Factors contributing to the integration of global capital markets include the reduction in

trade barriers, removal of capital controls, the growing disparity in tax rates among

countries, floating exchange rates, and the free convertibility of currencies. True or

False

Answer:

Poorly defined roles and responsibilities are an important factor contributing to the

failure of many alliances to achieve their objectives. True or False

Answer:

Unlike the European Economic Union, a decision by U.S. antitrust regulators to block a

transaction may be appealed in the courts. True or False

Answer:

The timing of a divestiture is important. If the business to be sold is highly cyclical, the

sale should be timed to coincide with the firm’s peak year earnings. True or False

Answer:

Free cash flow to equity is calculated using operating income. True or False

Answer:

An LBO model helps define the amount of debt a firm can support given its assets and

cash flows. True or False

Answer:

The loan agreement stipulates the terms and conditions under which the lender will loan

the borrower funds. True or False

Answer:

Differences in the way the management of the acquiring and target firms make

decisions, the pace of decision-making, and perceived values are common examples of

cultural differences between the two firms. True or False

Answer:

Premiums paid to LBO target firm shareholders often exceed 40%. True or False

Answer:

Growth rates can be calculated based on the historical experience of the firm or

industry. True or False

Answer:

For capital markets to function smoothly, disputes involving the legal rights of all

participants (both debtors and creditors) need to be resolved quickly and equitably by

the courts. True or False

Answer:

Confidentiality agreements usually also cover publicly available information on the

potential acquirer and target firms. True or False

Answer:

In the absence of a voluntary settlement out of court, the debtor firm may seek

protection from its creditors by initiating bankruptcy or may be forced into bankruptcy

by its creditors. True or False

Answer:

Pro forma financial statements rarely deviate from those compiled in accordance with

GAAP. True or False

Answer:

A target firm’s high employee turnover is often considered a destroyer of value. True or

False

Answer:

The use of convertible preferred stock as a form of payment provides some downside

protection to sellers in the form of continuing dividends, while providing upside

potential if the acquirer’s common stock price increases above the conversion point.

True or False

Answer:

Since an LBO’s debt is to be paid off over time, the cost of equity decreases over time,

assuming other factors remain unchanged. Therefore, in valuing a leveraged buyout, the

analyst must project free cash flows, adjusting the discount rate to reflect changes in the

capital structure. True or False

Answer:

Preferred dividends are tax deductible to U.S. corporations. True or False

Answer:

In a one-tier offer, the acquirer announces the same offer to all target shareholders. True

or False.

Answer:

In calculating the value of net synergy, the costs required to realize the anticipated

synergy should be ignored because they are difficult to forecast. True or False

Answer:

If the form of acquisition is a statutory merger, the seller retains all known, unknown or

contingent liabilities.

True or False

Answer:

Revenue may be inflated by booking as revenue products shipped to resellers without

adequately adjusting for probable returns. True or False

Answer:

Language barriers, different customs, working conditions, work ethics, and legal

structures create a new set of challenges in integrating cross-border transactions. True

or False

Answer:

It is impossible for a leveraged buyout to make sense to common equity investors but

not to other investors, such as pre-LBO debt holders and preferred stockholders. True or

False

Answer:

A single asset is often used to collateralize loans from different lenders in LBO

transactions. True or False

Answer:

The primary forms of proxy contests are those for seats on the board of directors, those

concerning management proposals, and those seeking to force management to take a

particular action. True or False

Answer:

How ownership interests will be transferred in a business alliance is a relatively

unimportant deal structuring issue. True or False

Answer:

Valuations of target firms based on the comparable companies and recent transactions

methods must be adjusted to reflect control premiums. True or False

Answer:

The capitalization rate is equivalent to the discount rate when the firm’s revenues are

not expected to grow. True or False

Answer:

An affirmative covenant is a portion of a loan agreement that specifies the actions the

borrowing firm cannot take during the term of the loan. True or False

Answer:

Joint ventures sometimes represent good alternatives to an outright merger. True or

False

Answer:

The use of market-based valuation methods usually reflect actual demand and supply

considerations at a moment in time. True or False

Answer:

Interest rates and expected inflation in one country compared to another country seldom

affect exchange rates between the two countries. True or False

Answer:

If cash flows are in terms of local currency and the U.S. Treasury bond rate is used to

estimate the risk free rate, the analyst should add the expected inflation rate in the local

country relative to that in the U.S. to convert the U.S. Treasury bond rate to a local

country nominal rate. True or False

Answer:

If the regulatory authorities suspect that a potential transaction may be anti-competitive,

they will file a lawsuit to prevent completion of the transaction. True or False

Answer:

Corporate governance refers to a system of controls both internal and external to the

firm that protects stakeholders’ interests. True or False

Answer:

Confidentiality agreements often cover both the buyer and the seller, since both are

likely to be exchanging confidential information, although for different reasons. True or

False

Answer:

In general, the appropriate marginal tax rate used in calculating cash flows and the

discount rate should be that applicable to the country in which the cash flows are

produced. True or False

Answer:

The analyst should be careful not to mechanically add an acquisition premium to the

target firm’s estimated value based on the comparable companies’ method if there is

evidence that the market values of these “comparable firms” already reflect the effects

of acquisition activity elsewhere in the industry. True or False

Answer:

Asset oriented approaches to valuation involve the use of tangible book value,

liquidation value, discounted cash flows, and break-up values. True or False

Answer:

Which of the following is generally true about financing JVs and partnerships?

a. Lenders rarely require guarantees from the parents

b. Bank loans are commonly used to meet short-term cash requirements

c. Participants must agree on an appropriate financial structure for the organization

d. Contributions by the partners of intangible assets are usually easy to value

e. Corporations are an uncommon form of legal structure

Answer:

GENERAL MOTORS BUYS 20% OF SUBARU

In late 1999, General Motors (GM), the world’s largest auto manufacturer, agreed to

purchase 20% of Japan’s Fuji Heavy Industries, Ltd., the manufacturer of Subaru

vehicles, for $1.4 billion. GM’s objective is to accelerate GM’s push into Asia. The

investment gives GM an interest in an auto manufacturer known for four-wheel drive

vehicles. In combination with its current holdings, GM now has a position in every

segment of Japan’s auto market, including minivans, small and midsize cars, and trucks.

GM already owns 10% of Suzuki Motor Corporation and 49% of Isuzu Motors Ltd.

GM can now expand in Asia more quickly and at a lower cost than if it developed

products independently.

GM has been collaborating with Fuji on various products since 1995. The move

underscores GM’s commitment to expanding its current modest position in the Asian

market, which is expected to be the fastest growing market during the next decade. GM

has sold less than 500,000 in the Asia-Pacific region in 1999, including about 60,000 in

Japan. In 2002, GM bought the remaining outstanding stock of Subaru.

Discussion Questions:

1) What other motives may General Motors have had in making this investment?

2) Why do you believe that General Motors may have wanted to limit initially its

investment to 20%?

Answer:

The share exchange ratio is impacted by all of the following except for

a. The current share price of the target firm

b. The current share price of the acquirer

c. The offer price for the target firm

d. The number of shares outstanding for the target firm

e. A and D

Answer:

Successfully integrated mergers and acquisitions are frequently those which

a. Communicate candidly and continuously

b. Appoint an integration manager and team with clearly defined goals and

responsibilities

c. Establish well defined lines of authority

d. Focus on issues that have the greatest near-term impact

e. All of the above

Answer:

Which of the following are examples of cost-related synergy?

a. Spreading fixed costs over increased output levels

b. Eliminating duplicate jobs

c. Discounts from suppliers due to bulk purchases

d. Paying termination expenses

e. A, B, and C only

Answer:

Which of the following is true about integration planning? Without integration

planning, integration is not likely to

a. Provide anticipated synergies

b. Proceed without significant disruption to the target business’ operations

c. Proceed without significant disruption to the acquirer’s operations

d. Be completed without experiencing substantial customer attrition

e. All of the above

Answer:

Which of the following is generally not true of a financing contingency?

a. It is a condition of closing in the agreement of purchase and sale

b. Trigger the payment of break-up fees if not satisfied.

c. Protects both the lender and seller

d. Primarily protects the buyer

e. Primarily protects the seller

Answer:

Using the cost of capital method to value an LBO involves which of the following

steps?

a. Projection of annual cash flows

b. Projection of annual debt-to-equity ratios

c. Calculation of a terminal value

d. Adjusting the discount rate to reflect changing risk.

e. All of the above

Answer:

An equity carve-out by a parent of one of its subsidiaries is often a precursor to a

a. Complete divestiture or spin-off of the subsidiary

b. An acquisition

c. A merger

d. Joint venture

e. The creation of a tracking stock

Answer:

Which of the following is not true of an equity carve-out?

a. Creates cash infusion for the parent

b. Change in equity ownership of the unit involved in the carve-out

c. New shares issued to the public

d. Taxable if proceeds returned to shareholders through a dividend or stock buyback

e. Parent ceases to exist

Answer:

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question

Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical

companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and

Company (“Merck”) and Schering-Plough Corp. (Schering-Plough) voted

overwhelmingly to approve a $41.1 billion merger of the two firms. With annual

revenues of $42.4 billion, the new Merck will be second in size only to global

pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and

0.5767 of a share of the common stock of the combined company for each share of

Schering-Plough stock they held, and Merck shareholders received one share of

common stock of the combined company for each share of Merck they held. Merck

shareholders voted to approve the merger agreement, and Schering-Plough shareholders

voted to approve both the merger agreement and the issuance of shares of common

stock in the combined firms. Immediately after the merger, the former shareholders of

Merck and Schering-Plough owned approximately 68 percent and 32 percent,

respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual

cost savings, with Merck reducing its workforce by about 15 percent through facility

consolidations, a highly complementary product offering, and the substantial number of

new drugs under development at Schering-Plough. Furthermore, the deal increases

Merck’s international presence, since 70 percent of Schering-Plough’s revenues come

from abroad. The combined firms both focus on biologics (i.e., drugs derived from

living organisms). The new firm has a product offering that is much more diversified

than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of

shares and for Schering-Plough to argue that it was the acquirer in this transaction. The

importance of the latter point is explained in the following section.

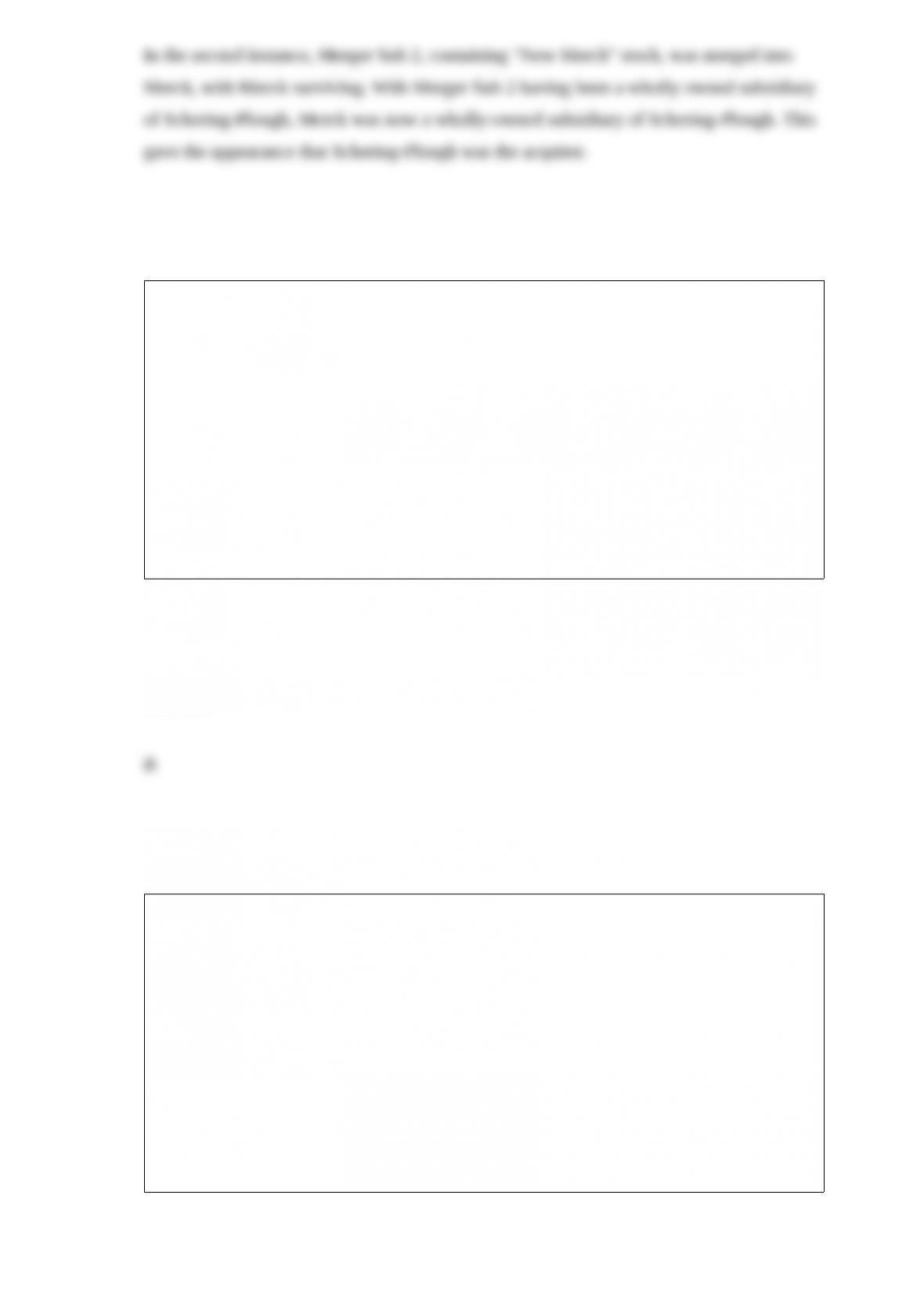

To implement the transaction, Schering-Plough created two merger subsidiaries (i.e.,

Merger Subs 1 and 2) and moved $10 billion in cash provided by Merck and 1.5 billion

new shares (i.e., so-called “New Merck” shares approved by Schering-Plough

shareholders) in the combined Schering-Plough and Merck companies into the

subsidiaries. Merger Sub 1 was merged into Schering-Plough, with Schering-Plough the

surviving firm. Merger Sub 2 was merged with Merck, with Merck surviving as a

wholly-owned subsidiary of Schering-Plough. The end result is the appearance that

Schering-Plough (renamed Merck) acquired Merck through its wholly-owned

subsidiary (Merger Sub 2). In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new

Merck. The “New Merck” is simply Schering-Plough renamed Merck. This structure

allows Schering-Plough to argue that no change in control occurred and that a

termination clause in a partnership agreement with Johnson & Johnson should not be

triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis

drug it had developed called Remicade, and Schering-Plough has the exclusive right to

sell the drug outside the United States, reflecting its stronger international distribution

channel. If the change of control clause were triggered, rights to distribute the drug

outside the United States would revert back to J&J. Remicade represented $2.1 billion

or about 20 percent of Schering-Plough’s 2008 revenues and about 70 percent of the

firm’s international revenues. Consequently, retaining these revenues following the

merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following

diagrams. From a legal perspective, all these actions occur concurrently.

Step 1: Schering-Plough renamed Merck (denoted in the diagrams as “New Merck”)

a. Schering-Plough creates two wholly-owned merger subs

b. Schering-Plough transfers cash provided by Merck and newly issued “New Merck”

stock

into Merger Sub 1 and only “New Merck” stock into Merger Sub 2.

Step 2: Schering-Plough Merger:

a. Merger Sub 1 merges into Schering-Plough in a reverse merger with Schering-Plough

surviving

b. To compensate shareholders, Schering-Plough shareholders exchange their

shares for cash and stock in “New Merck”

c. Former Schering-Plough shareholders now hold stock in “New Merck”

Step 3: Merck Merger:

a. Merger Sub 2 merges into Merck with Merck surviving

b. To compensate shareholders, Merck shareholders exchange their shares for

shares in “New Merck”

c. Former shareholders in Merck now hold shares in “New Merck” (i.e.,

a renamed Schering-Plough)

e. Merger Sub 2, a subsidiary of “New Merck,” now owns Merck.

Concluding Comments

In reality, Merck was the acquirer. Merck provided the money to purchase

Schering-Plough, and Richard Clark, Merck’s chairman and CEO, will run the newly

combined firm when Fred Hassan, Schering-Plough’s CEO, steps down. The new firm

has been renamed Merck to reflect its broader brand recognition. Three-fourths of the

new firm’s board consists of former Merck directors, with the remainder coming from

Schering-Plough’s board. These factors would give Merck effective control of the

combined Merck and Schering-Plough operations. Finally, former Merck shareholders

own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a

conventional merger and, as such, triggered the change of control provision in its

partnership agreement with Schering-Plough. Schering-Plough argued that the reverse

merger bypasses the change of control clause in the agreement, and, consequently, J&J

could not terminate the joint venture. In the past, U.S. courts have tended to focus on

the form rather than the spirit of a transaction. The implications of the form of a

transaction are usually relatively explicit, while determining what was actually intended

(i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a

final ruling would be forthcoming in 2011. Potential outcomes could include J&J

receiving rights to Remicade with damages to be paid by Merck; a finding that the

merger did not constitute a change in control, which would keep the distribution

agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas

but providing for more royalties to J&J.

Discussion Questions

Discussion Questions:

1) Do you agree with the argument that the courts should focus on the form or structure

of an agreement and not try to interpret the actual intent of the parties to the

transaction? Explain your answer.

2) How might allowing the form of a transaction to override the actual spirit or intent of

the deal impact the cost of doing business for the parties involved in the distribution

agreement? Be specific.

3) How did the use of a reverse merger facilitate the transaction?

Answer:

What happens to the outstanding shares of the target firm when the acquirer

purchases 100% of the target’s outstanding stock?

a. They are added to the number of shares of Acquirer stock outstanding

b. They are cancelled.

c. They are converted into preferred stock.

d. They are shown as treasury stock on the books of the combined companies.

e. They are swapped for debt in the new company.

Answer:

Which of the following statements are true about due diligence?

a. The seller should perform due diligence on its own operations.

b. The seller should perform due diligence on the buyer.

c. The seller should perform due diligence on the lender used by the buyer to finance

the transaction.

d. A & B

e. A, B, & C

Answer:

News Corporation of America announced its intention to purchase shares in another

national newspaper chain.

Which one of the following terms best describes this announcement?

a. Divestiture

b. Spinoff

c. Consolidation

d. Tender offer

e. Merger proposal

Answer:

Which of the following is not true of a 338 election ?

a. It applies to asset purchases only.

b. It applies to stock purchases only.

c. It allows a purchase of stock to be treated as an asset purchase for tax purposes.

d. The buyer must adopt the 338 election.

e. The seller must agree with the adoption of the 338 election.

Answer:

Bank of America Acquires Merrill Lynch

Against the backdrop of the Lehman Brothers’ Chapter 11 bankruptcy filing, Bank of

America (BofA) CEO Kenneth Lewis announced on September 15, 2008, that the bank

had reached agreement to acquire megaretail broker and investment bank Merrill

Lynch. Hammered out in a few days, investors expressed concern that the BofA’s swift

action on the all-stock $50 billion transaction would saddle the firm with billions of

dollars in problem assets by pushing BofA’s share price down by 21 percent.

BofA saw the takeover of Merrill as an important step toward achieving its long-held

vision of becoming the number 1 provider of financial services in its domestic market.

The firm’s business strategy was to focus its efforts on the U.S. market by expanding its

product offering and geographic coverage. The firm implemented its business strategy

by acquiring selected financial services companies to fill gaps in its product offering

and geographic coverage. The existence of a clear and measurable vision for the future

enabled BofA to make acquisitions as the opportunity arose.

Since 2001, the firm completed a series of acquisitions valued at more than $150

billion. The firm acquired FleetBoston Financial, greatly expanding its network of

branches on the East Coast, and LaSalle Bank to improve its coverage in the Midwest.

The acquisitions of credit cardissuing powerhouse MBNA, U.S. Trust (a major private

wealth manager), and Countrywide (the nation’s largest residential mortgage loan

company) were made to broaden the firm’s financial services offering.

The acquisition of Merrill makes BofA the country’s largest provider of wealth

management services to go with its current status as the nation’s largest branch banking

network and the largest issuer of small business, home equity, credit card, and

residential mortgage loans. The deal creates the largest domestic retail brokerage and

puts the bank among the top five largest global investment banks. Merrill also owns 45

percent of the profitable asset manager BlackRock Inc., worth an estimated $10 billion.

BofA expects its retail network to help sell Merrill and BlackRock’s investment

products to BofA customers.

The hurried takeover encouraged by the U.S. Treasury and Federal Reserve did not

allow for proper due diligence. The extent of the troubled assets on Merrill’s books was

largely unknown. While the losses at Merrill proved to be stunning in the short run$15

billion alone in the fourth quarter of 2008the acquisition by Bank of America averted

the possible demise of Merrill Lynch. By the end of the first quarter of 2009, the U.S.

government had injected $45 billion in loans and capital into BofA in an effort to offset

some of the asset write-offs associated with the acquisition. Later that year, Lewis

announced his retirement from the bank.

Mortgage loan losses and foreclosures continued to mount throughout 2010, with a

disproportionately large amount of such losses attributable to the acquisition of the

Countrywide mortgage loan portfolio. While BofA’s vision and strategy may still prove

to be sound, the rushed execution of the Merrill acquisition, coupled with problems

surfacing from other acquisitions, could hobble the financial performance of BofA for

years to come.

When Companies OverpayMattel Acquires The Learning Company

Mattel, Inc. is the world’s largest designer, manufacturer, and marketer of a broad

variety of children’s products selling directly to retailers and consumers. Most people

recognize Mattel as the maker of the famous Barbie, the best-selling fashion doll in the

world, generating sales of $1.7 billion annually. The company also manufactures a

variety of other well-known toys and owns the primary toy license for the most popular

kids’ educational program “Sesame Street.” In 1988, Mattel revived its previous

association with The Walt Disney Company and signed a multiyear deal with them for

the worldwide toy rights for all of Disney’s television and film properties

Business Plan

Mission Statement and Strategy

Mattel’s mission is to maintain its position in the toy market as the largest and most

profitable family products marketer and manufacturer in the world. Mattel will continue

to create new products and innovate in their existing toy lines to satisfy the constant

changes of the family-products market. Its business strategy is to diversify Mattel

beyond the market for traditional toys at a time when the toy industry is changing

rapidly. This will be achieved by pursuing the high-growth and highly profitable

children’s technology market, while continuing to enhance Mattel’s popular toys to gain

market share and increase earnings in the toy market. Mattel believes that its current

software division, Mattel Interactive, lacks the technical expertise and resources to

penetrate the software market as quickly as the company desires. Consequently, Mattel

seeks to acquire a software business that will be able to manufacture and market

children’s software that Mattel will distribute through its existing channels and through

its Website (Mattel.com).

Defining the Marketplace

The toy market is a major segment within the leisure time industry. Included in this

segment are many diverse companies, ranging from amusement parks to yacht

manufacturers. Mattel is one of the largest manufacturers within the toy segment of the

leisure time industry. Other leading toy companies are Hasbro, Nintendo, and Lego.

Annual toy industry sales in recent years have exceeded $21 billion. Approximately

one-half of all sales are made in the fourth quarter, reflecting the Christmas holiday.

Customers. Mattel’s major customers are the large retail and e-commerce stores that

distribute their products. These retailers and e-commerce stores in 1999 included Toys

“R” Us Inc., Wal-Mart Stores Inc., Kmart Corp., Target, Consolidated Stores Corp.,

E-toys, ToyTime.com, Toysmart.com, and Toystore.com. The retailers are Mattel’s

direct customers; however, the ultimate buyers are the parents, grandparents, and

children who purchase the toys from these retailers.

Competitors. The two largest toy manufacturers are Mattel and Hasbro, which together

account for almost one-half of industry sales. In the past few years, Hasbro has acquired

several companies whose primary products include electronic or interactive toys and

games. On December 8, 1999, Hasbro announced that it would shift its focus to

software and other electronic toys. Traditional games, such as Monopoly, would be

converted into software.

Potential Entrants. Potential entrants face substantial barriers to entry in the toy

business. Current competitors, such as Mattel and Hasbro, already have secured

distribution channels for their products based on longstanding relationships with key

customers such as Wal-Mart and Toys “R” Us. It would be costly for new entrants to

replicate these relationships. Moreover, brand recognition of such toys as Barbie,

Nintendo, and Lego makes it difficult for new entrants to penetrate certain product

segments within the toy market. Proprietary knowledge and patent protection provide

additional barriers to entering these product lines. The large toymakers have licensing

agreements that grant them the right to market toys based on the products of the major

entertainment companies.

Product Substitutes. One of the major substitutes for traditional toys such as dolls and

cars are video games and computer software. Other product substitutes include virtually

all kinds of entertainment including books, athletic wear, tapes, and TV. However, these

entertainment products are less of a concern for toy companies than the Internet or

electronic games because they are not direct substitutes for traditional toys.

Suppliers. An estimated 80% of toy production is manufactured abroad. Both Mattel

and Hasbro own factories in the Far East and Mexico to take advantage of low labor

costs. Parts, such as software and microchips, often are outsourced to non-Mattel

manufacturing plants in other countries and then imported for the assembly of such

products as Barbie within Mattel-owned factories. Although outsourcing has resulted in

labor cost savings, it also has resulted in inconsistent quality.

Opportunities and Threats

Opportunities

New Distribution Channels. Mattel.com represents 80 separate toy and software

offerings. Mattel hopes to spin this operation off as a separate company when it

becomes profitable. Mattel.com lost about $70 million in 1999. The other new channel

for distributing toys is directly to consumers through catalogs. The so-called direct

channels offered by the internet and catalog sales help Mattel reduce its dependence on

a few mass retailers.

Aging Population. Grandparents accounted for 14% of U.S. toy purchases in 1999. The

number of grandparents is expected to grow from 58 million in 1999 to 76 million in

2005.

Interactive Media. As children have increasing access to computers, the demand for

interactive computer games is expected to accelerate. The “high-tech” toy market

segment is growing 20% annually, compared with the modest 5% growth in the

traditional toy business.

International Growth. In 1999, 44% of Mattel’s sales came from its international

operations. Mattel already has redesigned its Barbie doll for the Asian and the South

American market by changing Barbie’s face and clothes.

Threats

Decreasing Demand for Traditional Toys. Children’s tastes are changing. Popular items

are now more likely to include athletic clothes and children’s software and video games

rather than more traditional items such as dolls and stuffed animals.

Distributor Returns. Distributors may return toys found to be unsafe or unpopular. A

quality problem with the Cabbage Patch Doll could cost Mattel more than $10 million

in returns and in settling lawsuits.

Shrinking Target Market. Historically, the toy industry has considered their prime

market to be children from birth to age 14. Today, the top toy-purchasing years for a

child range from birth to age 10.

Just-In-Time Inventory Management. Changing customer inventory practices make it

difficult to accurately forecast reorders, which has resulted in lost sales as unanticipated

increases in orders could not be filled from current manufacturer inventories.

Internal Assessment

Strengths

Mattel’s key strengths lie in its relatively low manufacturing cost position, with 85% of

its toys manufactured in low-labor-cost countries like China and Indonesia, and its

established distribution channels. Moreover, licensing agreements with Disney enable

Mattel to add popular new characters to its product lines.

Weaknesses

Mattel’s Barbie and Hot Wheels product lines are mature, but the company has been

slow to reposition these core brands. The lack of technical expertise to create

software-based products limits Mattel’s ability to exploit the shift away from traditional

toys to video or interactive games.

Acquisition Plan

Objectives and Strategy

Mattel’s corporate strategy is to diversify Mattel beyond the mature traditional toys

segment into high-growth segments. Mattel believed that it had to acquire a recognized

brand identity in the children’s software and entertainment segment of the toy industry,

sometimes called the “edutainment” segment, to participate in the rapid shift to

interactive, software-based toys that are both entertaining and educational. Mattel

believed that such an acquisition would remove some of the seasonality from sales and

broaden their global revenue base. Key acquisition objectives included building a

global brand strategy, doubling international sales, and creating a $1 billion software

business by January 2001.

Defining the Target Industry

The “edutainment” segment has been experiencing strong growth predominantly in the

entertainment segment. Parents are seeing the importance of technology in the

workplace and want to familiarize their children with the technology as early as

possible. In 1998, more than 40% of households had computers and, of those

households with children, 70% had educational software. As the number of homes with

PCs continues to increase worldwide and with the proliferation of video games, the

demand for educational and entertainment software is expected to accelerate.

Management Preferences

Mattel was looking for an independent children’s software company with a strong brand

identity and more than $400 million in annual sales. Mattel preferred not to acquire a

business that was part of another competitor (e.g., Hasbro Interactive). Mattel’s

management stated that the target must have brands that complement Mattel’s business

strategy and the technology to support their existing brands, as well as to develop new

brands. Mattel preferred to engage in a stock-for-stock exchange in any transaction to

maintain manageable debt levels and to ensure that it preserved the rights to all

software patents and licenses. Moreover, Mattel reasoned that such a transaction would

be more attractive to potential targets because it would enable target shareholders to

defer the payment of taxes.

Potential Targets

Game and edutainment development divisions are often part of software conglomerates,

such as Cendant, Electronic Arts, and GT Interactive, which produce software for

diverse markets including games, systems platforms, business management, home

improvement, and pure educational applications. Other firms may be subsidiaries of

large book, CD-ROM, or game publishers. The parent firms showed little inclination to

sell these businesses at what Mattel believed were reasonable prices. Therefore, Mattel

focused on five publicly traded firms: Acclaim Entertainment, Inc., Activision, Inc.,

Interplay Entertainment Corp, The Learning Company, Inc. (TLC), and Take-Two

Interactive Software. Of these, only Acclaim, Activision, and The Learning Company

had their own established brands in the games and edutainment sectors and the size

sufficient to meet Mattel’s revenue criterion.

In 1999, TLC was the second largest consumer software company in the world, behind

Microsoft. TLC was the leader in educational software, with a 42% market share, and

in-home productivity software (i.e., home improvement software), with a 44% market

share. The company has been following an aggressive expansion strategy, having

completed 14 acquisitions since 1994. At 68%, TLC also had the highest gross profit

margin of the target companies reviewed. TLC owned the most recognized titles and

appeared to have the management and technical skills in place to handle the kind of

volume that Mattel desired. Their sales were almost $1 billion, which would enable

Mattel to achieve its objective in this “high-tech” market. Thus, TLC seemed the best

suited to satisfy Mattel’s acquisition objectives.

Completing the Acquisition

Despite disturbing discoveries during due diligence, Mattel acquired TLC in a

stock-for-stock transaction valued at $3.8 billion on May 13, 1999. Mattel had

determined that TLC’s receivables were overstated because product returns from

distributors were not deducted from receivables and its allowance for bad debt was

inadequate. A $50 billion licensing deal also had been prematurely put on the balance

sheet. Finally, TLC’s brands were becoming outdated. TLC had substantially

exaggerated the amount of money put into research and development for new software

products. Nevertheless, driven by the appeal of rapidly becoming a big player in the

children’s software market, Mattel closed on the transaction aware that TLC’s cash

flows were overstated.

Epilogue

For all of 1999, TLC represented a pretax loss of $206 million. After restructuring

charges, Mattel’s consolidated 1999 net loss was $82.4 million on sales of $5.5 billion.

TLC’s top executives left Mattel and sold their Mattel shares in August, just before the

third quarter’s financial performance was released. Mattel’s stock fell by more than 35%

during 1999 to end the year at about $14 per share. On February 3, 2000, Mattel

announced that its chief executive officer (CEO), Jill Barrad, was leaving the company.

On September 30, 2000, Mattel virtually gave away The Learning Company to rid itself

of what had become a seemingly intractable problem. This ended what had become a

disastrous foray into software publishing that had cost the firm literally hundreds of

millions of dollars. Mattel, which had paid $3.5 billion for the firm in 1999, sold the

unit to an affiliate of Gores Technology Group for rights to a share of future profits.

Essentially, the deal consisted of no cash upfront and only a share of potential future

revenues. In lieu of cash, Gores agreed to give Mattel 50% of any profits and part of

any future sale of TLC. In a matter of weeks, Gores was able to do what Mattel could

not do in a year. Gores restructured TLC’s seven units into three, set strong controls on

spending, sifted through 467 software titles to focus on the key brands, and repaired

relationships with distributors. Gores also has sold the entertainment division and is

seeking buyers for the remainder of TLC.

Discussion Questions:

1) Why was Mattel interested in diversification?

2) What alternatives to acquisition could Mattel have considered? Discuss the pros and

cons of each

alternative?

3) How might the internet affect the toy industry? What potential conflicts with

customers might be

created?

4) What are the primary barriers to entering the toy industry?

5) What could Mattel have done to protect itself against risks uncovered during due

diligence?

Answer:

All of the following are true except for

a. Chapter 15 deals with international or cross-border bankruptcies.

b. Chapter 11 deals with reorganizing the firm.

c. Chapter 7 defines the process and priorities of the liquidation process for commercial

businesses.

d. Chapter 11 also addresses issues pertaining to personal bankruptcy.

e. A and B

Answer:

Which of the following is not true of a divestiture?

a. May create cash infusion for the parent firm

b. Parent ceases to exist

c. Proceeds of sale taxable if returned to shareholders through a dividend or stock

buyback

d. A new legal subsidiary may be created

e. B and C

Answer:

Which of the following represent important shortcomings of using industry

concentration ratios to

determine whether the combination of certain firms will result in an increase in market

power?

a. Frequent inability to define what constitutes an industry

b. Failure to measure ease of entry or exit for other firms

c. Failure to account for foreign competition

d. Failure to account properly for the distribution of firms of different sizes

e. All of the above

Answer:

Empirical evidence suggests that forecasts of earnings and other value indicators are

better predictors of firm value than value indicators based on historical data. True or

False

Answer:

Which of the following factors is excluded from the calculation of free cash flow to the

firm?

a. Principal repayments

b. Operating income

c. Depreciation

d. The change in working capital

e. Gross plant and equipment spending

Answer:

Valuing a Privately Held Company

Background

BigCo is interested in acquiring PrivCo, whose owner desires to retire. The firm is

100% owned by the current owner. PrivCo has revenues of $10 million and an EBIT of

$2 million in the preceding year. The market value of the firm’s debt is $5 million; the

book value of equity is $4 million. For publicly traded firms in the same industry, the

average debt-to-equity ratio is .4 (based on the market value of debt and equity), and the

marginal tax rate is 40%. Typically, the ratio of the market value of equity to book value

for these firms is The average ß of publicly traded firms that are in the same business is

2.00. Capital expenditures and depreciation amounted to $0.3 million and $0.2 million

in the prior year. Both items are expected to grow at the same rate as revenues for the

next 5 years. Capital expenditures and depreciation are expected to be equal beyond 5

years (i.e., capital spending will be internally funded). As a result of excellent working

capital management practices, the change in working capital is expected to be

essentially zero throughout the forecast period and beyond. The revenues of this firm

are expected to grow 15% annually for the next 5 years and 5% per year thereafter. Net

income is expected to increase 15% a year for the next 5 years and 5% thereafter. The

10-year U.S. Treasury bond rate is 6%. The pretax cost of debt for a nonrated firm is

10%. No adjustment is made in the calculation of the cost of equity for a marketability

discount. Estimate the shareholder value of the firm.

Note: To estimate the WACC for a leveraged private firm, it is necessary to calculate

the firm’s leveraged . This requires an estimate of the firm’s unleveraged ß which can be

obtained by estimating the unleveraged ß for similar firms in the same industry. In

addition, the value of debt and equity in calculating the cost of capital should be

expressed as market rather than book values.

Answer:

The Sarbanes-Oxley bill is intended to achieve which of the following:

a. Auditor independence

b. Corporate responsibility

c. Improved financial disclosure

d. Increased penalties for fraudulent behavior

e. All of the above

Answer:

Pfizer Acquires Wyeth Labs Despite Tight Credit Markets

Pfizer and Wyeth began joint operations on October 22, 2009, when Wyeth shares

stopped trading and each Wyeth share was converted to $33 in cash and 0.985 of a

Pfizer share. Valued at $68 billion, the cash and stock deal was first announced in late

January of 2009. The purchase price represented a 12.6 percent premium over Wyeth’s

closing share price the day before the announcement. Investors from both firms

celebrated as Wyeth’s shares rose 12.6 percent and Pfizer’s 1.4 percent on the news. The

announcement seemed to offer the potential for profit growth, despite storm clouds on

the horizon.

As is true of other large pharmaceutical companies, Pfizer expects to experience serious

erosion in revenue due to expiring patent protection on a number of its major drugs.

Pfizer faced the expiration of patent rights in 2011 to the cholesterol-lowering drug

Lipitor, which accounted for 25 percent of the firm’s $52 billion in 2008 revenue. Pfizer

also faces 14 other patent expirations through 2014 on drugs that, in combination with

Lipitor, contribute more than one-half of the firm’s total revenue. Pfizer is not alone,

Merck, Bristol-Myers Squibb, and Eli Lilly are all facing significant revenue reduction

due to patent expirations during the next five years as competition from generic drugs

undercuts their pricing. Wyeth will also be losing its patent protection on its top-selling

drug, the antidepressant Effexor XR.

Pfizer’s strategy appears to have been to acquire Wyeth at a time when transaction

prices were depressed because of the recession and tight credit markets. Pfizer

anticipates saving more than $4 billion annually by combining the two businesses, with

the savings being phased in over three years. Pfizer also hopes to offset revenue erosion

due to patent expirations by diversifying into vaccines and arthritis treatments.

By the end of 2008, Pfizer already had a $22.5 billion commitment letter in order to

obtain temporary or “bridge” financing and $26 billion in cash and marketable

securities. Pfizer also announced plans to cut its quarterly dividend in half to $0.16 per

share to help finance the transaction. However, there were still questions about the

firm’s ability to complete the transaction in view of the turmoil in the credit markets.

Many transactions that were announced during 2008 were never closed because buyers

were unable to arrange financing and would later claim that the purchase agreement had

been breached due to material adverse changes in the business climate. Such

circumstances, they would argue, would force them to renege on their contracts.

Usually, such contracts contain so-called reverse termination fees, in which the buyer

would agree to pay a fee to the seller if they were unwilling to close the deal. This is

called a reverse termination or breakup fee because traditionally breakup fees are paid

by a seller that chooses to break a contract with a buyer in order to accept a more

attractive offer from another suitor.

Negotiations, which had begun in earnest in late 2008, became increasingly

contentious, not so much because of differences over price or strategy but rather under

what circumstances Pfizer could back out of the deal. Under the terms of the final

agreement, Pfizer would have been liable to pay Wyeth $4.5 billion if its credit rating

dropped prior to closing and it could not finance the transaction. At about 6.6 percent of

the purchase price, the termination fee was about twice the normal breakup fee for a

transaction of this type.

What made this deal unique was that the failure to obtain financing as a pretext for exit

could be claimed only under very limited circumstances. Specifically, Pfizer could

renege only if its lenders refused to finance the transaction because of a credit

downgrade of Pfizer. If lenders refused to finance primarily for this reason, Wyeth

could either demand that Pfizer attempt to find alternative financing or terminate the

agreement. If Wyeth had terminated the agreement, Pfizer would have been obligated to

pay the termination fee.

Using Form of Payment as a Takeover Strategy:

Chevron’s Acquisition of Unocal

Unocal ceased to exist as an independent company on August 11, 2005 and its shares

were de-listed from the New York Stock Exchange. The new firm is known as Chevron.

In a highly politicized transaction, Chevron battled Chinese oil-producer, CNOOC, for

almost four months for ownership of Unocal. A cash and stock bid by Chevron, the

nation’s second largest oil producer, made in April valued at $61 per share was accepted

by the Unocal board when it appeared that CNOOC would not counter-bid. However,

CNOOC soon followed with an all-cash bid of $67 per share. Chevron amended the

merger agreement with a new cash and stock bid valued at $63 per share in late July.

Despite the significant difference in the value of the two bids, the Unocal board

recommended to its shareholders that they accept the amended Chevron bid in view of

the growing doubt that U.S. regulatory authorities would approve a takeover by

CNOOC.

In its strategy to win Unocal shareholder approval, Chevron offered Unocal

shareholders three options for each of their shares: (1) $69 in cash, (2) 1.03 Chevron

shares; or (3) .618 Chevron shares plus $27.60 in cash. Unocal shareholders not

electing any specific option would receive the third option. Moreover, the all-cash and

all-stock offers were subject to proration in order to preserve an overall per share mix of

.618 of a share of Chevron common stock and $27.60 in cash for all of the 272 million

outstanding shares of Unocal common stock. This mix of cash and stock provided a

“blended” value of about $63 per share of Unocal common stock on the day that Unocal

and Chevron entered into the amendment to the merger agreement on July 22, 2005.

The “blended” rate was calculated by multiplying .618 by the value of Chevron stock

on July 22nd of $57.28 plus $27.60 in cash. This resulted in a targeted purchase price

that was about 56 percent Chevron stock and 44 percent cash.

This mix of cash and stock implied that Chevron would pay approximately $7.5 billion

(i.e., $27.60 x 272 million Unocal shares outstanding) in cash and issue approximately

168 million shares of Chevron common stock (i.e., .618 x 272 million of Unocal shares)

valued at $57.28 per share as of July 22, 2005. The implied value of the merger on that

date was $17.1 billion (i.e., $27.60 x 272 million Unocal common shares outstanding

plus $57.28 x 168 million Chevron common shares). An increase in Chevron’s share

price to $63.15 on August 10, 2005, the day of the Unocal shareholders’ meeting,

boosted the value of the deal to $18.1 billion.

Option (1) was intended to appeal to those Unocal shareholders who were attracted to

CNOOC’s all cash offer of $67 per share. Option (2) was designed for those

shareholders interested in a tax-free exchange. Finally, it was anticipated that option (3)

would attract those Unocal shareholders who were interested in cash but also wished to

enjoy any appreciation in the stock of the combined companies.

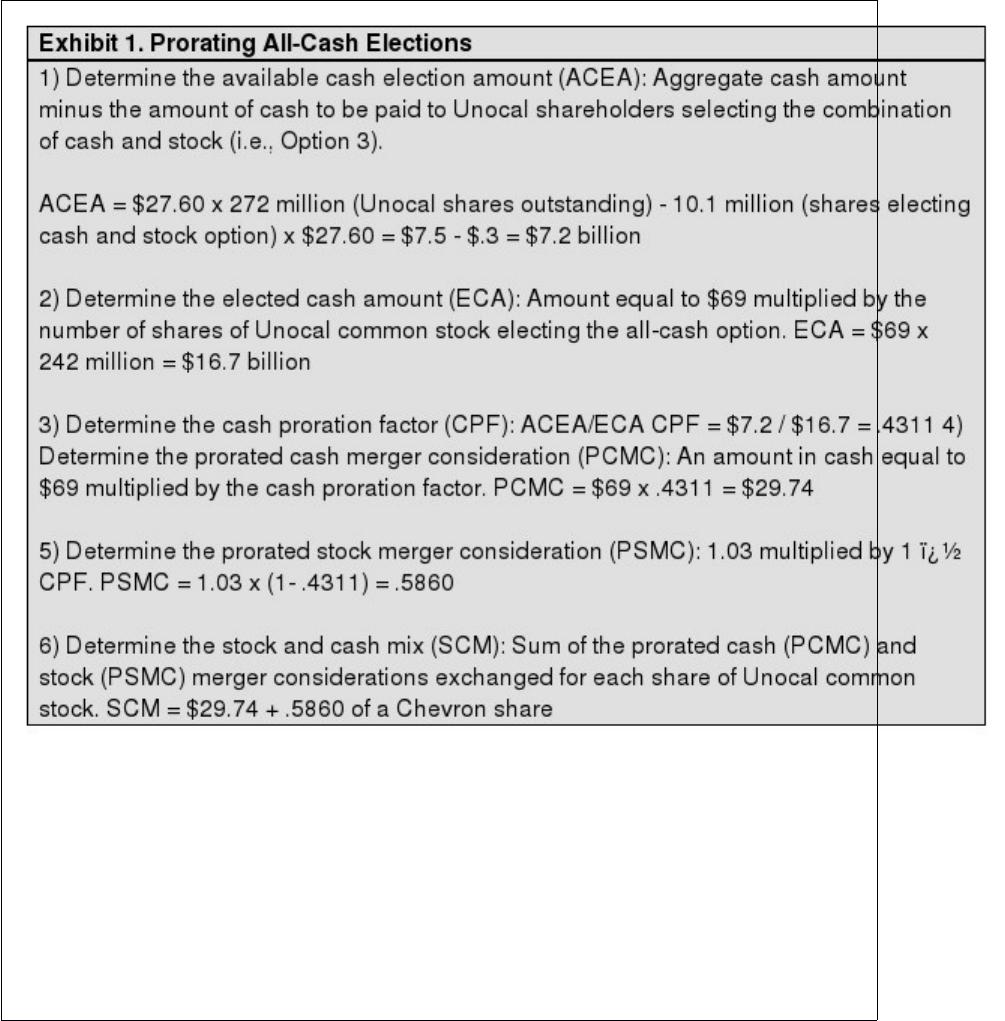

The agreement of purchase and sale between Chevron and Unocal contained a

“proration clause.” This clause enabled Chevron to limit the amount of total cash it

would payout under those options involving cash that it had offered to Unocal

shareholders and to maintain the “blended” rate of $63 it would pay for each share of

Unocal stock. Approximately 242 million Unocal shareholders elected to receive all

cash for their shares, 22.1 million opted for the all-stock alternative, and 10.1 million

elected the cash and stock combination. No election was made for approximately .3

million shares. Based on these results, the amount of cash needed to satisfy the number

shareholders electing the all-cash option far exceeded the amount that Chevron was

willing to pay. Consequently, as permitted in the merger agreement, the all-cash offer

was prorated resulting in the Unocal shareholders who had elected the all-cash option

receiving a combination of cash and stock rather than $69 per share. The mix of cash

and stock was calculated as shown in Exhibit 1.

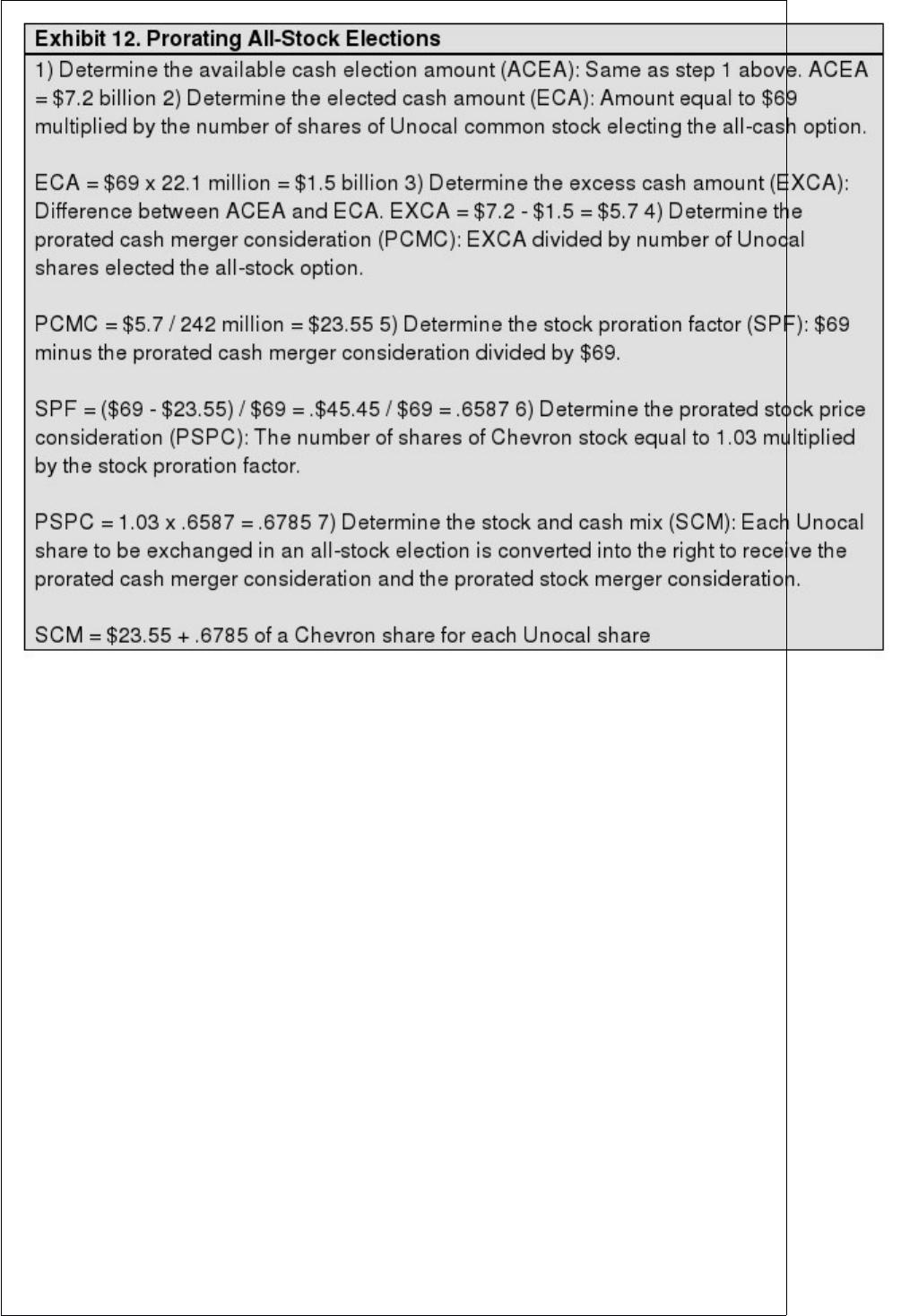

If too many Unocal shareholders had elected to receive Chevron stock, those making

the all-stock election would not have received 1.03 shares of Chevron stock for each

share of Unocal stock. Rather, they would have received a mix of stock and cash to help

preserve the approximate 56 percent stock and 44 percent cash composition of the

purchase price desired by Chevron. For illustration only, assume the number of Unocal

shares to be exchanged for the all-cash and all-stock options are 22.1 and 242 million,

respectively. This is the reverse of what actually happened. The mix of stock and cash

would have been prorated as shown in Exhibit 2.

It is typical of large transactions in which the target has a large, diverse shareholder

base that acquiring firms offer target shareholders a “menu” of alternative forms of

payment. The objective is to enhance the likelihood of success by appealing to a

broader group of shareholders. To the unsophisticated target shareholder, the array of

options may prove appealing. However, it is likely that those electing all-cash or

all-stock purchases are likely to be disappointed due to probable proration clauses in

merger contracts. Such clauses enable the acquirer to maintain an overall mix of cash

and stock in completing the transaction. This enables the acquirer to limit the amount of

cash they must borrow or the number of new shares they must issue to levels they find

acceptable.

Discussion Questions

1) What was the form of payment employed by both bidders for Unocal? In your

judgment, why were they

different? Be specific.

2) How did Chevron use the form of payment as a potential takeover strategy?

3) Is the “proration clause” found in most merger agreements in which target

shareholders are given several ways in which they can choose to be paid for their shares

in the best interests of the target shareholders? In the best interests of the acquirer?

Explain your answer.

Answer:

Form of payment can involve which of the following:

a. Cash

b. Stock

c. Cash and stock

d. Rights, royalties and fees

e. All of the above

Answer:

Determining where a firm should compete requires management to consider which of

the following factors?

a. Determining the firm’s current customers only

b. Determining the firm’s potential customers only

c. Determining the needs of current and potential customers, as well as suppliers

d. Determining the needs of potential suppliers only

e. A and D only

Answer:

News Corp.’s Power Play in Satellite Broadcasting The share prices of Rupert

Murdoch’s News Corp., Fox Entertainment Group Inc., and Hughes Electronics Corp.

(a subsidiary of General Motors Corporation) tumbled immediately following the

announcement that News Corp had reached an agreement to take a controlling interest

in Hughes on April 10, 2003. Immediately following the announcement, shares of Fox

fell by 17 percent, News Corp.’s ADRs (i.e., shares issued by foreign firms trading on

U.S. stock exchanges) by 6.5 percent and Hughes by 9.8 percent.

Hughes Electronics is a world leader in providing digital television entertainment,

broadband satellite networks and services (DirecTV), and global video and data

broadcasting. The News Corporation is a diversified international media and

entertainment company with operations in a number of industry segments, including

filmed entertainment, television, cable network programming, magazines and inserts,

newspapers and book publishing.

News Corp.’s Chairman Rupert Murdoch, had pursued control of Hughes, the parent

company of DirecTV, for several years. News Corp.’s bid valued at about $6.6 billion to

acquire control of Hughes Electronics Corp. and its DirecTV unit gives News Corp a

U.S. presence to augment its satellite TV operations in Britain and Asia. In one bold

move, News Corp became the second largest provider of pay-TV service to U.S. homes,

second only to Comcast. By transferring News Corp.’s stake in Hughes to Fox, Fox

gained control over 11 million subscribers. It gives Fox more leverage for its cable

networks when negotiating rights fees with cable operators that compete with DirecTV.

In negotiating with film studios or sports companies over pay television rights, News

Corp. is now the only global customer, with satellite systems spanning Europe, Asia,

and Latin America. Moreover, News Corp. can cross-promote among DirecTV and its

others businesses (e.g., packaging DirecTV subscriptions with subscriptions to TV

Guide).

General Motors was motivated to sell its investment in Hughes because of its poor

financial performance in recent years and GM’s need for cash. GM and Hughes had first

agreed to a deal with rival satellite broadcaster EchoStar Communications Inc.

However, the deal was blocked by antitrust regulators. Subsequent discussions between

GM/Hughes with SBC Communications and Liberty Media proved unproductive with

these firms offering primarily a share for share exchange. GM’s desire to quickly pull

cash out of Hughes made News Corp.’s offer the most attractive. Consequently, they

chose to accept News Corp.’s proposal rather than pursue a riskier proposal for a

Hughes’ management-sponsored leveraged buyout.

News Corp. financed its purchase of a 34.1% stake in Hughes (i.e., GM’s 20%

ownership and 14.1% from public shareholders) by paying $3.1 billion in cash to GM,

plus 34.3 million in nonvoting American depository receipts (ADRs) in News Corp.

shares. Hughes’ public shareholders will be paid with 122.2 million nonvoting ADRs in

News Corp. Each ADR is equivalent to four News Corp. shares. The resulting issue of

156.5 million shares would dilute News Corp. shareholders by about 13%. Immediately

following closing, News Corp.’s ownership interest was transferred to Fox in exchange

for a $4.5 billion promissory note from Fox and 74 million new Fox shares. This

transfer will saddle Fox with $4.5 billion in debt. This debt would need to be serviced

by Fox’s cash flow and could limit Fox’s access to new capital.

Now that News Corp. controls DirecTV through its 81 percent ownership in Fox, it

must find away to revitalize DirecTV. Against tough cable-TV competition, DirecTV

has experienced a 20% turnover rate among its subscribers, due in part to GM’s benign

neglect while it looked for a buyer. News Corp. will now have to compete against

larger, better financed cable operations, as well as the nimble, low cost EchoStar

Communications Corp’s Dish Network. As an indication of the extent to which Hughes

has stumbled in recent years, News Corp. made a formal bid to acquire all of Hughes

for about $25 billion in cash in 2001. News Corp.’s current investment stake implies a

valuation of less the $20 billion for 100 percent ownership of Hughes (i.e., $6.6

billion/.341).

Discussion Questions:

1) Why did the share prices of News Corp., Fox, and Hughes fall precipitously

following the announcement? Explain your answer. 2) How did News Corp.’s proposed

deal structure better satisfy GM’s needs than those of other bidders? 3) How can it be

said that News Corp. obtained a controlling interest in Hughes when its stake amounted

to only about one-third of Hughes outstanding voting shares? Explain your answer.

Answer:

Which of the following represent options available to managers in making investment

decisions?

a. Delay initial investment

b. Accelerate cumulative investment

c. Abandon the investment at a later date

d. A & B only

e. A, B, & C

Answer:

Which of the following are ways to implement a firm’s business strategy?

a. Merge or acquisition

b. Joint venture

c. Going it alone

d. Asset swap

e. All of the above

Answer:

Greenfield operations represent an appropriate entry if which of the following is true?

a. Entry barriers are low

b. Cultural differences are high

c. Entrant has limited multinational experience

d. Entrant is risk adverse

e. A and B only

Answer:

State “blue sky” laws are designed to

a. Allow states to block M&As deemed as anticompetitive

b. Protect individual investors from investing in fraudulent securities’ offerings

c. Restrict foreign investment in individual states

d. Protect workers’ pensions

e. Prevent premature announcement of M&As

Answer:

Leveraged employee stock ownership plans are frequently used by owners of private

businesses to

a. Hide assets

b. Motivate employees

c. Sell the firm to the employees

d. B and C

e. A, B, and C

Answer: