchmark bond and the bank’s loan to the borrower are the same.

Answer:

Market value of equity is more appropriate than book value of equity at reflecting

changes in the credit risk and interest rate risk of an FI.

Answer:

Identify the action taken by OCC and the Federal Reserve in 1997, to expand the

permitted activities of bank holding companies. A. Repealed the Glass-Steagall barriers

between commercial banking and investment banking.

B. Allowed commercial banks to acquire directly existing investment banks.

C. Allowed investment banks to offer banking products.

D. Allowed investment banks to offer deposit products.

E. All of the above.

Answer:

When a DI makes a shift from an “originate-to-hold” banking model to an

“originate-to-distribute” model, the change is likely to result in A. increased operating

costs.

B. increased interest rate risk.

C. increased liquidity risk.

D. decreased monitoring costs.

E. decreased fee income.

Answer:

An investor purchases fund shares with a 3 percent front-end load and expects to hold

the shares for 10 years. The annualized sales load incurred by the investor is _______

per year. A. 3 percent

B. 30 percent

C. 0.3 percent

D. 1.3 percent

E. 1 percent

Answer:

Which of the following best explains the term burn-out factor? A. The percent of

mortgage contract that is transferred from the seller to the buyer of a house.

B. The required interest spread of a pass-through security over a treasury when

prepayment risk is taken into account.

C. The aggregate percent of the mortgage pool that has been prepaid prior to the month

under consideration.

D. A mortgage-backed bond issued in multiple classes or tranches.

E. Bonds collateralized by a pool of assets.

Answer:

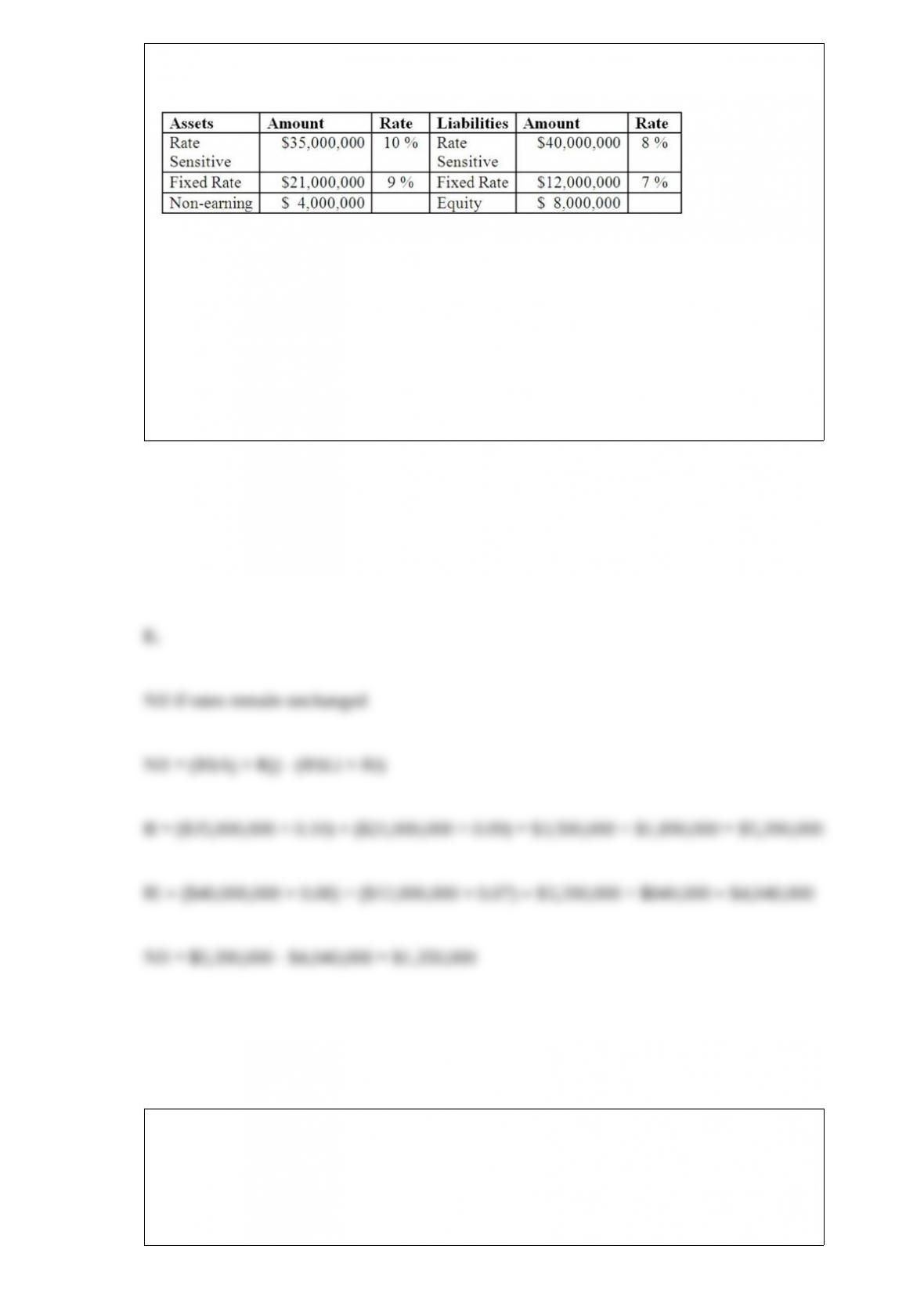

The balance sheet of ARGH Insurance shows the following fixed and rate sensitive

assets and liabilities.

What will be

the FI’s net interest income at year-end if interest rates do not change? A. $3.20 million.

B. $5.39 million.

C. $4.04 million.

D. $1.89 million.

E. $1.35 million.

Answer:

What information does the net liquidity statement provide? A. A long-term focus on

liquidity.

B. Sources and uses of liquidity.

C. Net asset value.

D. Liquidity index information.

E. Peer group ratio comparison.

Answer:

Which of the following best describes/defines X-inefficiencies? A. The average cost of

production decreases as the level of output increases.

B. The effects on costs related to managerial ability and other hard-to-quantify factors.

C. Cost savings are realized from using many of the same inputs to produce multiple

products.

D. The average cost of production increases as the level of output increases.

E. Cost increases are realized from using many of the same inputs to produce multiple

products.

Answer:

If problem loans reduce the market value of the loan portfolio by 25 percent, what is the

value of regulatory defined (book value) capital? A. $35 million.

B. -$155 million.

C. $7 million.

D. -$7 million.

E. $0.

Answer:

What are the savings to the corporation if it obtains a loan commitment to back its $10

million issue of commercial paper? A. $1,250.

B. $2,500.

C. $3,750.

D. $5,000.

E. $6,250

Answer:

An existing swap can be effectively hedged against interest rate risk by A. selling out

to another party.

B. entering into another swap agreement that is the mirror image of the original swap.

C. setting interest sensitive assets equal to interest sensitive liabilities.

D. setting asset duration equal to liability duration.

E. defaulting to the swap intermediary.

Answer:

These bonds have some prepayment protection and expected durations of five to seven

years depending on the level of interest rates and are primarily purchased by pension

funds and life insurance companies. A. Class A bonds.

B. Class R bonds.

C. Class C bonds.

D. Class Z bonds.

E. Class B bonds.

Answer:

If the bank experiences a $50,000 sudden liquidity drain caused by a loan commitment

draw down, what will be the impact on the balance sheet if stored liquidity management

techniques are used?A. A reduction in cash of $21,000 and an increase in demand

deposits of $29,000.

B. A reduction in securities and/or current loans totaling $50,000.

C. A reduction in cash of $21,000 and a decrease in securities holdings of $29,000.

D. A decrease in equity of $50,000.

E. A decrease in lending of $50,000.

Answer:

How many currency contracts are necessary to hedge this asset?A. 112 contracts.

B. 57 contracts.

C. 80 contracts.

D. 75 contracts.

E. 42 contracts.

Answer:

Conyers Bank holds U.S. Treasury bonds with a book value of $30 million. However,

the U.S. Treasury bonds currently are worth $28,387,500.

The bank’s portfolio manager wants to shorten asset maturities. Which of the following

statements is TRUE? A. The portfolio manager is reluctant to sell the bonds outright

since the bank will have to take a loss.

B. The portfolio manager is willing to sell the bonds outright since they are not as

valuable as their book value.

C. The portfolio manager is willing to sell the bonds outright since they are more

valuable than their book value.

D. The portfolio manager is reluctant to sell the bonds outright since the bank will have

to pay taxes on the gain.

E. None of the above.

Answer:

If a future credit crunch is possible, a loan commitment may expose the FI to A. credit

risk.

B. interest rate risk.

C. sovereign country risk.

D. funding risk.

E. exchange rate risk.

Answer:

An FI has assets of $800 million and liabilities of $740 million.

What is the balance sheet capital? A. -$60 million.

B. $60 million.

C. $740 million.

D. $800 million.

E. This question cannot be answered without information about off-balance sheet assets

and liabilities.

Answer:

A DI offers a $500 minimum balance NOW account paying 5.5 percent annual interest.

The account has a service charge of $0.05 per check, and processing costs per check are

$0.15. The customer maintains a balance of $1,000, and averages 150 checks per year.

What is the annual gross interest return on this account to the customer? A. $22.50.

B. $70.00.

C. $15.00.

D. $55.00.

E. $7.50.

Answer:

The following are the net currency positions of a U.S. FI (stated in U.S. dollars).

What is the FI’s net

exposure in British pounds? A. -45,400.

B. -150,600.

C. -196,000.

D. +105,200.

E. +196,000.

Answer:

An FI has $5 million in cash reserves with the Fed in excess of its reserve requirements,

$5 million in T-Bills, and a credit line of $10 million to borrow in the repo market. It

currently has lent $2 million in the Fed Funds market and borrowed $1 million from the

Federal discount window to meet its seasonal needs.

What are the bank’s total available sources of liquidity? A. $17 million.

B. $18 million.

C. $20 million.

D. $21 million.

E. $22 million.

Answer:

What are the bank’s current total uses of liquidity? A. $1 million.

B. $3 million.

C. $8 million.

D. $10 million.

E. $15 million.

Answer:

Most profits or losses on foreign trading for FIs come from A. open positions or

speculation.

B. market making.

C. acting as agents for retail customers.

D. acting as agents for wholesale customers.

E. hedging activities.

Answer:

Under the 1982 guidelines, would the Fed approve the merger of Banks A and C? A. It

is likely to approve because it is not a concentrated market.

B. It is unlikely to approve because the post-merger HHI has increased by over 100.

C. It is likely to approve because the post-merger HHI has increased by over 100.

D. Likely to approve because the post-merger HHI has increased by less than 5,000.

E. It is unlikely to approve because the post-merger HHI has increased by an amount

over 5,000.

Answer:

The Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA) required

the FDIC to establish risk-based premiums for deposit insurance coverage at banks.

Answer:

The repricing gap approach calculates the gaps in each maturity bucket by subtracting

the A. current assets from the current liabilities.

B. long term liabilities from the fixed assets.

C. rate sensitive assets from the total assets.

D. rate sensitive liabilities from the rate sensitive assets.

E. current liabilities from tangible assets.

Answer:

If interest rates decrease 50 basis points for an FI that has a gap of +$5 million, the

expected change in net interest income is A. + $2,500.

B. + $25,000.

C. + $250,000.

D. – $250,000.

E. – $25,000.

Answer:

An FI has financial assets of $800 and equity of $50. If the duration of assets is 1.21

years and the duration of all liabilities is 0.25 years, what is the leverage-adjusted

duration gap? A. 0.9000 years.

B. 0.9600 years.

C. 0.9756 years.

D. 0.8844 years.

E. Cannot be determined.

Answer:

Considering the securities firms and investment banking industries, The National

Securities Markets Improvement Act (NSMIA) of 1996 A. appointed the Federal

Reserve System as the primary regulator of the industry.

B. diminished the role of the National Association of Securities Dealers (NASD) in

regulating the industry.

C. allowed individual states the right to require registration of firms operating in the

state.

D. effectively affirmed the SEC as the primary regulator of the industry.

E. required all firms in the industry to maintain minimum amounts of capital.

Answer:

Daylight overdrafts occur when A. FIs in different time zones clear transactions.

B. FI debits exceed credits during the day.

C. FI credits exceed debits during the day.

D. the sum of all debits transmitted over the system exceed the sum of all credits

during the day.

E. the sum of all credits transmitted over the system exceed the sum of all debits during

the day.

Answer:

Which of the following dominates the loan portfolios of banks with assets less than one

billion dollars? A. Commercial loans.

B. Consumer loans.

C. Real estate loans.

D. Credit card debt.

E. Industrial loans.

Answer:

Because of its simplicity, smaller depository institutions still use this model as their

primary measure of interest rate risk. A. The repricing model.

B. The maturity model.

C. The duration model.

D. The convexity model.

E. The option pricing model.

Answer:

A pure credit swapA. is like buying credit insurance.

B. is like buying a multi-period credit option.

C. eliminates the interest rate risk contained in a total return swap.

D. All of the above.

E. None of the above.

Answer:

Using a modified discriminant function similar to Altman’s, Burger Bank estimates the

following coefficients for its portfolio of loans:

Z = 1.4X1 + 1.09X2 + 1.5X3

where X1 = debt to asset ratio; X2 = net income and X3 = dividend payout ratio.

What is the Z-score if the debt to asset ratio is 40 percent, net income is 12 percent, and

the dividend payout ratio is 60 percent? A. 1.59.

B. 1.48.

C. 1.36.

D. 1.28.

E. 1.20.

Answer:

Banks that sell many of their loans A. utilize more of a dealer intermediation approach.

B. utilize more of a broker intermediation approach.

C. utilize more of a trader intermediation approach.

D. utilize more of a market maker intermediation approach.

E. relinquish some of their roles as financial intermediaries.

Answer:

All other things equal, longer term loans are more likely to be A. variable-rate loans.

B. fixed-rate loans.

C. commitment loans.

D. lowest risk category loans.

E. high interest rate loans.

Answer:

Which of the following is not accomplished by securitization of assets? A. Increases

the liquidity of assets.

B. Provides a new source of funds.

C. Increases the costs of monitoring.

D. Decreases the duration of assets.

E. Decreases the costs of regulation.

Answer: