1) the nyse recently merged with the london stock exchange to form the merged

company nyse euronext.

2) loans comprise the single largest asset category for a bank.

3) writing a call option on a bond pays off if interest rates rise.

4) brokerage commission income and stock market valuations tend to move inversely in

most years, including in 2010 .

5) american options can only be exercised at maturity.

6) privately placed securities are usually sold to one or more investment bankers and

then resold to the general public.

7) the longer the time to maturity, the lower the security’s price sensitivity to an interest

rate change, ceteris paribus.

8) there were a greater number of bank failures from 1980 to 1990 inclusive than from

1934 to 1979 .

9) a negotiated non-standardized agreement between a buyer and seller (with no third

party involvement) to exchange an asset for cash at some future date, with the price set

today is called a forward agreement.

10) money markets exist to help reduce the opportunity cost of holding cash balances.

11) there are now roth versions of 401(k) plans and 403(b) plans as well as roth iras.

12) federal reserve board members are appointed by the u.s. president and confirmed by

the senate for a non-renewable 14-year term.

13) an investor in a gnma mortgage-backed security may be able to earn a return higher

than the rate on a comparable maturity treasury without taking on much, if any, default

risk.

14) life insurance policy reserves are the estimated current worth of expected future

payouts.

15) you have $15,000 to invest in a mutual fund. you choose a fund with a 3.5% front

load, a 1.75% management fee, and a 0.5% 12b-1 fee. assume that the management and

12b-1 fees are charged on year-end assets for simplicity. the gross annual return on the

fund’s shares was 12.50%. what was your net annual rate of return to the nearest basis

point?

a.9.97%

b.6.12%

c.9.25%

d.5.42%

e.8.56%

16) an annual payment bond has a 9% required return. interest rates are projected to fall

25 basis points. the bond’s duration is 12 years. what is the predicted price change?

a.-2.75%

b.33.33%

c.1.95%

d.-1.95%

e.2.75%

17) a u.s. bank converted $1 million to swiss francs to make a swiss franc loan to a

valued corporate customer when the exchange rate was 1.2 francs per dollar. the

borrower agreed to repay the principle plus 5% interest in 1 year. the borrower repaid

swiss francs at loan maturity and when the loan was repaid the exchange rate was 1.3

francs per dollar. what was the bank’s dollar rate of return?

a.26.00%

b.-2.69%

c.7.14%

d.-3.08%

e.5.00%

18) you borrow $95 today for six and a half weeks. you must repay $100 at loan

maturity. what is the effective annual rate on this loan?

a.50.73%

b.40.00%

c.32.33%

d.27.95%

e.37.93%

19) diversified full-line securities firms engage in all but which one of the following?

a.trading and brokerage of existing securities

b.corporate restructuring and advice

c.issuing new securities

d.raising money via insured deposits

20) a u.s. exporter sells $150,000 of furniture to a latin american importer. the exporter

requires the importer to obtain a letter of credit. when the bank accepts the draft the

exporter discounts the 120-day note at a 5.25% discount. what is the exporter’s true

effective annual financing cost?

a.5.52%

b.5.42%

c.5.34%

d.5.29%

e.5.25%

21) the first bank of the ozarks generates $0.0155 dollars of net income per dollar of

assets and it has a profit margin of 12.25%. how much operating income per dollar of

total assets does first bank generate?

a.12.50%

b.12.65%

c.12.75%

d.12.85%

e.12.95%

22) erisa established all but which one of the following?

a.prudent man rule

b.maximum vesting times

c.minimum funding requirements

d.insurance for pension plan participants

e.minimum payouts for defined contribution plans

23) a t-bond with a $1000 par is quoted at 97:14 bid, 97:15 ask. the clean price for you

to buy this bond is

a.$974.38

b.$975.42

c.$974.69

d.$975.77

e.none of the above

24) a four-class cmo has class a, class b, class c, and the residual class z securities

outstanding. which class has the longest duration?

a.class a

b.class b

c.class c

d.class z

e.all have the same duration

25) an insurance line has a loss ratio of 62%, an expense ratio of 35%, the firm pays 2%

of premiums to policyholders as dividends, and has an investment yield to premium

ratio of 9%. the operating ratio for this line is

a.86

b.90

c.95

d.106

e.109

26) a japanese investor can earn a 1% annual interest rate in japan or about 3.5% per

year in the united states. if the spot exchange rate is 101 yen to the dollar, at what

one-year forward rate would an investor be indifferent between the u.s. and japanese

investments?

a.100.58

b.98.56

c.101.68

d.97.42

e.103.50

27) the pbgc

i. insures participants of defined benefit plans if plan funds are insufficient to meet

contractual pension obligations.

ii. insures participants of defined contribution plans if investment returns are

insufficient to meet expected pension obligations.

iii. regulates day-to-day pension fund operations.

a.i only

b.ii only

c.i and iii only

d.ii and iii only

e.i, ii, and iii

28) ceteris paribus, if the fed was targeting the quantity of money supplied and money

demand dropped the fed would likely ______________. if the fed was instead targeting

interest rates and money demand dropped the fed would likely _______________.

a.increase the money supply; do nothing

b.do nothing; decrease the money supply

c.decrease the money supply; do nothing

d.do nothing; increase the money supply

e.increase the money supply; decrease the money supply

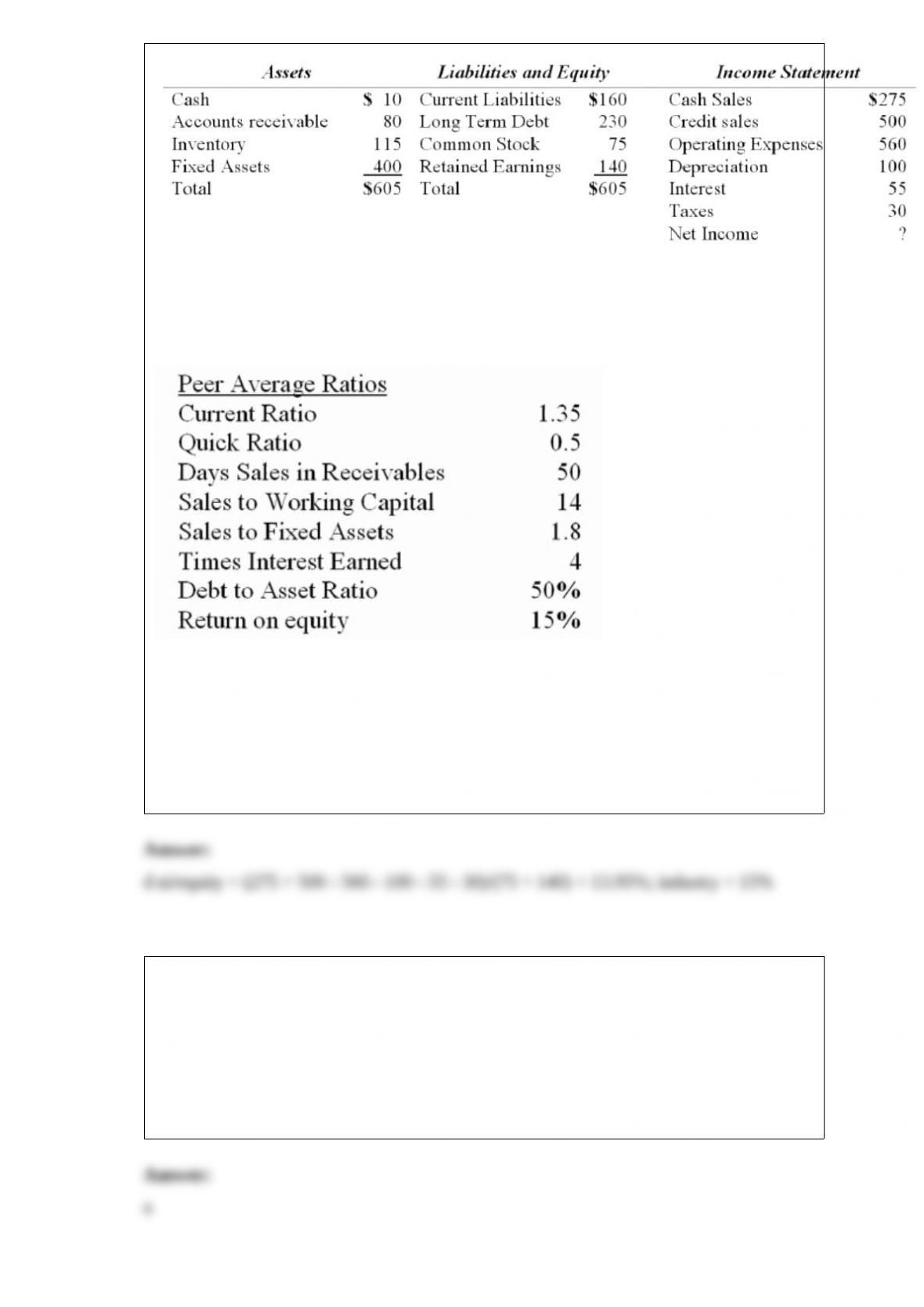

29) figure 20-2

balance sheet big valley enterprises

interest is big valley’s only fixed cash charge.

big valley’s market value of equity to book value of debt ratio = 1.5

big valley’s return on equity indicates that the firm generates a _____ return to their

shareholders than their peers.

a.3.02% higher

b.15.25% higher

c.5.75% lower

d.1.05% lower

e.2.04% higher

30) a speculator may write a put option on stock with an exercise price of $15 and earn

a $3 premium only if they thought

a.the stock price would stay above $12

b.the stock volatility would increase

c.the stock price would fall below $18

d.the stock price would stay above $15

e.the stock price would rise above $18 or fall below $12

31) a $995 million bank has a negative repricing gap equal to 6% of assets. the bank is

currently paying 4.5% on its rate-sensitive liabilities. these rates will vary as interest

rates move. the managers wish to reduce the effective repricing gap to zero with an

interest rate cap or floor. a one-year cap is available with a 5% cap rate and a one-year

floor is available at a floor rate of 4%.

a) suggest a position using either the cap or the floor (but not both) that will limit the

bank’s interest rate risk. explain.

b) suppose that interest rates are volatile this year and the cap costs $275,000 and the

floor costs $195,000. suggest a collar that helps limit the bank’s cost of hedging. how

does the collar affect the bank’s risk?

32) among other things, the _____________ prohibits u.s. banks from providing

banking services to foreign shell banks.

a.international banking act

b.financial services modernization act

c.usa patriot act

d.foreign bank supervision enhancement act

e.foreign banking activity powers enforcement act

33) the most liquid of the money market securities are

a.commercial paper

b.banker’s acceptances

c.t-bills

d.fed funds

e.repurchase agreements

34) suppose a stock is priced at $50. you are bullish on the stock and are considering

buying march calls with an exercise price of $45 and $55, respectively. the 45 call is

priced at $8.50 and the 55 call is quoted at $2.75. what should you consider in deciding

which to purchase if you do not plan on exercising prior to maturity? be specific.

35) why have international stock prices fallen as a result of the subprime crisis in the

united states?

36) you are a corporate treasurer seeking to raise funds for your firm. what are some

advantages of raising funds via a financial intermediary (fi) rather than by selling

securities to the public?

37) what are four major weaknesses of the repricing model?

38) why is the credit risk on a plain vanilla interest rate swap generally less than the

credit risk of a loan with an equivalent (notional) principle amount?

39) you are an investment banker and one of your large u.s. corporate clients has come

to you asking for help deciding on the best market in which to place a sizeable issue of

bonds. you could try to issue dollar-denominated bonds, or euro or yen-denominated

bonds. you could also issue in the united states or overseas. what major factors should

you consider in advising your client on where to market the issue?