Which of the following is the equation for cost of goods sold?

A) Beginning inventory + Purchases – Ending inventory

B) Beginning inventory + Purchases + Ending inventory

C) Net purchases – Ending inventory

D) Ending inventory + Purchases – Beginning inventory

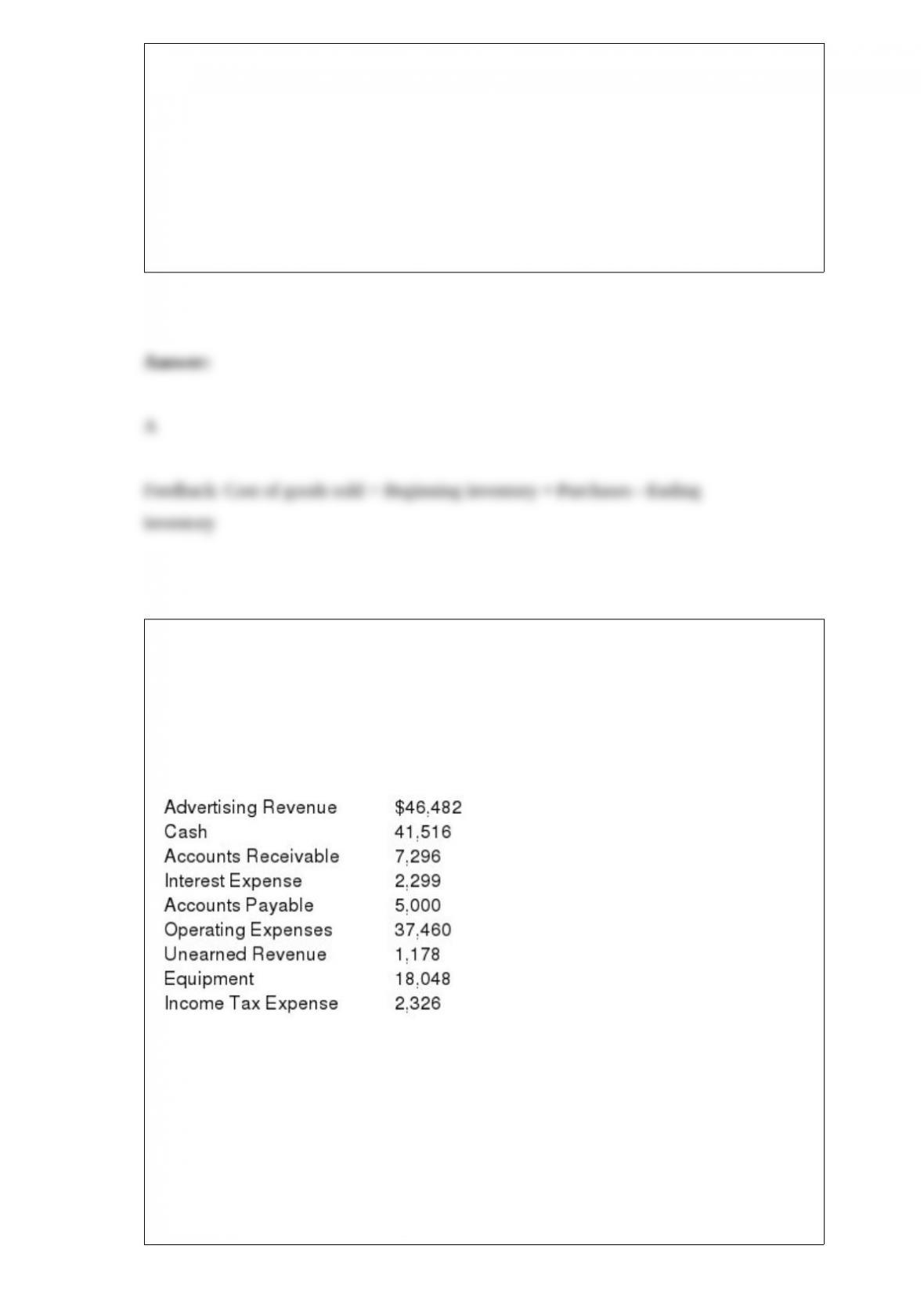

Use the information above to answer the following question. What is the amount of

revenue that will be reported on the income statement for the year ended December 31,

2016?

The following account balances are taken from the December 31, 2015, financial

statements of ABZ Advertising Company. The company uses accrual basis accounting.

The following activities occurred in 2016:

1) Performed advertising services on account, $55,000.

2) Received cash payments on account, $10,400.

3) Received deposits from customers for advertising services to be performed in 2017,

$2,500.

4) Made payments to suppliers on account, $5,000.

5) Incurred $45,000 of operating expenses; $39,000 was paid in cash and $6,000 was on

account and unpaid as of the end of the year.

A) $57,500.

B) $39,000.

C) $55,000.

D) $50,000.

Some bonds allow the borrower to repay the bond by issuing stock. These bonds are

known as:

A) convertible bonds.

B) debenture bonds.

C) callable bonds.

D) coupon bonds.

Which one of the following statements about inventory is not correct?

A) An increase in inventory levels is always a sign of inefficiency in inventory

management.

B) The measurement of inventory affects both the balance sheet and the income

statement within an accounting period.

C) The ending inventory of one accounting period becomes the beginning inventory of

the next accounting period.

D) The cost of inventory can vary over time and may be affected by technological

innovation.

When existing assets are used up in the ordinary course of business:

A) an expense is recorded.

B) unearned revenue is recorded.

C) an accrual is recorded.

D) a prepaid expense is recorded.

On January 1, a company lends a corporate customer $80,000 at 6% interest. The

amount of interest revenue that should be recorded for the quarter ending March 31

equals:

A) $4,800

B) $1,200

C) $400

D) $1,600

On October 31, 2015, your company’s records say that the company has $16,451.03 in

its checking account. A review of the bank statement shows you have three outstanding

checks totaling $5,643.01, and the bank has paid you interest of $12.19 and charged you

$9.00 in service charges. The bank statement dated October 31, 2015 would report a

balance of:

A) $22,090.85.

B) $16,454.22.

C) $22,097.23.

D) $10,804.83.

Soar Inc. enters into the following transactions:

– Stockholders contribute $10,000 cash to a company in exchange for common stock.

– The company purchases $5,000 to buy new equipment by paying cash.

– The company pays $3,000 to suppliers on account.

Required:

Part a. Show the effect of these transactions on the basic accounting equation.

Part b. Prepare the journal entries that would be used to record the transactions.

If a corporation declares and distributes a stock dividend on its common shares:

A) the amount of total assets increases.

B) stockholders’ equity decreases.

C) contributed capital decreases.

D) the account Retained Earnings is decreased.

Which of the following would be in the work in process inventory of a company

making cheese?

A) Milk and cream used to make the cheese

B) Cheese that has been made but is curing before being ready to sell

C) Cured cheese that is waiting to be shipped to retailers

D) Cured cheese that has been sold to retailers

Which of the following would decrease net income?

A) Failing to post an adjusting entry to accrue revenue

B) Understating the amount of Depreciation Expense recorded

C) Failing to prepare an adjusting entry to recognize the portion of prepaid rent that has

expired

D) Overstating the year-end balance of the Supplies account

Use the information above to answer the following question. What is the amount of

revenue that will be reported on the income statement for the month ended July 31?

The following transactions occurred during July:

1) Received $800 cash for services performed during July.

2) Received $5,000 cash from the issuance of common stock to owners.

3) Received $400 from a customer as payment for services performed during June.

4) Billed $3,500 to customers for services performed on account in July.

5) Borrowed $2,500 from the bank and signed a promissory note.

6) Received $1,000 from a customer for services to be performed during August.

A) $5,300.

B) $5,700.

C) $4,300.

D) $7,200.

A company pays $9,000 in interest on notes consisting of $6,000 of interest that was

accrued during the last accounting period and $3,000 of interest that accumulated

during the current accounting period but has not yet been accrued on the books. The

journal entry for the interest payment should include a:

A) debit to Interest Expense for $9,000 and a credit to Cash for $9,000.

B) debit to Cash for $9,000 and a credit to Interest Payable for $9,000.

C) debit to Interest Expense for $3,000, a debit to Interest Payable for $6,000, and a

credit to Cash for $9,000.

D) debit to Interest Payable for $6,000, a debit to Accrued Interest for $3,000, and a

credit to Cash for $9,000.

If an expense has been incurred but will be paid later, then:

A) nothing is recorded on the financial statements.

B) a liability account is created or increased and an expense is recorded.

C) an asset account is decreased or eliminated and an expense is recorded.

D) a revenue and an expense are accrued.

B. Darin Company issued common stock to investors and received $50,000. Which of

the following statements about this transaction is correct?

A) This is an example of a cash inflow from an investing activity.

B) The journal entry to record this transaction will include a credit to Cash.

C) This is an example of a cash outflow from a financing activity.

D) The journal entry to record this transaction will include a credit to Common Stock.

When a company records depletion on natural resources, it will have which of the

following effects?

A) Expenses increase

B) Net income decreases

C) Inventory increases

D) Cash flow decreases

Consider each of the following transactions.

Required:

Indicate how each transaction will affect the elements of the accounting equation by

answering increase, decrease, or no effect.

Assets Liabilities Stockholders’ Equity

a. The company uses the direct write-off method and writes off specific receivables that

have been identified as uncollectible.

b. The company uses the allowance method and records the Bad Debt Expense for the

year in an adjusting entry.

c. The company receives a one-year promissory note from a customer in payment of his

account because he needs additional time to pay.

d. The company receives a payment from a different customer on her account; the

account had been previously written off as worthless.

e. The company accrues interest earned on the note received in (c) in an adjusting entry.

Which of the following journal entries has an effect on cash provided by (used in)

operating activities?

A) Bad debts expense

B) Depreciation expense

C) Sale of an investment

D) Payment of interest on long-term notes payable

A company buys a piece of equipment for $48,000. The equipment has a useful life of

ten years. No residual value is expected at the end of the useful life. Using the

double-declining-balance method, what is the company’s depreciation expense in the

first year of the equipment’s useful life?

A) $9,600

B) $12,000

C) $4,800

D) $24,000

Which of the following statements about adjustments is not correct?

A) Adjusting entries affect the cash account.

B) Adjustments to prepaid expenses and unearned revenues are deferral adjustments.

C) Adjustments for wages and income taxes are normally accrual adjustments. .

D) Adjusting entries involve one income statement account and one balance sheet

account.