All off-balance-sheet items will eventually move on to the balance sheet at some point

in time.

Answer:

Under Basel III, banks are allowed to use their internal estimates of borrower

creditworthiness to assess credit risk subject to strict disclosure standards.

Answer:

As interest rates rise, the duration of a consol bond decreases.

Answer:

A fully integrated universal bank allows a bank to engage in securities activities only

through a separately owned securities affiliate.

Answer:

Mutual fund share distributions and transactions are supervised and cleared by the

National Association of Securities Dealers (NASD).

Answer:

Failure to monitor the actions of firms in a timely and complete fashion after

purchasing securities in that firm exposes the investor to agency costs.

Answer:

Protecting FI insurance funds in the event of an FI failure is the responsibility of

taxpayers.

Answer:

The increased securitization of bank loans has reduced the liquidity of bank assets.

Answer:

According to Hitachi Data Systems, recovery time from system failures averages 12

hours.

Answer:

Current statistics show that the servicing fee depository institutions can earn by

securitizing through GNMA approximates 44 basis points.

Answer:

The exact interest rate to be charged on a fixed-rate loan is agreed upon by all parties at

the time the commitment is negotiated.

Answer:

An FI acting as an agent in matching savers and borrowers of funds can attain

economies of scale and provide this service more efficiently than either the saver or

borrower could on their own.

Answer:

Compared to the United States, the use of electronic methods of payment is lower in

other major developed countries.

Answer:

Commercial banks in the U.S. often are subject to several of the four regulatory

agencies.

Answer:

In the middle part of the twentieth century, large banks addressed the issue of interstate

branch banking restrictions by forming multibank holding companies with bank

subsidiaries in different states.

Answer:

Firm-specific credit risk can be eliminated by diversification.

Answer:

Income from trading activities of FIs is less important today than the traditional

activities of banks.

Answer:

The success in technologically related innovation often is dependent on changes in

regulations and regulatory procedures.

Answer:

In evaluating the risk-adjusted asset value of foreign exchange forward contracts, the

value of the current exposure can be either positive or zero.

Answer:

CRA statistical credit scoring models are very adept at capturing political risk events

such as strikes, elections, corruption, etc.

Answer:

Under Basel III, the credit risk-adjusted value of the bank’s on-balance-sheet assets can

be found by adding the products of the risk weights for each asset times the market

value of each asset.

Answer:

In a pure credit swap the FI lender makes a payment each period in exchange for the

payment of interest in any period that the borrower defaults on the loan.

Answer:

FIs participating in the fed funds market, either buying or selling, are usually able to do

so without amount or maturity restrictions.

Answer:

The book value of equity is seldom equal to the market value of equity.

Answer:

The change in economic value of a fixed-rate liability for a decrease in interest rates is

considered to be good news.

Answer:

A positive relationship is considered to exist between domestic money supply growth

and the probability of rescheduling debt.

Answer:

The greater is convexity, the more insurance a portfolio manager has against interest

rate increases and the greater potential gain from rate decreases.

Answer:

The implementation of TRUE market value accounting for FIs may have adverse

effects on small business finance and economic growth because of the hesitancy of FIs

to invest in long-term assets.

Answer:

The efficiency with which FIs provide payment services directly benefits the economy.

Answer:

Requiring higher capital ratios often is proposed as method to reduce the incentive to

take excessive risk because the moral-hazard risk-taking incentives are thought to

decrease as the amount of net worth increases.

Answer:

Mortgage-backed bonds differ from CMOs and pass-through securities in that there is

no direct link between the cash flows on the mortgages and the interest and principal

payments on the bonds.

Answer:

The growth of the commercial paper market has led to a decline in the demand for

business loans from commercial banks.

Answer:

What is the expected probability of default in year 2 of two-year maturity B-rated debt?

A. 2.83 percent.

B. 3.00 percent.

C. 4.43 percent.

D. 2.68 percent.

E. 5.00 percent.

Answer:

A naive hedge occurs when A. an FI manager wishes to use futures or other derivative

securities to hedge the entire balance sheet duration gap.

B. a cash asset is hedged on a direct dollar-for-dollar basis with a forward or futures

contract.

C. an FI reduces its interest rate or other risk exposure to the lowest possible level by

selling sufficient futures to offset the interest rate risk exposure of its whole balance

sheet.

D. an FI purchases an insurance cover to the extent of 80% of losses arising from

adverse movement in asset prices.

E. All of the above.

Answer:

By March 2008, the notational value of credit derivative products in the commercial

banking industry hit its peak at approximately $16.44 trillion. In 2012, the notational

value of these products was approximately A. $8.9 trillion.

B. $10.6 trillion.

C. $13.6 trillion.

D. $15.7 trillion.

E. $18.1 trillion.

Answer:

Who are the common buyers of credit forwards? A. Insurance companies.

B. Banks.

C. Federal Reserve.

D. Stock brokers.

E. Credit unions.

Answer:

Why do spreads on HLT loans behave more like investment-grade bonds than like

high-yield bonds? A. They tend to be more junior in bankruptcy.

B. They tend to have greater collateral backing than do high-yield bonds.

C. Because no bank makes a market in this debt.

D. Because securities firms do not make a market in this debt.

E. They tend to have no covenant protection.

Answer:

If a US bank has variable-rate assets in US dollars and fixed-rate liabilities in Euros, the

bank is exposed to A. interest rate increases and an appreciation of the dollar.

B. interest rate declines and an appreciation of the dollar.

C. interest rate increases and a depreciation of the dollar.

D. interest rate declines and a depreciation of the dollar.

E. zero exposure to interest rate and exchange rate exposures.

Answer:

Which of the following securities is most unlikely to have a symmetrical return

distribution, making the use of RiskMetrics model inappropriate? A. Common stock.

B. Preferred stock.

C. Option contracts.

D. Consol bonds.

E. 30-year U.S. Treasury bonds.

Answer:

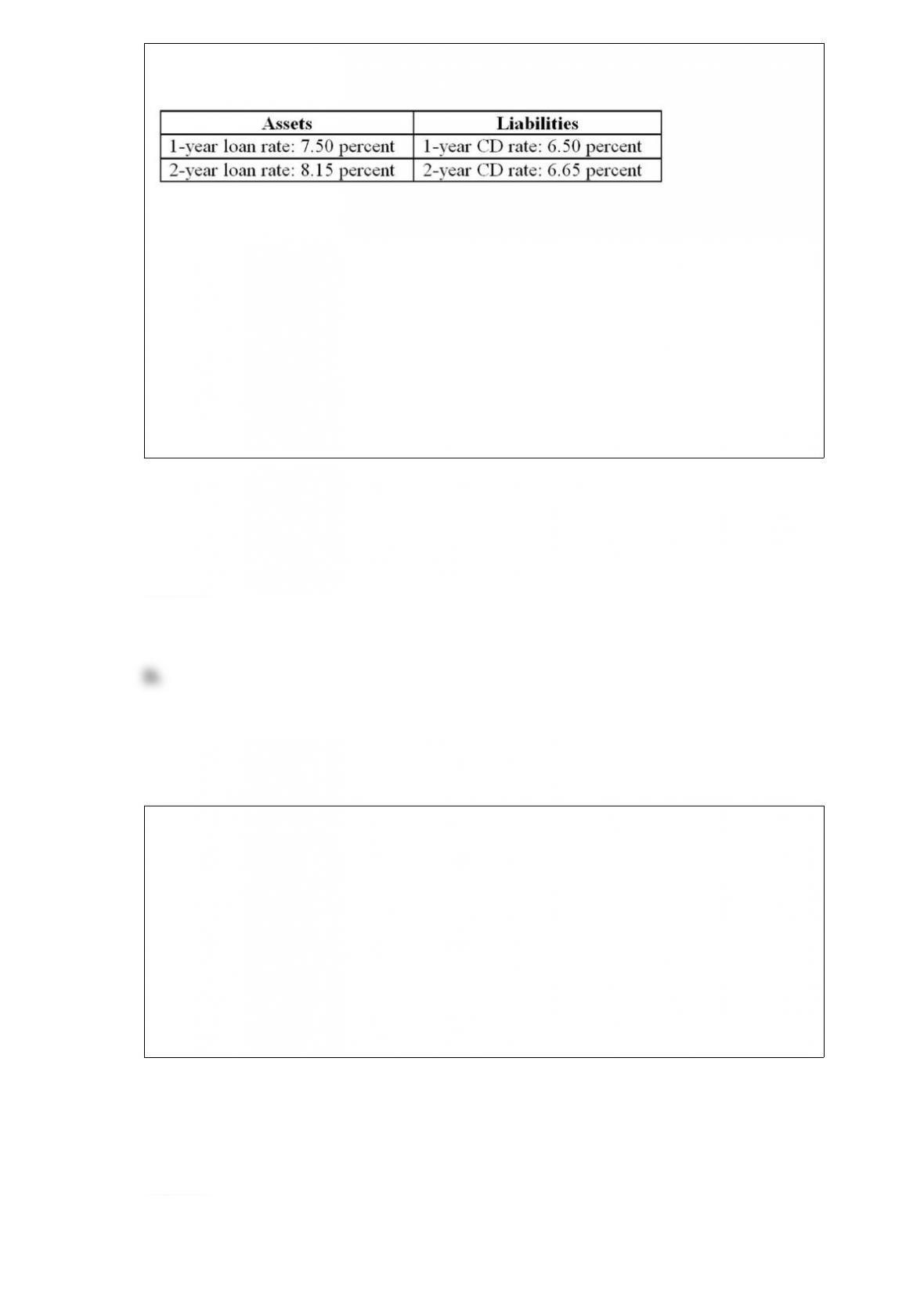

The following information is about current spot rates for Second Duration Savings’

assets (loans) and liabilities (CDs). All interest rates are fixed and paid annually.

If rates do not

change, the balance sheet position that maximizes the FI’s returns is A. a positive

spread of 15 basis points by selling 1-year CDs to finance 2-year CDs.

B. a positive spread of 100 basis points by selling 1-year CDs to finance 1-year loans.

C. a positive spread of 85 basis points by financing the purchase of a 1-year loan with a

2-year CD.

D. a positive spread of 165 basis points by selling 1-year CDs to finance 2-year loans.

E. a positive spread of 150 basis points by selling 2-year CDs to finance 2-year loans.

Answer:

The largest asset class on credit unions’ balance sheet as of September 30, 2012 was A.

cash.

B. investment securities.

C. home mortgages.

D. checkable deposits.

E. consumer credit.

Answer:

As with other DIs, profits or return on assets (ROA) is the primary goal of credit union

management.

Answer:

How could insurance companies get around the restrictive provisions imposed by the

bank holding company act of 1956? A. Through the organizational mechanism of

establishing nonbank bank subsidiaries.

B. By opening federally chartered thrifts.

C. By offering credit-related life, accident, health, or unemployment loans.

D. By buying a full-service bank and then divesting its demand deposits or commercial

loans.

E. Answers A and D only.

Answer:

Besides reducing credit risks, an FI has an incentive to sell loans it originates for all of

the following reasons EXCEPT to: A. geographically diversify.

B. decrease core deposits.

C. lower reserve requirements.

D. lower capital requirements.

E. generate reinvestment income.

Answer:

On further analysis, it is estimated that the project has a finite life of 5 years, i.e. further

investment will be required to generate the same savings. Should they undertake the

project if they assume a five-year horizon for evaluating the project? A. Yes, because

the NPV of the project is $500,000.

B. Yes, because the NPV of the project is $342,016.

C. No, because the NPV of the project is -$500,000.

D. No, because the NPV of the project is -$201,458.

E. No, because the IRR of the project is greater than 15 percent.

Answer:

An increase in interest rates A. increases the market value of the FI’s financial assets

and liabilities.

B. decreases the market value of the FI’s financial assets and liabilities.

C. decreases the book value of the FI’s financial assets and liabilities.

D. increases the book value of the FI’s financial assets and liabilities.

E. has no impact on the market value of the FI’s financial assets and liabilities.

Answer:

FIs perform their intermediary function in two ways A. they specialize as brokers

between savers and users.

B. they serve as asset transformers by purchasing primary securities and issuing

secondary securities.

C. they serve as asset transformers by purchasing secondary securities and issuing

primary securities.

D. Answers A and B.

E. Answers A and C.

Answer:

The least cost resolution strategy of FDICIA requires failure resolution alternatives for

all banks to be evaluated on a A. historical cost basis.

B. opportunity cost basis.

C. market value basis.

D. present value basis.

E. replacement cost basis.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation limited the use of “too big to fail” bailouts.

Answer:

In its role as a delegated monitor, an FI A. keeps track of required interest and principal

payments on loans it originates.

B. works with financially distressed borrowers in danger of defaulting on their loans.

C. holds portfolios of loans that they continue to service.

D. maintains contact with borrowers to ensure that loan proceeds are utilized for

intended purposes.

E. All of the above.

Answer:

Is the bank adequately capitalized for its on-balance-sheet assets based on the Basel

standards? A. Yes, because both Tier I and Tier II capital each exceed the required

minimum.

B. Yes, because both the Tier I and Tier II combined exceeds the required minimum.

C. No, because both Tier I and Tier II capital each are below the required minimum.

D. No, because Tier I is below the required minimum while Tier II exceeds the

required minimum.

E. No, because Tier I is above the required minimum while Tier II is below the

required minimum.

Answer:

The Basel II Accord effective at year-end 2007 in the United StatesA. includes

provisions covering minimum capital requirements for credit, market, and interest rate

risk.

B. stresses the regulatory supervisory process by requiring regulators to be more

involved in evaluating the bank’s specific risk profile and environment.

C. requires only banks on the regulatory problem bank list to disclose publicly the

degree and depth of problem issues as well as their capital adequacy.

D. All of the above.

E. Answers B and C only.

Answer:

Which of the following is NOT a factor that may cause the prepayment risk on a pool of

mortgages to differ from the PSA’s assumed pattern? A. The age of the mortgage pool.

B. Geographic location.

C. Seasons in the year in which the mortgage was originated.

D. Full or partial amortization of the payments.

E. Assumability of mortgages in the pool.

Answer:

What can you conclude about the cost structure of the market consisting of the two FIs?

A. There are significant economies of scale because both companies A and B coexist in

the industry.

B. There are no significant economies of scale because company A is much larger than

company B.

C. There are no significant economies of scale because the unit costs are constant.

D. There are significant economies of scale because the unit costs decline as size

increases.

E. There are no significant economies of scale because the unit costs increase as size

increases.

Answer:

Which of the following methods was NOT a method used to replenish the FDIC’s

deposit insurance reserve fund during the most recent financial crisis? A. A special

assessment was imposed on participating FIs in early 2009.

B. Individual depositor insurance coverage was increased to $250,000.

C. Deposit insurance premiums were increased.

D. Participating institutions were required to pre-pay insurance premiums.

E. A special assessment was imposed on participating FIs during the fall of 2009.

Answer:

What is the change in the value of its liabilities if all interest rates decrease by 1

percent? A. Approximately $2.003 million.

B. Approximately -$2.355 million.

C. Approximately $2.697 million.

D. Approximately $2.906 million.

E. Approximately $3.211 million.

Answer:

Which of the following makes international loan rescheduling more likely than bond

rescheduling? A. International loan contracts are not allowed to contain cross-default

provisions.

B. Typically there are more FIs in an international lending syndicate compared to the

number of potential bondholders.

C. Since World War II more international debt has been in the form of bonds.

D. An international loan syndicate typically comprises the same FIs which allows

greater cohesiveness for negotiations.

E. All of the above.

Answer:

FIs are competing directly with loan commitments, one of their own OBS products,

when they also offer: A. Futures contracts.

B. Swaps.

C. Standby letters of credit.

D. Forward contracts.

E. When-issued trading.

Answer:

If a 16-year 12 percent semi-annual $100,000 T-bond, currently yielding 10 percent, is

used to deliver against a 20-year, 8 percent T-bond at 114-16/32, what is the conversion

factor? What would the buyer have to pay the seller? A. 1.158; $132,591.

B. 1.156; $115,600.

C. 1.150; $131,284.

D. 1.102; $124,200.

E. 1.000; $114,160.

Answer:

A contract whose payoff increases as a yield spread increases above some stated

exercise spread is a A. put option.

B. call option.

C. digital default option.

D. futures option.

E. credit spread call option.

Answer:

Calculate the cash flows on the above futures contract if all interest rates increase by

1.49 percent. (That is, ΔR/(1 + R) = 1.49 percent, and 1 bp = $25.) A. The long futures

position earns a profit of $3,766.39.

B. The short futures position earns a profit of $3,725.00.

C. The long futures position earns a profit of $1.49 million.

D. The short futures position earns a profit of $1.49 million.

E. The short futures position suffers a loss of $3,725.

Answer:

An investment banker agrees to underwrite an issue of 5 million shares of stock for

NetChoice, Inc. on a best-efforts basis. The investment banker is able to sell 4.5 million

shares for $31.00 per share and it charges NetChoice, Inc. $0.375 per share sold.

What is the profit to the investment banker if it is able to sell 4.5 million shares for $31

per share? A. Profit of $1,875,000.

B. Loss of $1,275,000.

C. Profit of $1,687,500.

D. Loss of $3,125,000.

E. Profit of $3,125,500.

Answer:

Which of the following is NOT a possible result when a property-liability company

purchases reinsurance?A. improved capital position.

B. limits on losses on reinsured policies.

C. stabilized cash flows.

D. dilution of earnings per share.

E. All of the above are possible results of purchasing reinsurance.

Answer:

If interest rates decrease 40 basis points (0.40 percent) for an FI that has a cumulative

gap of -$25 million, the expected change in net interest income is A. +$100,000.

B. -$100,000.

C. -$625,000.

D. -$250,000.

E. +$250,000.

Answer:

Economies of scale refer to an FI’s ability toA. lower its average costs of operations by

expanding its output of financial services.

B. generate cost synergies by producing more than one output with the same inputs.

C. understand each risk and its interaction with other risks.

D. finance its assets completely with borrowed funds.

E. moderate the long-tailed downside risk of the return distribution.

Answer:

How would you characterize the FI’s risk exposure to fluctuations in the Swiss

franc/dollar exchange rate?A. The FI is net short in the franc and therefore faces the

risk that the franc will rise in value against the U.S. dollar.

B. The FI is net short in the franc and therefore faces the risk that the franc will fall in

value against the U.S. dollar.

C. The FI is net long in the franc and therefore faces the risk that the franc will fall in

value against the U.S. dollar.

D. The FI is net long in the franc and therefore faces the risk that the franc will rise in

value against the U.S. dollar.

E. The FI has a balanced position in the Swiss franc.

Answer: