Which type of fund generally has the lowest average expense ratio?

A. actively managed bond funds

B. hedge funds

C. indexed funds

D. actively managed international funds

LIBOR is a key reference rate in the money markets. Many ______ of dollars of loans

and derivative assets are tied to it.

A. thousands

B. millions

C. billions

D. trillions

A portfolio generates an annual return of 16%, a beta of 1.2, and a standard deviation of

19%. The market index return is 12% and has a standard deviation of 16%. What is the

Sharpe ratio of the portfolio if the risk-free rate is 6%?

A. .4757

B. .5263

C. .6842

D. .7252

The financial statements of Flathead Lake Manufacturing Company are shown below.

Note: The common shares are trading in the stock market for $15 per share.

Refer to the financial statements of Flathead Lake Manufacturing Company. The firm’s

total asset turnover for 2015 is _________. (Please keep in mind that when a ratio

involves both income statement and balance sheet numbers, the balance sheet numbers

for the beginning and end of the year must be averaged.)

A. 3.56

B. 3.26

C. 3.14

D. 3.02

You are considering purchasing a put option on a stock with a current price of $33. The

exercise price is $35, and the price of the corresponding call option is $2.25. According

to the put-call parity theorem, if the risk-free rate of interest is 4% and there are 90 days

until expiration, the value of the put should be ____________.

A. $2.25

B. $3.91

C. $4.05

D. $5.52

The _________ price is the price at which a dealer is willing to purchase a security.

A. bid

B. ask

C. clearing

D. settlement

Generally speaking, the higher a firm’s ROA, the _________ the dividend payout ratio

and the _________ the firm’s growth rate of earnings.

A. higher; lower

B. higher; higher

C. lower; lower

D. lower; higher

A hedge fund has $150 million in assets at the beginning of the year and 10 million

shares outstanding throughout the year. Throughout the year assets grow at 12%. The

fund charges a 3% management fee on the assets. The fee is imposed on year-end asset

values. What is the end-of-year NAV for the fund?

A. $15

B. $15.60

C. $16.30

D. $17.55

The CAL provided by combinations of 1-month T-bills and a broad index of common

stocks is called the ______.

A. SML

B. CAPM

C. CML

D. total return line

You earn 6% on your corporate bond portfolio this year, and you are in a 25% federal

tax bracket and an 8% state tax bracket. Your after-tax return is _____. (Assume that

federal taxes are not deductible against state taxes and vice versa).

A. 4.5%

B. 4.14%

C. 4.02%

D. 3.12%

In 2013, NYSE Euronext was acquired by _______.

A. DOT

B. ICE

C. BATS

D. It was not acquired.

All major stock markets today are effectively _______________.

A. specialist trading systems

B. electronic trading systems

C. continuous auction markets

D. direct search markets

Which one of the statements about margin requirements on option positions is not

correct?

A. The margin required will be lower if the option is in the money.

B. If the required margin exceeds the posted margin, the option writer will receive a

margin call.

C. A buyer of a put or call option does not have to post margin.

D. Even if the writer of a call option owns the stock, the writer will have to meet the

margin requirement in cash.

Debt securities promise:

I. A fixed stream of income.

II. A stream of income that is determined according to a specific formula.

III. A share in the profits of the issuing entity.

A. I only

B. I or II only

C. I and III only

D. II or III only

A 1-year oil futures contract is selling for $74.50. Spot oil prices are $68, and the 1-year

risk-free rate is 3.25%. Based on the above data, which of the following sets of

transactions will yield positive riskless arbitrage profits?

A. Buy oil in the spot market with borrowed money, and sell the futures contract.

B. Buy the futures contract, and sell the oil spot and invest the money earned.

C. Buy the oil spot with borrowed money, and buy the futures contract.

D. Buy the futures contract, and buy the oil spot using borrowed money.

Hedge fund managers receive incentive bonuses when they increase portfolio assets

beyond a stipulated benchmark but lose nothing when they fail to perform. This is

equivalent to __________.

A. writing a call option

B. receiving a free call option

C. writing a put option

D. receiving a free put option

The type of mutual fund that primarily engages in market timing is called _______.

A. a sector fund

B. an index fund

C. an ETF

D. an asset allocation fund

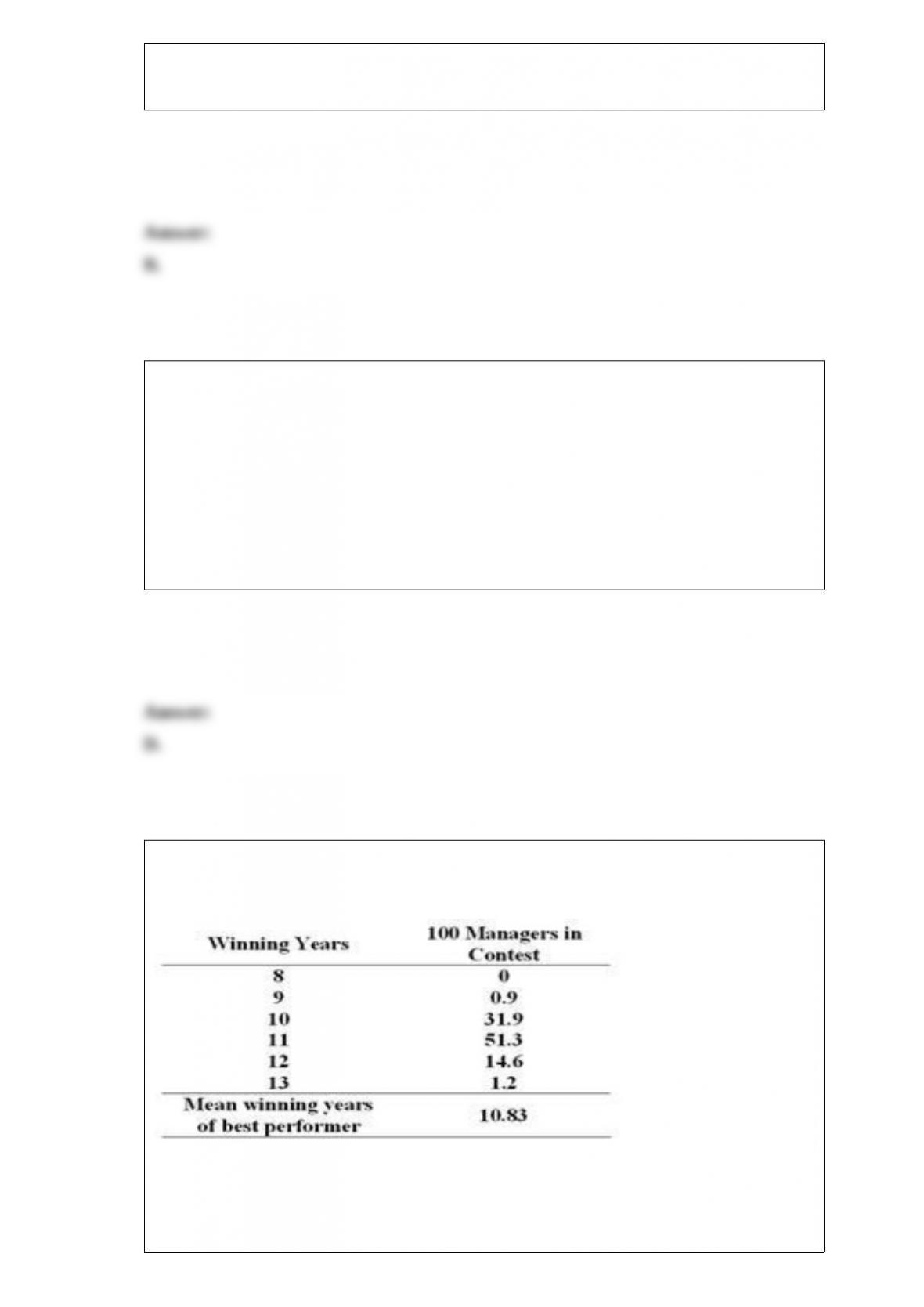

One hundred fund managers enter a contest to see how many times in 13 years they can

earn a higher return than their competitors. The probability distribution of the number

of successful years out of 13 for the best-performing money managers is

Out of this

sample, chance

alone would

indicate that

there is a

______

probability that

someone would

beat the market

at least 11 times

out of 13 years.

A. 51.3%

B. 65.9%

C. 67.1%

D. 10.83%

You purchase one MBI July 90 call contract for a premium of $4. The stock has a

2-for-1 split prior to the expiration date. You hold the option until the expiration date,

when MBI stock sells for $48 per share. You will realize a ______ on the investment.

A. $300 profit

B. $100 loss

C. $400 loss

D. $200 profit

The ________ and the _______ have the lowest correlations with the large-cap indexes.

A. Nasdaq Composite; Russell 2000

B. NYSE; DJIA

C. S&P 500; DJIA

D. Russell 2000; S&P 500

Research by Aragon (2007) indicates that lock-up restrictions tend to hold

____________ portfolios.

A. less liquid

B. more liquid

C. event-driven

D. shorter-maturity

You have an investment horizon of 6 years. You choose to hold a bond with a duration

of 10 years. Your realized rate of return will be larger than the promised yield on the

bond if ___________________.

A. interest rates increase

B. interest rates stay the same

C. interest rates fall

D. The answer cannot be determined from the information given.

The average rate of return on U.S. Treasury bills since 1926 was _________.

A. less than 1%

B. less than 3%

C. less than 4%

D. less than 7%

An expanding economy requires more workers. If the supply of workers becomes

inadequate to meet the demand, what is the likely impact on the economy?

A. an economic slowdown is likely

B. employment trends will reverse and unemployment will occur

C. government deficits will result from capacity utilization

D. inflation may result from upward wage pressures

The risk-free rate in the United States is 2.5%, and the risk-free rate in Europe is 3.2%.

If the spot rate of dollars per euro is 1.32, what is the likely forward rate in terms of

dollars per euro?

A. 1.30

B. 1.31

C. 1.32

D. 1.33

The stock price of Apax Inc. is currently $105. The stock price a year from now will be

either $130 or $90 with equal probabilities. The interest rate at which investors can

borrow is 10%. Using the binomial OPM, the value of a call option with an exercise

price of $110 and an expiration date 1 year from now should be worth __________

today.

A. $11.59

B. $15

C. $20

D. $40

The option smirk in the Black-Scholes option model indicates that __________.

A. implied volatility changes unpredictably as the exercise price rises

B. stock prices may fall by a larger amount than the model assumes

C. stock prices evolve continuously in today’s actively traded markets

D. stocks with lower exercise prices are more likely to pay dividends

To attract new clients, hedge funds often include past returns of funds only if they were

successful. This is called __________.

A. long-short bias

B. survivorship bias

C. backfill bias

D. incentive bias

A project has a 50% chance of doubling your investment in 1 year and a 50% chance of

losing half your money. What is the expected return on this investment project?

A. 0%

B. 25%

C. 50%

D. 75%

A dollar-denominated deposit at a London bank is called _____.

A. eurodollars

B. LIBOR

C. fed funds

D. bankers’ acceptance

Which of the following are examples of cyclical industries?

I. Maytag

II. Computer chip manufacturers

III. Kellogg’s Frosted Flakes

IV. Pfizer

A. I and II only

B. I, II, and III only

C. II, III, and IV only

D. I, II, III, and IV

Assume that you have invested $500,000 to purchase shares in a hedge fund reporting

$800 million in assets, $100 million in liabilities, and 70 million shares outstanding.

Your initial lockout period is 3 years.

If the share price after 3 years increases to $15.28, what is the value of your

investment?

A. $553,600

B. $625,000

C. $733,800

D. $764,000