1) There are four major factors accounting for the existence of yield differentials.

Which of the following is not a factor?

a. Segments

b. Sectors

c. Indentures

d. Coupons

e. Maturities

2) Research has shown that the asset allocation decision explains ____% of the

variation in fund returns across all funds, and ____% of the variation in returns for a

particular fund over time.

a.90 and 100.

b.100 and 40.

c.90 and 40.

d.40 and 100.

e.40 and 90.

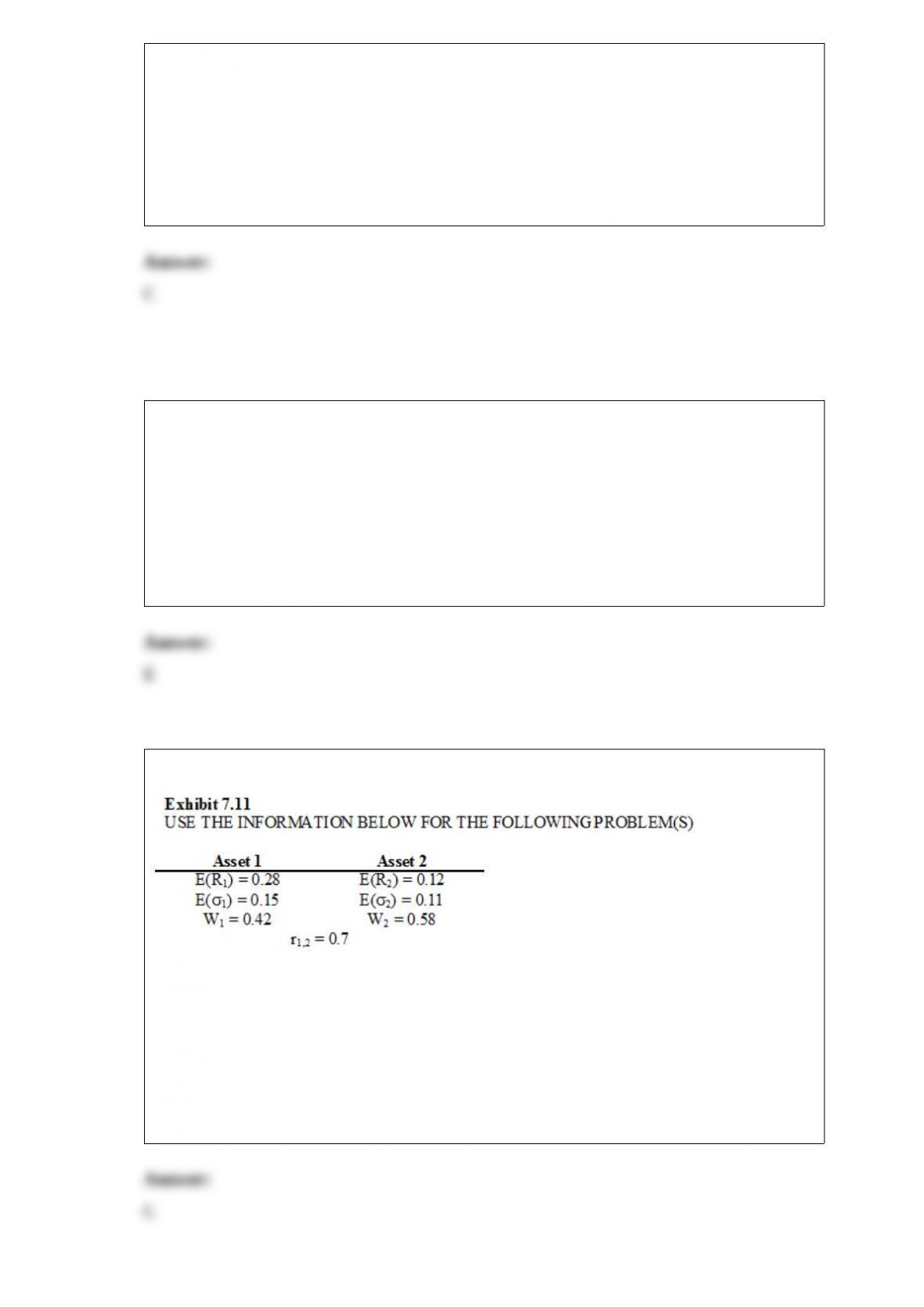

3)

Refer to Exhibit 7.11. Calculate the expected standard deviation of the two stock

portfolio.

a. 0.1367

b. 0.1872

c. 0.1169

d. 0.20

e. 0.3950

4) The yield to call is a more conservative yield measure whenever the price of a

callable bond is quoted at a value

a. Equal to or greater than par plus one year’s interest.

b. Equal to par.

c. Equal to par less one year’s interest.

d. Less than par.

e. Five percent over par.

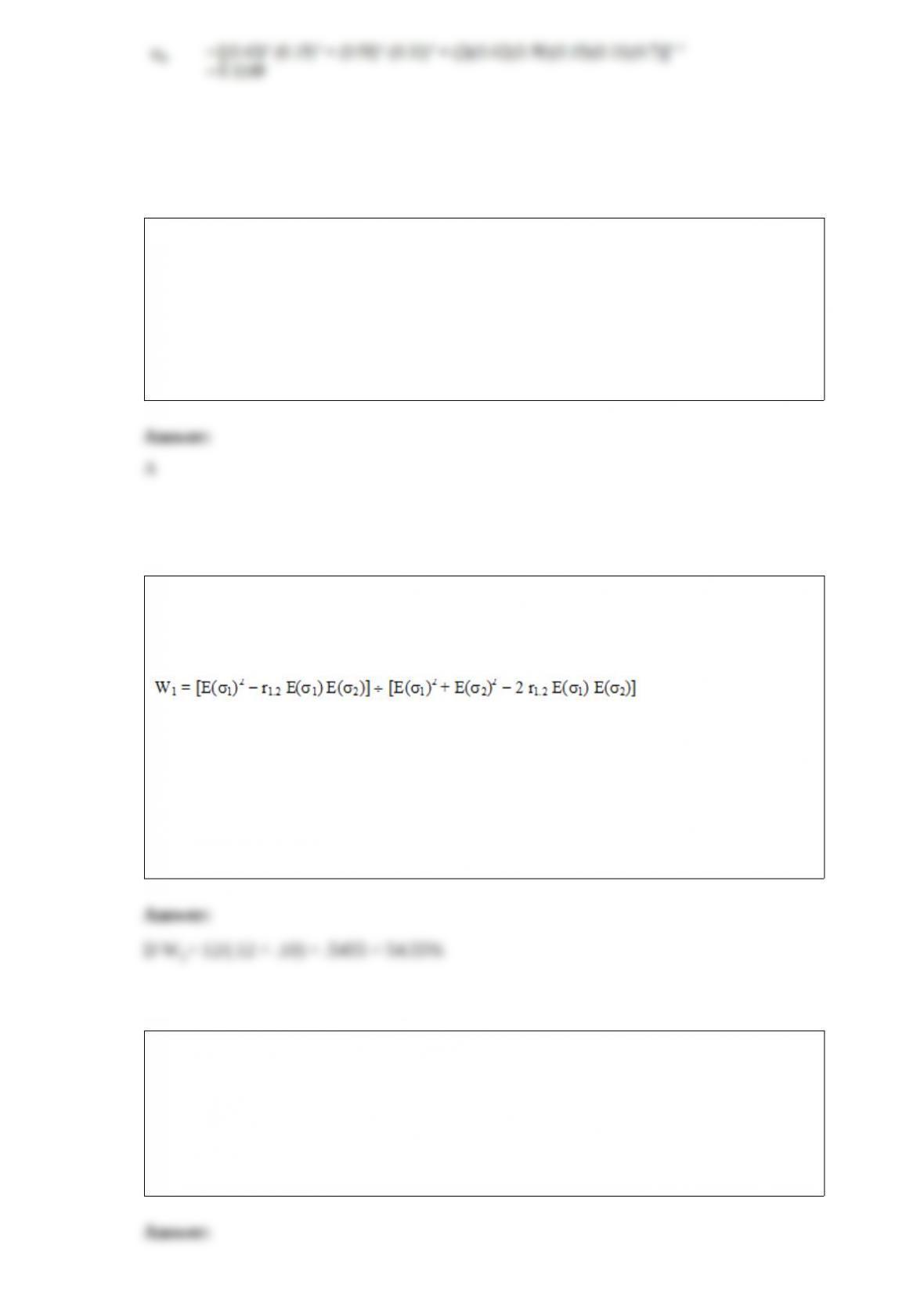

5) Exhibit 7B.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum

variance (in a two stock portfolio) is given by:

Refer to Exhibit 7B.1. What is the value of W1when r1.2= -1 and E(s1) = .10 and E(s2) =

.12?

a. 45.46%

b. 50.00%

c. 59.45%

d. 54.55%

e. 74.55%

6) What does WRF= -0.50 mean?

a. The investor can borrow money at the risk-free rate.

b. The investor can lend money at the current market rate.

c. The investor can borrow money at the current market rate.

d. The investor can borrow money at the prime rate of interest.

e. The investor can lend money at the prime rate of interest.

7) A backwardated futures market occurs when

a. F0,T< S0

b. F0,T= S0

c. F0,T> S0

d. F0,T> E( ST)

e. F0,T> ST

8) If the price before yields changed was $975, what is the resulting price?

a. $937.46

b. $918.66

c. $965.55

d. $898.62

e. $1012.45

9) If the return increases as more global investments with low correlation are added to

the market portfolio, the efficient frontier moves

a. Up and right.

b. Up and left.

c. Down and right.

d. Down and left.

e. Up only.

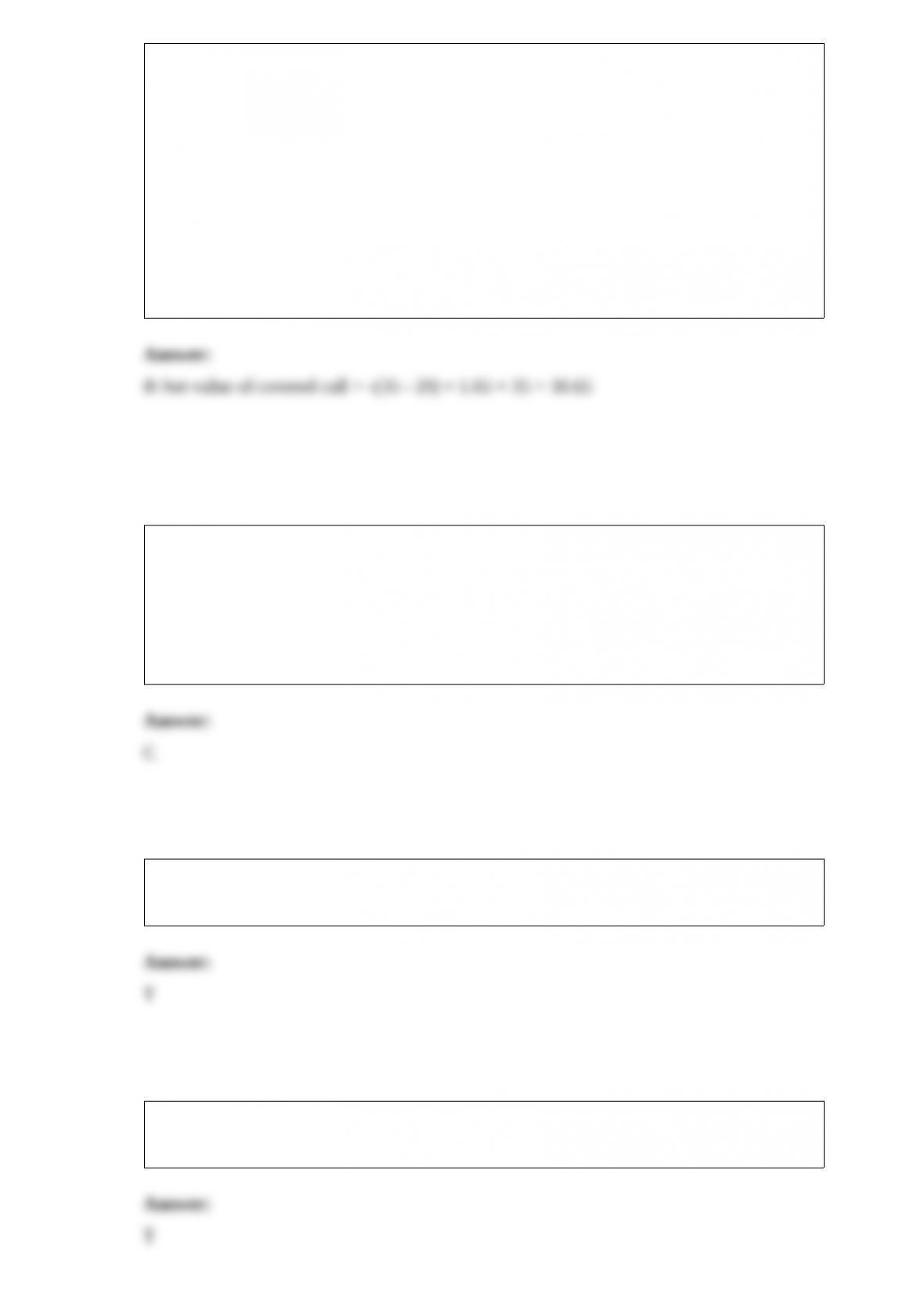

10) Exhibit 22.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

GE Corporation has a put option selling for $2.90 and a call option selling for $1.95,

both with a strike price of $29.00.

What would the net value of a covered call position be if the stock price at expiration is

$35?

a. $29.00

b. $30.65

c. $33.55

d. $36.00

e. $36.65

11) The closed-end fund index is

a. Value weighted and based on market values.

b. Value weighted and based on NAVs.

c. Price weighted and based on market values.

d. Price weighted and based on NAVs.

e. Equally weighted and based on market values.

12) Stock index futures are useful in providing a hedge against movements in an

underlying financial asset.

13) If the aggregate market is rising, but the breadth index is declining, it is a bearish

signal.

14) In tests of the semistrong-form EMH, it is not necessary to use risk-adjusted rates of

return.

15) Forward contracts do not require an upfront premium.

16) A two for one stock split causes the divisor in a price-weighted series to decline.

17) The initial value of a future contract is the price agreed upon in the contract.

18) Active equity portfolio management is a long-term buy-and-hold strategy.

19) The binomial option pricing model and the Black and Scholes model are similar

because they are both discrete models.