Which of the inputs in the Black-Scholes option pricing model are directly observable?

A. The price of the underlying security

B. The risk-free rate of interest

C. The time to expiration

D. The variance of returns of the underlying asset return

E. The price of the underlying security, risk-free rate of interest, and time to expiration

Studies of closed end funds find __________, which __________ the EMH.

A. prices at a premium to NAV; is consistent with

B. prices at a premium to NAV; is inconsistent with

C. prices at a discount to NAV; is consistent with

D. prices at a discount to NAV; is inconsistent with

E. prices at premiums and discounts to NAV; is inconsistent with

The current market price of a share of Boeing stock is $75. If a put option on this stock

has a strike price of $70, the put

A.is out of the money.

B. is in the money.

C. sells for a higher price than if the market price of Boeing stock is $70.

D. is out of the money and sells for a higher price than if the market price of Boeing

stock is $70.

E. is in the money and sells for a higher price than if the market price of Boeing stock is

$70.

CDOs are divided in tranches

A. that provide investors with securities with varying degrees of credit risk.

B. and each tranch is given a different level of seniority in terms of its claims on the

underlying pool.

C. and none of the tranches is risky.

D. and equity tranch is very low risk.

E. that provide investors with securities with varying degrees of credit risk, and each

tranch is given a different level of seniority in terms of its claims on the underlying

pool.

Which one of the following stock index futures has a multiplier of $50 times the index

value?

A. Russell 2000

B. S&P 500 (E-mini)

C. Nikkei

D. DAX-30

E. NASDAQ 100

Given an optimal risky portfolio with expected return of 6%, standard deviation of

23%, and a risk free rate of

3%, what is the slope of the best feasible CAL?

A. 0.64

B. 0.39

C. 0.08

D. 0.13

E. 0.36

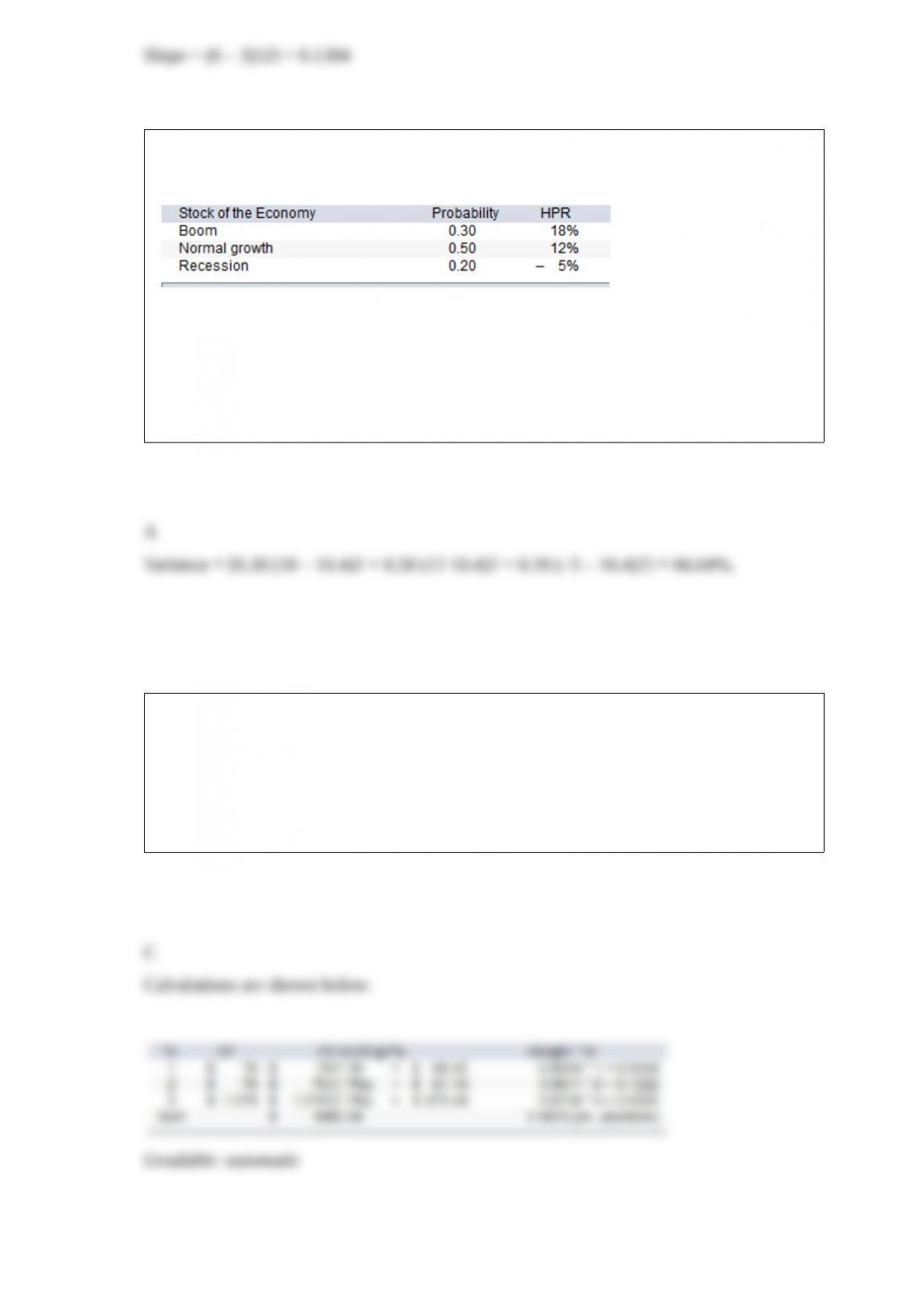

You have been given this probability distribution for the holding-period return for KMP

stock:

What is the expected variance for KMP stock?

A. 66.04%

B. 69.96%

C. 77.04%

D. 63.72%

E. 78.45%

The duration of a par-value bond with a coupon rate of 7% and a remaining time to

maturity of 3 years is

A. 3 years.

B. 2.71 years.

C. 2.81 years.

D. 2.91 years.

The required rate of return on equity is the most appropriate discount rate to use when

applying a ______

valuation model.

A. FCFE

B. FCEF

C. DDM

D. FCEF or DDM

E. P/E

A firm in an industry that is very sensitive to the business cycle will likely have a stock

beta

A.-greater than 1.0.

B. equal to 1.0.

C. less than 1.0 but greater than 0.0.

D. equal to or less than 0.0.

E. There is no relationship between beta and sensitivity to the business cycle.

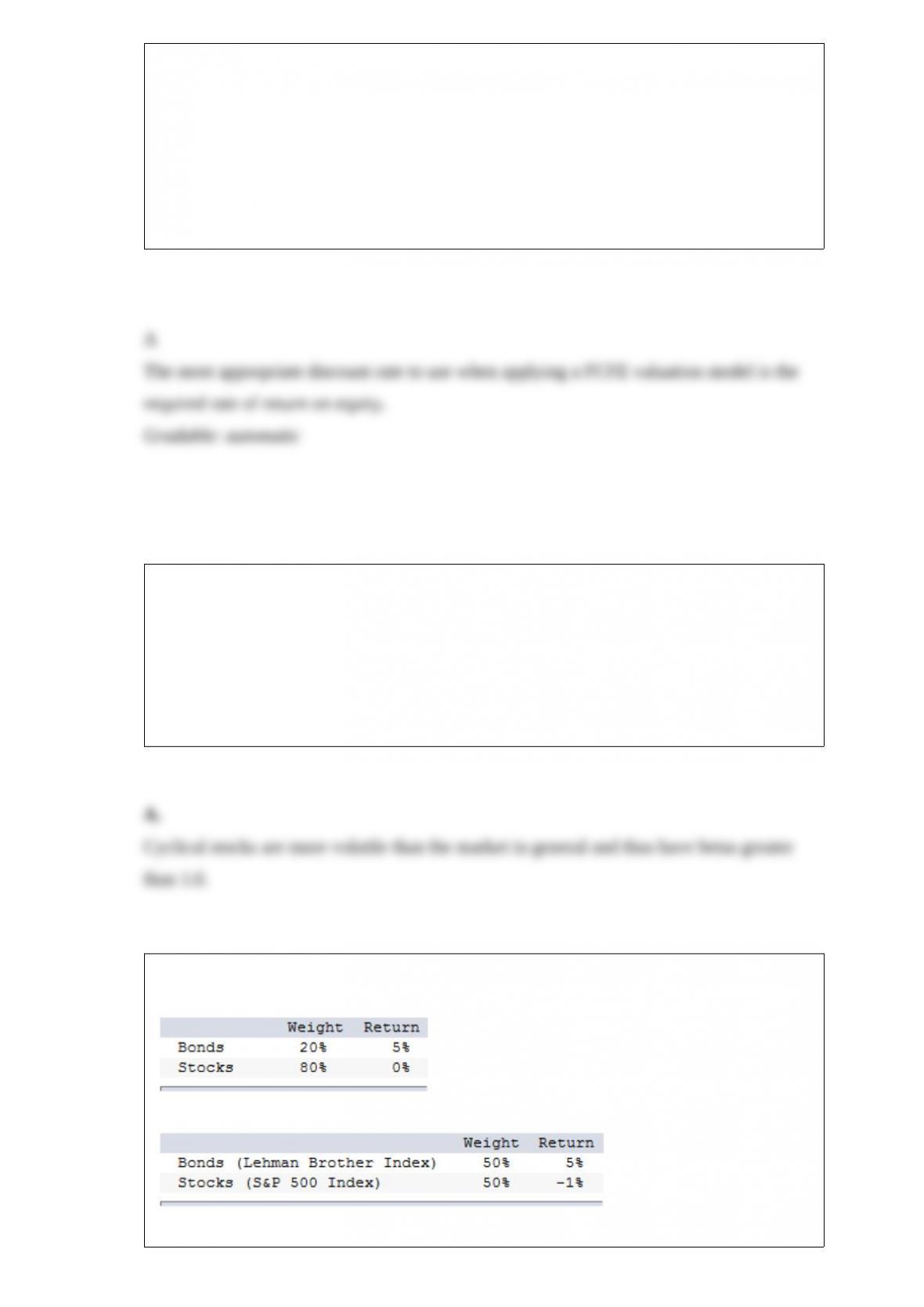

In a particular year, Razorback Mutual Fund earned a return of 1% by making the

following investments in asset classes:

The return on a bogey portfolio was 2%, calculated from the following information.

The total excess return on the Razorback Fund’s managed portfolio was

A. –1.80%.

B. –1.00%.

C. 0.80%.

D. 1.00%.

If the annual real rate of interest is 4%, and the expected inflation rate is 3%, the

nominal rate of interest would

be approximately

A. 4%.

B. 3%.

C. 1%.

D. 5%.

E. None of the options are correct.

The value of a futures contract for storable commodities can be determined by the

_______, and the model

__________ consistent with parity relationships.

A. CAPM; will be

B. CAPM; will not be

C. APT; will not be

D. APT; will be

E. CAPM and APT; will be

Suppose two portfolios have the same average return and the same standard deviation

of returns, but portfolio A has a higher beta than portfolio B. According to the Treynor

measure, the performance of portfolio A

A. is better than the performance of portfolio B.

B. is the same as the performance of portfolio B.

C. is poorer than the performance of portfolio B.

D. cannot be measured as there are no data on the alpha of the portfolio.

E. None of the options are correct.

The Black-Litterman model and Treynor-Black model are

A. nice in theory but practically useless in modern portfolio management.

B.complementary tools that should be used in portfolio management.

C. contradictory models that cannot be used together. Therefore, portfolio managers

must choose which one

suits their needs.

D. not useful due to their complexity.

E. None of the options are correct.

Which two indices had the lowest correlation between them during the 2008-2012

period?

A. S&P and DJIA; the correlation was 0.979

B. S&P and NASDAQ 100; the correlation was 0.928

C. DJIA and Russell 2000; the correlation was 0.908

D. S&P and Russell 2000; the correlation was 0.948

E. NASDAQ 100 and DJIA; the correlation was 0.876

Most professionally managed equity funds generally

A. outperform the S&P 500 Index on both raw and risk-adjusted return measures.

B. underperform the S&P 500 Index on both raw and risk-adjusted return measures.

C. outperform the S&P 500 Index on raw return measures and underperform the S&P

500 Index on risk-adjusted return measures.

D. underperform the S&P 500 Index on raw return measures and outperform the S&P

500 Index on risk-adjusted return measures.

E. match the performance of the S&P 500 Index on both raw and risk-adjusted return

measures.

The risk-free rate is 7%. The expected market rate of return is 15%. If you expect a

stock with a beta of 1.3 to

offer a rate of return of 12%, you should

A. buy the stock because it is overpriced.

B. sell short the stock because it is overpriced.

C. sell the stock short because it is underpriced.

D. buy the stock because it is underpriced.

E. None of the options, as the stock is fairly priced.

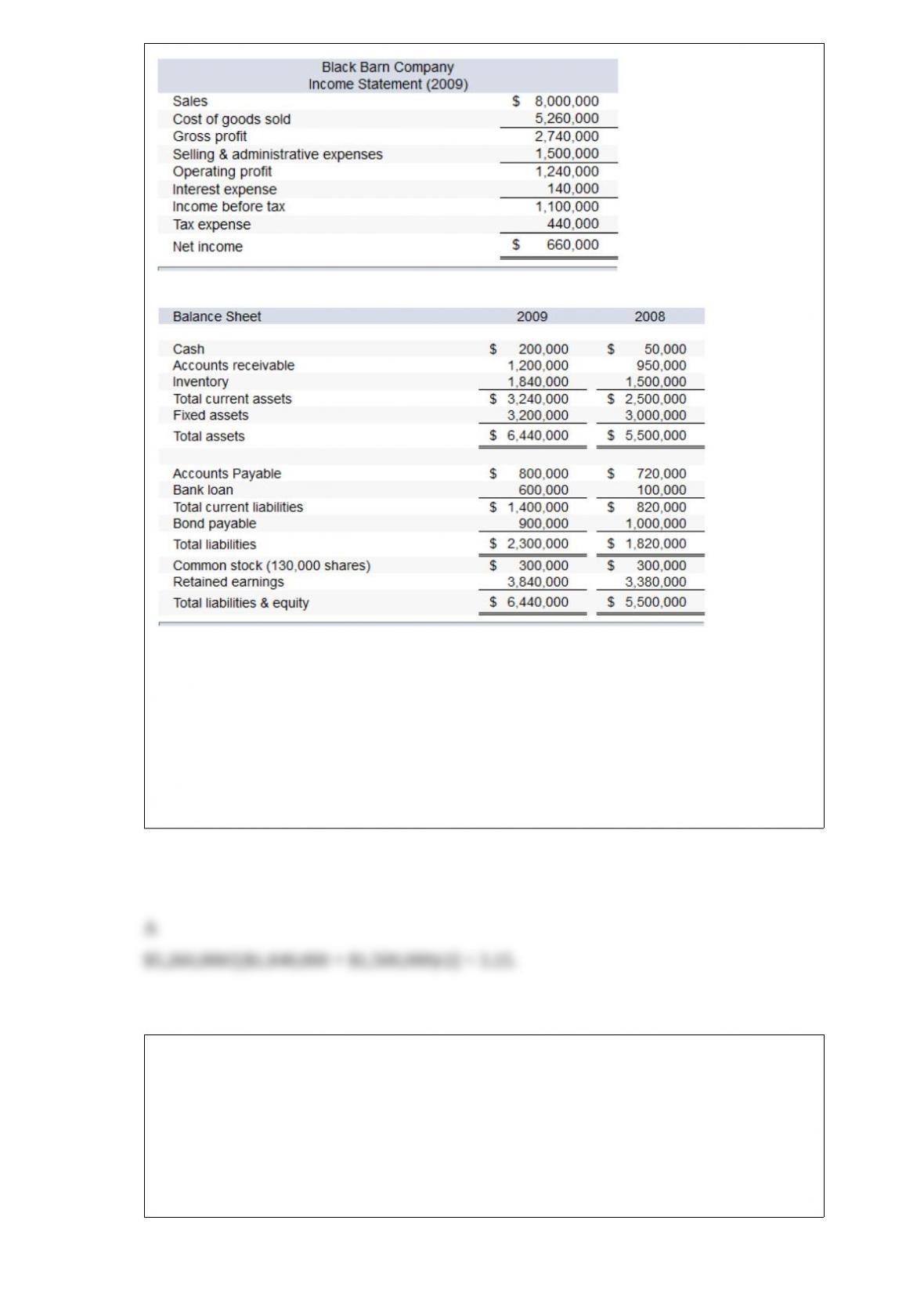

The financial statements of Black Barn Company are given below.

Note: The common shares are trading in the stock market for $40 each.

Refer to the financial statements of Black Barn Company. The firm’s inventory turnover

ratio for 2009 is

A. 3.15.

B. 3.63.

C. 3.69.

D. 2.58.

E. 4.20.

If you determine that the DAX-30 Index futures is underpriced relative to the spot

DAX-30 Index, you could make an arbitrage profit by

A. buying all the stocks in the DAX-30 and selling put options on the DAX-30 Index.

B. selling short all the stocks in the DAX-30 and buying DAX-30 futures.

C. selling all the stocks in the DAX-30 and buying call options on the DAX-30 Index.

D. buying DAX-30 Index futures and selling all the stocks in the DAX-30.

E. None of the options are correct.

Certificates of deposit are insured by the

A. SPIC.

B. CFTC.

C. Lloyds of London.

D. FDIC.

E. All of the options are correct.

Which of the following measures of risk best highlights the potential loss from extreme

negative returns?

A. Standard deviation

B. Variance

C. Upper partial standard deviation

D. Value at risk (VaR)

E. None of the options are correct.

Assume that Bolton Company will pay a $2.00 dividend per share next year, an increase

from the current dividend of $1.50 per share that was just paid. After that, the dividend

is expected to increase at a constant rate of 5%. If you require a 12% return on the

stock, the value of the stock is

A. $28.57.

B. $28.79.

C. $30.00.

D. $31.78.

E. None of the options are correct.

Seaman had a FCFE of $4.6B last year and has 113.2M shares outstanding. Seaman’s

required return on equity is 11.6%, and WACC is 10.4%. If FCFE is expected to grow

at 5% forever, the intrinsic value of Seaman’s shares is

A. $646.48.

B. $64.66.

C. $6,464.80

D. $6.46.

Proponents of the EMH think technical analysts

A. should focus on relative strength.

B. should focus on resistance levels.

C. should focus on support levels.

D. should focus on financial statements.

E. are wasting their time.

Financial futures contracts are actively traded on which of the following indices?

A. The All ordinary index

B. The DAX 30 Index

C. The CAC 40 Index

D. The Toronto 35 Index

E. All of the options are correct.

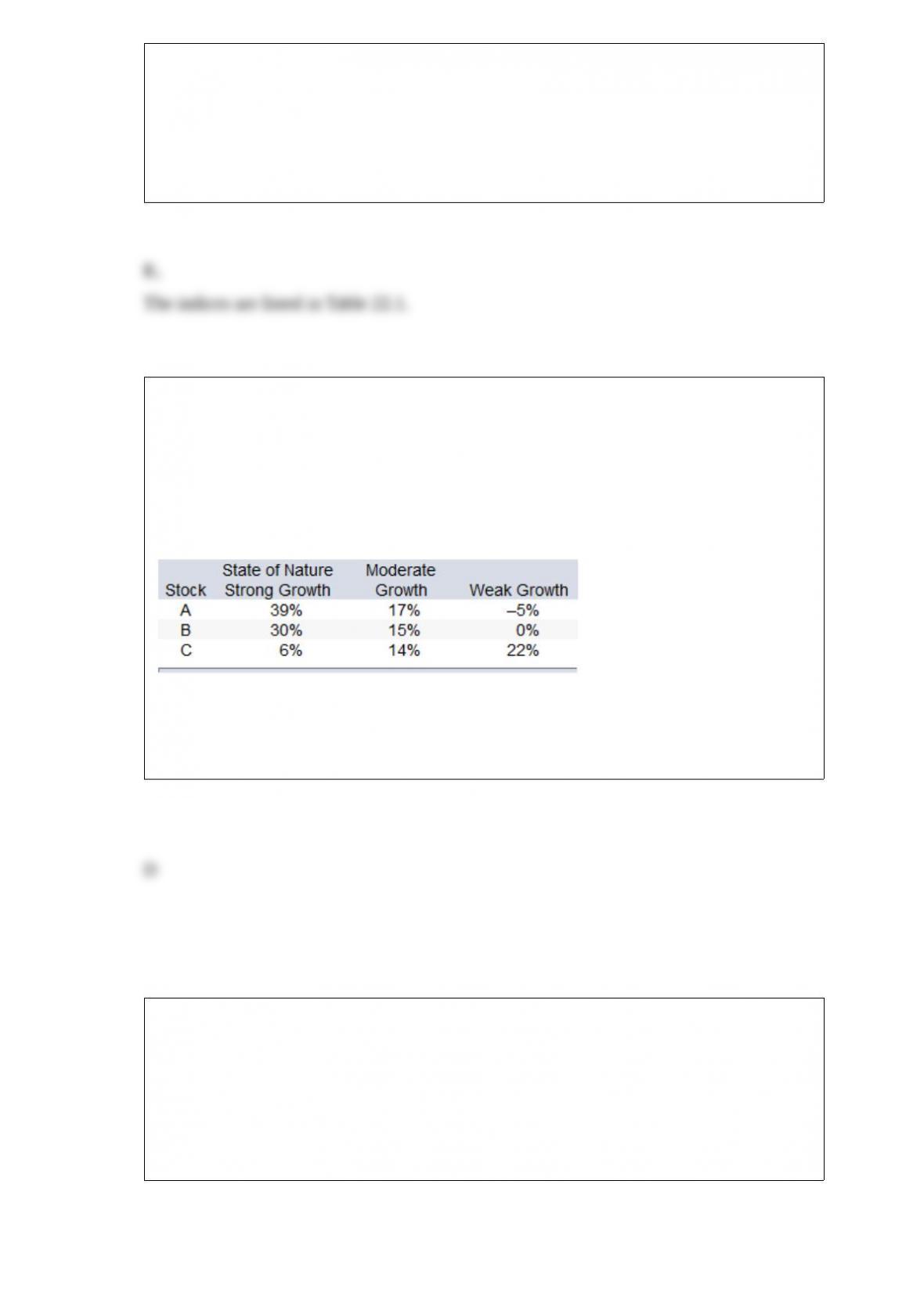

If you invested in an equally-weighted portfolio of stocks B and C, your portfolio return

would be _____________ if economic growth was weak.

There are three stocks: A, B, and C. You can either invest in these stocks or short sell

them. There are three possible states of nature for economic growth in the upcoming

year (each equally likely to occur); economic growth may be strong, moderate, or weak.

The returns for the upcoming year on stocks A, B, and C for each of these states of

nature are given below:

A. -2.5%

B. 0.5%

C. 3.0%

D. 11.0%

A credit default swap is

A. a fancy term for a low-risk bond.

B. an insurance policy on the default risk of a federal government bond or loan.

C. an insurance policy on the default risk of a corporate bond or loan.

D. an insurance policy on the default risk of federal government and corporate bonds

and loans.

E. None of the options are correct.

The smallest component of the fixed-income market is _______ debt.

A. Treasury

B. other asset-backed

C. corporate

D. tax-exempt

E. mortgage-backed

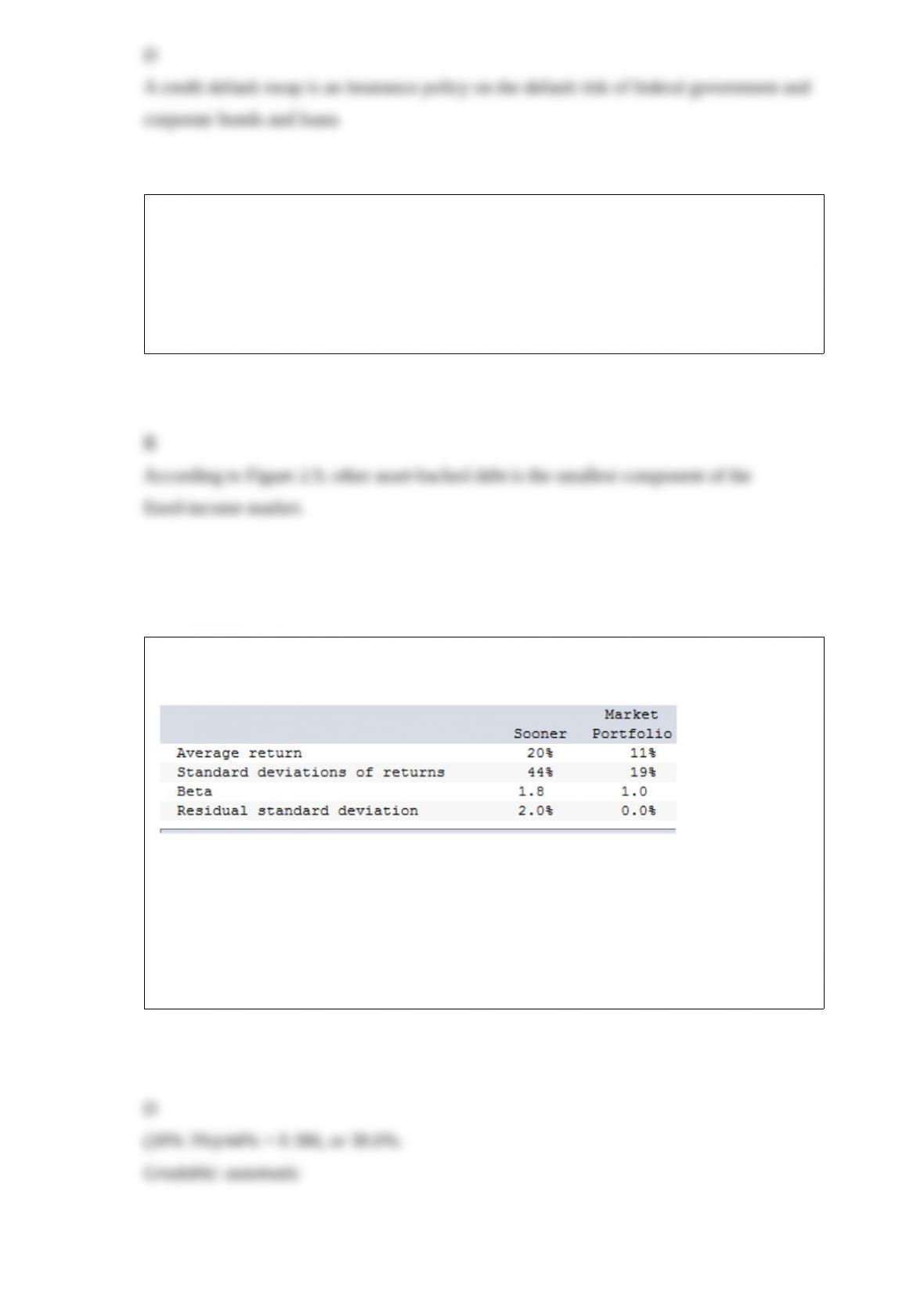

The following data are available relating to the performance of Sooner Stock Fund and

the market portfolio:

The risk-free return during the sample period was 3%.

What is the Sharpe measure of performance evaluation for Sooner Stock Fund?

A. 1.33%

B. 4.00%

C. 8.67%

D. 38.6%

E. 37.14%

When a firm markets new securities, a preliminary registration statement must be filed

with

A. the exchange on which the security will be listed.

B. the Securities and Exchange Commission.

C. the Federal Reserve.

D. all other companies in the same line of business.

E. the Federal Deposit Insurance Corporation.

One incorrect belief that is often cited as a reason for fullyfunded pension funds to

invest in equities is

A. stocks have higher risk.

B. bonds have lower returns.

C. stocks provide a hedge against inflation.

D. stocks have higher returns.

E. All of the options are incorrect beliefs that are often cited.

The market risk, beta, of a security is equal to

A. the covariance between the security’s return and the market return divided by the

variance of the market’s

returns.

B. the covariance between the security and market returns divided by the standard

deviation of the market’s

returns.

C. the variance of the security’s returns divided by the covariance between the security

and market returns.

D. the variance of the security’s returns divided by the variance of the market’s returns.