Interest rate risk is part of the loan commitment contingent risk because of the

uncertainty of changes in interest rates before the borrower exercises his option to

borrow.

Answer:

An interest-only (IO) mortgage-backed strip is a rare example of a negative duration

asset.

Answer:

One reason for basis risk in an interest rate swap is that changes in the index on the

variable rate portion of the swap may not be perfectly correlated with changes in the

index on the balance sheet portion of the liabilities.

Answer:

One reason for the rapid growth of the OTC interest rate and foreign exchange swap

markets is that banks are not required to allocate any capital toward their usage.

Answer:

Which of the following is TRUE about the values of most money market mutual fund

shares?A. They fluctuate heavily.

B. Values are fixed at $1.

C. Values are fixed at $100.

D. They depend on market demand.

E. They are considered closed-end funds.

Answer:

A disadvantage to modern portfolio theory (MPT) is that small institutions generally

hold significant amounts of regionally specific and illiquid loans.

Answer:

The buyer of a bond call option stands to make a positive payoff if changes in market

interest rates cause the bond price to rise above the exercise price.

Answer:

All commercial banks must be members of the Federal Reserve System.

Answer:

In recent years, commercial banks have attempted to expand their activities into

nonbanking areas, but securities firms have not been interested in expanding into

commercial banking.

Answer:

The trading process of options is the same as that of futures contracts.

Answer:

Cash management services include the collection, disbursement, and transfer of funds.

Answer:

NOW accounts are potentially less prone to withdrawal risk than demand deposits.

Answer:

Which of the following observations concerning trust departments is TRUE?A. They

are found only among smaller community banks.

B. Only the largest banks have sufficient staff to offer trust services.

C. They provide banking services to other banks.

D. Pension fund assets are the largest category of assets managed by trust departments.

E. They primarily handle assets for financially sophisticated investors.

Answer:

Long-term mutual funds invest primarily in long-term, fixed-income securities such as

corporate and/or government bonds.

Answer:

Financial institutions act as intermediaries between suppliers and demanders of money.

Answer:

Class B shares of a mutual fund are typically charged a back-end load when the shares

are redeemed.

Answer:

Depository institutions generally rely on each other for cash and to meet their daily

liquidity needs.

Answer:

An interest rate swap is essentially a series of forward contracts on interest rates.

Answer:

Savings institutions enjoyed record profitability during the late 1990s and early 2000s.

Answer:

All else equal, once a mortgage pool has aged, prior prepayments of mortgages in the

pool have no bearing on the current value of the pool or the future prepayment rates of

mortgages left in the pool.

Answer:

RAROC is a measure of a firm’s cost of debt.

Answer:

Funding costs generally are positively related to the period of time the liability remains

on the balance sheet.

Answer:

Immunization of an FIs net worth requires the duration of the liabilities to be adjusted

for the amount of leverage on the balance sheet.

Answer:

Equity mutual funds may contain common stock, but not preferred stock.

Answer:

A positive net exposure position in FX implies the FI is net short in a currency.

Answer:

By definition, all transaction accounts at U.S. FIs allow account holders to make

unlimited withdrawals.

Answer:

Commercial bank call reports are provided by banks to the Federal Reserve and are

useful in determining the proportion of loans in different classifications for the entire

banking system.

Answer:

If the interest rate spread between rate sensitive assets and rate sensitive liabilities

increases for a bank, future increases in interest rates will lead to an increase in net

interest income.

Answer:

In the case where a borrower defaults on a loan, the FI may lose only a portion of the

principal that was loaned.

Answer:

Managerial monitoring efficiency and credit risk management strategies affect the

shape of the risk of the loan return distribution.

Answer:

Under Generally Accepted Accounting Principles, FIs have flexible rules in recognizing

the amount and timing of loan losses.

Answer:

despite a sovereign debt problem that plagued Greece in 2010, by 2012 U.S. Banks had

increased their exposure to Greek debt.

Answer:

Price volatility is the price sensitivity times the potential adverse move in yield.

Answer:

The Security Investor Protection Corporation (SIPC) protects investors against losses of

up to $25,000,000 caused by the failure of a securities firm.

Answer:

Directed brokerage is a trading abuse where a mutual fund and a brokerage agree to

promote sales of certain funds in exchange for orders of specific stocks and bonds.

Answer:

What is the minimum total risk-adjusted capital (Tier I + Tier II) required for both of

the off-balance-sheet letters of credit under the Basel II standards? A. $3.84 million.

B. $3.68 million.

C. $3.20 million.

D. $4.80 million.

E. $6.40 million.

Answer:

Which term refers to the risk that the cost of rolling over or re-borrowing funds will rise

above the returns being earned on asset investments? A. Reinvestment risk.

B. Credit risk.

C. Refinancing risk.

D. Liquidity risk.

E. Sovereign risk.

Answer:

The root cause of much of the losses of FIs during the financial crisis of 2008-2009 was

A. interest rate risk.

B. market risk.

C. sovereign risk.

D. firm-specific risk.

E. systematic risk.

Answer:

Which of the following FIs does not provide a business lending function? A.

Depository institutions.

B. Insurance companies.

C. Finance companies.

D. Pension funds.

E. Mutual funds.

Answer:

Eveningstar open-end fund has 1,000 shares outstanding and has the following assets in

its portfolio: 100 shares of Procter & Gamble (P&G) priced at $30.00, 300 shares of

Intel priced at $50.00 and 200 shares of Microsoft priced at $60.00. The Morningstar

closed-end fund has the following stocks in its portfolio: 300 shares of P&G and 300

shares of Microsoft. It has a total of 500 shares outstanding.

Suppose Morningstar issues another 250 shares and purchases shares of Intel with the

funds. What is its new NAV of Morningstar? (Assume the NAV found before the price

change in P&G and Microsoft in the previous question).A. $39.20.

B. $55.20.

C. $34.40.

D. $30.00.

E. $34.00.

Answer:

A Eurodollar transaction A. can only occur in Europe.

B. is a swap of Euros for dollars.

C. is a transaction that involves dollars outside of the U.S.

D. is a swap of dollars for Euros.

E. must be reported immediately to international monetary authorities.

Answer:

Why were inverse floaters developed? A. To exchange specified periodic cash flows in

the future based on some underlying instrument.

B. To better manage their interest rate, foreign exchange, and credit risks of corporate

enterprises.

C. To lower the cost of financing for government agencies.

D. To determine payments and timing of payments when there is no standardized

contract.

E. To keep the swap market liquid by locating or matching counterparties.

Answer:

Up-front fees on loan commitments are charged as a certain percentage ofA.

commitment size.

B. loan taken down.

C. utilized portion of commitment size.

D. unused portion of commitment size.

E. interest payable on the loan commitment.

Answer:

What is the credit equivalent amount of the off-balance-sheet interest rate swaps if it is

in-the-money by $1 million? A. $1.0 million.

B. $2.0 million.

C. $3.0 million.

D. $4.0 million.

E. $5.0 million.

Answer:

Which of the following is the newest addition to the derivative securities markets? A.

Options contracts.

B. Futures contracts.

C. Swap agreements.

D. Forward contracts.

E. Credit derivatives.

Answer:

The realization of revenue synergies from the acquisition of a bank may comeA. from

expansion into less than fully competitive markets.

B. from acquiring a bank in a growing market.

C. through diversification of asset and liability mixes between the two banks.

D. All of the above.

E. Answers B and C only.

Answer:

The following question are based on material in Appendix 8B

The term structure of interest rates assumes thatA. the risk of all assets is the same.

B. the time to maturity for all assets is the same.

C. the coupon rate of all assets is the same.

D. The market value of assets is the same.

E. All of the above.

Answer:

What is the net gain or loss on the loan given that the exchange rates at the time of

repayment were $1.63/≤ in the cash market and 1.62/≤ in the futures market? Assume

that the futures position is opened and unwound as stated in previous question. A.

$2,120,000 loss.

B. $1,330,000 loss.

C. $2,670,000 loss.

D. $1,330,000 gain.

E. $2,670,000 gain.

Answer:

Selling a credit forward agreement generates a payoff similar to A. selling a call option.

B. buying a call option.

C. selling a put option.

D. buying a put option.

E. buying forward contracts.

Answer:

The most common benchmark of relative size of a firm in the securities trading and

underwriting industry is based on A. total asset value.

B. total equity.

C. total debt.

D. annual sales.

E. annual profits.

Answer:

The primary difference between Basel I and the proposed Basel III in calculating

risk-adjusted assets isA. that Basel II considers OBS assets.

B. the use of only three weight classes rather than four classes.

C. a heavier reliance on the use of ratings by external credit rating agencies for the

assignment of assets to weight classes.

D. All of the above.

E. Answers A and C only.

Answer:

Which of these CMO issues has characteristics of both a zero-coupon bond and a

regular bond? A. Class A bonds.

B. Class B bonds.

C. Class C bonds.

D. Class Z bonds.

E. None of the above.

Answer:

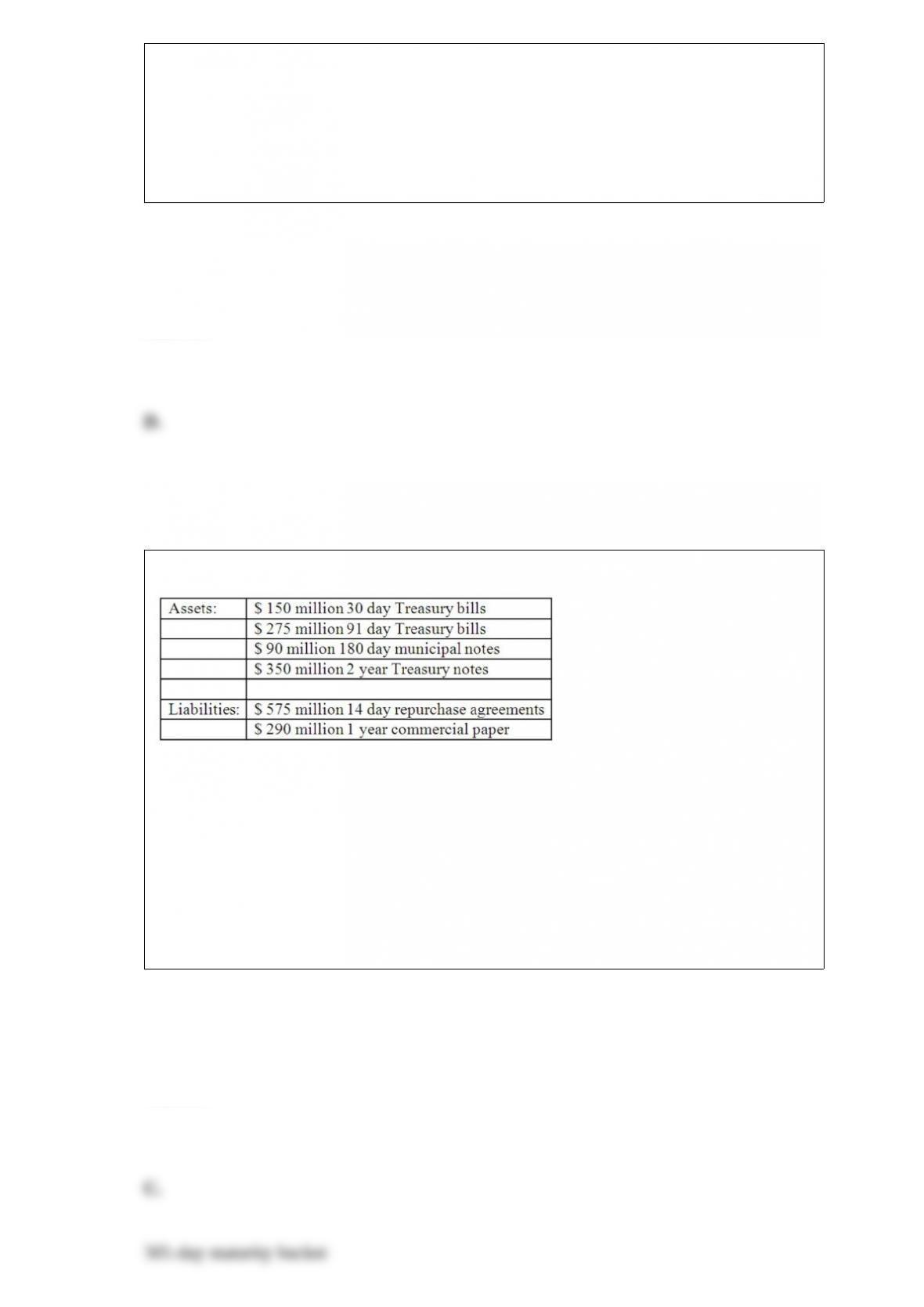

The following are the assets and liabilities of a government security dealer.

Use the repricing model to

determine the funding gap for a maturity bucket of 365 days. A. +$15 million.

B. -$20 million.

C. -$350 million.

D. -$450 million.

E. -$290 million.

Answer:

What are the ways in which an FI can establish a global or international presence?A.

Selling financial services from its domestic offices to foreign customers.

B. Selling financial services through a branch, agency, or representative office

established in the foreign customer’s country.

C. Selling financial services to a foreign customer through subsidiary companies in the

foreign customer’s country.

D. All of the above.

E. Answers A and B only.

Answer:

If Allright wanted to hedge the balance sheet position, what is the interest rate risk

exposure and what hedge would be appropriate?A. The balance sheet position is

exposed to interest rate increases; use a short hedge.

B. The balance sheet position is exposed to interest rate increases; use a long hedge.

C. The balance sheet position is exposed to interest rate decreases; use a long hedge.

D. The balance sheet position is exposed to interest rate decreases; use a short hedge.

E. There is no interest rate risk exposure.

Answer:

Why does basis risk occur? A. Changes in the spot asset’s price are not perfectly

correlated with changes in the price of the asset delivered under a forward or futures

contract.

B. The daily marking-to-market process enables an FI manager to close out a futures

position by taking an exactly offsetting position.

C. Spot and futures contracts are traded in different markets with different demand and

supply functions.

D. Answers B and C only.

E. Answers A and C only.

Answer:

A swap that technically is a succession of forward contracts on interest rates is A. a

commodity swap.

B. a credit swap.

C. a currency swap.

D. an equity swap.

E. an interest rate swap.

Answer:

Under the 1982 guidelines, would the Fed approve the merger of Banks A and B? A. It

is likely to approve because it is not a concentrated market.

B. It is unlikely to approve because the post-merger HHI has increased by over 100.

C. It is likely to approve because the post-merger HHI has increased by over 100.

D. Likely to approve because the post-merger HHI has increased by less than 5,000.

E. It is unlikely to approve because the post-merger HHI has increased by an amount

over 5,000.

Answer:

Which of the following may occur when a sufficient number of borrowers are unable to

repay interest and principal on loans, thus causing an FI’s equity to approach zero? A.

Insolvency risk.

B. Sovereign risk.

C. Foreign exchange risk.

D. Liquidity risk.

E. Interest rate risk.

Answer:

What spread is expected between the one-year maturity B-rated bond and the one-year

Treasury bond in one year? A. 3.00 percent.

B. 5.06 percent.

C. 4.00 percent.

D. 5.00 percent.

E. 7.00 percent.

Answer:

What are the expected end-of-year profits or losses if the bank hedges its interest rate

risk exposure using the swap? A. The bank expects to lose $0.45 million in the first

year and earn $0.58 million in the second year by buying the swap to hedge against

interest rate increases.

B. The bank expects to lose $0.45 million in the first year and earn $0.58 million in the

second year by selling the swap to hedge against interest rate decreases.

C. The bank expects to earn $0.45 million in the first year, lose $0.58 million in the

second year by buying the swap to hedge against interest rate increases.

D. The bank expects to earn $0.45 million in the first year and lose $0.58 million in the

second year by selling the swap to hedge against interest rate decreases.

E. The bank will not do the swap because it has no interest rate risk exposure.

Answer:

Match the following pieces of legislation with the function achieved by each regulation

as stated in question

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Advisers Act

D. Investment Company Act

E. Insider Trading and Securities Fraud Enforcement Act of 1988

F. Market Reform Act of 1990

G. National Securities Markets Improvement Act of 1996

Makes the purchase and sale of mutual fund shares subject to various antifraud

provisions.

Answer:

What is the risk of the loan using the Moody’s Analytics model? A. 4.75 percent.

B. 0.48 percent.

C. 6.89 percent.

D. 2.18 percent.

E. 1.50 percent.

Answer:

What would have been the capital requirements if the FI had securitized the mortgage?

A. $0.

B. $400,000.

C. $200,000.

D. $500,000.

E. $5,000,000.

Answer:

Using the term structure of default probabilities, the implied default probability for

BBB corporate debt during the second year is A. 4.20 percent.

B. 98.0 percent.

C. 2.35 percent.

D. 2.71 percent.

E. 3.88 percent.

Answer:

The BIS definition: “the risk of loss resulting from inadequate or failed internal

processes, people, and systems or from external events,” encompasses which of the

following risks? A. Credit risk and liquidity risk

B. Operational risk and technology risk

C. Credit risk and market risk

D. Technology risk and liquidity risk

E. Sovereign risk and credit risk

Answer: