1) When identifying undervalued and overvalued assets, which of the following

statements is false?

a. An asset is properly valued if its estimated rate of return is equal to its required rate

of return.

b. An asset is considered overvalued if its estimated rate of return is below its required

rate of return.

c. An asset is considered undervalued if its estimated rate of return is above its required

rate of return.

d. An asset is considered overvalued if its required rate of return is below its estimated

rate of return.

e. None of the above (that is, all are true statements)

2) The term structure of interest rates is a static function that relates the

a. Term to call and the yield to maturity.

b. Term to maturity and the yield to maturity.

c. Term to call and the yield to call.

d. Term to maturity and the coupon rate.

e. Term to maturity and the current yield.

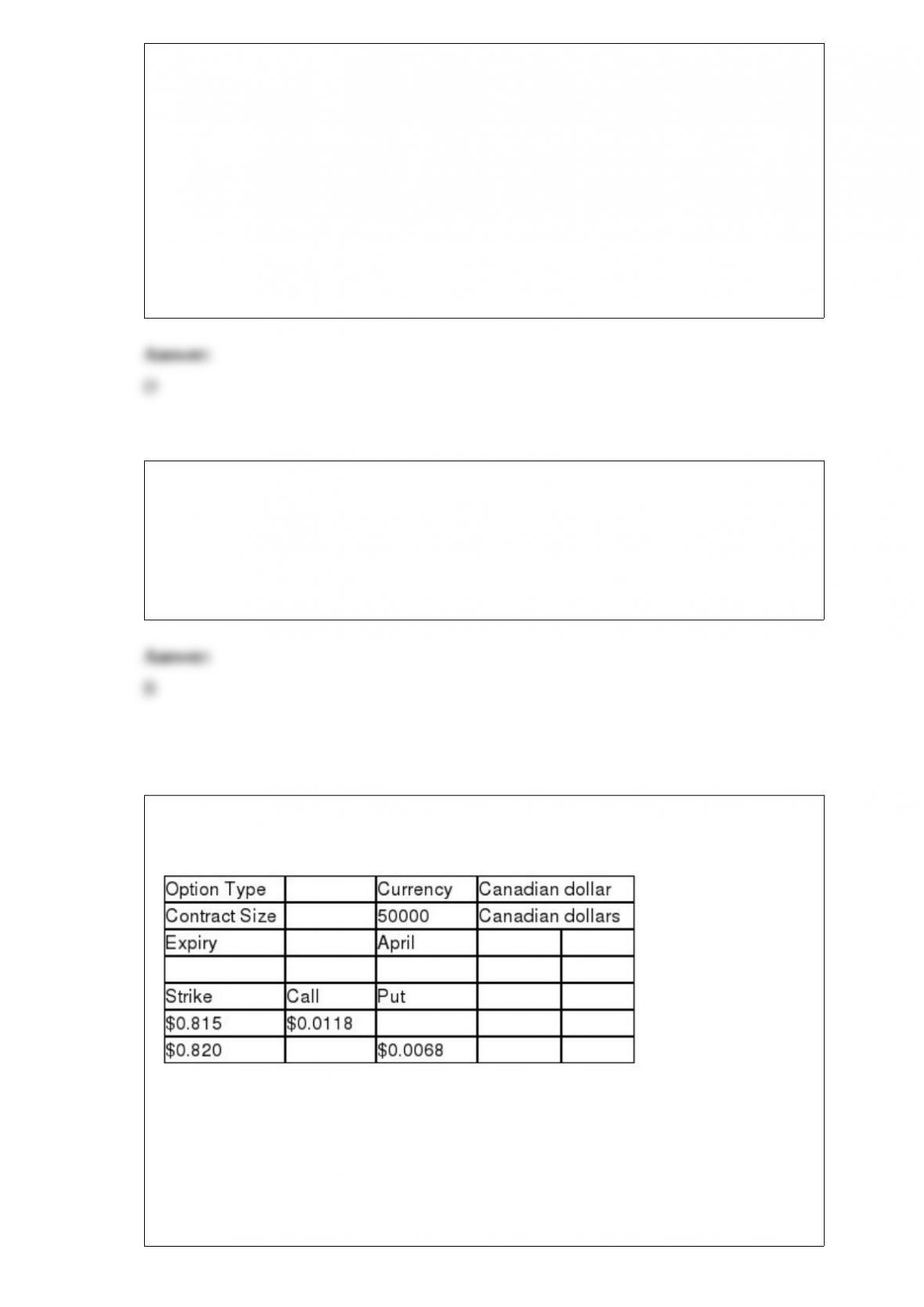

3) Exhibit 22.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

If the spot rate at expiration is $0.90 and the call option was purchased, what is the

dollar gain or loss?

a. $0

b. $3750 gain

c. $3660 gain

d. $4650 loss

e. $2680 loss

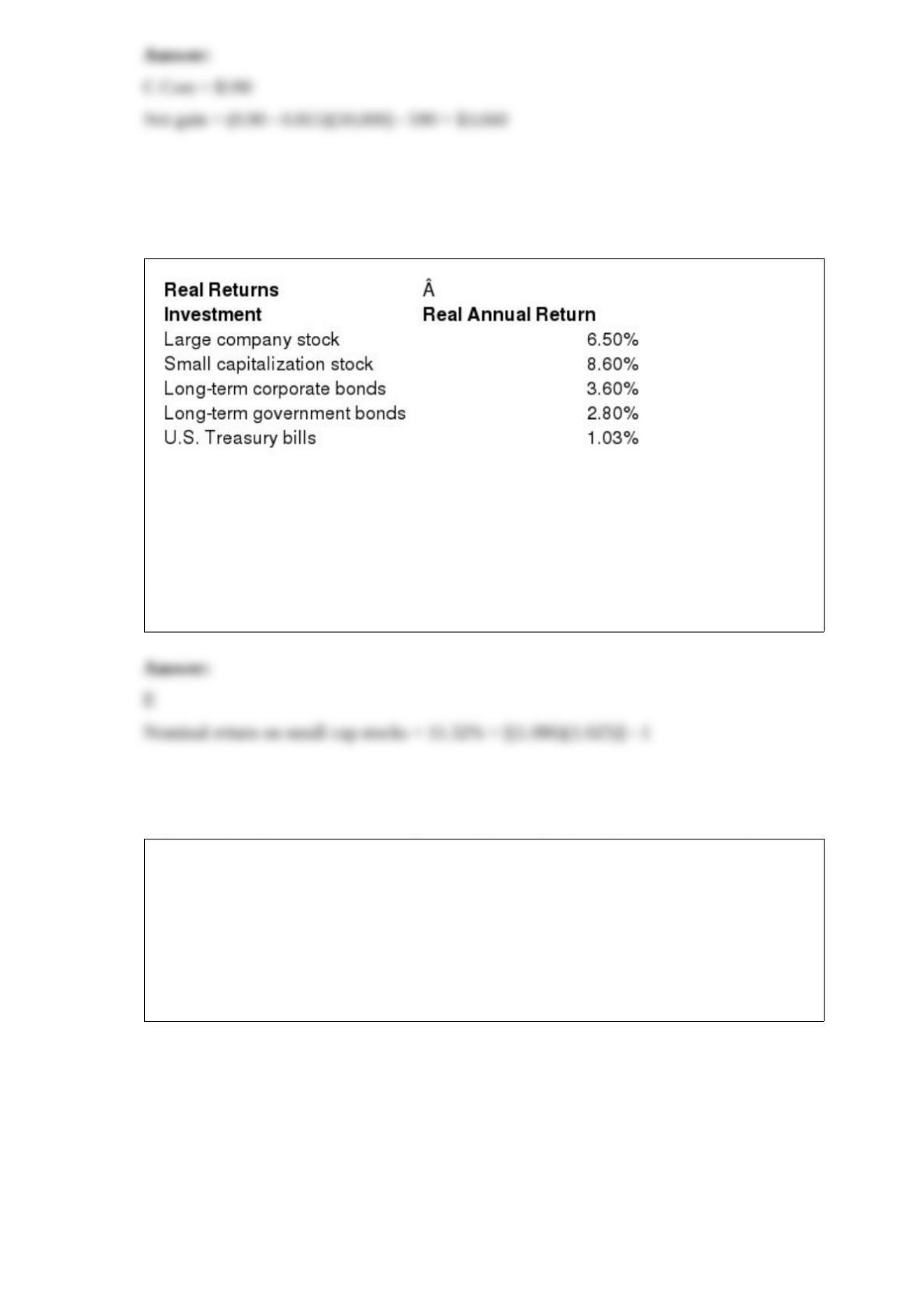

4) The annual rate of inflation is 2.5%

Refer to Exhibit 3.2. What is the small capitalization stock nominal return?

a.3.56%

b.5.37%

c.6.19%

d.9.16%

e.11.32%

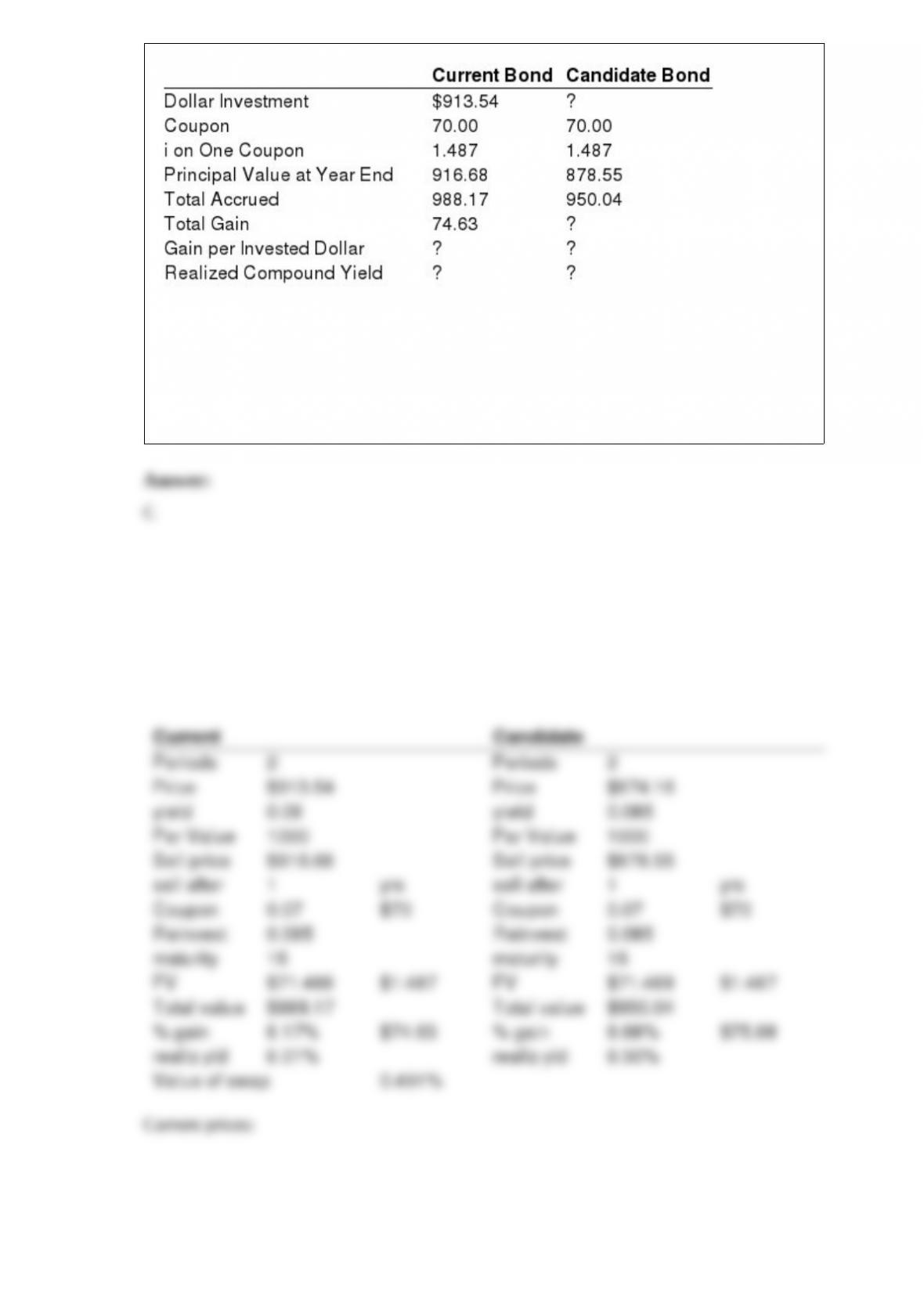

5) Exhibit 19.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The following information is given concerning a substitution swap. You currently hold

a 15 year, 7 percent coupon bond priced to yield 8 percent. As a swap candidate you are

considering a 15 year, 7 percent coupon bond priced to yield 8.5 percent. Assume a

reinvestment rate of 8.5 percent, semiannual compounding, and a one-year workout

period.

The value of the swap is ____ basis points in one year.

a. 18.4

b. 23.3

c. 49.1

d. 46.5

e. 46.8

6) The following are classified as contrary trading rules, except the

a. Odd lot short sales.

b. Investment advisory opinions.

c. Relative OTC volume.

d. CBOE put/call ratio.

e. Confidence index.

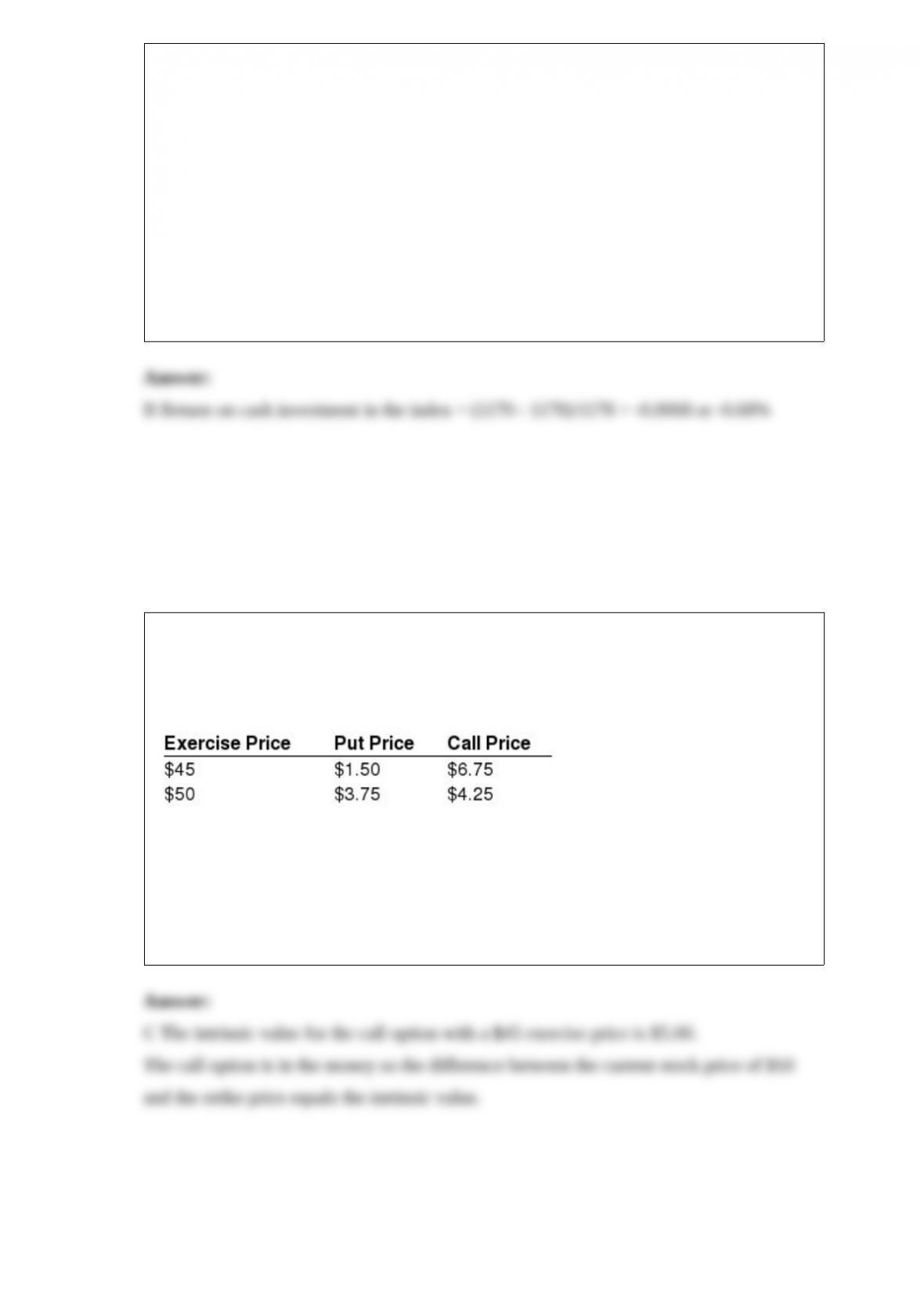

7) Exhibit 20.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

December futures on the S&P 500 stock index trade at 250 times the index value of

1187.70. Your broker requires an initial margin of 10% percent on futures contracts.

The current value of the S&P 500 stock index is 1178.

Calculate the return on a cash investment in the S&P 500 stock index if the ending

index value is 1170 over the same time period.

a. 1.87%

b. -0.68%

c. -14.90%

d. 10.36%

e. None of the above

8) Exhibit 20.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The current stock price of Zanco Corporation is $50. Zanco Corporation has the

following put and call option prices with exercise prices at $45 and $50.

The intrinsic value for the call option with a $45 exercise price is

a. $0.00

b. $1.50

c. $5.00

d. $5.25

e. $6.75

9) Wagner and Tito suggested that a bond portfolio return differing from the return from

the Lehman Brothers Index can be divided into four components. Which of the

following is not included?

a. Policy effect

b. Rate anticipation effect

c. Sector/Quality effect

d. Analysis effect

e. Trading effect

10) Information ratio portfolio performance measures

a. Adjust portfolio risk to match benchmark risk.

b. Compare portfolio returns to expected returns under CAPM.

c. Evaluate portfolio performance on the basis of return per unit of risk.

d. Indicate historic average differential return per unit of historic variability of

differential return.

e. None of the above.

11) A return series has an arithmetic mean of 10.5% and standard deviation of 13%.

Assuming the returns are normally distributed what is the range of returns that an

investor would expect to receive 95% of the time?

a.10.5% to 13%

b.-2.5% to 23.5%

c.-28.5% to 49.5%

d.-15.5% to 36.5%

e.0% to 36.5%

12) A bond portfolio manager expects a cash inflow of $12,000,000. The manager plans

to hedge potential risk with a Treasury futures contract with a value of $105,215. The

conversion factor between the CTD and the bond specified in the Treasury futures

contract is 0.85. The duration of bond portfolio is 8 years, and the duration of the CTD

bond is 6.5 years. Indicate the number of contracts required and whether the position to

be taken is short or long.

a. 114 contracts short

b. 114 contracts long

c. 119 contract short

d. 119 contracts long

e. None of the above

13) Collateralized Mortgage obligations are

a. Mortgage pass-through securities.

b. Mortgage pass-through securities with varying maturities.

c. Mortgage pass-through securities with no default risk.

d. Mortgage pass-through securities with variable coupon rates.

e. None of the above.

14) Which of the following is true of the various market index series?

a.A low correlation exists between the U.S. indexes and those of Japan.

b.The NYSE series have higher rates of return and risk measures than the AMEX and

OTC series.

c.A low correlation exists between alternative series that include almost all NYSE

stocks.

d.A low correlation exists between alternative bond series.

e.None of the above

15) Under the following conditions, what are the expected returns for stocks Y and Z?

a. 17.61% and 13.23%

b. 16.25% and 18.25%

c. 13.24% and 28.46%

d. 14.83% and 17.69%

e. None of the above

16) When applying active management techniques to a global portfolio the additional

concern is expectations regarding exchange rates between countries.

17) The value of the stocks traded in the over-the-counter market is greater than the

combined values of the stocks traded on the New York Stock Exchange and the

American Stock Exchange combined.

18) Growth companies are those firms that consistently earn higher rates of return by

assuming greater amounts of risk.

19) Bonds rated BB or above are considered to be investment grade bonds.

20) Index options are settled by delivery of the stocks that make up the index.

21) Tracking error is defined as the degree to which the portfolio’s returns deviate from

those of the actual index.