Active portfolio management consists of

A. market timing.

B. security analysis.

C. indexing.

D.market timing and security analysis.

E. None of the options are correct.

You purchased one AT&T March 50 call and sold one AT&T March 55 call. Your

strategy is known as

A. a long straddle.

B. a horizontal spread.

C.a money spread.

D. a short straddle.

E. None of the options are correct.

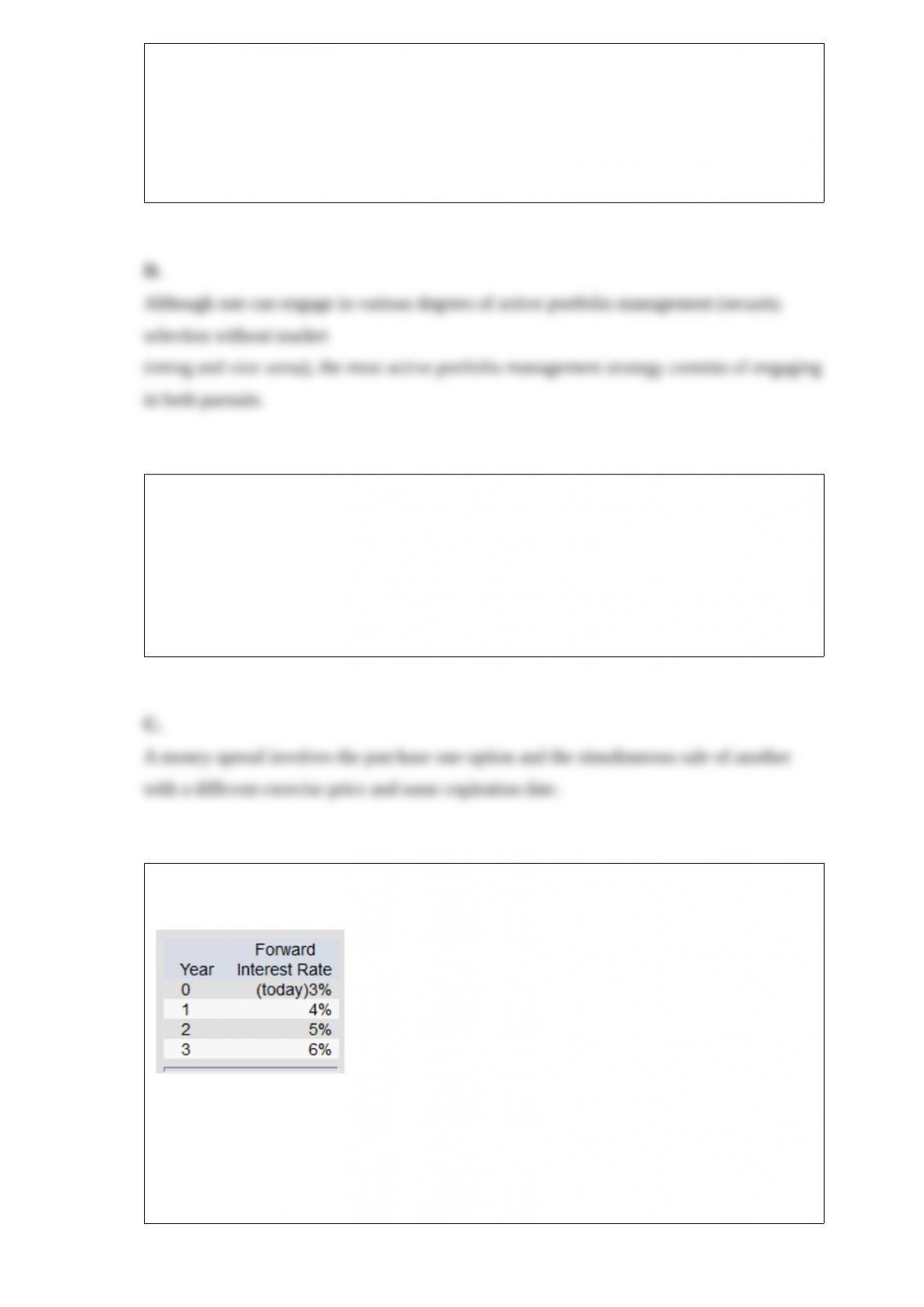

Suppose that all investors expect that interest rates for the 4 years will be as follows:

What is the price of 3-year zero-coupon bond with a par value of $1,000?

A. $889.08

B. $816.58

C. $772.18

D. $765.55

E. None of the options are correct.

The stock price index and new orders for nondefense capital goods are

A.-leading economic indicators.

B. coincidental economic indicators.

C. lagging economic indicators.

D. not useful as economic indicators.

Of the following five investments, ________ is (are) considered the least risky.

A. Treasury bills

B. corporate bonds

C. U.S. agency issues

D. Treasury bonds

E. commercial paper

Alan Barnett is 43 years old and has accumulated $78,000 in his selfdirected defined

contribution pension plan. Each year he contributes $1,500 to the plan, and his

employer contributes an equal amount. Alan thinks he will retire at age 60 and figures

he will live to age 83. The plan allows for two types of investments. One offers a 4%

riskfree real rate of return. The other offers an expected return of 10% and has a

standard deviation of 34%. Alan now has 40% of his money in the riskfree investment

and 60% in the risky investment. He plans to continue saving at the same rate and keep

the same proportions invested in each of the investments. His salary will grow at the

same rate as inflation. How much can Alan expect to have in his risky account at

retirement?

A. $158,982

B. $309,529

C. $543,781

D. $224,651

E. $345,886

In 2016, the proportion of mutual funds (based on total assets) specializing in money

market securities was

A. 21.7%.

B. 28.0%.

C. 54.1%.

D. 73.4%.

E. 17.6%.

If a 7.75% coupon bond is trading for $1,019.00, it has a current yield of

A. 7.38%.

B. 6.64%.

C. 7.25%.

D. 7.61%.

E. 7.18%.

In a factor model, the return on a stock in a particular period will be related to

A. factor risk.

B. nonfactor risk.

C. standard deviation of returns.

D. factor risk and nonfactor risk.

E. None of the options are true.

The standard deviation of a two-asset portfolio is a linear function of the assets’ weights

when

A. the assets have a correlation coefficient less than zero.

B. the assets have a correlation coefficient equal to zero.

C. the assets have a correlation coefficient greater than zero.

D. the assets have a correlation coefficient equal to one.

E. the assets have a correlation coefficient less than one.

Portfolio theory as described by Markowitz is most concerned with

A. the elimination of systematic risk.

B. the effect of diversification on portfolio risk.

C. the identification of unsystematic risk.

D. active portfolio management to enhance returns.

Barrier options have payoffs that

A. have payoffs that only depend on the minimum price of the underlying asset during

the life of the option.

B.depend both on the asset’s price at expiration and on whether the underlying asset’s

price has crossed through some barrier.

C. are known in advance.

D. have payoffs that only depend on the maximum price of the underlying asset during

the life of the option. Barrier options have payoffs that depend both on the asset’s price

at expiration and on whether the underlying asset’s price has crossed through some

barrier.

If the annual real rate of interest is 2.5%, and the expected inflation rate is 3.4%, the

nominal rate of interest

would be approximately

A. 4.9%.

B. 0.9%.

C. –0.9%.

D. 7%.

E. None of the options are correct.

When two risky securities that are positively correlated but not perfectly correlated are

held in a portfolio,

A. the portfolio standard deviation will be greater than the weighted average of the

individual security standard

deviations.

B. the portfolio standard deviation will be less than the weighted average of the

individual security standard

deviations.

C. the portfolio standard deviation will be equal to the weighted average of the

individual security standard

deviations.

D. the portfolio standard deviation will always be equal to the securities’ covariance.

Assume that stock market returns do follow a single-index structure. An investment

fund analyzes 750 stocks in order to construct a mean-variance efficient portfolio

constrained by 750 investments. They will need to calculate ________ estimates of

firm-specific variances and ________ estimate/estimate(s) for the variance of the

macroeconomic factor.

A. 750; 1

B. 750; 750

C. 124,750; 1

D. 124,750; 750

E. 562,500; 750

Hedge fund performance may reflect significant compensation for ________ risk.

A. liquidity

B. systematic

C. unsystematic

D. default

E. unsystematic and default

Assume that stock market returns do not resemble a single-index structure. An

investment fund analyzes 100 stocks in order to construct a mean-variance efficient

portfolio constrained by 100 investments. They will need to calculate ____________

covariances.

A. 45

B. 100

C. 4,950

D. 10,000

Investors want high plowback ratios

A. for all firms.

B. whenever ROE > k.

C. whenever k > ROE.

D. only when they are in low tax brackets.

E. whenever bank interest rates are high.

You buy one Home Depot June 60 call contract and one June 60 put contract. The call

premium is $5 and the put premium is $3.

Your strategy is called

A. a short straddle.

B.a long straddle.

C. a horizontal straddle.

D. a covered call.

E. None of the options are correct.

Given an optimal risky portfolio with expected return of 12%, standard deviation of

26%, and a risk free rate of

3%, what is the slope of the best feasible CAL?

A. 0.64

B. 0.14

C. 0.08

D. 0.35

E. 0.36

The finalized registration statement for new securities approved by the SEC is called

A. a red herring.

B. the preliminary statement.

C. the prospectus.

D. a best-efforts agreement.

E. a firm commitment.

Which of the following factors did Chen, Roll, and Ross not include in their multifactor

model?

A. Change in industrial production

B. Change in expected inflation

C. Change in unanticipated inflation

D. Excess return of long-term government bonds over T-bills

E. All of the factors are included in the Chen, Roll, and Ross multifactor model.

The certainty equivalent rate of a portfolio is

A. the rate that a risk-free investment would need to offer with certainty to be

considered equally attractive as

the risky portfolio.

B. the rate that the investor must earn for certain to give up the use of his money.

C. the minimum rate guaranteed by institutions such as banks.

D. the rate that equates “A” in the utility function with the average risk aversion

coefficient for all risk-averse

investors.

E. represented by the scaling factor “-.005” in the utility function.

Multiple Mutual Funds had year-end assets of $457,000,000 and liabilities of

$17,000,000. There were 24,300,000 shares in the fund at year end. What was Multiple

Mutual’s net asset value?

A. $18.11

B. $18.81

C. $69.96

D. $7.00

E. $181.07

You purchased an annual interest coupon bond one year ago that now has six years

remaining until maturity. The coupon rate of interest was 10%, and par value was

$1,000. At the time you purchased the bond, the yield to maturity was 8%. The amount

you paid for this bond one year ago was

A. $1,057.50.

B. $1,075.50.

C. $1,088.50.

D. $1.092.46.

E. $1,104.13.

GDP refers to

A. the amount of personal disposable income in the economy.

B. the difference between government spending and government revenues.

C. the total manufacturing output in the economy.

D.-the total production of goods and services in the economy.

E. None of the options are correct.

The optimal portfolio on the efficient frontier for a given investor does not depend on

A. the investor’s degreeofrisk tolerance.

B. the coefficient, A, which is a measure of risk aversion.

C. the investor’s required rate of return.

D. the investor’s degreeofrisk tolerance and the investor’s required rate of return.

E. the investor’s degreeofrisk tolerance and the coefficient, A, which is a measure of

risk aversion.

A reward-to-volatility ratio is useful in

A. measuring the standard deviation of returns.

B. understanding how returns increase relative to risk increases.

C. analyzing returns on variable-rate bonds.

D. assessing the effects of inflation.

E. None of the options are correct.

If you took a long position in a pork bellies futures contract and then forgot about it,

what would happen at the expiration of the contract?

A. Nothing—the seller understands that these things happen.

B. You would wake up to find the pork bellies on your front lawn.

C. Your broker would send you a nasty letter.

D. You would be notified that you owe the holder of the short position a certain amount

of cash.

E. You would be notified that you have to pay a penalty in addition to the regular cost

of the pork bellies.

In order for you to be indifferent between the after-tax returns on a corporate bond

paying 8.5% and a tax-exempt municipal bond paying 6.12%, what would your tax

bracket need to be?

A. 33%

B. 72%

C. 15%

D. 28%

E. Cannot be determined from the information given.

Suppose the following equation best describes the evolution of β over time:

t = 0.18 + 0.63βt– 1.

If a stock had a β of 1.09 last year, you would forecast the β to be _______ in the

coming year.

A. 0.87

B. 0.18

C. 0.63

D. 0.81

In 2015, the U.S. equity market represented __________ of the world equity market.

A. 19%

B. 60%

C. 43%

D. 41%

A portfolio consists of 400 shares of stock and 200 calls on that stock. If the hedge ratio

for the call is 0.6, what would be the dollar change in the value of the portfolio in

response to a $1 decline in the stock price?

A. +$700

B. +$500

C. −$580

D. −$520

If you sold an S&P 500 Index futures contract at a price of 950 and closed your position

when the index futures was 947, you incurred

A. a loss of $1,500.

B. a gain of $1,500.

C. a loss of $750.

D. a gain of $750.

E. None of the options are correct.

The performance of an internationally-diversified portfolio may be affected by

A. country selection.

B. currency selection.

C. stock selection.

D. All of the options are correct.

E. None of the options are correct.