The number of equivalent units for direct materials and conversion costs must always

be equal.

The main difference between activity-based costing and traditional costing systems is

that activity-based costing uses a separate allocation base for each activity.

Absorption costing is more appropriate than variable costing for making plant

production capacity decisions.

If the expected accounting rate of return meets or exceeds the required rate of return,

the decision rule is to not make the investment.

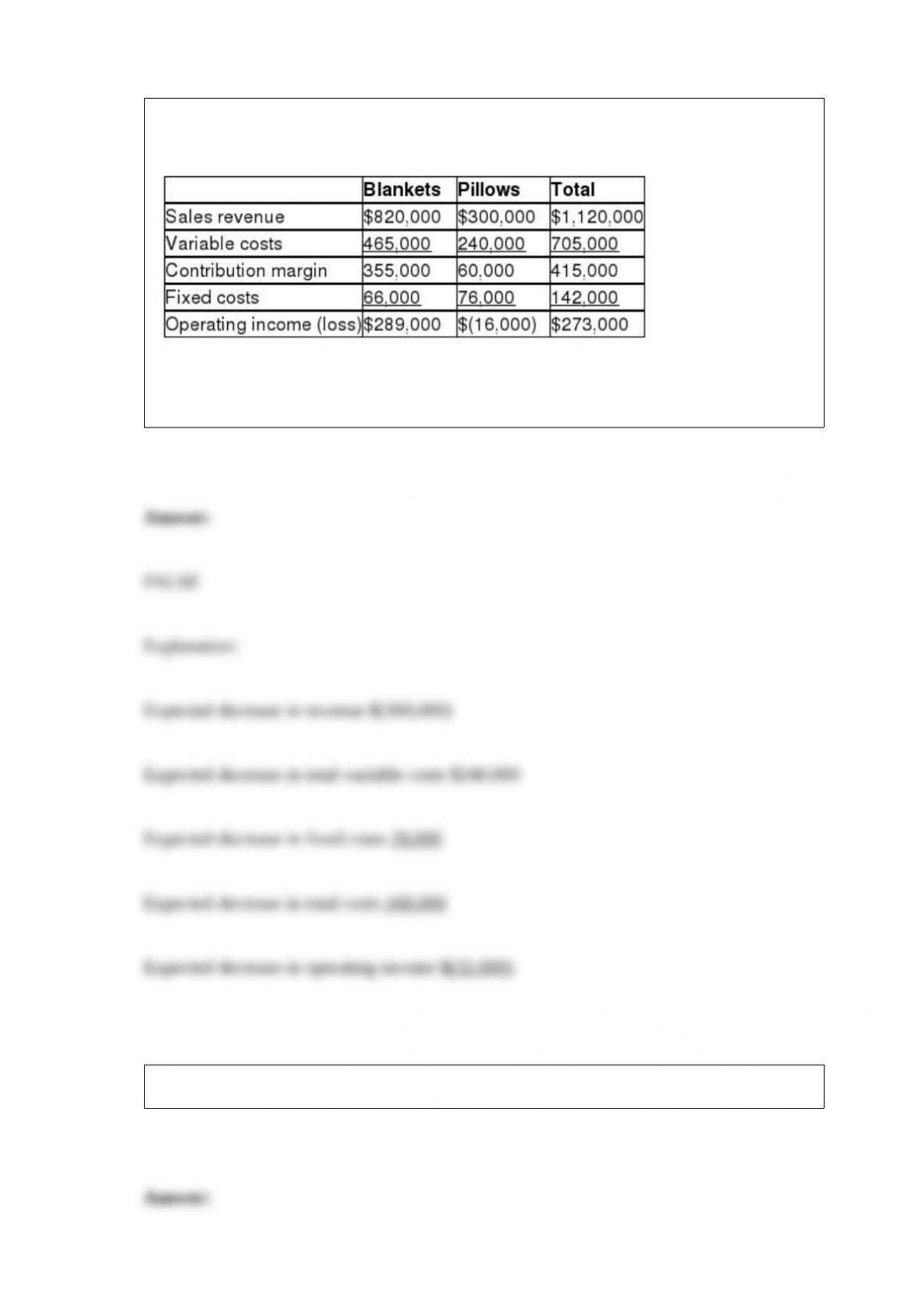

The income statement for Sweet Dreams Company is divided by its two product lines,

blankets and pillows, as follows:

If Sweet Dreams can eliminate total fixed costs of $28,000 by dropping the pillows line,

operating income will increase by $16,000.

Fixed overhead volume variance is a flexible budget variance.

If both favorable and unfavorable variances exist, the variances are subtracted from

each other. The variance is determined to be favorable or unfavorable based on which

one is the larger amount.

An efficiency variance measures how well the business uses its materials or human

resources.

A favorable direct materials cost variance occurs when the actual direct materials cost

incurred is less than the standard direct materials cost.

In a computerized accounting information system, all data are contained in paper

documents that are often stored in filing cabinets and off-site document warehouses.

For short-term pricing decisions, fixed costs are usually not relevant because they do

not change.

A budget is a financial plan that managers use to coordinate a business’s activities.

When preparing the selling and administrative expense budget, there is no need to

separate mixed costs into the fixed and variable components.

When computing the present value, the interest rate will vary depending on the amount

of risk. Safer investments, such as FDIC-insured bank deposits, yield lower interest

rates.

An increase in sales price per unit increases the number of units required to break even.

Comparing actual performance to previously budgeted amounts is part of the ________.

A) controlling function of managerial accounting

B) planning function of managerial accounting

C) reporting function of managerial accounting

D) organizing function of managerial accounting

Which of the following is a period cost for a manufacturing company?

A) office rent

B) wages of factory janitor

C) insurance cost of production equipment

D) raw materials

In which of the following ways is the management of a company accountable to its

communities?

A) making timely interest payments to creditors and dividend payments to investors

B) ensuring the company’s environmental impact is not harmful to its community

C) providing a capital return on the shareholders’ investment

D) repaying principal and interest to the suppliers

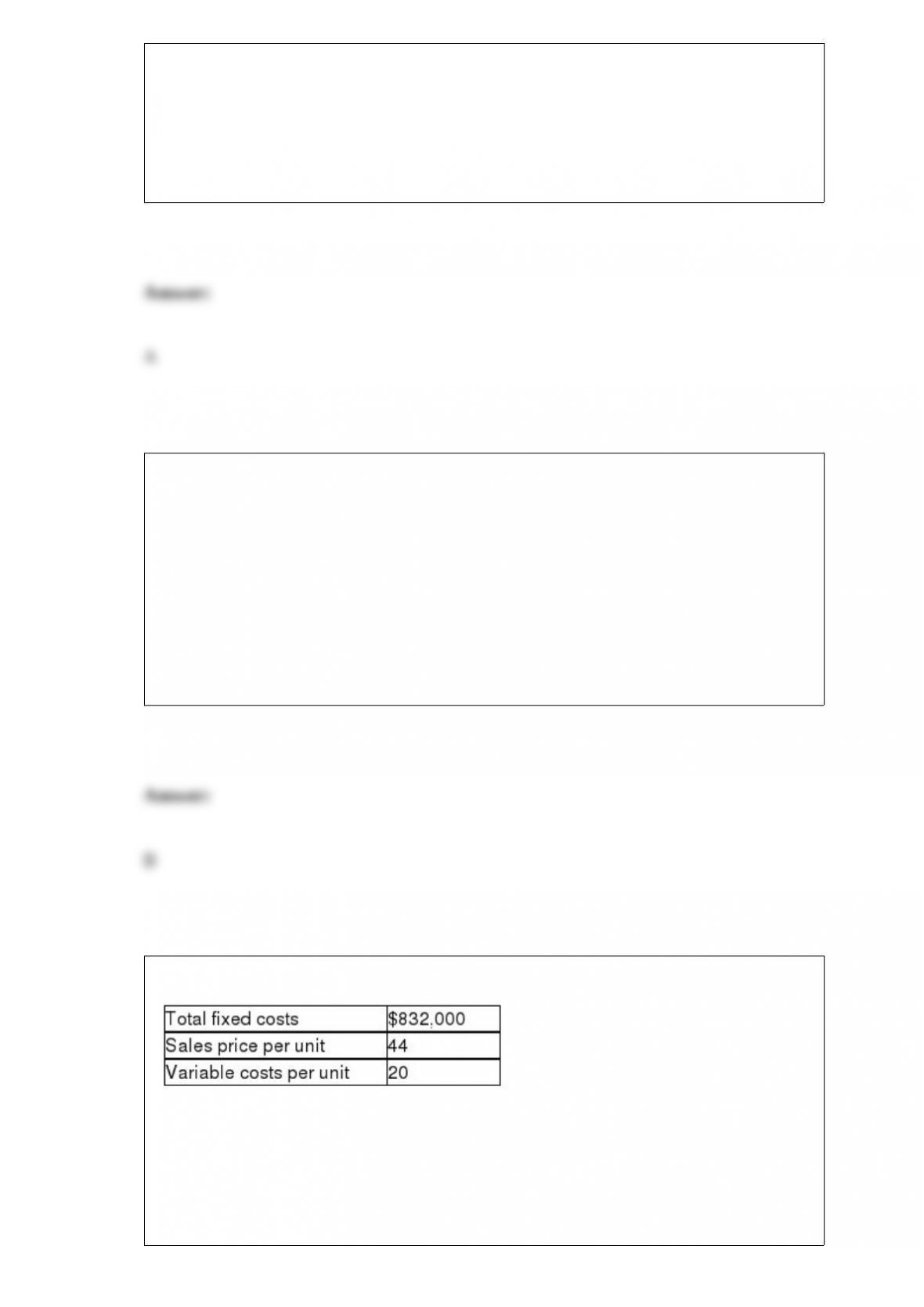

Evans Tiles Company has estimated the following amounts for its next fiscal year:

What will happen to the breakeven point (in units) if Evans can reduce fixed costs by

$22,000? (Round your answer up to the nearest whole unit.)

A) The breakeven point will decrease by 917 units.

B) The breakeven point will decrease by 1,100 units.

C) The breakeven point will increase by 1,100 units.

D) The breakeven point will increase by 500 units.

The cost of goods sold for Frye Manufacturing in the year was $297,000. The January 1

Finished Goods Inventory balance was $31,600, and the December 31 Finished Goods

Inventory balance was $25,600. Calculate the cost of goods manufactured during the

year.

A) $322,600

B) $57,200

C) $291,000

D) $6,000

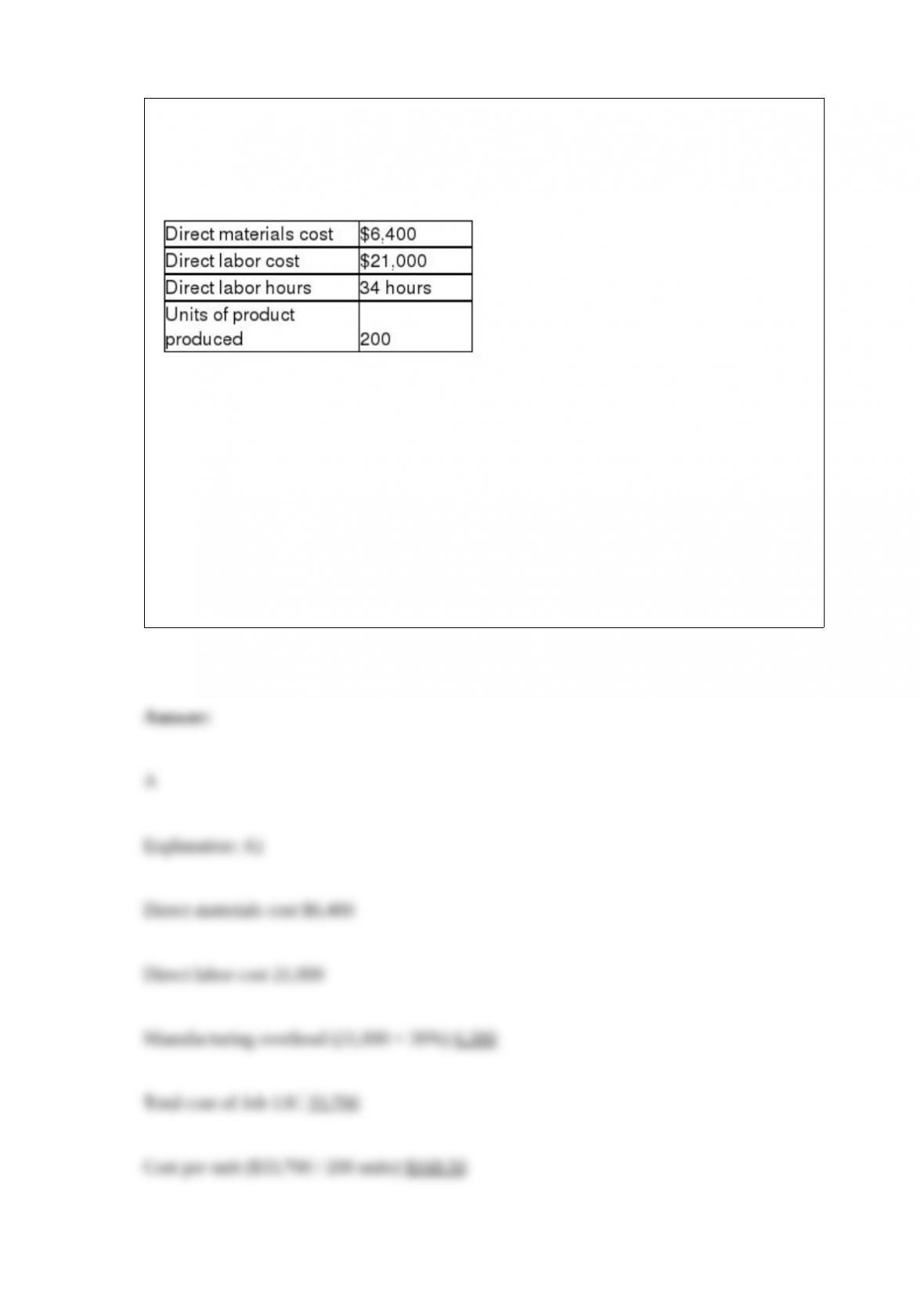

Jordan Manufacturing uses a predetermined overhead allocation rate based on a

percentage of direct labor cost. At the beginning of the year, it estimated the

manufacturing overhead rate to be 30% times the direct labor cost. In the month of

June, Jordan completed Job 13C, and its details are as follows:

What is the cost per unit of finished product of Job 13C? (Round your answer to the

nearest cent.)

A) $168.50

B) $146.60

C) $137.05

D) $136.50

Which of the following is a prime cost and a conversion cost?

A) manufacturing overhead

B) direct materials

C) direct labor

D) selling expenses

AAA Metal Bearings produces two sizes of metal bearings (sold by the crate)-standard

and heavy. The standard bearings require $200 of direct materials per unit (per crate),

and the heavy bearings require $245 of direct materials per unit. The operation is

mechanized, and there is no direct labor. Previously AAA used a single plantwide

allocation rate for manufacturing overhead, which was $1.55 per machine hour. Based

on the single rate, gross profit was as follows:

Per unit Standard Heavy

Direct materials cost $200.00 $245.00

Manufacturing overhead cost 124.00 93.00

Total manufacturing cost $324.00 $338.00

Sales price per unit 350.00 370.00

Gross profit per unit $26.00 $32.00

Although the data showed that the heavy bearings were more profitable than the

standard bearings, the plant manager knew that the heavy bearings required much more

processing in the metal fabrication phase than the standard bearings, and that this factor

was not adequately reflected in the single plantwide allocation rate. He suspected that it

was distorting the profit data. He suggested adopting an activity-based costing

approach.

Working together, the engineers and accountants identified the following three

manufacturing activities and broke down the annual overhead costs as shown below:

Activities: Estimated Cost

Metal fabrication $420,000

Machine processing 152,000

Packaging 17,000

Total overhead cost $589,000

Engineers believed that metal fabrication costs should be allocated by weight and

estimated that the plant processed 12,000 kilos of metal per year. Machine processing

costs were correlated to machine hours, and the engineers estimated a total of 380,000

machine hours for the year. Packaging costs were the same for both types of products,

and so they could be allocated simply by the number of units produced. The production

plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be

produced during the year. Additional data on a per unit basis was as given below:

Standard Heavy

Kilos per unit 2.00 4.00

Machine hours per unit 80.00 60.00

Using the data above, calculate the predetermined overhead allocation rates using

activity-based costing. Then, following the ABC methodology, calculate the production

cost and gross profit for one unit of standard bearings. (Round your intermediate

calculations to two decimal places.)

Which of the following would be considered a product cost for a manufacturing

company?

A) depreciation on delivery vehicles

B) depreciation on administrative building furniture and fixtures

C) depreciation on manufacturing equipment

D) depreciation on the accounting department’s computer equipment

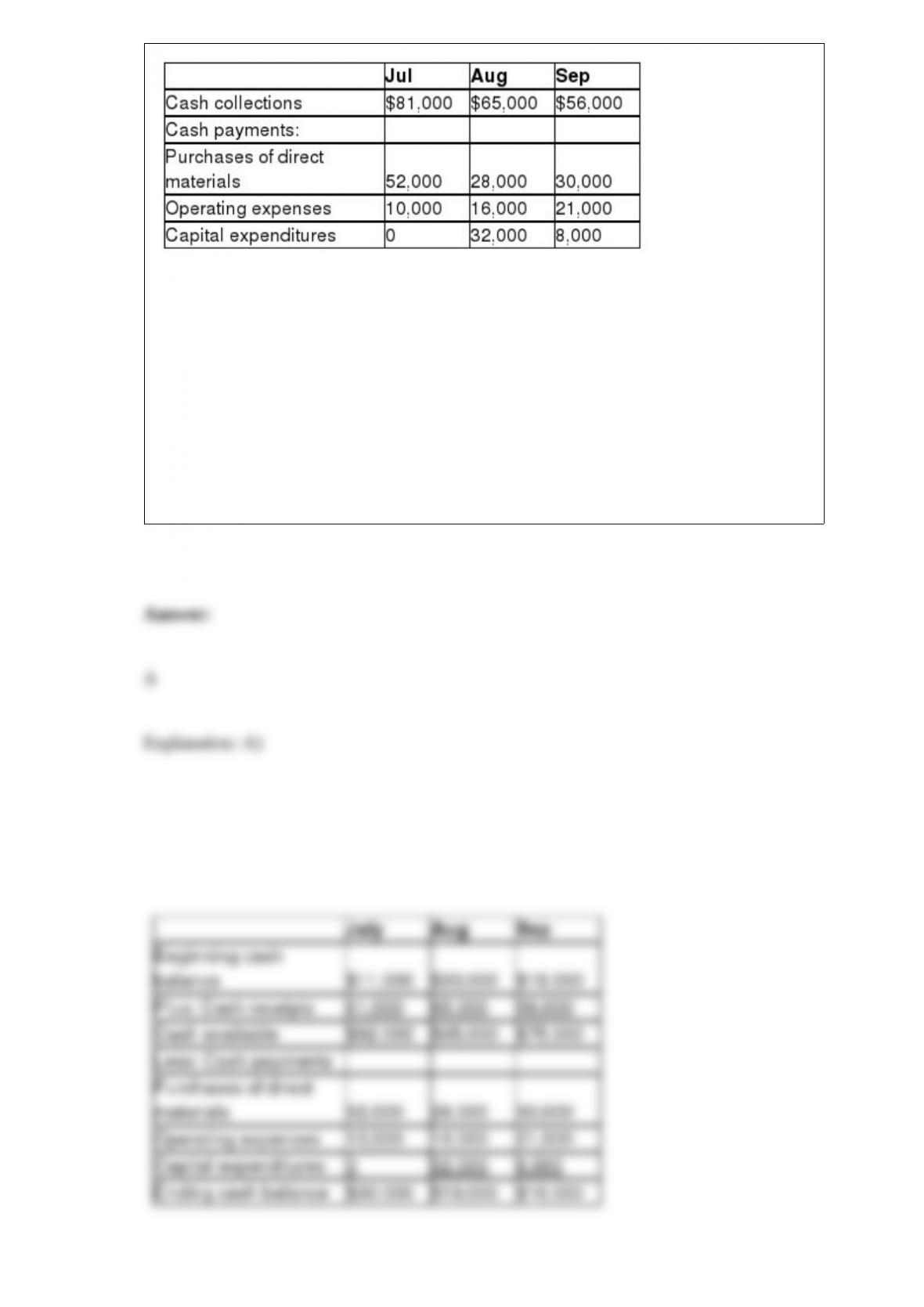

Iowa Supply, Inc. provides the following data taken from its third quarter budget:

The cash balance on June 30 is projected to be $11,000. Based on the above data,

calculate the cash balance the company is projected to have at the end of September.

A) $16,000

B) $19,000

C) $75,000

D) $59,000

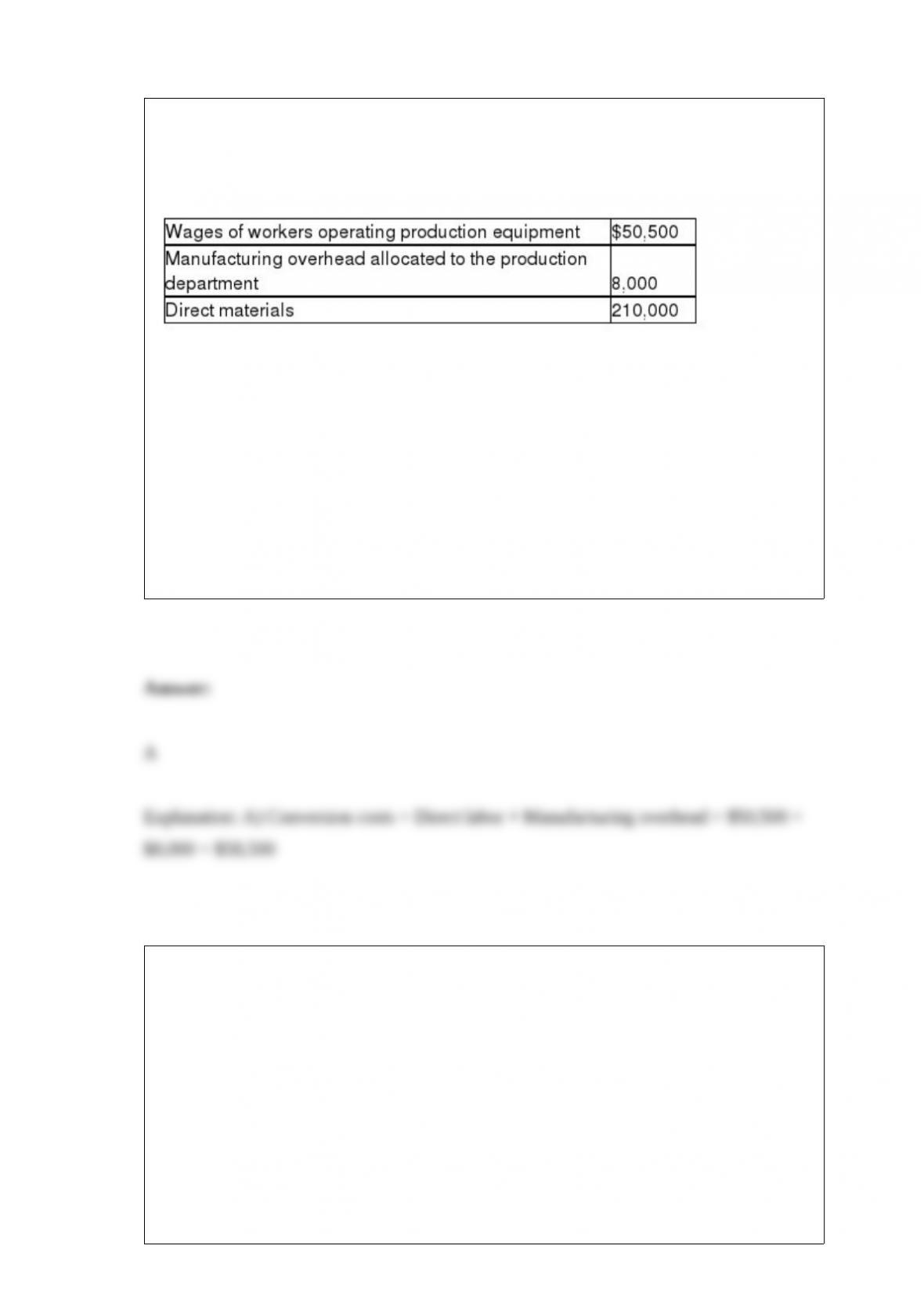

Ellie’s Candies, Inc. produces gummy bears. The company purchases raw materials,

stores them in a warehouse, and then runs them through two processes: production and

packaging. During September, the production process incurred the following costs in

processing 20,000 gummy bears:

Use the FIFO method to compute the September conversion costs in the Production

Department.

A) $58,500

B) $268,500

C) $50,500

D) $8,000

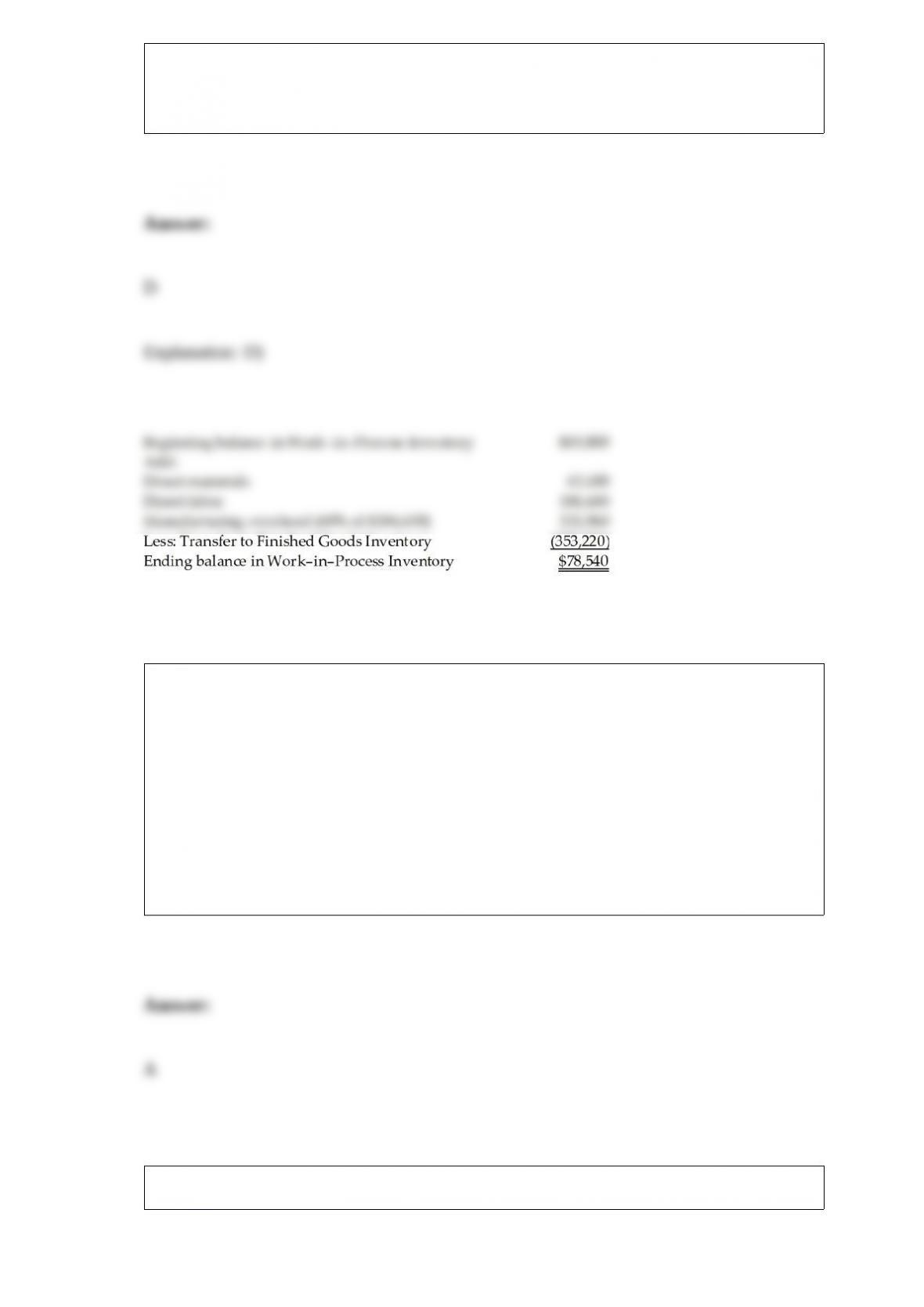

On January 1, Jackson, Inc.’s Work-in-Process Inventory account showed a balance of

$65,800. During the year, materials requisitioned for use in production amounted to

$70,900, of which $67,400 represented direct materials. Factory wages for the period

were $209,000 of which $186,600 were for direct labor. Manufacturing overhead is

allocated on the basis of 60% of direct labor cost. Actual overhead was $116,340. Jobs

costing $353,220 were completed during the year. The December 31 balance in

Work-in-Process Inventory is ________.

A) $65,800

B) $319,800

C) $431,760

D) $78,540

Following GAAP, the income statement issued to investors and creditors must

________.

A) be prepared in the traditional format

B) be prepared using variable costing

C) be prepared in the contribution margin format

D) show the value of contribution margin

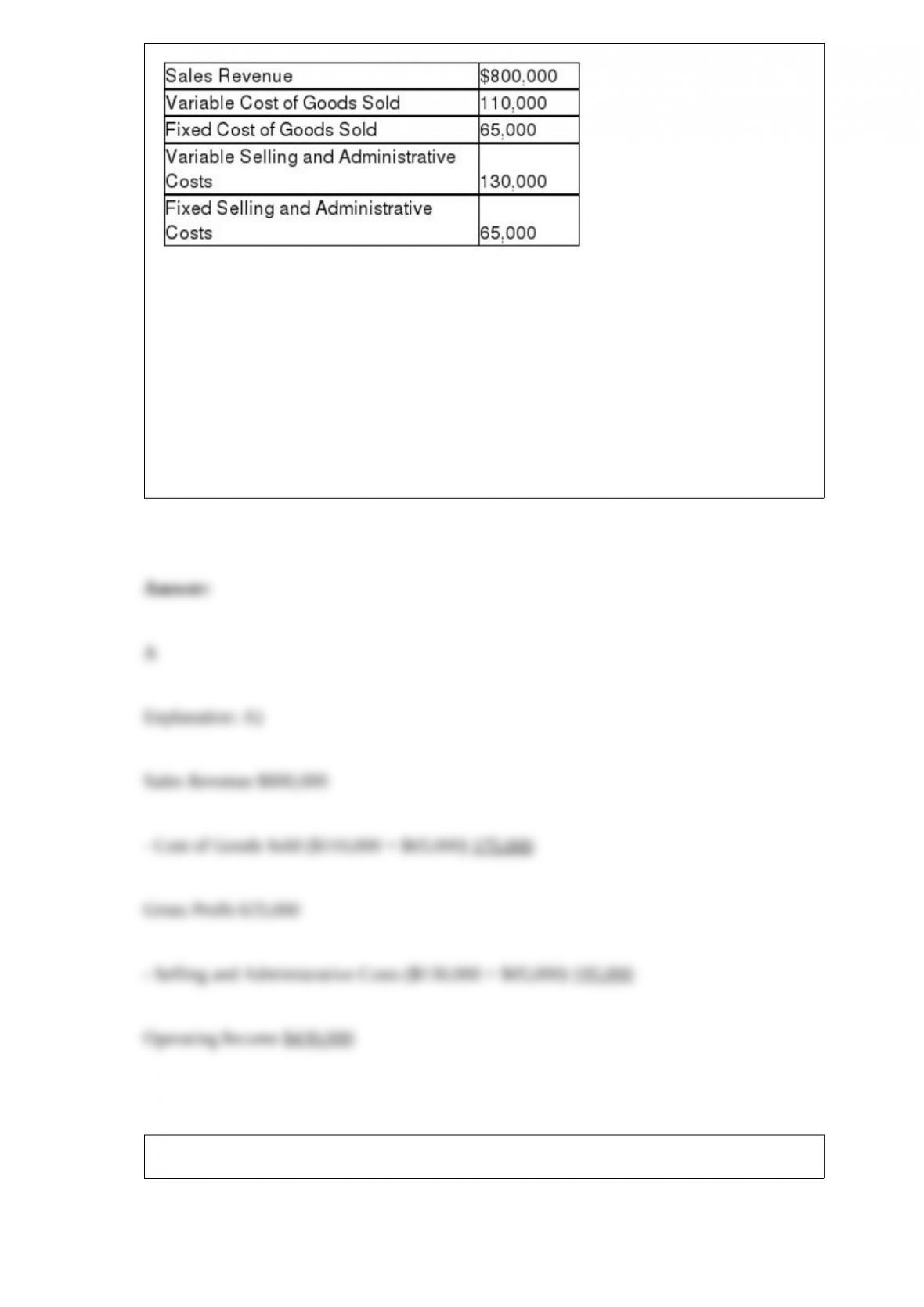

Dentofax, Inc. reports the following information for August:

Calculate the operating income for August using absorption costing.

A) $430,000

B) $240,000

C) $995,000

D) $370,000

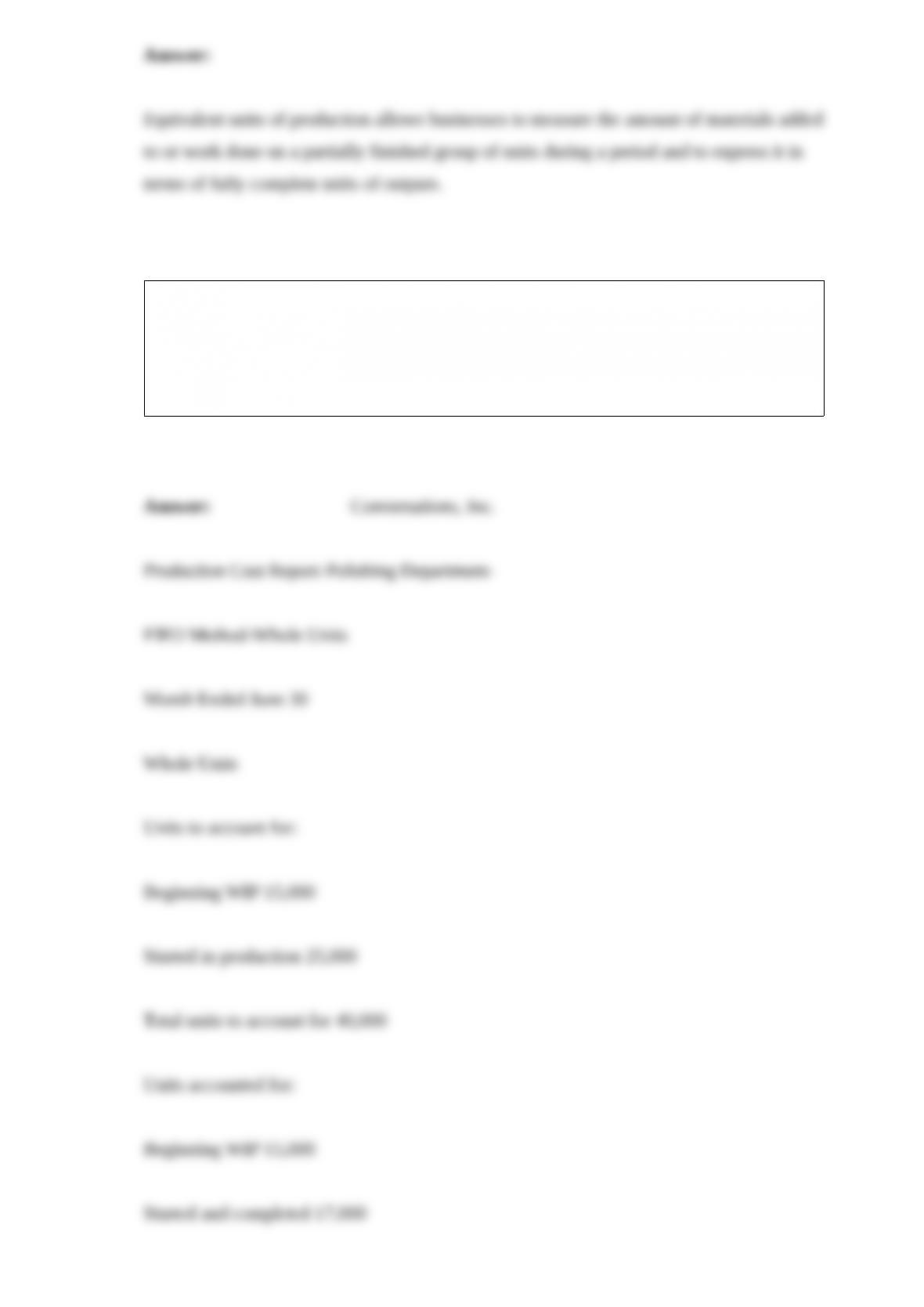

What does the concept of equivalent units of production allow businesses to measure?

The Polishing Department of Conversations, Inc. had 15,000 units in process on June 1

and received 25,000 units from the Machining Department. During the month, it

completed 32,000 units and transferred them to the Packaging Department. Prepare the

production cost report for the Polishing Department for the whole units for the month of

June. (Use the first-in, first-out method.)

Egerton, Inc. has two processes-Coloring Department and Mixing Department. Egerton

sold 350 gallons on account at $110 per gallon. The total cost of processing was

$385,000 for 5,500 gallons of paint. Throughout the year, the company used a

predetermined overhead allocation rate to allocate $75,000 and $65,000 of indirect

costs to the Coloring Department and Mixing Department, respectively. The actual

overhead cost incurred amounted to $150,000 at the end of the year. Record the

necessary journal entries for the sale of goods and for adjustment of over- or

underallocated manufacturing overhead at the end of the year.

Managers can use activity-based management to make what two kinds of decisions?