Which one of the following is most apt to cause a firm to have a higher price-earnings

ratio?

A. slow industry outlook

B. very low current earnings

C. low market share

D. low prospect of firm growth

E. low investor opinion of firm

Answer:

Ritter’s study of SEO’s suggests that:

A. managers appear to be able to successfully time SEO issues when the stock is

overpriced.

B. managers can only successfully time SEO issuance by pure chance.

C. managers tend to be incorrect in their market assessment of the market movement of

their firm’s stock price.

D. returns on SEO-issuing firms are statistically the same as those of style-matched

non-issuers for the five years following issuance.

E. firms are better at timing IPOs than they are at timing SEOs.

Answer:

Last week, Railway Tours paid its annual dividend of $1.20 per share. The company has

been reducing the dividends by 10 percent each year. What is the value of this stock at a

discount rate of 13 percent?

A. $4.70

B. $3.71

C. $8.31

D. $36.00

E. $27.00

Answer:

Suppose your wealthy Aunt Minnie has asked you to manage her large stock portfolio.

You would like to use options to increase her total return and also reduce her risks.

Describe the types of options you would buy or sell, as well as your rationale, given the

following circumstances:

a. Aunt Minnie owns 10,000 shares of a large oil company common stock. You believe

the stock is overpriced, but she won’t let you sell any shares because her late husband

told her to never, ever sell any. How do you protect her from what you believe is an

impending price decline?

b. Your analysis suggests that a technology stock is poised for a large price increase

within the next year. Aunt Minnie won”t agree to spend the dollars required to obtain

shares but has consented to allow you to spend some money on options but only

because she trusts you. You don”t want to disappoint her. What should you do?

Answer:

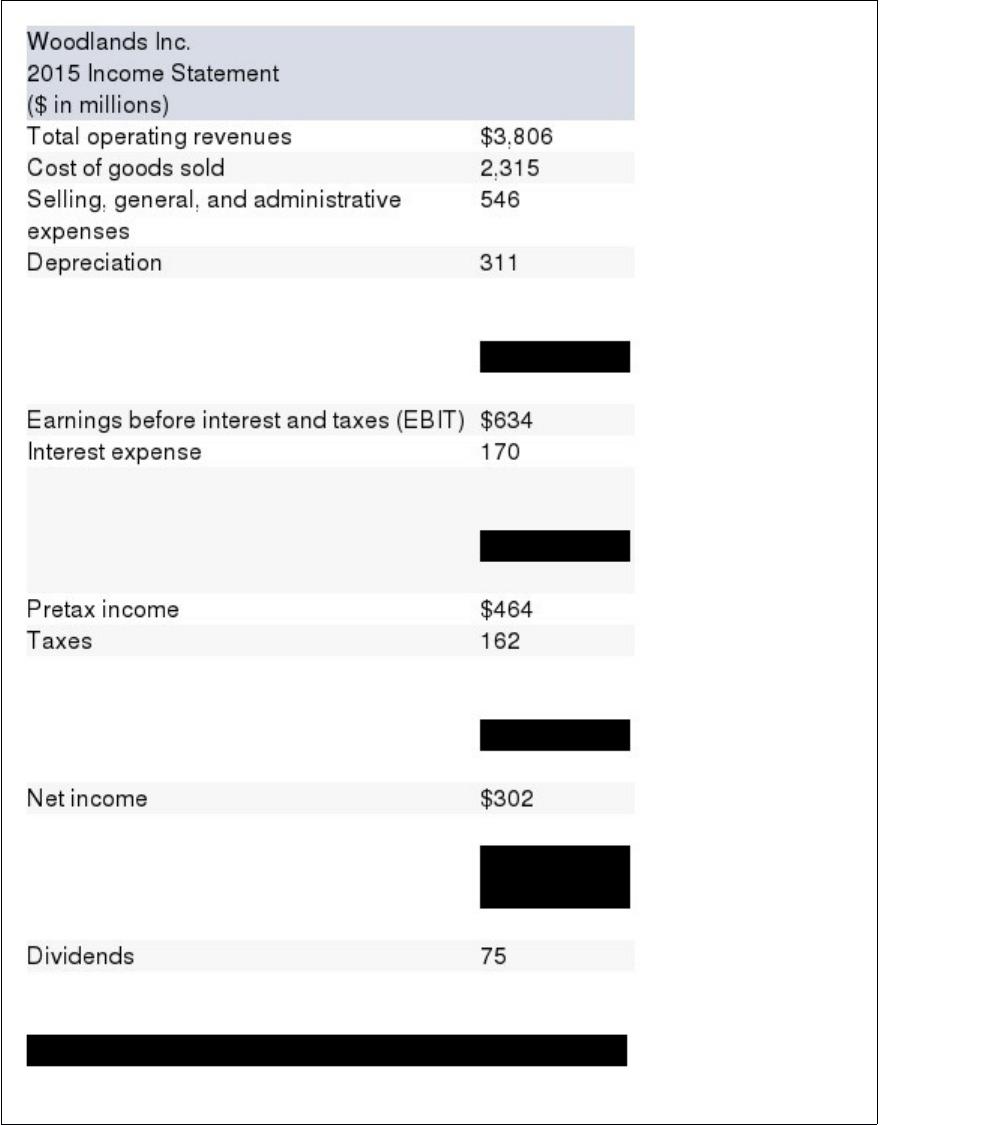

What is the cash flow to stockholders for 2015?

A.$152 million

B.$25 million

C.$0

D.$25 million

E.$75 million

Answer:

Top Notch Tools has average daily receipts of $132,600. These receipts are available

after 2 days on average. The interest rate that could be earned is .02 percent per day.

What is the daily cost of the collection float?

A. $13.26

B. $53.04

C. $6.63

D. $26.52

E. $38.09

Answer:

You purchased 300 shares of Deltona stock for $43.90 a share. You have received a

total of $630 in dividends and $14,620 in proceeds from selling the shares. What is your

capital gains yield on this stock?

A. 6.23%

B. 11.01%

C. 17.68%

D. 9.55%

E. 15.79%

Answer:

If you sell an asset, you are most apt to receive which value for that asset?

A.market value

B.original cost minus accumulated depreciation

C.historical value

D.book value

E.carrying value

Answer:

The payments made by a firm to repurchase shares of its outstanding stock from an

individual investor in an attempt to eliminate a potential unfriendly takeover attempt are

referred to as:

A. a golden parachute.

B. standstill payments.

C. greenmail.

D. a poison pill.

E. a white knight.

Answer:

Given a fixed level of sales and a constant profit margin, an increase in the accounts

payable period can result from:

A. an increase in the cost of goods sold account value.

B. an increase in the ending accounts payable balance.

C. an increase in the cash cycle.

D. a decrease in the operating cycle.

E. a decrease in the average accounts payable balance.

Answer:

Lengthening the credit period effectively _____ the price paid by the customer.

Generally, this acts to _____ sales.

A. increases; increase

B. increases; decrease

C. decreases; decrease

D. decreases; increase

E. increases; have no effect on

Answer:

Assume the spot rate for the British pound currently is .6391 per dollar and the one-year

forward rate is .6389. A risk-free asset in the U.S. is currently earning 3 percent. If

interest rate parity holds, approximately what rate can you earn on a one-year risk-free

British security?

A. 3.16%

B. 3.03%

C. 2.92%

D. 2.84%

E. 2.97%

Answer:

The dividend-irrelevance proposition of Miller and Modigliani depends on which one

of the following relationships between investment policy and dividend policy?

A. The level of investment does not influence or matter to the dividend decision.

B. Once dividend policy is set the investment decision can be made.

C. The investment policy is set ahead of time and not altered by changes in dividend

policy.

D. Since dividend policy is irrelevant there is no relationship between investment policy

and dividend policy.

E. Miller and Modigliani were only concerned about capital structure.

Answer:

The net present value of a project is equal to the:

A. present value of the future cash flows.

B. present value of the future cash flows minus the initial cost.

C. future value of the future cash flows minus the initial cost.

D. future value of the future cash flows minus the present value of the initial cost.

E. sum of the project’s anticipated cash flows.

Answer:

Assume that all costs, assets, and accounts payable change spontaneously with sales.

For simplicity’s sake, assume interest expense also changes spontaneously with sales

(even though you know if may not). The tax rate and dividend payout ratios remain

constant. If the firm’s managers project a firm growth rate of 16 percent for next year,

what will be the amount of external financing needed to support this level of growth?

ANS$$ANSA. $22,444

A. $18,700

B. $24,350

C. $23,911

D. $25,667

Answer:

Lucas invested $4,500 at 6.2 percent, compounded continuously. What will his

investment be worth after 15 years?

A. $15,557.78

B. $9,240.03

C. $11,405.29

D. $12,308.84

E. $8,685.00

Answer:

A corporation is adjudged bankrupt under Chapter 7. Based on APR, shareholders

receive payment, if funds are remaining, after the:

A. bankruptcy administrator but before the creditors.

B. secured creditors but before the unsecured creditors.

C. unsecured creditors but before the IRS.

D. after the employees but before the IRS.

E. after all other parties have been paid.

Answer:

Stock A has an expected return of 12 percent and a variance of .0203. The market has

an expected return of 11 percent and a variance of .0093. What is the beta of Stock A if

the covariance of Stock A with the market is .0137.

A. .68

B. .76

C. 1.55

D. 1.47

E. 1.32

Answer:

The internal rate of return for an investment project is best defined as the:

A. discount rate that causes the NPV to equal zero.

B. difference between the market rate of interest and the discount rate.

C. market rate of interest less the risk-free rate.

D. minimum project acceptance rate set by management.

E. maximum rate that can be earned for a project to be accepted.

Answer:

A project will have more than one IRR if, any only if, the:

A. primary IRR is positive.

B. primary IRR is negative.

C. NPV is zero.

D. cash flow pattern exhibits more than one sign change.

E. cash flow pattern exhibits exactly one sign change.

Answer:

Outdoor Products stock has an expected return of 12.6 percent and betas of: βGNP =

1.52; βI = 1.06; and βEx = 1.28. This expectation is based on a three-factor model with

expected values of: GNP growth of 3.2 percent; inflation of 2.9 percent; and export

growth of 2.2 percent. However, actual growth in these factors turns out to be 3.6

percent, 3.2 percent, and 2.5 percent, respectively. Calculate the stock’s total return if

the company announces they had an industrial accident and the operating facilities will

close down temporarilywhich will reduce the return by 7 percent (i.e.,from 10 percent

down to 3 percent).

A. -4.05%

B. 6.91%

C. 3.57%

D. 7.42%

E. “1.85%

Answer:

Which one of the following statements is false as it relates to considerations firms use

when establishing a credit policy?

A. A firm that supplies a perishable product will tend to offer restrictive credit terms.

B. A firm whose customers are in a high-risk business will tend to offer restrictive credit

terms.

C. Lengthening the credit period effectively reduces the price paid by the customer.

D. Small accounts, associated with firms that find it difficult to acquire a line of credit,

tend to receive longer credit periods.

E. Larger accounts tend to receive more favorable credit terms.

Answer:

Dixon’s has a beginning receivables balance on January 1st of $930. Sales for January

through April are $970, $1,050, $1,330, and $1,460, respectively. The accounts

receivable period is 36 days. How much did the firm collect in the month of March?

Assume a 30-day month.

A. $1,034

B. $1,316

C. $1,289

D. $1,350

E. $1,180

Answer:

All of these are carrying costs of inventory except:

A. storage costs.

B. insurance.

C. restocking costs.

D. theft.

E. the opportunity cost of capital.

Answer:

An asset that can be quickly converted into cash without significant loss in value is

referred to as being:

A.marketable.

B.tangible.

C.intangible.

D.liquid.

E.fixed.

Answer:

Robinson’s has 15,000 shares of stock outstanding with a par value of $1 per share and

a market price of $36 a share. How many shares of stock will be outstanding of the firm

does a 3-for-2 stock split?

A. 10,000 shares

B. 12,500 shares

C. 20,000 shares

D. 22,500 shares

E. 27,500 shares

Answer:

The financial ratio measured as net income divided by sales is known as the firm’s:

A. profit margin.

B. return on assets.

C. return on equity.

D. asset turnover.

E. earnings before interest and taxes.

Answer:

Today, you purchased two natural gas forward contracts for a May 15 delivery. The

contract size is 5,000 MMBtu with quotes in dollars per MMBtu. The spot price was

2.951 at the time you placed your order. The day’s high was 2.954, the low was 2.939,

and the settle was 2.948. What was the total amount you had to pay today?

A. $14,740

B. $14,695

C. $14,770

D. $14,755

E. $0

Answer:

A capital budgeting project is usually evaluated on its own merits. That is, capital

budgeting decisions are treated separately from capital structure decisions. In reality,

these decisions may be highly interwoven. This interweaving is most apt to result in:

A. firms rejecting positive NPV, all-equity projects because changing to a capital

structure with debt will always create negative net present values.

B. firms foregoing project analysis and just making decisions at random.

C. corporate financial managers first checking with their investment bankers to

determine the best type of capital to raise before valuing a project.

D. firms accepting some negative NPV all-equity projects because changing the capital

structure adds enough positive leverage tax shield value to create a positive NPV.

E. firms never changing their capital structure because all capital budgeting decisions

will be overridden by capital structure decisions.

Answer:

Which one of these statements is correct concerning the cash cycle?

A. The longer the cash cycle, the more likely a firm will need external financing.

B. Increasing the accounts payable period increases the cash cycle.

C. A positive cash cycle is preferable to a negative cash cycle.

D. The cash cycle can exceed the operating cycle if the payables period is equal to zero.

E. Adopting a more liberal accounts receivable policy will tend to decrease the cash

cycle.

Answer:

The Backwoods Lumber Co. has a debt-equity ratio of .68. The firm’s required return

on assets is 11.7 percent and its levered cost of equity is 15.54 percent. What is the

pretax cost of debt based on MM Proposition II with no taxes?

A. 6.76%

B. 6.39%

C. 7.25%

D. 6.05%

E. 7.50%

Answer:

The capital market line:

A. and the characteristic line are two terms describing the same function.

B. intersects the feasible set at its midpoint.

C. has a vertical intercept at the risk-free rate of return.

D. has a horizontal intercept at the market beta.

E. lies tangent to the opportunity set at its minimum point.

Answer:

One company wishes to acquire another. Which one of the following does not require a

formal vote by the shareholders of the acquired firm?

A. merger

B. acquisition of stock

C. horizontal acquisition of assets

D. consolidation

E. vertical acquisition of assets

Answer: