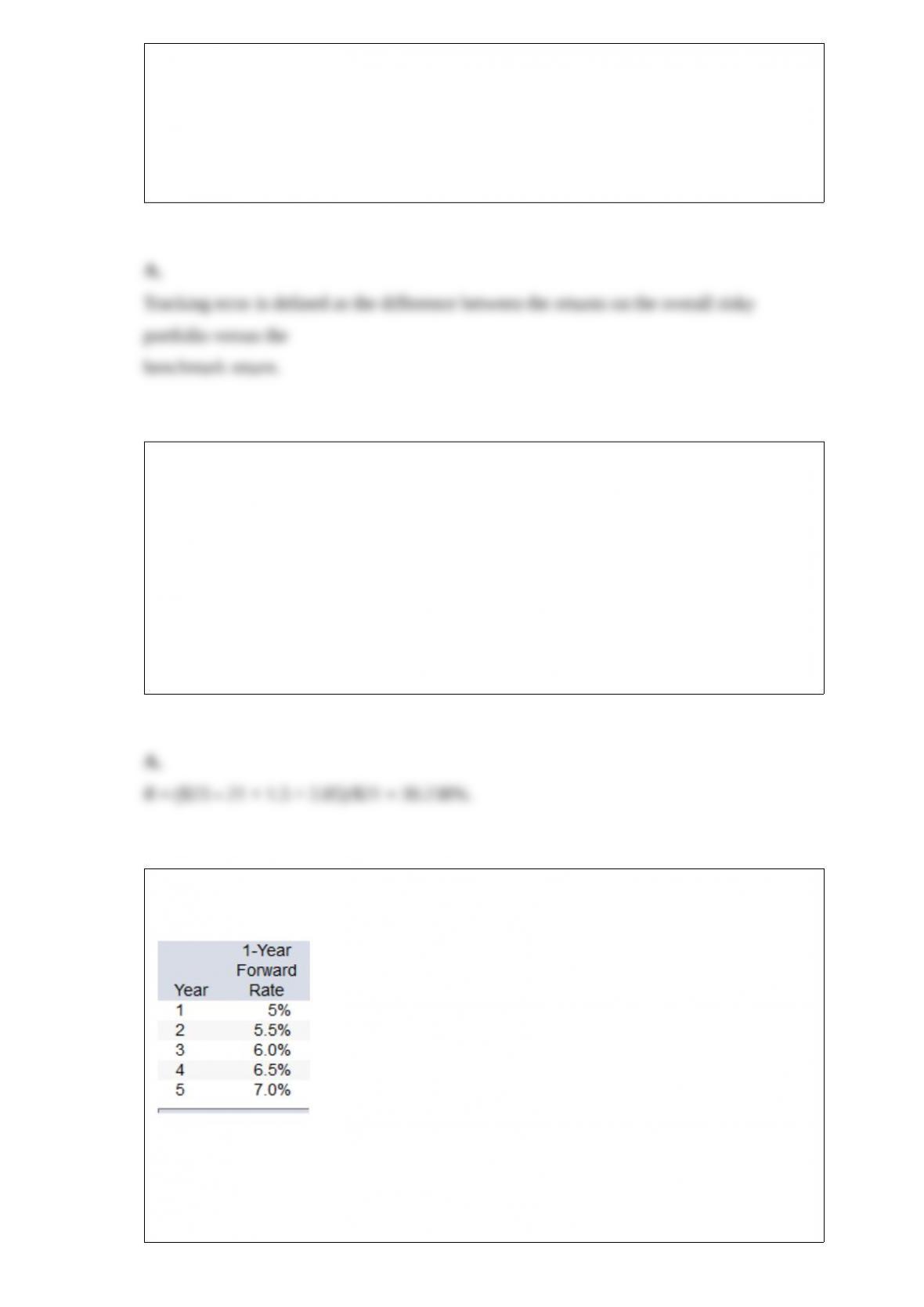

Tracking error is defined as

A.the difference between the returns on the overall risky portfolio versus the benchmark

return.

B. the variance of the return of the benchmark portfolio.

C. the variance of the return difference between the portfolio and the benchmark.

D. the variance of the return of the actively-managed portfolio.

Assume that you purchased 200 shares of Super Performing mutual fund at a net asset

value of $21 per share. During the year, you received dividend income distributions of

$1.50 per share and capital gains distributions of $2.85 per share. At the end of the year,

the shares had a net asset value of $23 per share. What was your rate of return on this

investment?

A. 30.24%

B. 25.37%

C. 27.19%

D. 22.44%

E. 29.18%

Calculate the price at the beginning of year 1 of an 8% annual coupon bond with face

value $1,000 and 5 years to maturity.

A. $1,105.47

B. $1,131.91

C. $1,084.25

D. $1,150.01

E. $719.75

You purchased 100 shares of common stock on margin for $35 per share. The initial

margin is 50%, and the stock pays no dividend. What would your rate of return be if

you sell the stock at $42 per share? Ignore interest on margin.

A. 28%

B. 33%

C. 14%

D. 40%

E. 24%

An upward sloping yield curve is a(n) _______ yield curve.

A. normal

B. humped

C. inverted

D. flat

E. None of the options are correct.

The following data are available relating to the performance of Sooner Stock Fund and

the market portfolio:

The risk-free return during the sample period was 3%.

What is the Treynor measure of performance evaluation for Sooner Stock Fund?

A. 1.33%

B. 4.00%

C. 8.67%

D. 9.44%

E. 37.14%

The value of a derivative security

A. depends on the value of the related security.

B. is unable to be calculated.

C. is unrelated to the value of the related security.

D. has been enhanced due to the recent misuse and negative publicity regarding these

instruments.

E. is worthless today.

Covariances between security returns tend to be

A. positive because of SEC regulations.

B. positive because of Exchange regulations.

C. positive because of economic forces that affect many firms.

D. negative because of SEC regulations.

E. negative because of economic forces that affect many firms.

Hedge funds ______ engage in market timing ______ take extensive derivative

positions.

A. cannot; and cannot

B. cannot; but can

C. can; and can

D. can; but cannot

E. None of the options are correct.

Which of the following would best explain a situation where the ratio of net

income/total equity of a firm is higher than the industry average, while the ratio of net

income/total assets is lower than the industry average?

A. The firm’s net profit margin is higher than the industry average.

B. The firm’s asset turnover is higher than the industry average.

C. The firm’s equity multiplier must be lower than the industry average.

D. The firm’s debt ratio is higher than the industry averagE.

E. None of the options are correct.

Assume that at retirement you have accumulated $825,000 in a variable annuity

contract. The assumed investment return is 5.5%, and your life expectancy is 18 years.

If the first year’s actual investment return is 7%, what is the starting benefit payment?

A. $30,000.00

B. $74,401.95

C. $51,481.38

D. $52,452.73

E. The answer cannot be determined from the information provided.

In 2016, ____________ was(were) the least significant real asset(s) of U.S.

nonfinancial businesses in terms of total value.

A. equipment and software

B. inventory

C. real estate

D. trade credit

E. marketable securities

A preferred stock will pay a dividend of $3.50 in the upcoming year and every year

thereafter; i.e., dividends are not expected to grow. You require a return of 11% on this

stock. Use the constant growth DDM to calculate the intrinsic value of this preferred

stock.

A. $0.39

B. $0.56

C. $31.82

D. $56.25

In terms of total value, the most significant liability(ies) of U.S. nonfinancial businesses

in 2016 was(were)

A. bank loans.

B. bonds and mortgages.

C. trade debt.

D. other loans.

E. marketable securities.

Rosenberg and Guy found that __________ helped to predict a firm’s beta.

A. the firm’s financial characteristics

B. the firm’s industry group

C. firm size

D. the firm’s financial characteristics and the firm’s industry group

E. All of the options are correct.

Consider the single-index model. The alpha of a stock is 0%. The return on the market

index is 10%. The risk-free rate of return is 5%. The stock earns a return that exceeds

the risk-free rate by 5%, and there are no firm-specific events affecting the stock

performance. The β of the stock is

A. 0.67.

B. 0.75.

C. 1.0.

D. 1.33.

E. 1.50.

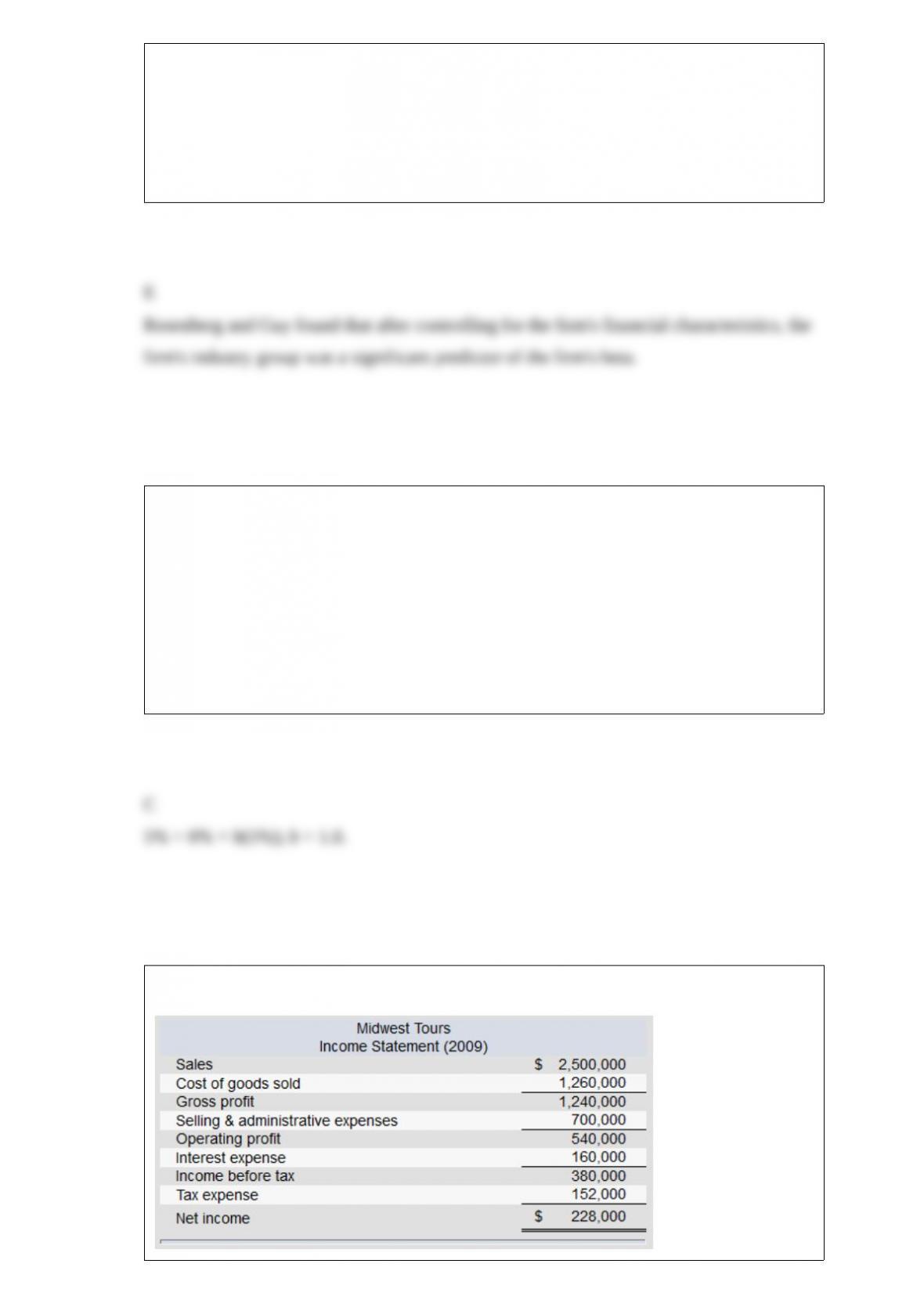

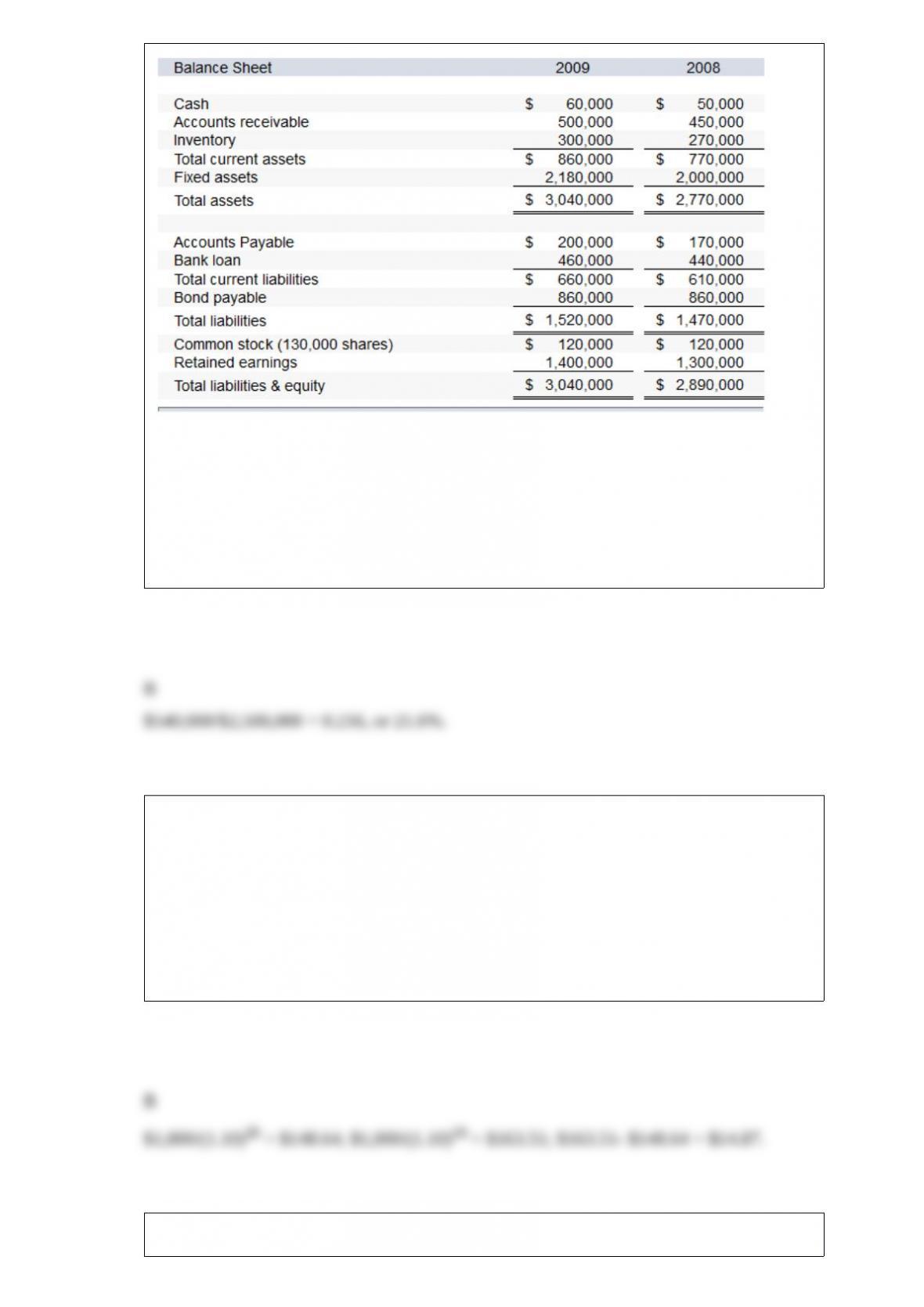

The financial statements of Midwest Tours are given below.

Note: The common shares are trading in the stock market for $36 each.

Refer to the financial statements of Midwest Tours. The firm’s return on sales ratio for

2009 is

A. 20.2%.

B. 21.6%.

C. 22.4%.

D. 18.0%.

Consider a $1,000-par-value 20-year zero-coupon bond issued at a yield to maturity of

10%. If you buy that bond when it is issued and continue to hold the bond as yields

decline to 9%, the imputed interest income for the first year of that bond is

A. zero.

B. $14.87.

C. $45.85.

D. $7.44.

E. None of the options are correct.

A portfolio consists of 800 shares of stock and 100 calls on that stock. If the hedge ratio

for the call is 0.5, what would be the dollar change in the value of the portfolio in

response to a $1 decline in the stock price?

A. +$700

B. −$850

C. −$580

D. −$520

A mutual fund had year-end assets of $465,000,000 and liabilities of $37,000,000. If the

fund NAV was $56.12, how many shares must have been held in the fund?

A. 4,300,000

B. 6,488,372

C. 8,601,709

D. 7,626,515

E. None of these options are correct.

An American call option allows the buyer to

A. sell the underlying asset at the exercise price on or before the expiration date.

B. buy the underlying asset at the exercise price on or before the expiration date.

C. sell the option in the open market prior to expiration.

D. sell the underlying asset at the exercise price on or before the expiration date and sell

the option in the open market prior to expiration.

E.buy the underlying asset at the exercise price on or before the expiration date and sell

the option in the open market prior to expiration.

The index model for stock A has been estimated with the following result:

RA = 0.01 + 0.9RM + eA.

If σM = 0.25 and R2

A = 0.25, the standard deviation of return of stock A is

A. 0.2025.

B. 0.2500.

C. 0.4500.

D. 0.8100.

You sold JCP stock short at $80 per share. Your losses could be minimized by placing a

A. limit-sell order.

B. limit-buy order.

C. stop-buy order.

D. day-order.

E. None of the options are correct.

Genny Webb is 27 years old and has accumulated $7,500 in her selfdirected defined

contribution pension plan. Each year she contributes $2,000 to the plan, and her

employer contributes an equal amount. Genny thinks she will retire at age 63 and

figures she will live to age 90. The plan allows for two types of investments. One offers

a 3% riskfree real rate of return. The other offers an expected return of 12% and has a

standard deviation of 39%. Genny now has 20% of her money in the riskfree

investment and 80% in the risky investment. She plans to continue saving at the same

rate and keep the same proportions invested in each of the investments. Her salary will

grow at the same rate as inflation. Of the total amount of new funds that will be

invested by Genny and by her employer on her behalf, how much will Genny put into

the safe account each year; how much into the risky account?

A. $1,500; $2,500

B. $1,200; $1,800

C. $800; $3,200

D. $1,250; $2,750

E. $1,400; $1,600

At expiration, the time value of an at-the-money put option is always

A. equal to zero.

B. equal to the stock price minus the exercise price.

C. negative.

D. positive.

10 and 65% in a T-bill that pays 4%. His portfolio’s expected return and standard

deviation are __________

and __________, respectively.

A. 0.089; 0.111

B. 0.087; 0.063

C. 0.096; 0.126

D. 0.087; 0.144

The risk profile of hedge funds ______, making performance evaluation ______.

A. can shift rapidly and substantially; challenging

B. can shift rapidly and substantially; straightforward

C. is stable; challenging

D. is stable; straightforward

E. None of the options are correct.

Hedge funds traditionally have ______ than 100 investors and ______ to the general

public.

A. more; advertise

B. more; do not advertise

C. less; advertise

D. less; do not advertise

Before expiration, the time value of a call option is equal to

A. zero.

B.the actual call price minus the intrinsic value of the call.

C. the intrinsic value of the call.

D. the actual call price plus the intrinsic value of the call.

The law of one price posits that ability to arbitrage would force prices of identical

goods to trade at equal prices. However, empirical evidence suggests that __________

are often mispriced.

A. Siamese twin companies

B. equity carve outs

C. closed end funds

D. Siamese twin companies and closed end funds

E. All of the options are correct.

According to the Capital Asset Pricing Model (CAPM), which one of the following

statements is false?

A. The expected rate of return on a security increases in direct proportion to a decrease

in the risk-free rate.

B. The expected rate of return on a security increases as its beta increases.

C. A fairly priced security has an alpha of zero.

D. In equilibrium, all securities lie on the security market line.

E. All of the statements are true.

Analysts may use regression analysis to estimate the index model for a stock. When

doing so, the intercept of the regression line is an estimate of

A. the α of the asset.

B. the β of the asset.

C. the σ of the asset.

D. the δ of the asset.

A $1 decrease in a call option’s exercise price would result in a(n) __________ in the

call option’s value of __________ one dollar.

A. increase; more than

B. decrease; more than

C. decrease; less than

D. increase; less than

E. increase; exactly