1) ____ gains are taxable and occur when an asset is sold for more than its basis (the

value of the asset when it was purchased by the original owner, or inherited by the heirs

of the original owner).

a.Realized capital

b.Income

c.Portfolio

d.Nominal

e.Real

2) Exhibit 12.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that the dividend payout ratio will be 75 percent when the rate on long-term

government bonds falls to 8 percent. Since investors are becoming more risk averse, the

equity risk premium will rise to 7 percent and investors will require a 15 percent return.

The return on equity will be 12 percent.

What is the expected sustainable growth rate?

a. 9.0%

b. 7.2%

c. 6.0%

d. 3.0%

e. 3.6%

3) Financial risk is the additional uncertainty of returns to equity holders due to

a. The firm’s use of fixed financial obligations

b. The firm’s level of fixed productions costs

c. Business risk

d. a and b.

e. b and c.

4) In equity portfolio management, tracking error occurs when

a. The managed portfolio outperforms the benchmark portfolio.

b. The managed portfolio under performs the benchmark portfolio.

c. The return volatility of the managed portfolio is positively correlated with the return

volatility of the benchmark portfolio.

d. The return volatility of the managed portfolio is negatively correlated with the return

volatility of the benchmark portfolio.

e. The return volatility of the managed portfolio is not correlated with the return

volatility of the benchmark portfolio.

5) A portfolio of two securities that are perfectly positively correlated has

a. A standard deviation that is the weighted average of the individual securities standard

deviations.

b. An expected return that is the weighted average of the individual securities expected

returns.

c. No diversification benefit over holding either of the securities independently.

d. Both b and c

e. All of the above

6) All of the following questions remain to be answered in the real world except

a. What is a good proxy for the market portfolio?

b. What happens when you cannot borrow or lend at the risk free rate?

c. How good is the capital asset model as a predictor?

d. What is the beta of the market portfolio of risky assets?

e. What is the stability of beta for individual stocks?

7) Exhibit 11.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider a firm that has just paid a dividend of $1.5. An analyst expects dividends to

grow at a rate of 9% per year for the next three years. After that dividends are expected

to grow at a normal rate of 5% per year. Assume that the appropriate discount rate is

7%.

The dividends for years 1, 2, and 3 are

a. $1.5, $2.0, $2.05

b. $1.64, $1.78, $1.94

c. $1.64, $1.94, $2.24

d. $1.5, $2.40, $3.30

e. $2.07, $2.14, $2.21

8) Consider the following two factor APT model

E(R) = λ0+ λ1b1+ λ2b2

a. λ1is the expected return on the asset with zero systematic risk.

b. λ1is the expected return on asset 1.

c. λ1is the pricing relationship between the risk premium and the asset.

d. λ1is the risk premium.

e. λ1is the factor loading.

9) All of the following are underlying assumptions of the capital asset pricing model

(CAPM) except:

a.A large number of profit-maximizing participants analyze and value securities.

b.New information enters the market in a random fashion

c.Security prices adjust rapidly to reflect the effect of new information

d.Expected returns implicit in the current price of the security reflect its risk

e.All of the above are assumptions of the CAPM

10) Exhibit 19.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider two bonds, both pay annual interest. Bond Y has a coupon of 6% per year,

maturity of 5 years, yield to maturity of 6% per year, and a face value of $1000. Bond

X has a coupon of 7% per year, maturity of 10 years, yield to maturity of 4% per year,

and a face value of $1000.

Assume that your investment horizon is 5 years and your portfolio consists only of

Bond Y and Bond X. Indicate the proportions invested in each bond, so that the

portfolio is immunized.

a. 50% in Bond Y and 50% in Bond X

b. 76% in Bond Y and 24% in Bond X

c. 36% in Bond Y and 64% in Bond X

d. 100% in Bond X

e. 100% in Bond Y

11) Assume that you invest $750 at the end of each quarter for the next 20 years in a

mutual fund. The annual rate of interest that you expect to earn in this account is 5.25%.

The amount in the account at the end of 20 years is

a.$60,000.00

b.$105,039.84

c.$37,009.35

d.$123,510.52

e.$115,637.37

12) Assume that you invest $1250 at the end of each of the next 15 years in a mutual

fund. You currently have $10,000 in the mutual fund. The annual rate of interest that

you expect to earn in this account is 4.35%. The amount in the account at the end of 15

years is

a.$58,940.30

b.$28,750.00

c.$37,009.35

d.$44,630.81

e.$25,690.50

13) Exhibit 20.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

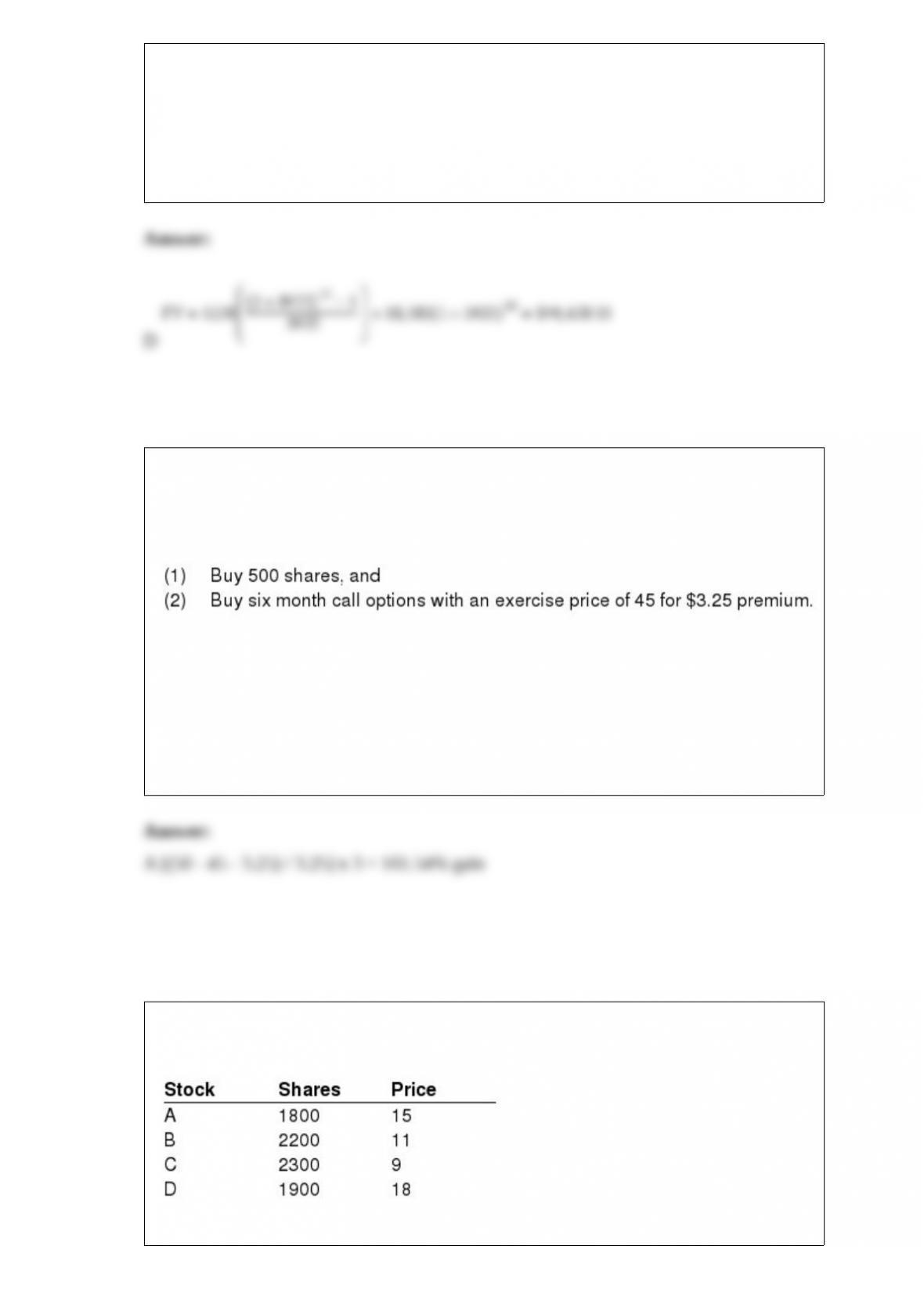

Rick Thompson is considering the following alternatives for investing in Davis

Industries which is now selling for $44 per share:

Assuming no commissions or taxes what is the annualized percentage gain if the stock

reaches $50 in four months and a call was purchased?

a. 161.54% gain

b. 53.85% gain

c. 161.54% loss

d. 11.11% gain

e. 53.85% loss

14) Suppose Mega Mutual Fund owns only the 4 stocks shown below with no

liabilities.

The fund originated by selling $300,000 of stock at $30.00 per share. What is its current

NAV?

a. $106.10

b. $12.94

c. $129.40

d. $10.61

e. None of the above

15) Selectivity measures how well a portfolio performed relative to a

a. Market portfolio (S&P 400).

b. Portfolio of the same securities in the previous period.

c. Naively selected portfolio of equal risk.

d. Naively selected portfolio of equal return.

e. World market portfolio.

16) In ____ strategy, certain economic sectors or industries are overweighted relative to

the benchmark in anticipation of the next phase of the business cycle.

a. Sector rotation

b. Price momentum

c. Earnings momentum

d. Return rotation

e. None of the above

17) The bond market segments that tend to be highly correlated and move together

include

a. Short and long term bonds.

b. Short and intermediate term bonds.

c. Intermediate and long term bonds.

d. Short, intermediate and long term bonds.

e. None of the above.

18) A market is a means through which buyers and sellers are brought together to aid in

the transfer of goods and/or services.

19) In the case of a bond, the only contractual factor is the amount of interest payments,

since beginning and ending bond prices are determined by market forces.

20) An example of a barrier to entry is high prices relative to costs.

21) The yield to maturity is normally equal to the coupon rate.

22) A call option is usually issued in conjunction with convertible bonds.

23) One of the assumptions of capital market theory is that investors can borrow or lend

at the risk free rate.

24) A cash or spot contract is an agreement for the immediate delivery of an asset such

as the purchase of stock on the NYSE.

25) A closed-end investment company is normally referred to as a mutual fund.

26) Indexing is an active portfolio management strategy that seeks to copy the

composition and performance of a selected market index.