A coupon bond that pays interest of $40 semi-annually has a par value of $1,000,

matures in four years, and is selling today at a $36 discount from par value. The yield to

maturity on this bond is

A. 8.69%.

B. 9.09%.

C. 10.43%.

D. 9.76%.

E. None of the options are correct.

The terms of futures contracts, such as the quality and quantity of the commodity and

the delivery date, are

A. specified by the buyers and sellers.

B. specified only by the buyers.

C. specified by the futures exchanges.

D. specified by brokers and dealers.

E. None of the options are correct.

Assume that stock market returns do not resemble a single-index structure. An

investment fund analyzes 40 stocks in order to construct a mean-variance efficient

portfolio constrained by 40 investments. They will need to calculate ____________

covariances.

A. 45

B. 780

C. 4,950

D. 10,000

Derivative securities are also called contingent claims because

A. their owners may choose whether or not to exercise them.

B. a large contingent of investors holds them.

C. the writers may choose whether or not to exercise them.

D.their payoffs depend on the prices of other assets.

E. contingency management is used in adding them to portfolios.

A Treasury bond due in one year has a yield of 4.3%; a Treasury bond due in five years

has a yield of 5.06%. A bond issued by Boeing due in five years has a yield of 7.63%; a

bond issued by Caterpillar due in one year has a yield of 7.16%. The default risk

premiums on the bonds issued by Boeing and Caterpillar, respectively, are

A. 3.33% and 2.10%.

B. 2.57% and 2.86%.

C. 1.2% and 1.0%.

D. 0.76% and 0.47%.

E. None of the options are correct.

Which one of the following stock index futures has a multiplier of $10 times the index

value?

A. Russell 2000

B. Dow Jones Industrial Average

C. Nikkei

D. DAX-30

E. NASDAQ 100

The maximum loss a buyer of a stock put option can suffer is equal to

A. the striking price minus the stock price.

B. the stock price minus the value of the call.

C.the put premium.

D. the stock price.

E. None of the options are correct.

Which of the following are used by technical analysts to determine proper stock prices?

I) Trendlines

II) Earnings

III) Dividend prospects

IV) Expectations of future interest rates

V) Resistance levels

A. I and V

B. I, II, and III

C. II, III, and IV

D. II, IV, and V

E. All of the items are used by fundamental analysts.

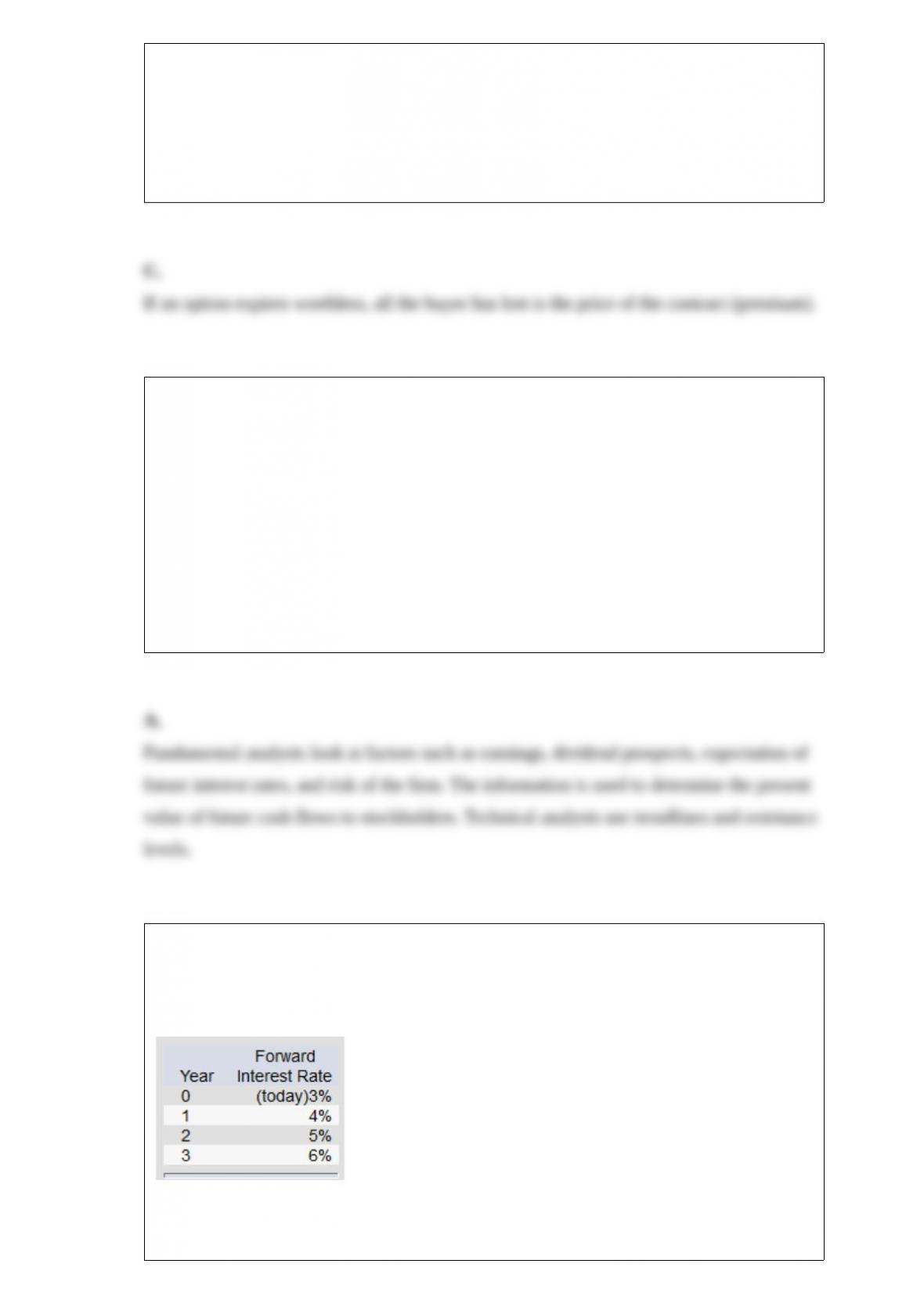

If you have just purchased a 4-year zero-coupon bond, what would be the expected rate

of return on your investment in the first year if the implied forward rates stay the same?

(Par value of the bond = $1,000.) Suppose that all investors expect that interest rates for

the 4 years will be as follows:

A. 5%

B. 3%

C. 9%

D. 10%

E. None of the options are correct.

You purchase one June 70 put contract for a put premium of $4. What is the maximum

profit that you could gain from this strategy?

A. $7,000

B. $400

C. $7,400

D.$6,600

E. None of the options are correct.

To improve future analyst forecasts using the statistical properties of past forecasts, a

regression model can

be fitted to past forecasts. The intercept of the regression is a __________ coefficient,

and the regression beta

represents a __________ coefficient.

A. bias; precision

B.bias; bias

C. precision; precision

D. precision; bias

Assume that stock market returns do follow a single-index structure. An investment

fund analyzes 175 stocks in order to construct a mean-variance efficient portfolio

constrained by 175 investments. They will need to calculate ________ estimates of

expected returns and ________ estimates of sensitivity coefficients to the

macroeconomic factor.

A. 175; 15,225

B. 175; 175

C. 15,225; 175

D. 15,225; 15,225

The buyer of a futures contract is said to have a __________ position, and the seller of

a futures contract is said to have a __________ position in futures.

A. long; short

B. long; long

C. short; short

D. short; long

E. margined; long

If the Federal Reserve lowers the Fed Funds rate, ceteris paribus, the equilibrium levels

of funds lent will

__________, and the equilibrium level of real interest rates will ___________.

A. increase; increase

B. increase; decrease

C. decrease; increase

D. decrease; decrease

E. reverse direction from their previous trends; reverse direction from their previous

trends

A purchase of a new issue of stock takes place

A. in the secondary market.

B. in the primary market.

C. usually with the assistance of an investment banker.

D. in the secondary and primary markets.

E. in the primary market and usually with the assistance of an investment banker.

Consider two perfectly negatively correlated risky securities, K and L. K has an

expected rate of return of 13%

and a standard deviation of 19%. L has an expected rate of return of 10% and a standard

deviation of 16%.

The weights of K and L in the global minimum variance portfolio are _____ and _____,

respectively.

A. 0.24; 0.76

B. 0.50; 0.50

C. 0.46; 0.54

D. 0.45; 0.55

E. 0.76; 0.24

Assume that stock market returns do follow a single-index structure. An investment

fund analyzes 60 stocks in order to construct a mean-variance efficient portfolio

constrained by 60 investments. They will need to calculate ________ estimates of

expected returns and ________ estimates of sensitivity coefficients to the

macroeconomic factor.

A. 200; 19,900

B. 200; 200

C. 60; 60

D. 19,900; 19.900

E. None of the options are correct.

Pinnacle Fund had year-end assets of $825,000,000 and liabilities of $25,000,000. If

Pinnacle’s NAV was $32.18, how many shares must have been held in the fund?

A. 21,619,346.92

B. 22,930,546.28

C. 24,860,161.59

D. 25,693,645.25

________ specialize in helping companies raise capital by selling securities.

A. Commercial bankers

B. Investment bankers

C. Investment issuers

D. Credit raters

A pension fund that begins with $500,000 earns 15% the first year and 10% the second

year. At the beginning of the second year, the sponsor contributes another $300,000.

The dollar-weighted and time-weighted rates of return, respectively, were

A. 11.7% and 12.5%.

B. 12.1% and 12.5%.

C. 12.5% and 11.7%.

D. 12.5% and 12.1%.

The optimal portfolio on the efficient frontier for a given investor depends on

A. the investor’s degreeofrisk tolerance.

B. the coefficient, A, which is a measure of risk aversion.

C. the investor’s required rate of return.

D. the investor’s degreeofrisk tolerance and the investor’s required rate of return.

E. the investor’s degreeofrisk tolerance and the coefficient, A, which is a measure of

risk aversion.

Suppose the risk-free return is 6%. The beta of a managed portfolio is 1.5, the alpha is

3%, and the average return is 18%. Based on Jensen’s measure of portfolio

performance, you would calculate the return on the market portfolio as

A. 12%.

B. 14%.

C. 15%.

D. 16%.

Immunization is not a strictly passive strategy because

A. it requires choosing an asset portfolio that matches an index.

B. there is likely to be a gap between the values of assets and liabilities in most

portfolios.

C. it requires frequent rebalancing as maturities and interest rates change.

D. durations of assets and liabilities fall at the same rate.

E. None of the options are correct.

Sales Company paid a $1.00 dividend per share last year and is expected to continue to

pay out 40% of earnings as dividends for the foreseeable future. If the firm is expected

to generate a 10% return on equity in the future, and if you require a 12% return on the

stock, the value of the stock is

A. $17.67.

B. $13.00.

C. $16.67.

D. $18.67.

The Jensen portfolio evaluation measure

A. is a measure of return per unit of risk, as measured by standard deviation.

B. is an absolute measure of return over and above that predicted by the CAPM.

C. is a measure of return per unit of risk, as measured by beta.

D. is a measure of return per unit of risk, as measured by standard deviation, and is an

absolute measure of return over and above that predicted by the CAPM.

E. is an absolute measure of return over and above that predicted by the CAPM, and is a

measure of return per unit of risk, as measured by beta.

As diversification increases, the total variance of a portfolio approaches

A. 0.

B. 1.

C. the variance of the market portfolio.

D. infinity.

E. None of the options are correct.

The capital asset pricing model assumes

A. all investors are fully informed.

B. all investors are rational.

C. all investors are mean-variance optimizers.

D. taxes are an important consideration.

E. all investors are fully informed, are rational, and are mean-variance optimizers.

The duration of a 20-year zero-coupon bond is

A. equal to 20.

B. larger than 20.

C. smaller than 20.

D. equal to that of a 20-year 10% coupon bond.

One reason swaps are desirable is that

A. they are free of credit risk.

B. they have no transactions costs.

C. they increase interest rate volatility.

D. they increase interest rate risk.

E. they offer participants easy ways to restructure their balance sheets.

Which one of the following variables influences the value of put options?

I) Level of interest rates

II) Time to expiration of the option

III) Dividend yield of underlying stock

IV) Stock price volatility

A. I and IV only

B. II and III only

C. I, II, and IV only

D. I, II, III, and IV

E. I, II, and III only