A trader who has a __________ position in gold futures wants the price of gold to

__________ in the future.

A. long; decrease

B. short; decrease

C. short; stay the same

D. short; increase

E. long; stay the same

Which of the following is not true?

A. Holding other things constant, the duration of a bond increases with time to maturity.

B. Given time to maturity, the duration of a zero-coupon decreases with yield to

maturity.

C. Given time to maturity and yield to maturity, the duration of a bond is higher when

the coupon rate is lower.

D. Duration is a better measure of price sensitivity to interest-rate changes than is time

to maturity.

E. All of the options are correct.

Which of the following is not required under the CFA Institute Standards of

Professional Conduct?

A. Knowledge of all applicable laws, rules, and regulations

B. Disclosure of all personal investments, whether or not they may conflict with a

client’s investments

C. Disclosure of all conflicts to clients and prospects

D. Reasonable inquiry into a client’s financial situation

E. All of the options are required under the CFA Institute standards.

If a firm’s beta was calculated as 0.6 in a regression equation, a commonly-used

adjustment technique would provide an adjusted beta of

A. less than 0.6 but greater than zero.

B. between 0.6 and 1.0.

C. between 1.0 and 1.6.

D. greater than 1.6.

E. zero or less.

Mature Products Corporation produces goods that are very mature in their product life

cycles. Mature Products Corporation is expected to pay a dividend in year 1 of $2.00, a

dividend of $1.50 in year 2, and a dividend

of $1.00 in year 3. After year 3, dividends are expected to decline at a rate of 1% per

year. An appropriate required rate of return for the stock is 10%. The stock should be

worth

A. $9.00.

B. $10.57.

C. $20.00.

D. $22.22.

Delta is defined as

A. the change in the value of an option for a dollar change in the price of the underlying

asset.

B. the change in the value of the underlying asset for a dollar change in the call price.

C. the percentage change in the value of an option for a 1% change in the value of the

underlying asset.

D. the change in the volatility of the underlying stock price.

E. None of the options are correct.

To exploit an expected increase in interest rates, an investor would most likely

A. sell Treasury bond futures.

B. take a long position in wheat futures.

C. buy S&P 500 Index futures.

D. take a long position in Treasury bond futures.

E. None of the options are correct.

Which of the following statement(s) is(are) true regarding the selection of a portfolio

from those that lie on the

capital allocation line?

I) Less risk-averse investors will invest more in the risk-free security and less in the

optimal risky portfolio than

more risk-averse investors.

II) More risk-averse investors will invest less in the optimal risky portfolio and more in

the risk-free security than

less risk-averse investors.

III) Investors choose the portfolio that maximizes their expected utility.

A. I only

B. II only

C. III only

D. I and III

E. II and III

If you believe in the reversal effect, you should

A. buy bonds in this period if you held stocks in the last period.

B. buy stocks in this period if you held bonds in the last period.

C. buy stocks this period that performed poorly last period.

D. go short.

E. buy stocks this period that performed poorly last period and go short.

You write one AT&T February 50 put for a premium of $5. Ignoring transactions costs,

what is the break-even price of this position?

A. $50

B. $55

C.$45

D. $40

Which of the following statements regarding the Dow Jones Industrial Average (DJIA)

is false?

A. The DJIA is not very representative of the market as a whole.

B. The DJIA consists of 30 blue chip stocks.

C. The DJIA is affected equally by changes in low- and high-priced stocks.

D. The DJIA divisor needs to be adjusted for stock splits.

E. The value of the DJIA is much higher than individual stock prices.

The ultimate stock index in the U.S. is the

A. Wilshire 5000.

B. DJIA.

C. S&P 500.

D. Russell 2000.

A firm has a P/E ratio of 12, an ROE of 13%, and a market-to-book value of

A. 0.64.

B. 0.92.

C. 1.08.

D. 1.56.

You are considering investing $1,000 in a T-bill that pays 0.05 and a risky portfolio, P,

constructed with two

risky securities, X and Y. The weights of X and Y in P are 0.60 and 0.40, respectively. X

has an expected rate

of return of 0.14 and variance of 0.01, and Y has an expected rate of return of 0.10 and a

variance of 0.0081.

What would be the dollar value of your positions in X, Y, and the T-bills, respectively, if

you decide to hold a

portfolio that has an expected outcome of $1,120?

A. $568; $378; $54

B. $568; $54; $378

C. $378; $54; $568

D. $108; $514; $378

E. Cannot be determined.

Other things equal, the price of a stock put option is positively correlated with which of

the following factors?

A. The stock price

B. The time to expiration

C. The stock volatility

D. The exercise price

E. The time to expiration, stock volatility, and exercise price

Studies of style analysis have found that ________ of fund returns can be explained by

asset allocation alone.

A. between 50% and 70%

B. less than 10%

C. between 40 and 50%

D. between 75% and 90%

E. over 90%

To determine the optimal risky portfolio in the Treynor-Black model, macroeconomic

forecasts are used for the

_________, and composite forecasts are used for the __________.

A.passive index portfolio; active portfolio

B. active portfolio, passive index portfolio

C. expected return; standard deviation

D. expected return ; beta coefficient

E. alpha coefficient; beta coefficient

A covered call position is

A. the simultaneous purchase of the call and the underlying asset.

B. the purchase of a share of stock with a simultaneous sale of a put on that stock.

C. the short sale of a share of stock with a simultaneous sale of a call on that stock.

D.the purchase of a share of stock with a simultaneous sale of a call on that stock.

E. the simultaneous purchase of a call and sale of a put on the same stock.

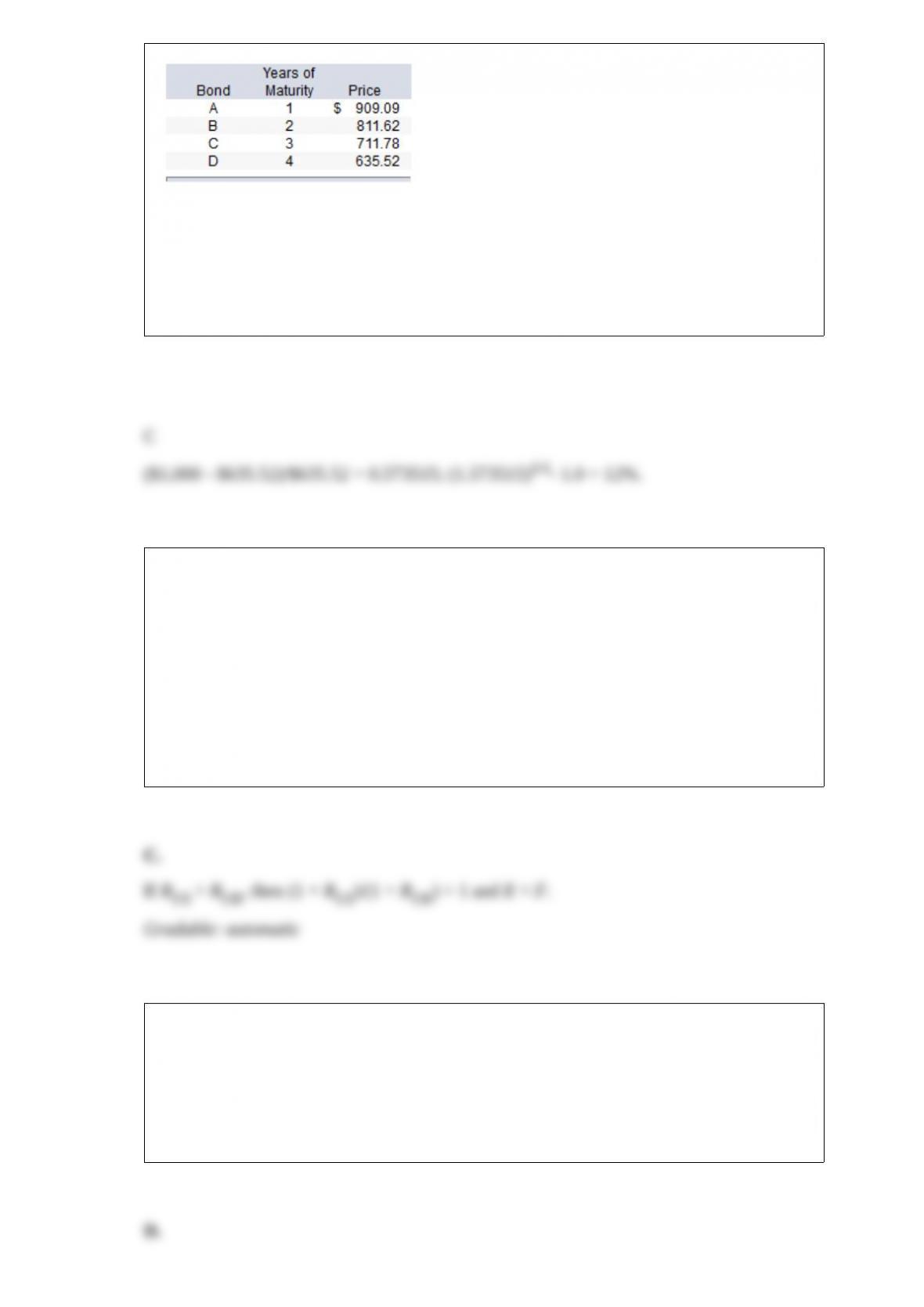

Consider the following $1,000-par-value zero-coupon bonds:

The yield to maturity on bond D is

A. 10%.

B. 11%.

C. 12%.

D. 14%.

E. None of the options are correct.

Let RUS be the annual risk-free rate in the United States, RUK be the risk-free rate in the

United Kingdom, F be the futures price of $/BP for a 1-year contract, and E the spot

exchange rate of $/BP. Which one of the following is true?

A. If RUS > RUK, then E > F.

B. If RUS < RUK, then E < F.

C. If RUS > RUK, then E < F.

D. If RUS < RUK, then F = E.

E. There is no consistent relationship that can be predicted.

Foreign currency futures contracts are actively traded on the

A. euro.

B. British pound.

C. drachma.

D. euro and British pound.

E. All of the options are correct.

Unsecured bonds are called

A. junk bonds.

B. debentures.

C. indentures.

D. subordinated debentures.

E. either debentures or subordinated debentures. Debentures are unsecured bonds.

Suppose the 1-year risk-free rate of return in the U.S. is 4%, and the 1-year risk-free

rate of return in Britain is 7%. The current exchange rate is 1 pound = U.S. $1.65. A

1-year future exchange rate of __________ for the pound would make a U.S. investor

indifferent between investing in the U.S. security and investing in the British security.

A. 1.6037

B. 2.0411

C. 1.7500

D. 2.3369

Which of the following two bonds is more price sensitive to changes in interest rates?

1) A par value bond, X, with a 5-year year to maturity and a 10% coupon rate.

2) A zero-coupon bond, Y, with a 5-year year to maturity and a 10% yield to maturity.

A. Bond X because of the higher yield to maturity

B. Bond X because of the longer time to maturity

C. Bond Y because of the longer duration

D. Both have the same sensitivity because both have the same yield to maturity.

E. None of the options are correct.

In 2016, ____________ was the most significant real asset of U.S. households in terms

of total value.

A. consumer durables

B. automobiles

C. real estate

D. mutual fund shares

E. bank loans

Financial assets

A. directly contribute to the country’s productive capacity.

B. indirectly contribute to the country’s productive capacity.

C. contribute to the country’s productive capacity, both directly and indirectly.

D. do not contribute to the country’s productive capacity, either directly or indirectly.

E. are of no value to anyone.

Patty O Furniture purchased 100 shares of Green Isle mutual fund at a net asset value of

$42 per share. During the year, Patty received dividend income distributions of $2.00

per share and capital gains distributions of $4.30 per share. At the end of the year, the

shares had a net asset value of $40 per share. What was Patty’s rate of return on this

investment?

A. 5.43%

B. 10.24%

C. 7.19%

D. 12.44%

E. 9.18%

In the APT model, what is the nonsystematic standard deviation of an equally-weighted

portfolio that has an

average value of σ(ei ) equal to 20% and 40 securities?

A. 12.5%

B. 625%

C. 0.5%

D. 3.54%

E. 3.16%

Assume that stock market returns do follow a single-index structure. An investment

fund analyzes 500 stocks in order to construct a mean-variance efficient portfolio

constrained by 500 investments. They will need to calculate ________ estimates of

firm-specific variances and ________ estimate/estimates for the variance of the

macroeconomic factor.

A. 500; 1

B. 500; 500

C. 124,750; 1

D. 124,750; 500

E. 250,000; 500

A fullyfunded pension plan can invest surplus assets in equities provided it reduces the

proportion in equities when the value of the fund drops near the accumulated benefit

obligation. This strategy is referred to as

A. immunization.

B. hedging.

C. diversification.

D. contingent immunization.

E. overfunding.