A junior colleague of yours has prepared the following pro forma to indicate his

forecasts for a firm (in millions of dollars):

The interest expense relates to bonds payable with an effective interest rate of 5% equal

to the coupon rate. The firm’s tax rate is 35%. There are no financial assets.

There are four things wrong with this pro forma. Can you spot them? (You are not

required to re-work the pro forma).

This exam comes in two parts. Part I involves an analysis of a set of financial

statements and Part II involves forecasting and valuation based on those financial

statements.

Part I: Analysis (20 Points)

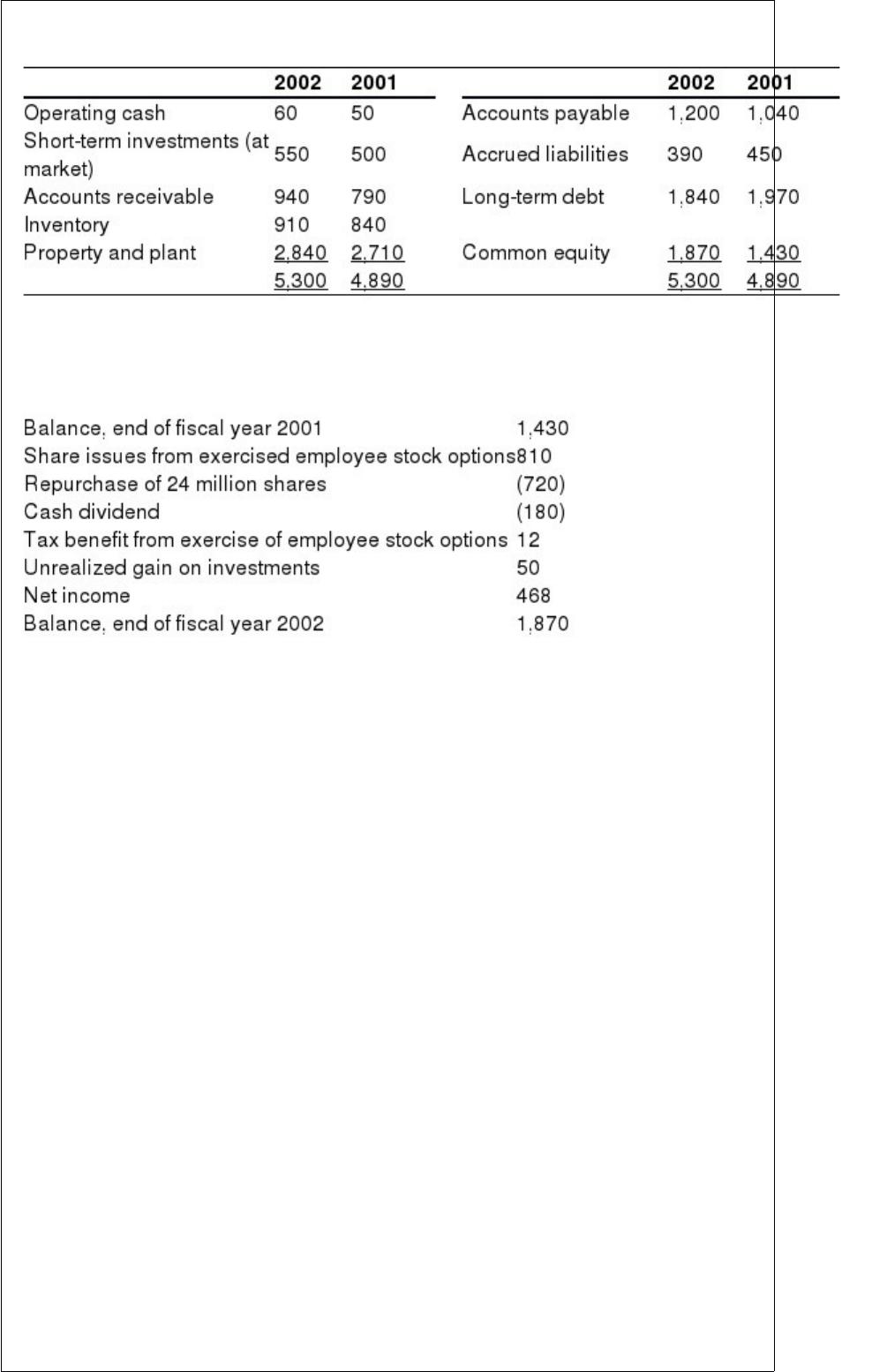

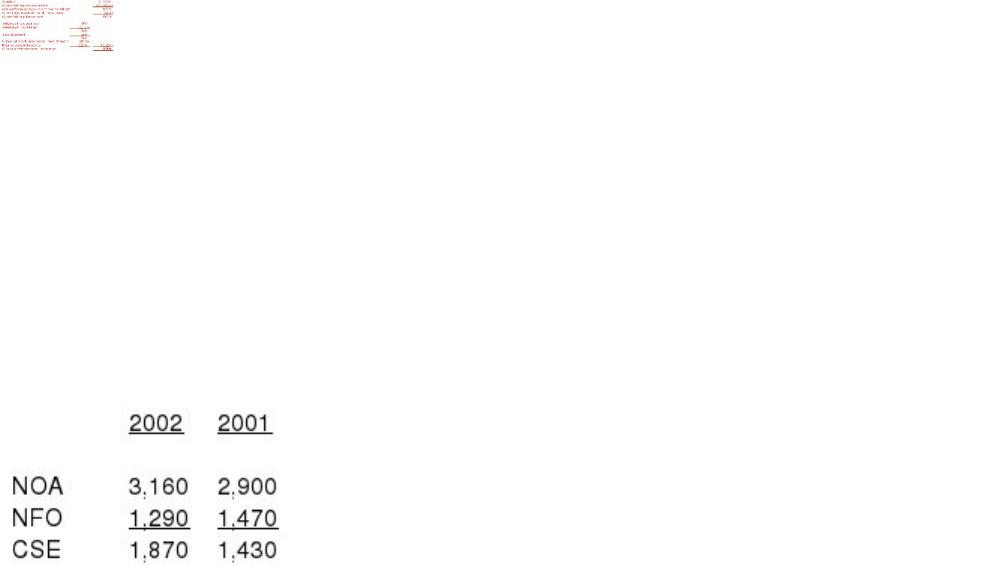

The following is a comparative balance sheet for a firm for fiscal year 2002 (in millions

of dollars):

The following is the statement of common shareholders’ equity for 2002 (in millions of

dollars):

The firm’s income tax rate is 35%. The firm reported $15 million in interest income and

$98 million in interest expense for 2002. Sales revenue was $3,726 million.

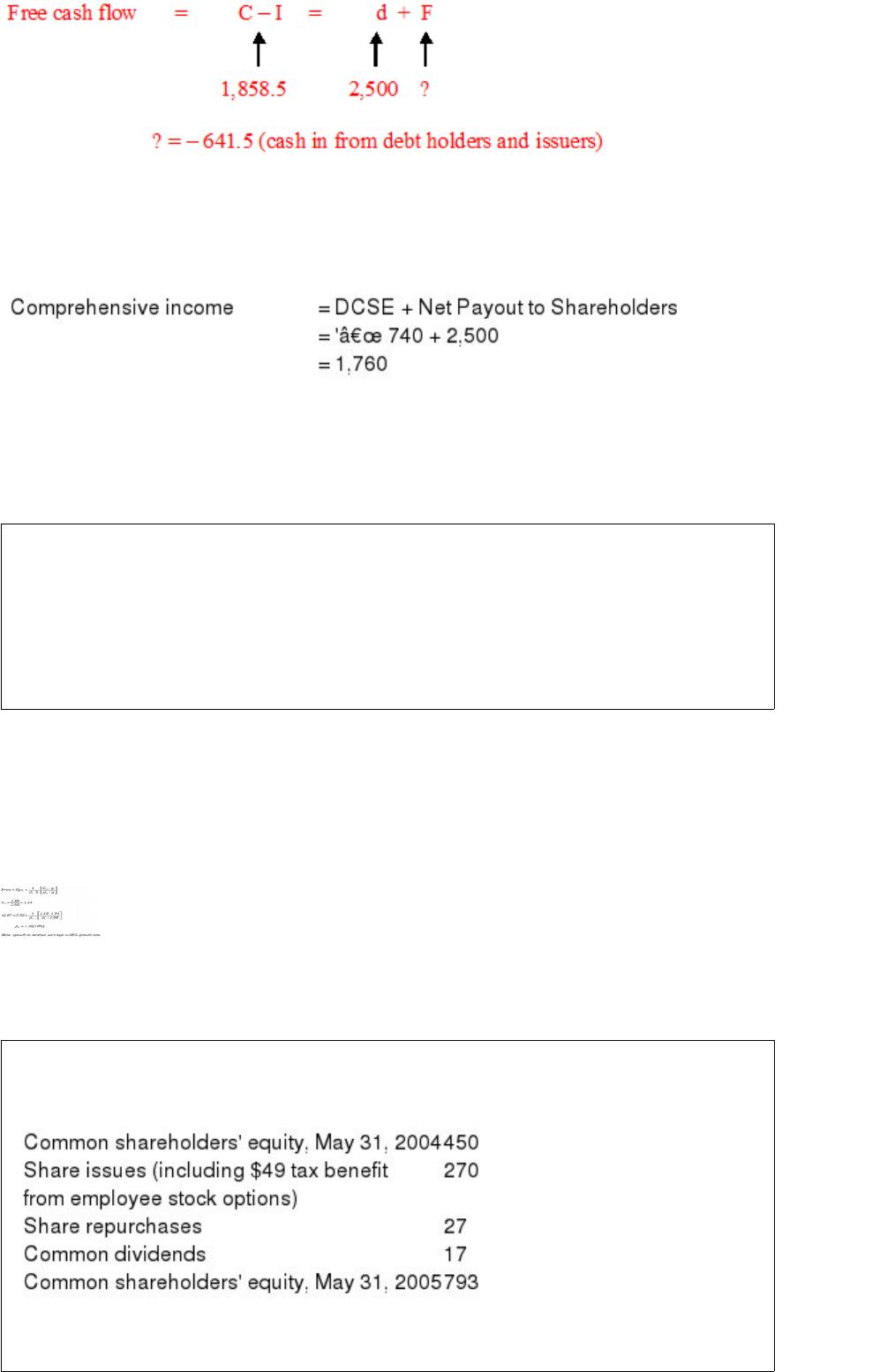

a. Calculate the loss to shareholders from the exercise of employee stock options during

2002.

b. The shares repurchased were in settlement of a forward purchase agreement. The

market price of the shares at the time of the repurchase was $25 each. What was the

effect of this transaction on the income for the shareholders?

c. Prepare a comprehensive income statement that distinguishes after-tax operating

income from financing income and expense. Include gains or losses from the

transactions in questions (a) and (b) above.

d. Prepare a reformulated comparative balance sheet that distinguishes assets and

liabilities employed in operations from those employed in financing activities. Calculate

the firms’ financial leverage and operating liability leverage at the end of 2002.

e. Calculate free cash flow for 2002.

Part II: Forecasting and Valuation (20 Points)

Use a cost of capital for operations of 9%.

Sales revenue is forecasted to grow at a 6% rate per year in the future, on a constant

asset turnover of 1.25. Operating profit margins of 14% are expected to be earned each

year.

a. Forecast return on net operating assets (RNOA) for 2003.

b. Forecast residual operating income for 2003.

c. Value the shareholders’ equity at the end of the 2002 fiscal year using residual income

methods.

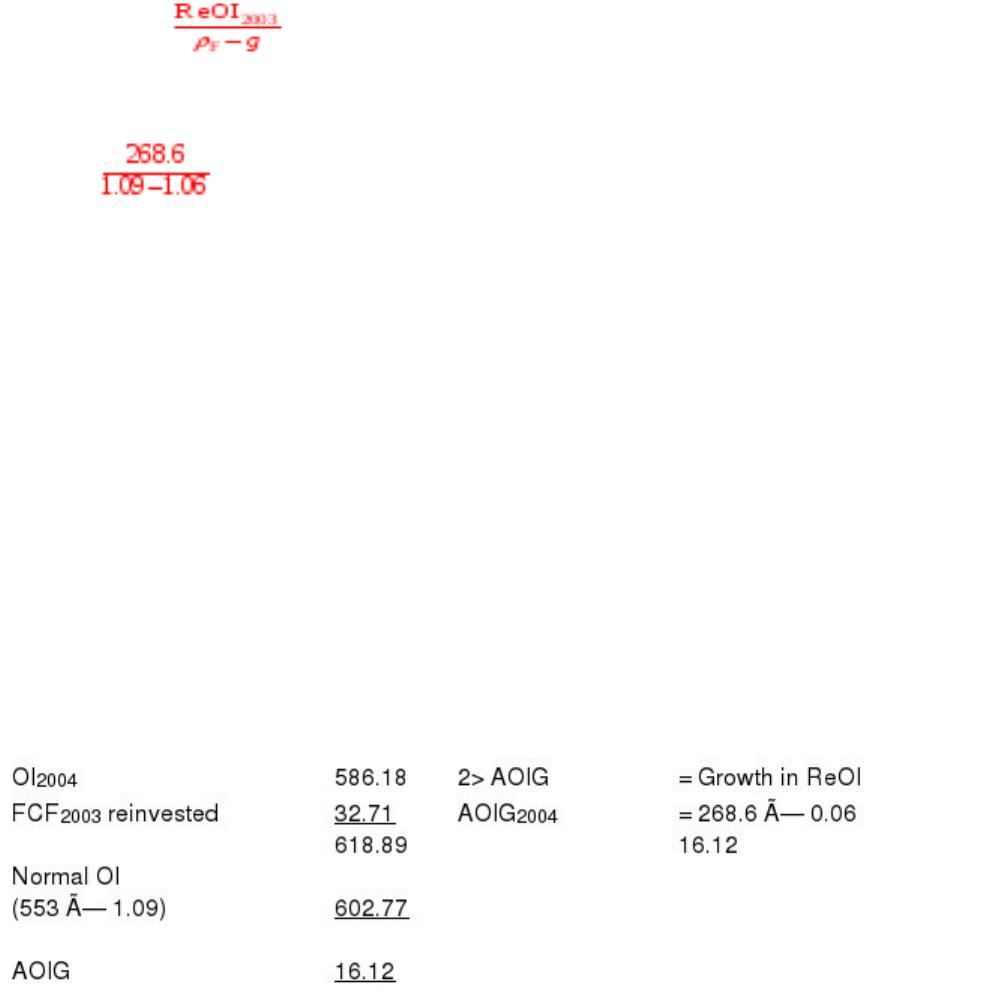

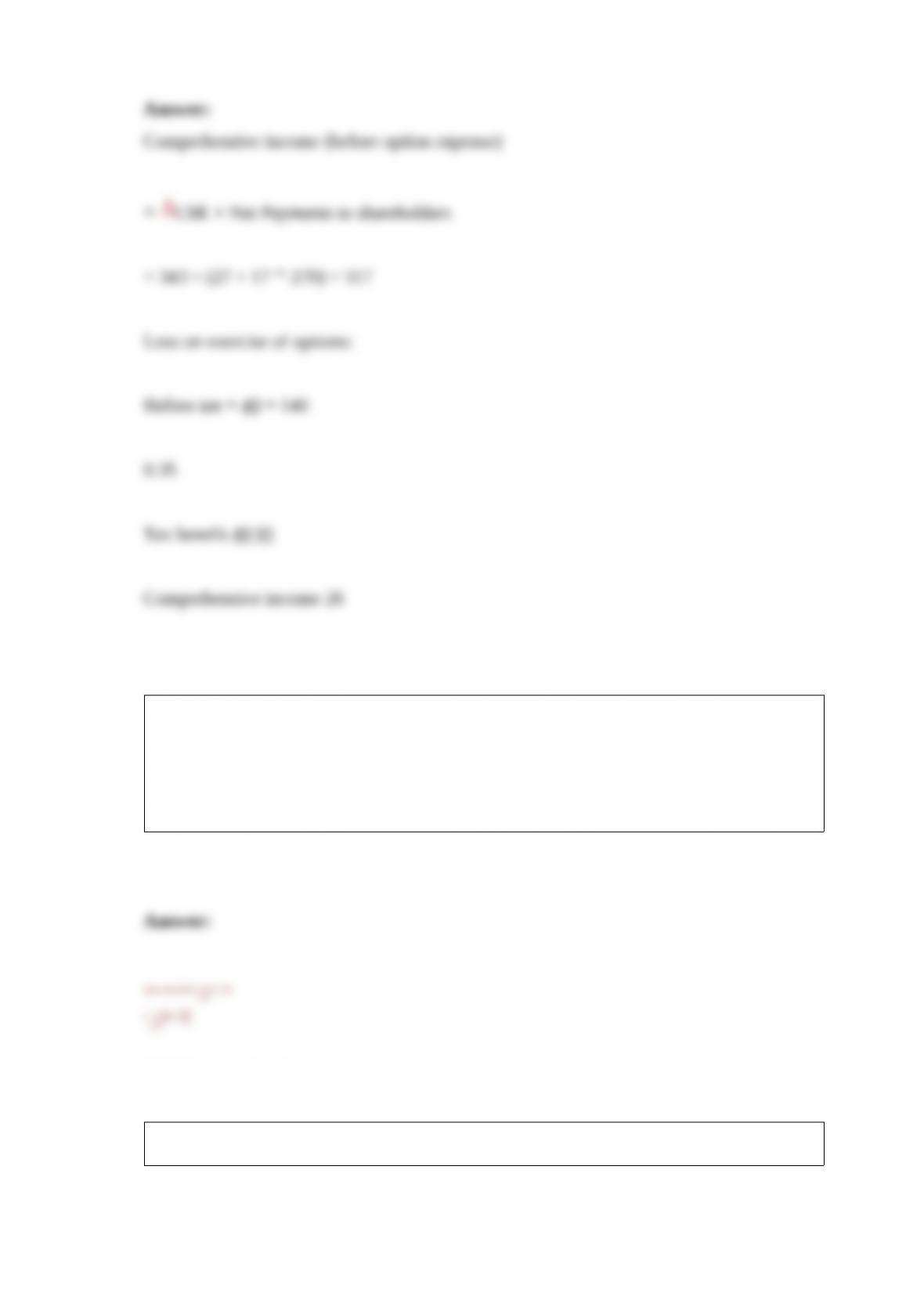

d. Forecast abnormal growth in operating income for 2004.

e. Value the shareholders’ equity at the end of 2002 using abnormal earnings growth

methods.

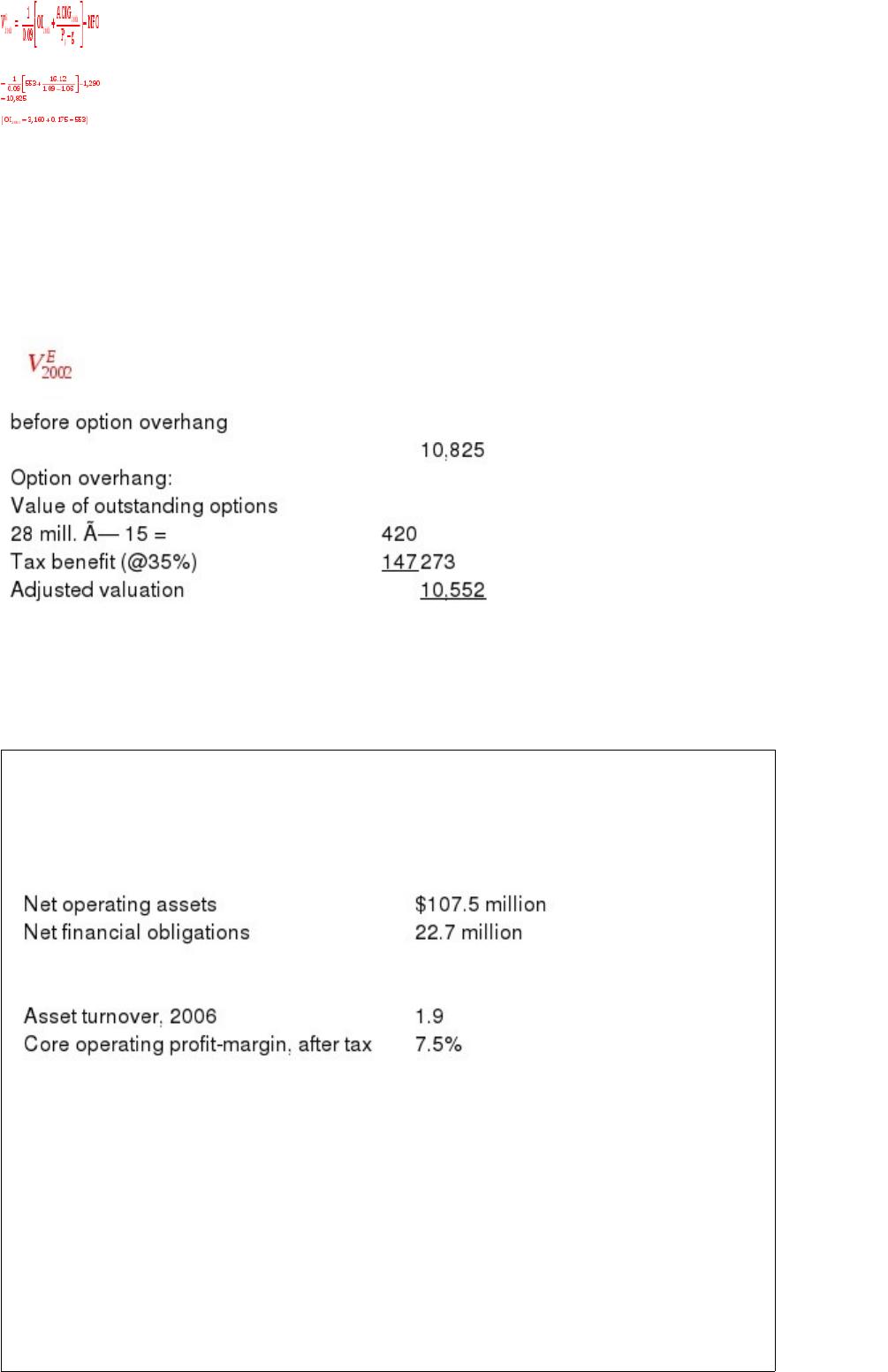

f. After reading the stock compensation footnote for this firm, you note that there are

employee stock options on 28 million shares outstanding at the end of 2002. A modified

Black-Scholes valuation of these options is $15 each. How does this information

change your valuation?

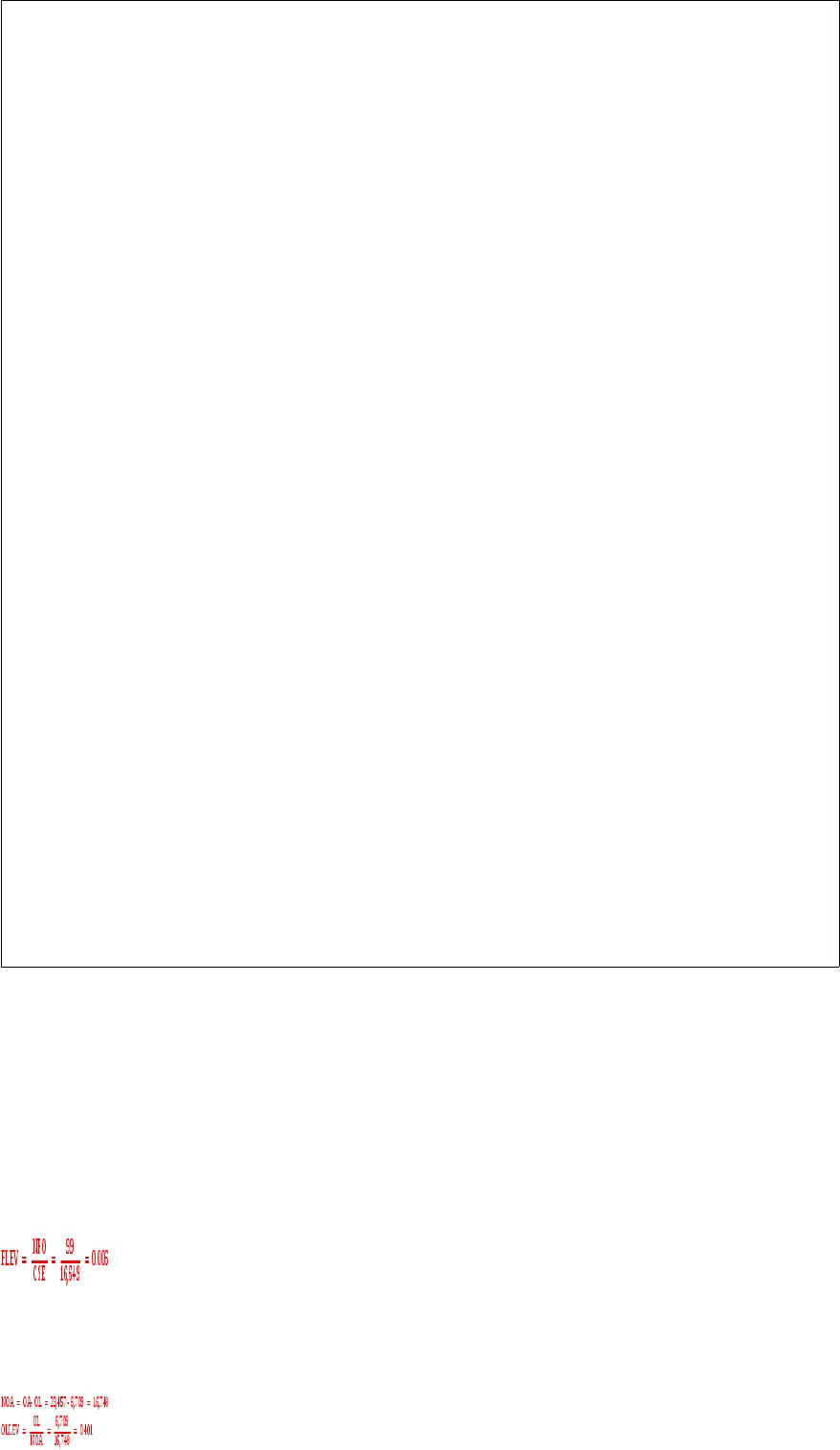

The following numbers were calculated from the financial statements of a firm for

fiscal year 2006.

(a) Calculate the core return on net operating assets for 2006.

(b) You forecast that the core profit margin and asset turnover in the future will be the

same as in 2006. You also forecast that sales will grow at 4% per year in the future. The

firm’s required return for its operations is 9%.

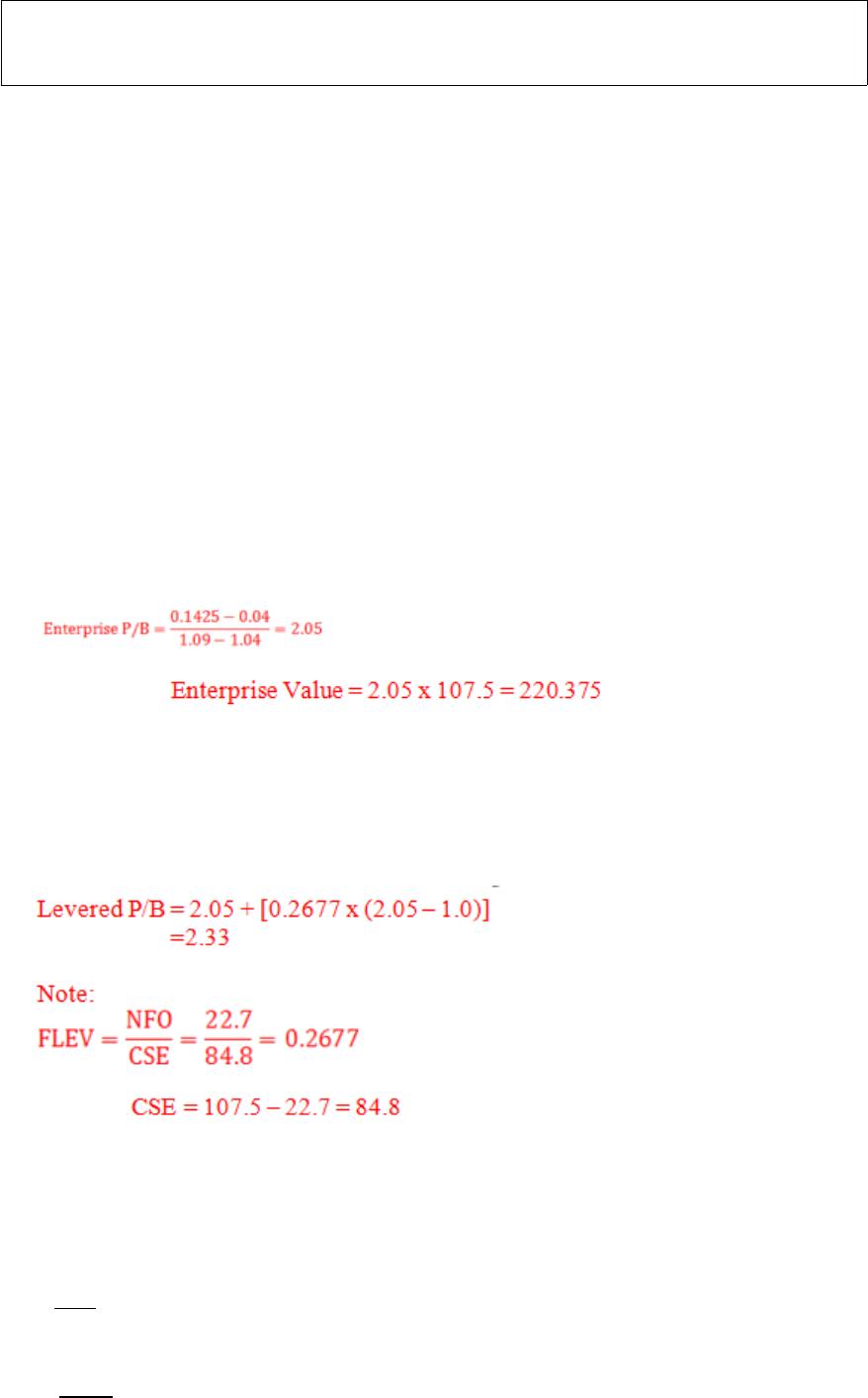

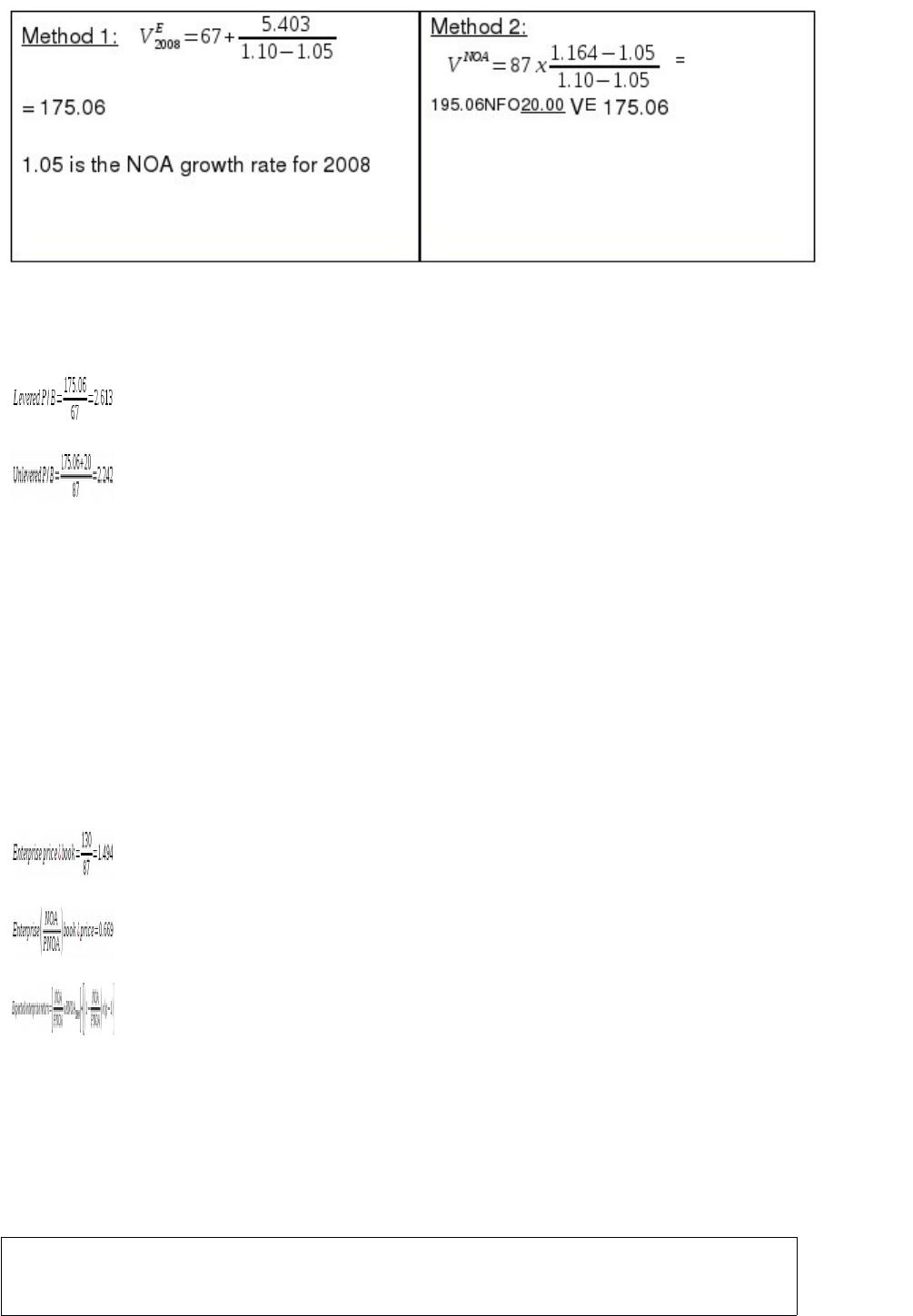

(i) Calculate the enterprise price-to-book ratio and enterprise value.

(ii) Calculate the levered price-to-book ratio.

(c) The firm’s 52 million outstanding shares are trading at $4.75 each. Given your

forecasts, what is your expected rate of return from buying the firm at this price?

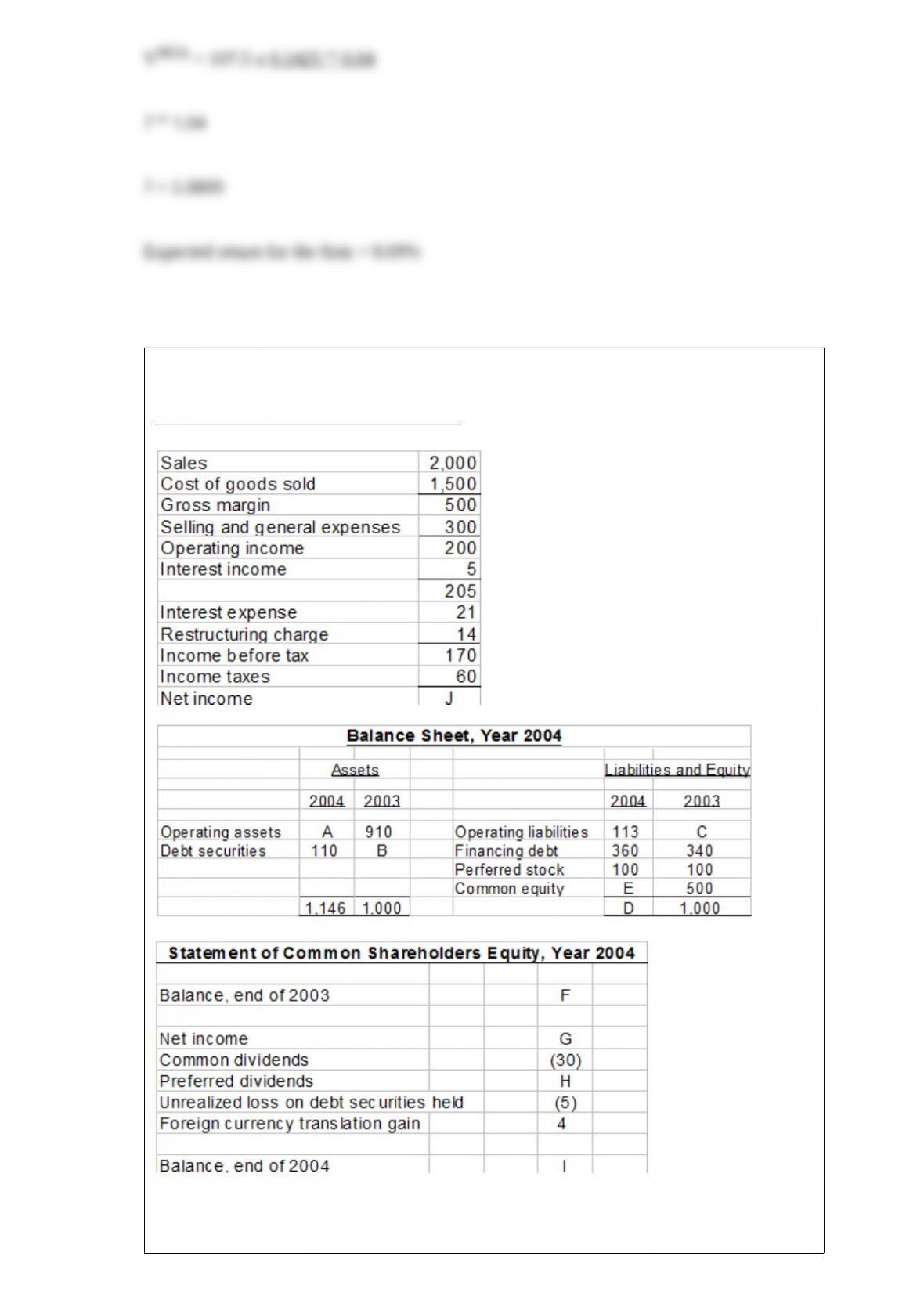

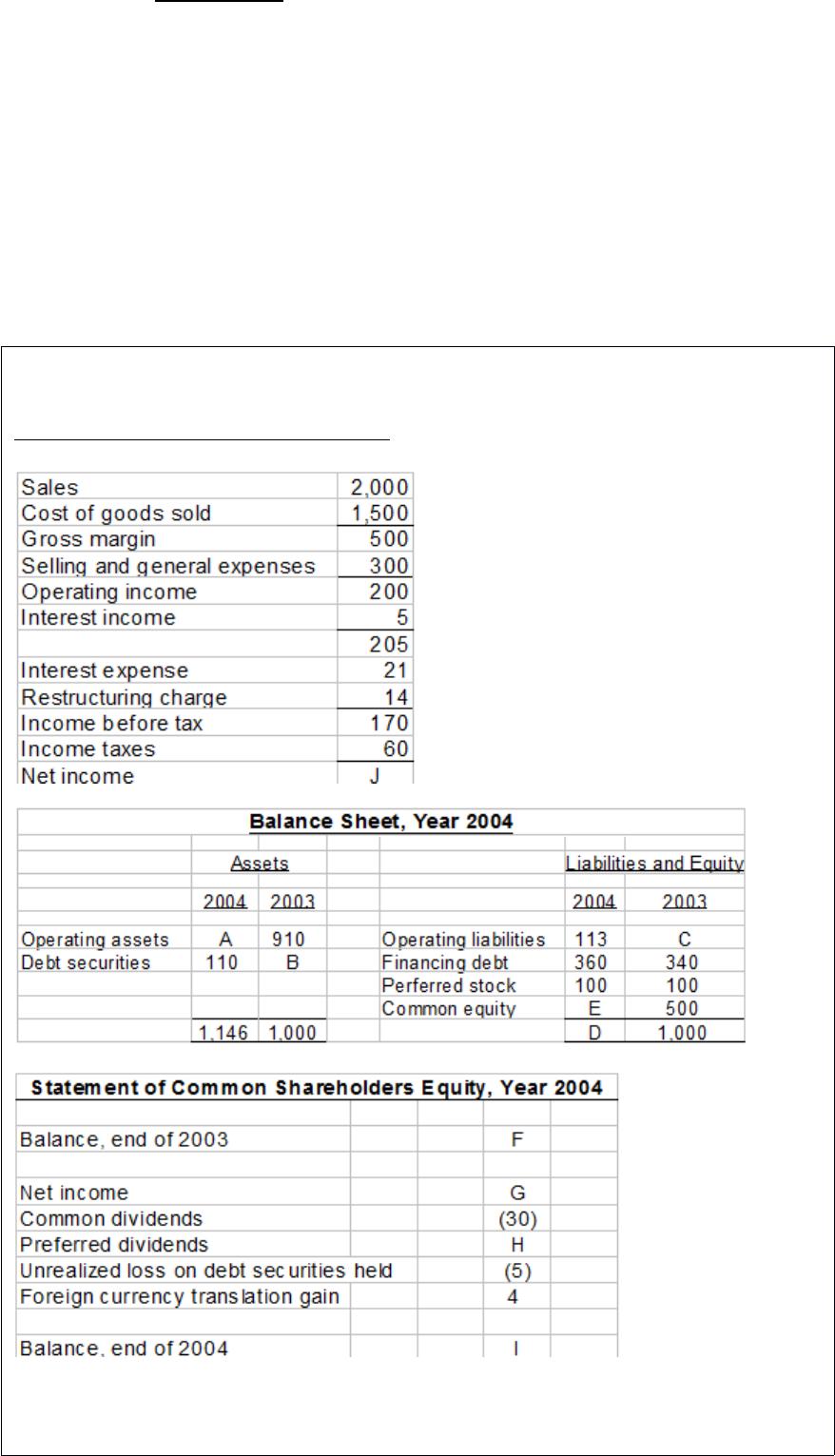

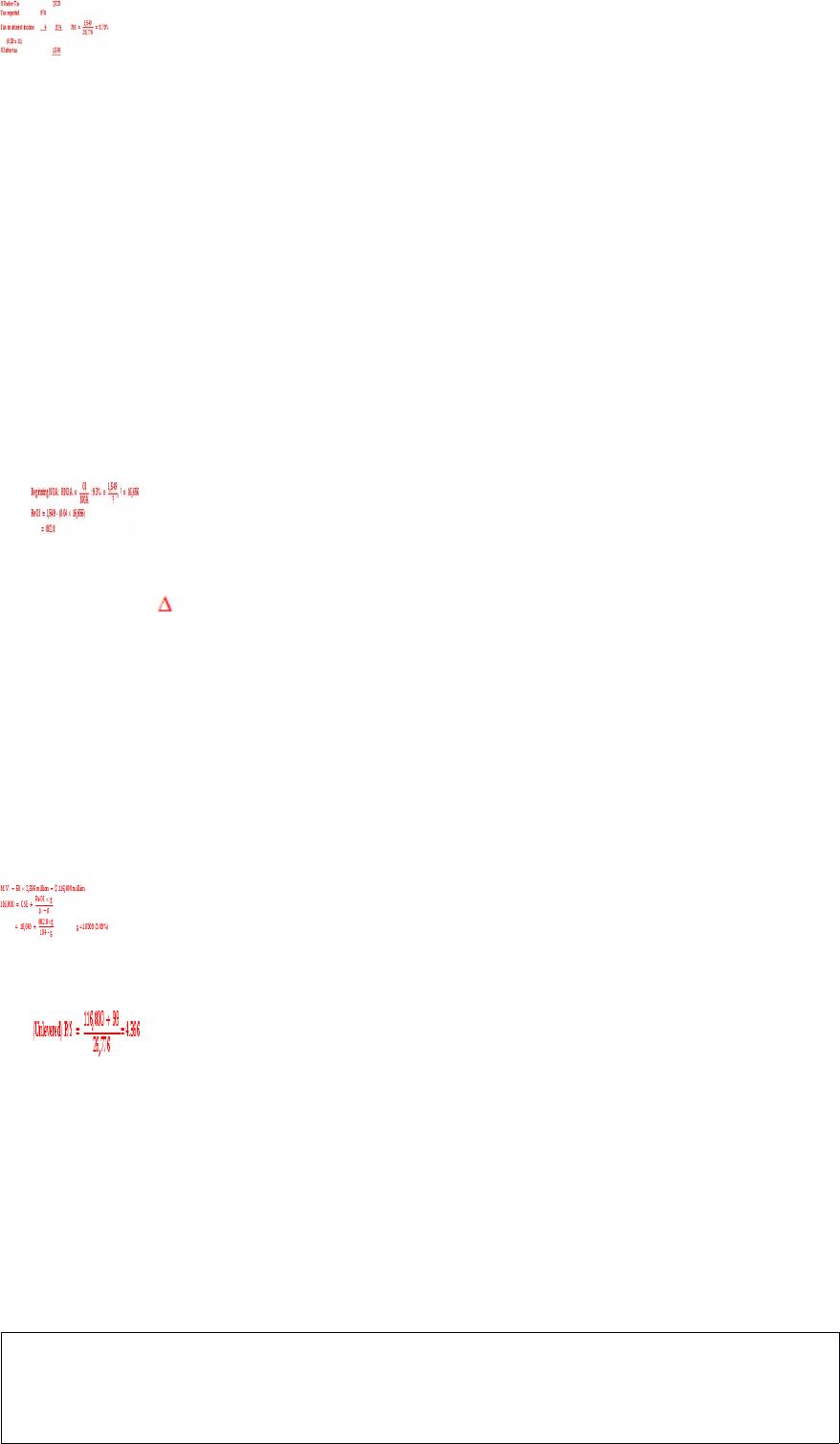

The following are partial financial statements for an industrial firm that you are

required to analyze and value. All amounts are in millions of dollars.

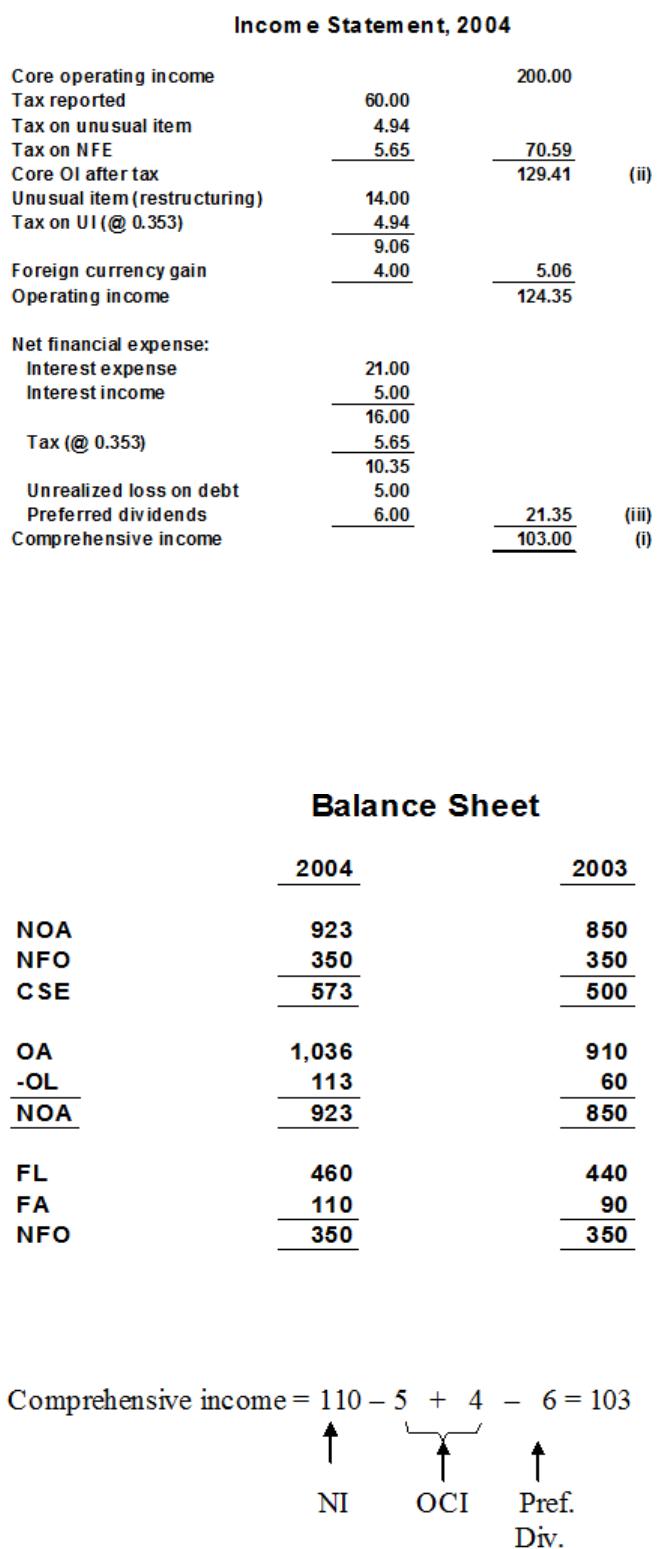

Income Statement for Fiscal Year 2004

The firm’s statutory tax rate is 35.3%.

(a.) Supply the missing numbers, A to J.

(If you are unable to calculate one of these numbers, make a reasonable guess before

proceeding to part (b) of the question.)

(b) Calculate the following for 2004. Use beginning of year balance sheet numbers in

denominators.

(i) Comprehensive income

(ii) Core operating income, after tax

(iii) Net financial expense, after tax

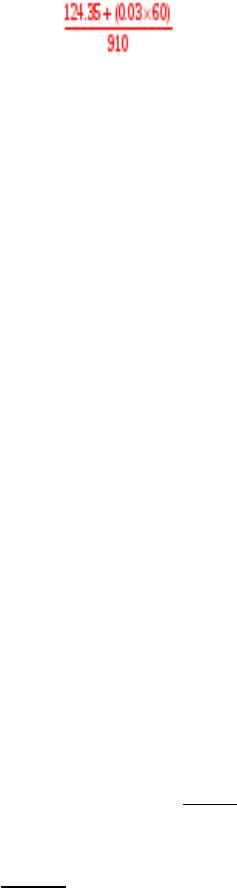

(iv) Return on net operating assets (RNOA)

(v) Core return on net operating assets (Core RNOA)

(vi) Net borrowing cost (NBC)

(vii) Free cash flow

(viii) Net payments to debt holders and debt issuers

(c) Show that the following relation holds for this firm:

ROCE = RNOA + (Financial Leverage x Operating Spread)

(d) Show that the following relation holds for this firm. Use 3% for the short-term

borrowing rate. ROOA is return on operating assets.

RNOA = ROOA + [Operating Liability Leverage x (ROOA ‘“ Short-term Borrowing

Rate)]

(e) Forecast ROCE for 2005 for the case where RNOA is expected to be the same as

core RNOA in 2004 and the net borrowing cost is expected to be the

same as in 2004.

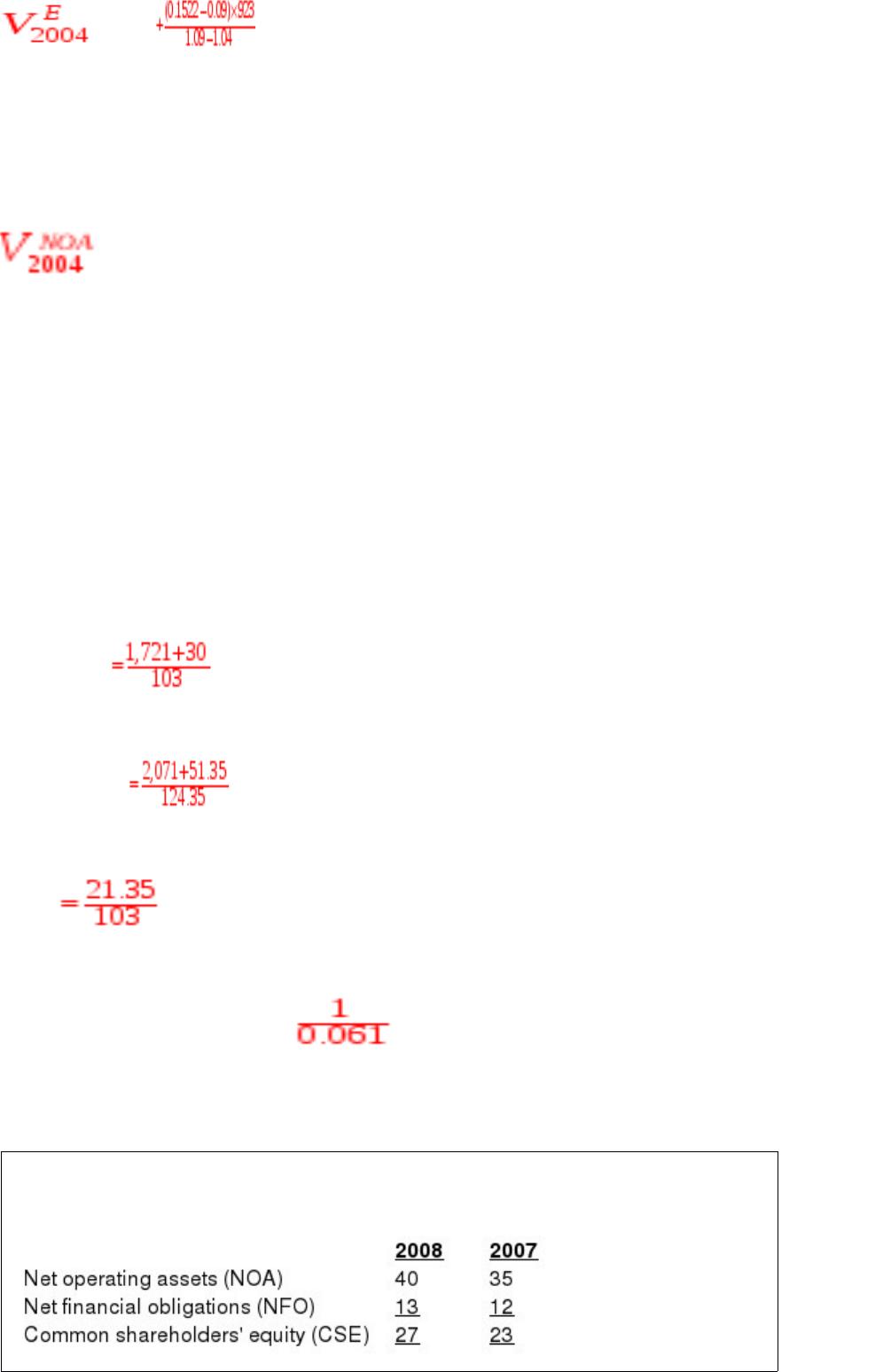

(f) Value the equity under a forecast that

(i) Return on net operating assets in the future will be the same as core

RNOA in 2004.

(ii) Sales are expected to grow at 4% per year.

(iii) Asset turnovers will be the same as in 2004.

The required return for operations is 9%.

(g) Calculate the intrinsic levered price-to-book ratio and enterprise price-to-book and

show that the two are related in the following way:

Levered P/B = Enterprise P/B + [Financial Leverage × (Enterprise P/B ‘“ 1)]

(h) Calculate the intrinsic trailing levered P/E and the trailing enterprise P/E. Show that

the two are related in the following way:

Levered P/E = Enterprise P/E + [Earnings Leverage × (Enterprise P/E ‘“ 1/NBC ‘“ 1)]

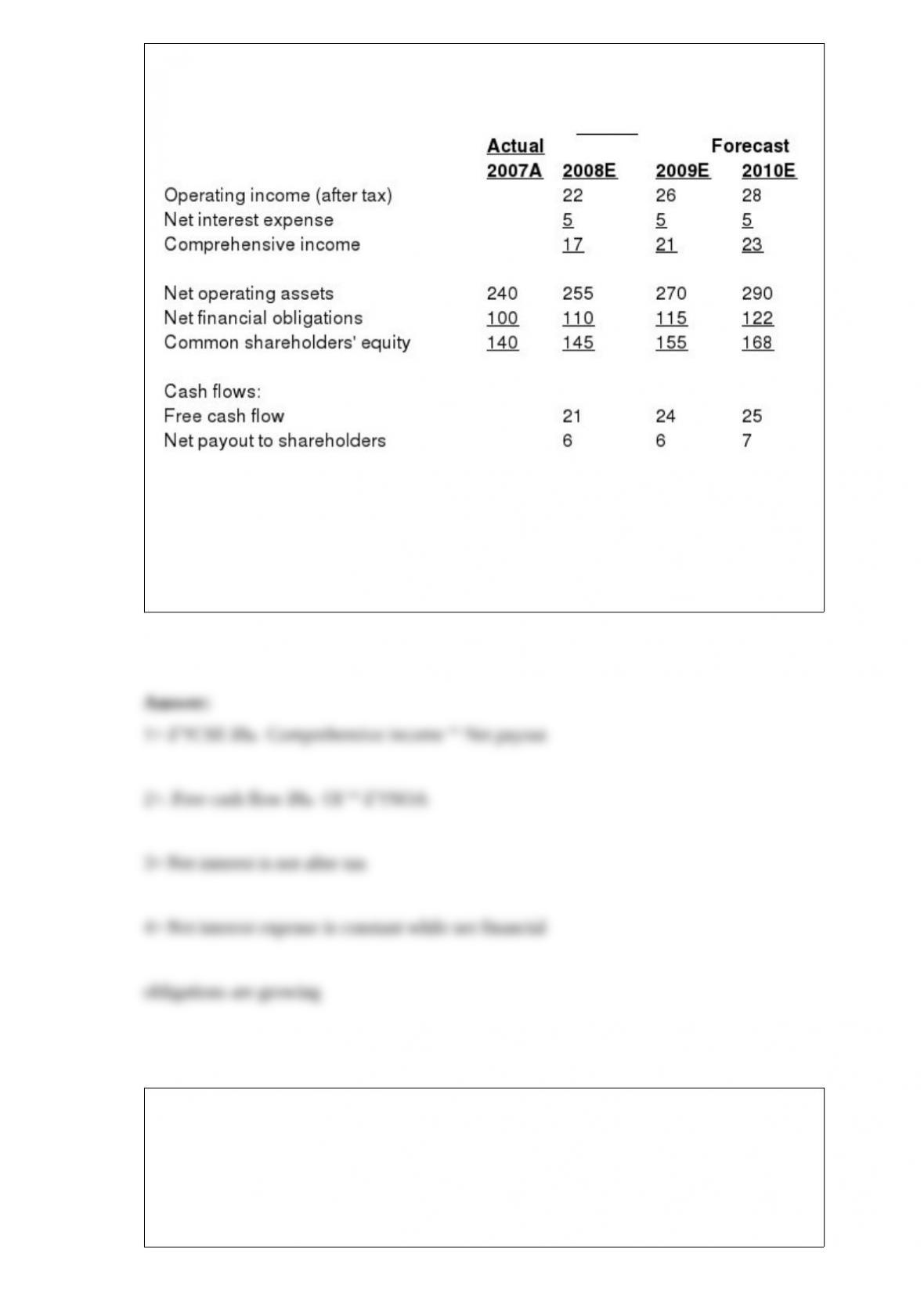

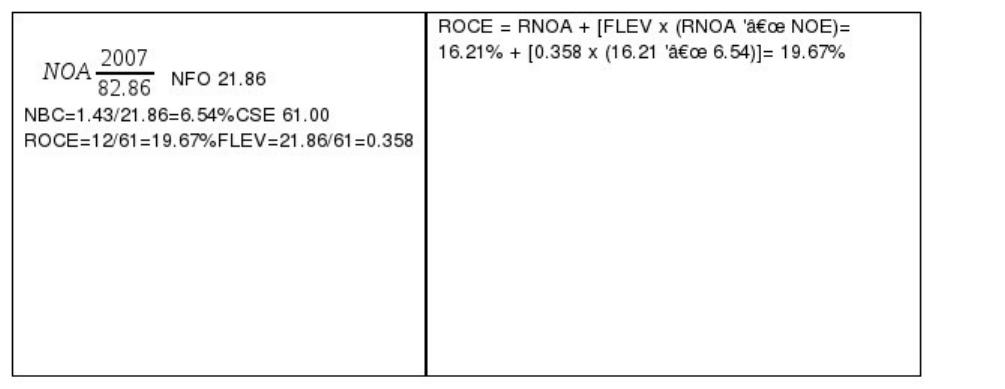

The following summarizes reformulated balance sheets at the end of fiscal years 2008

and 2007 (in millions of dollars):

Comprehensive income for 2008 was $7 million.

Free cash flow for 2008 was $3 million.

(a) What was operating income (after tax) for 2008?

(b) What was net financial expense (after tax) for 2008?

(c) What was the net payment to shareholders?

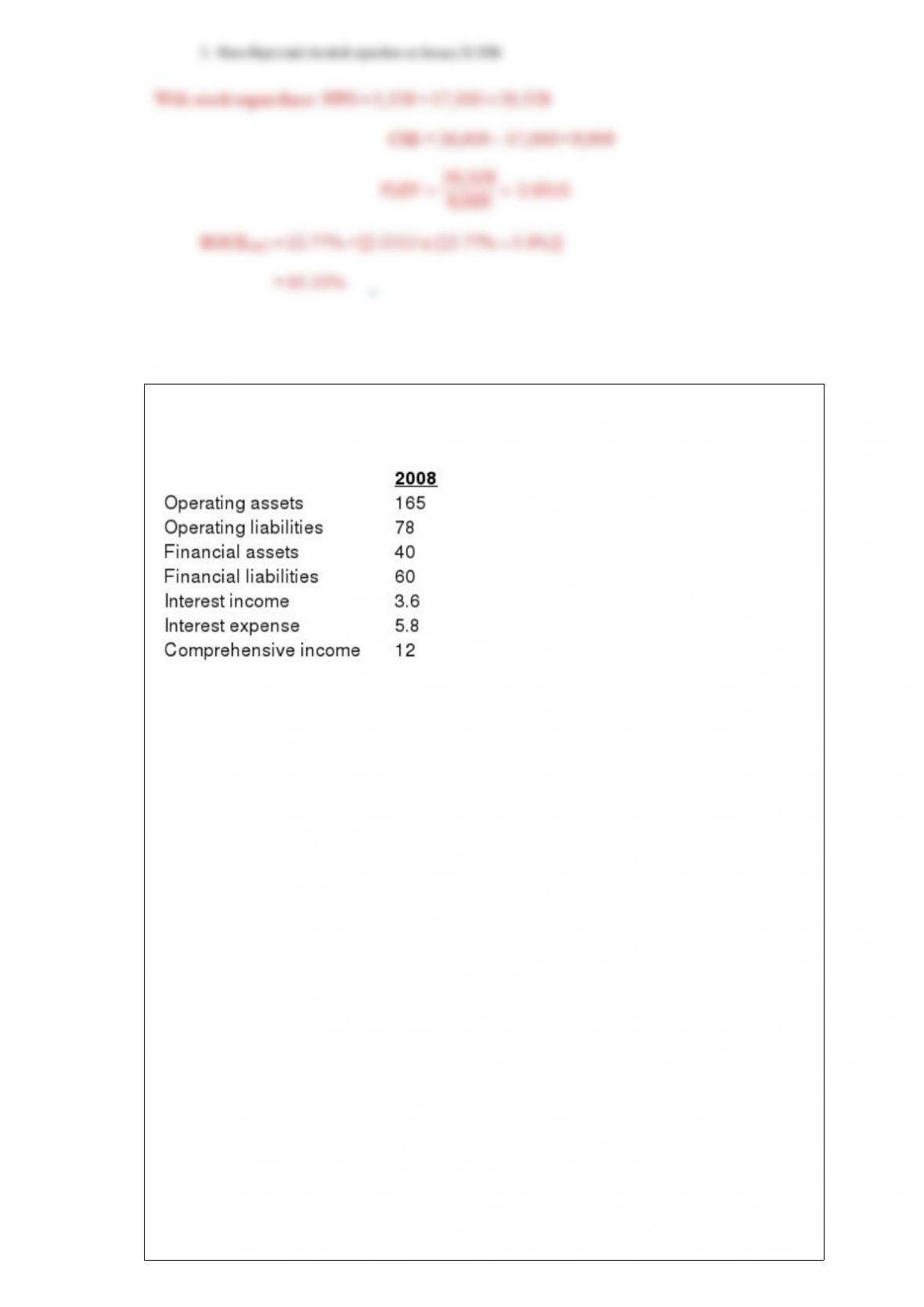

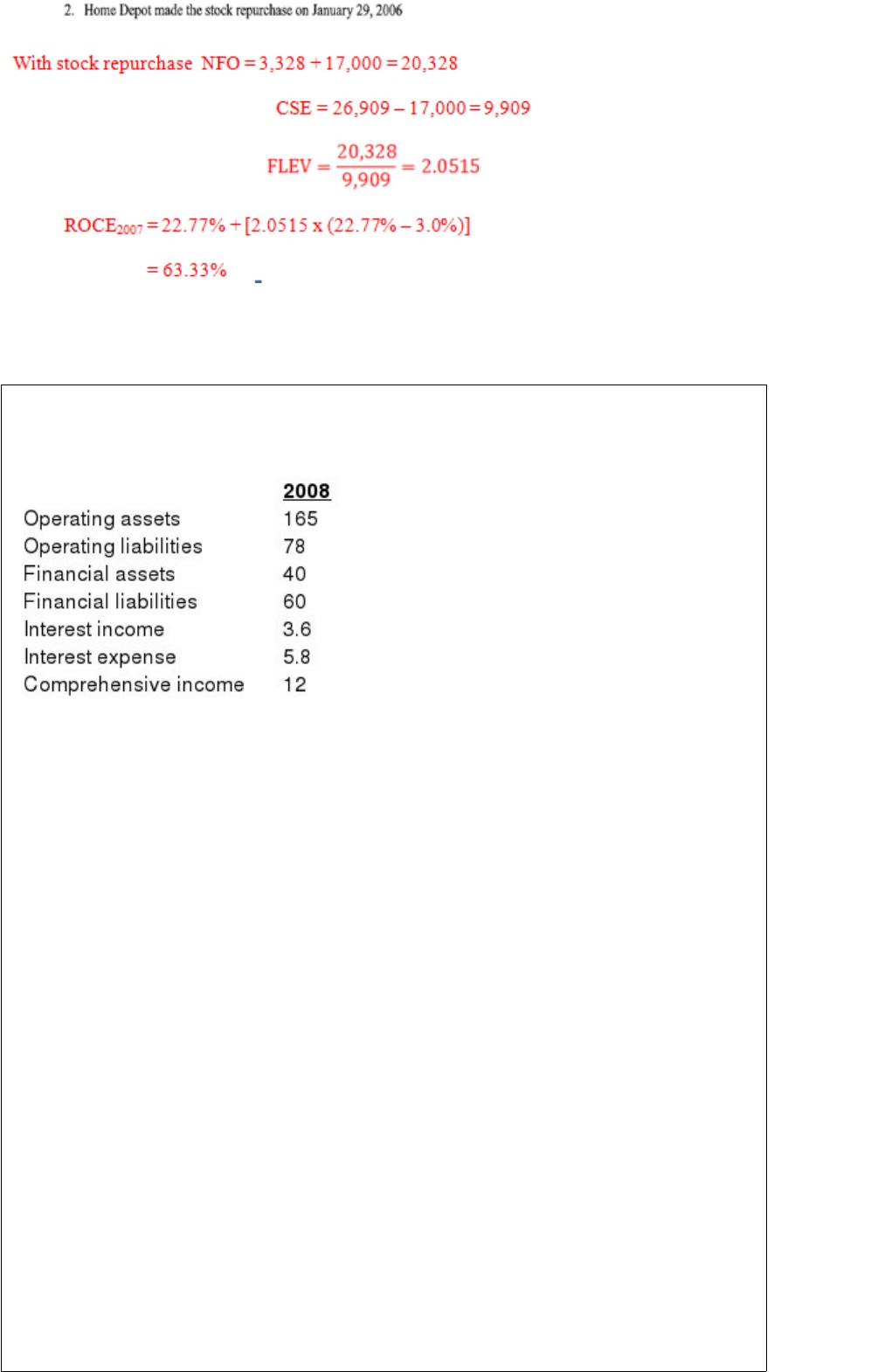

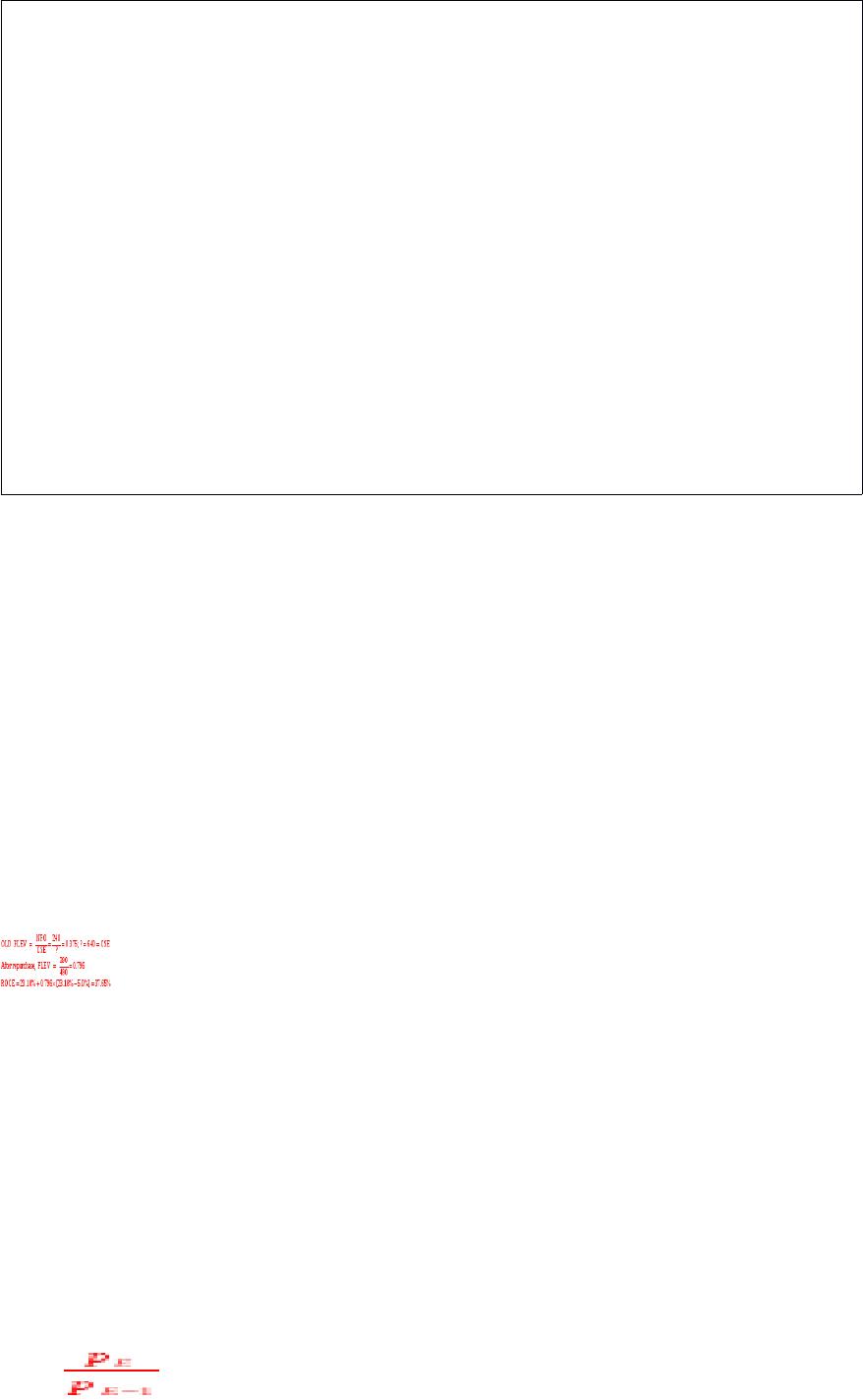

The following are summaries from financial statements for the warehouse retailer,

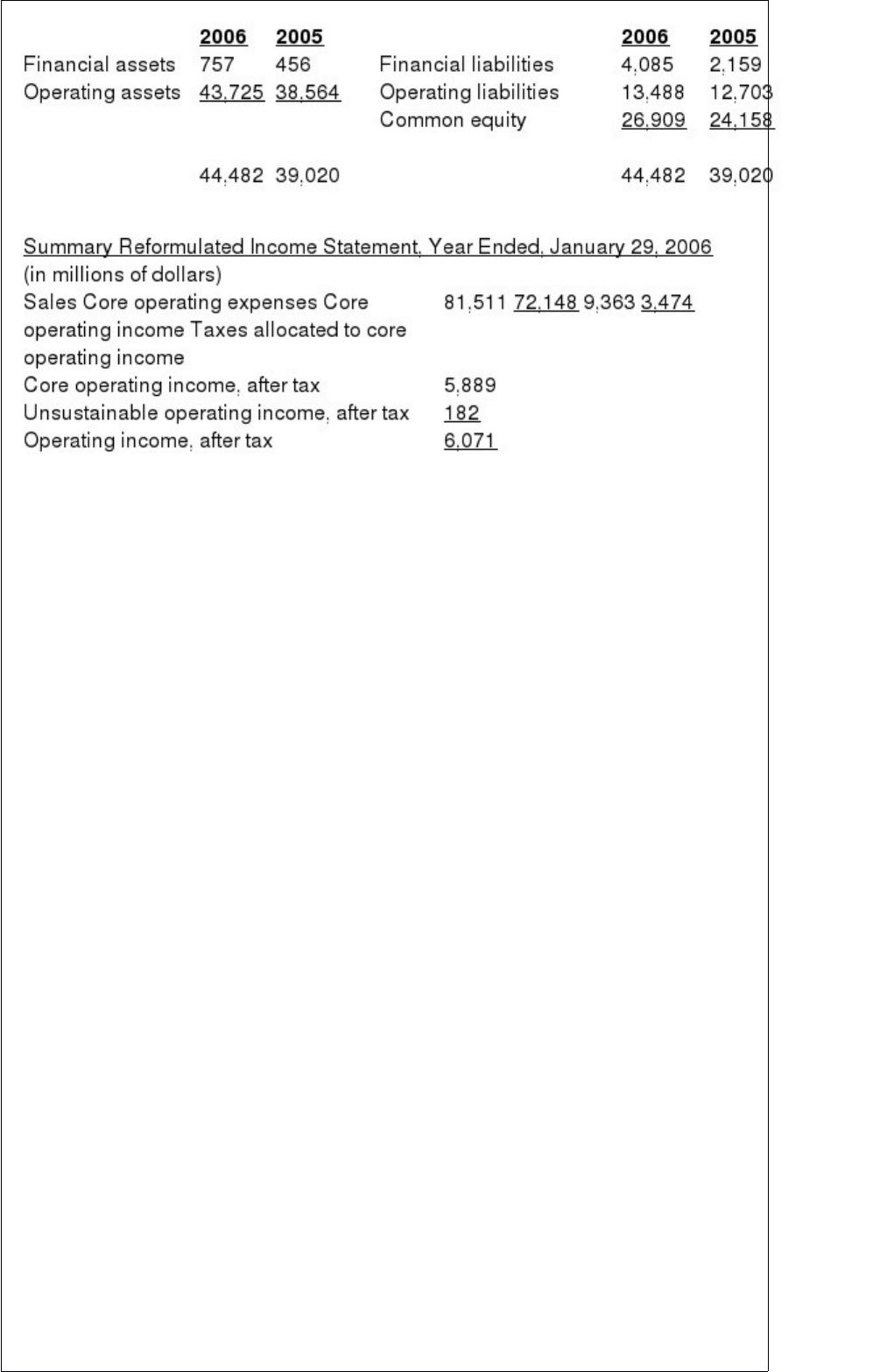

Home Depot Inc. for fiscal year ending January 29, 2006:

Summary Reformulated Balance Sheet, January 29, 2006

(in millions of dollars)

Where relevant, make all calculations for 2006 with beginning-of-period balance sheet

numbers in the questions below.

(a) Calculate the following from these statements:

1> Financial leverage at the end of fiscal year, 2005

2> Operating liability leverage at the end of fiscal year, 2005

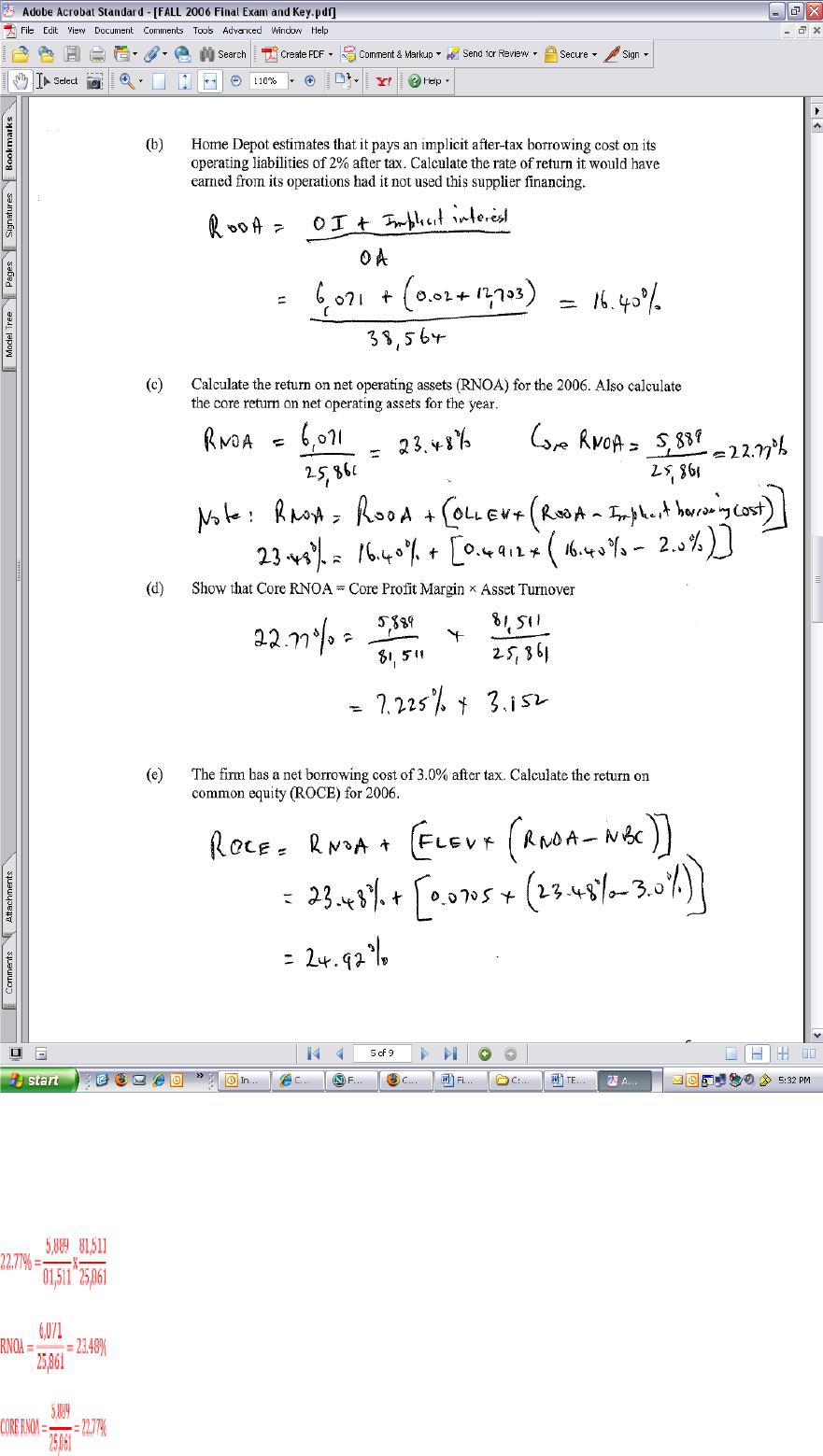

(b) Home Depot estimates that it pays an implicit after-tax borrowing cost on its

operating liabilities of 2% after tax. Calculate the rate of return it would have earned

from its operations had it not used this supplier financing.

(c) Calculate the return on net operating assets (RNOA) for the 2006. Also calculate the

core return on net operating assets for the year.

(d) Show that Core RNOA = Core Profit Margin × Asset Turnover

(e) The firm has a net borrowing cost of 3.0% after tax. Calculate the return on common

equity (ROCE) for 2006.

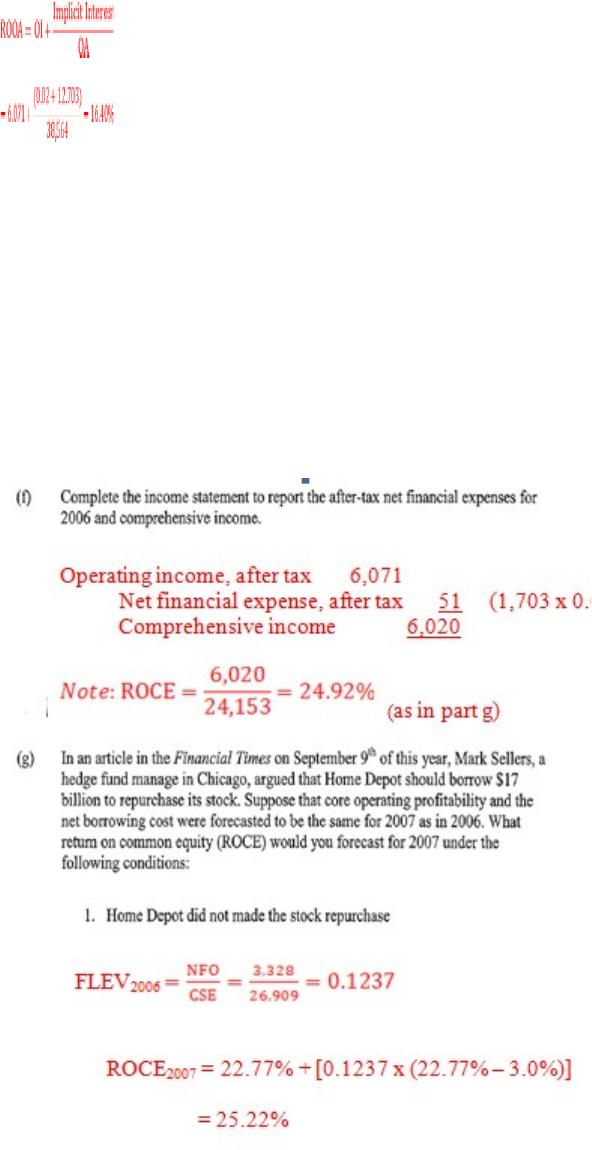

(f) Complete the income statement to report the after-tax net financial expenses for

2006 and comprehensive income.

(g) In an article in the Financial Times on September 9th of this year, Mark Sellers, a

hedge fund manage in Chicago, argued that Home Depot should borrow $17 billion to

repurchase its stock. Suppose that core operating profitability and the net borrowing

cost were forecasted to be the same for 2007 as in 2006. What return on common equity

(ROCE) would you forecast for 2007 under the following conditions:

1> Home Depot did not made the stock repurchase

2> Home Depot made the stock repurchase on January 29, 2006

The following were extracted from a financial report for a 2008 fiscal year (in millions

of dollars):

The firm has a statutory tax rate of 35%.

(a) What was operating income (after tax) for 2008?

(b) What was common shareholders’ equity at the end of 2008?

(c) Net operating assets (NOA) grew by 5% over the year. Calculate free cash flow for

2008.

(d) What was the return on net operating assets (RNOA) for 2008 (on beginning-of-year

NOA)?

(e) Net payout to shareholders for 2008 was $6 million. What was common

shareholders’ equity at the beginning of 2008?

(f) Show that the financing leverage equation (that reconciles return on common equity,

ROCE, to RNOA) holds for this firm.

(g) Forecast residual operating income for fiscal year 2009 based on the information

you have identified. Use a required return for operations of 10%.

(h) Estimate the equity value at the end of 2008 based on the following forecasts:

i. RNOA will continue in the future at the same level as in 2008.

ii. Net operating assets will grow at the same rate as in 2008.

(i) Calculate the levered P/B and unlevered (enterprise) P/B implied by your

calculations. Show that the following formula holds:

Levered P/B = Unlevered P/B + [Financial leverage x (Unlevered P/B -1)]

(j) The (equity) market capitalization for this firm is $110 million. If you think that your

forecasts of profitability and growth in part (h) of the question are appropriate, what is

your expected return to buying the enterprise at the current market price?

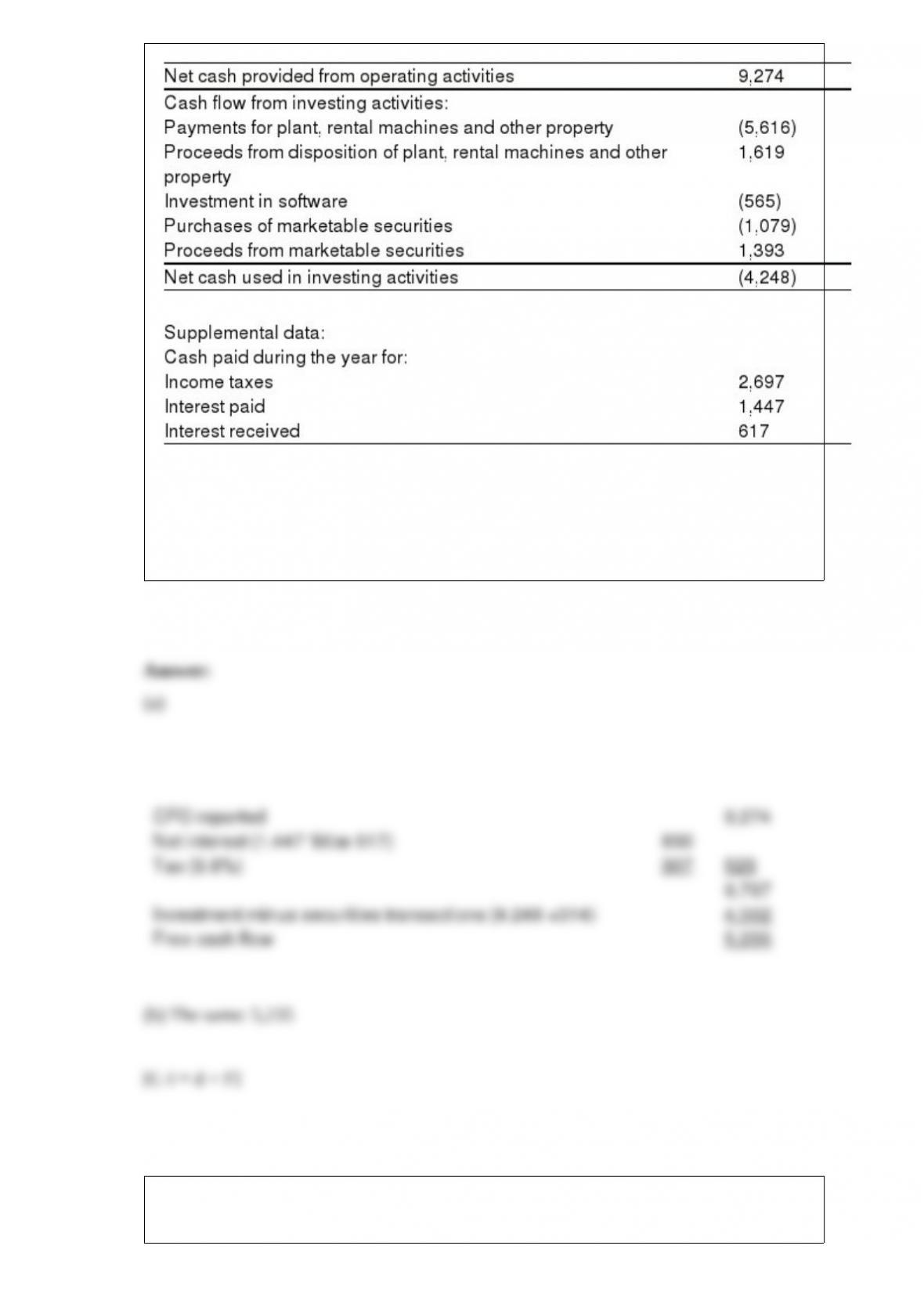

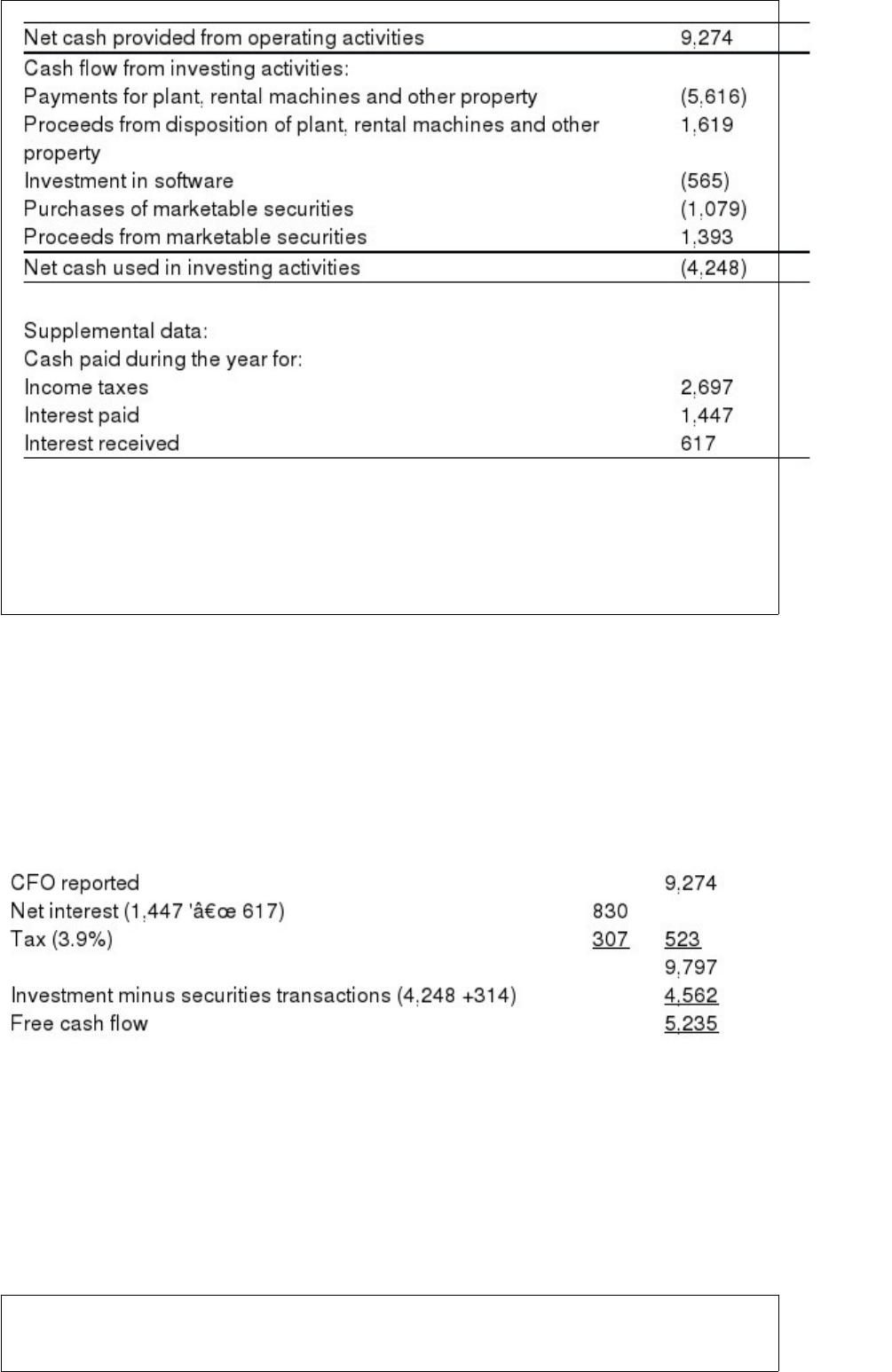

Below is a summary of part of IBM’s Statement of Cash Flows for the year ended

December 31, 2001 (in millions of dollars). The firm faces a 37% statutory tax rate.

(a) From this information, calculate free cash flow for 2001.

(b) What was the net amount of cash paid out of the firm in financing activities during

2001?

Part A

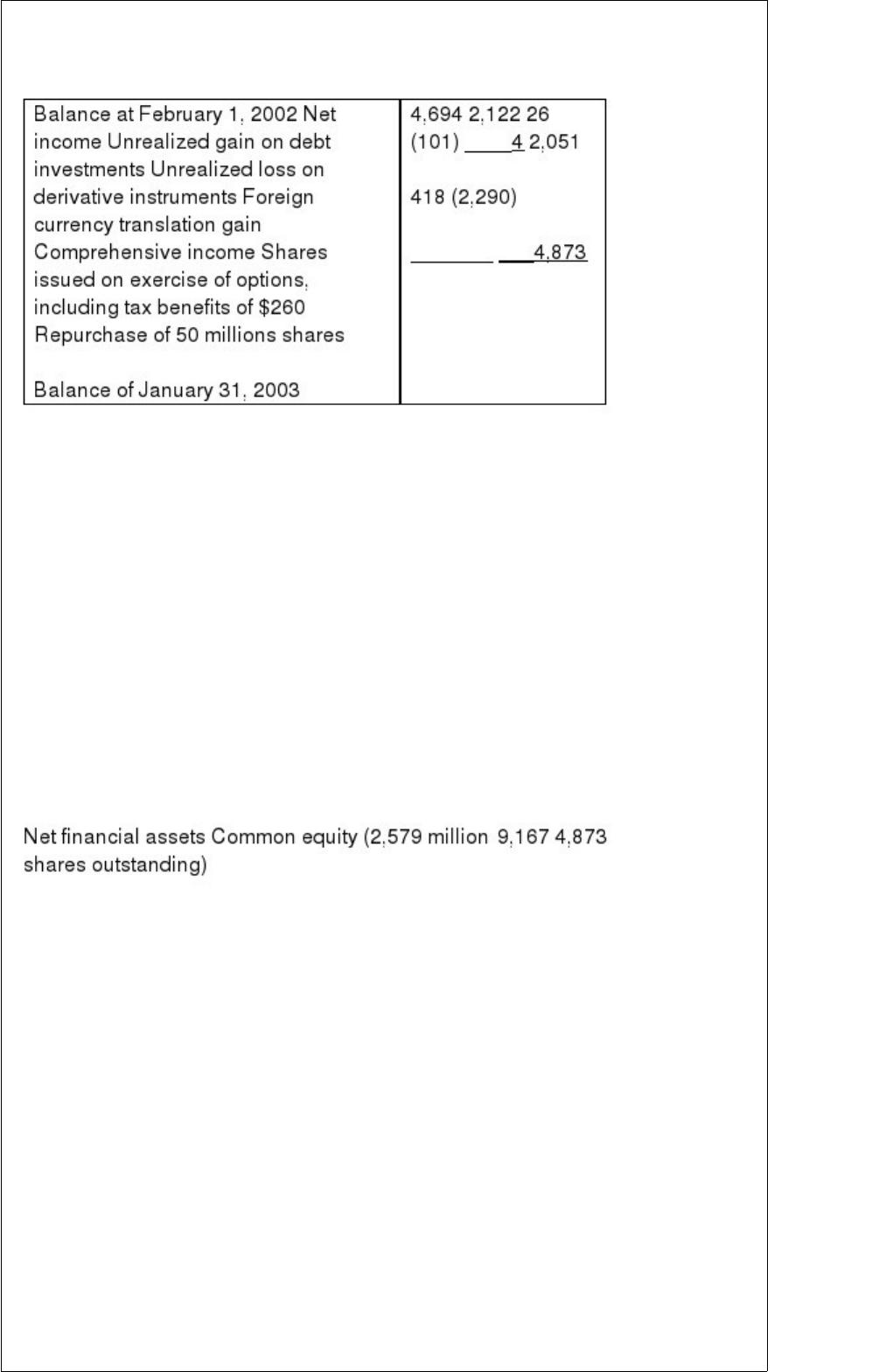

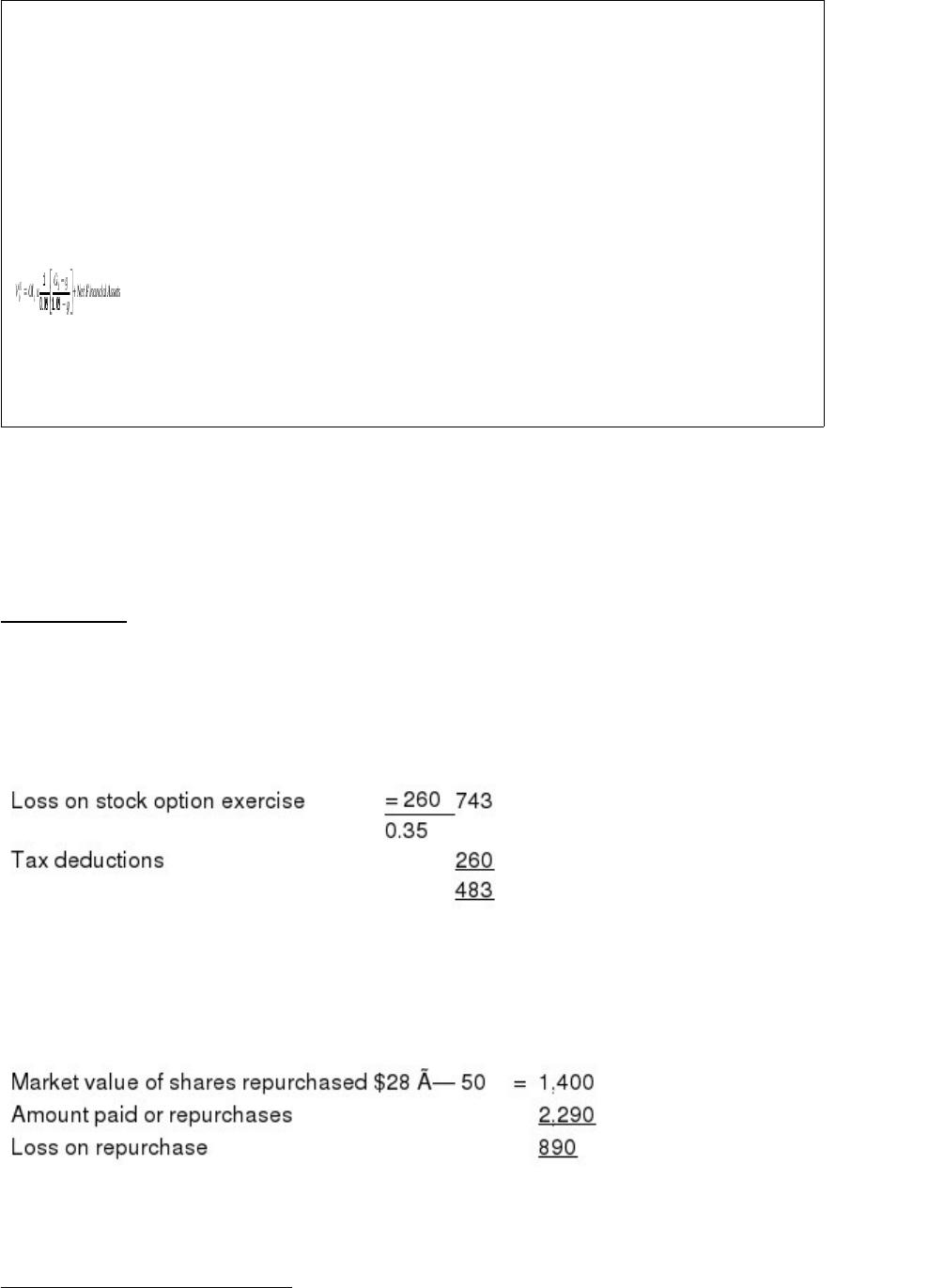

The following is a condensed version of the statement of shareholders’ equity for Dell

Computer Corporation for fiscal year ending January 31, 2003 (in millions of dollars):

Other information:

1> Dell’s tax rate is 35%

2> The repurchase occurred when the stock traded at $28 per share.

Required:

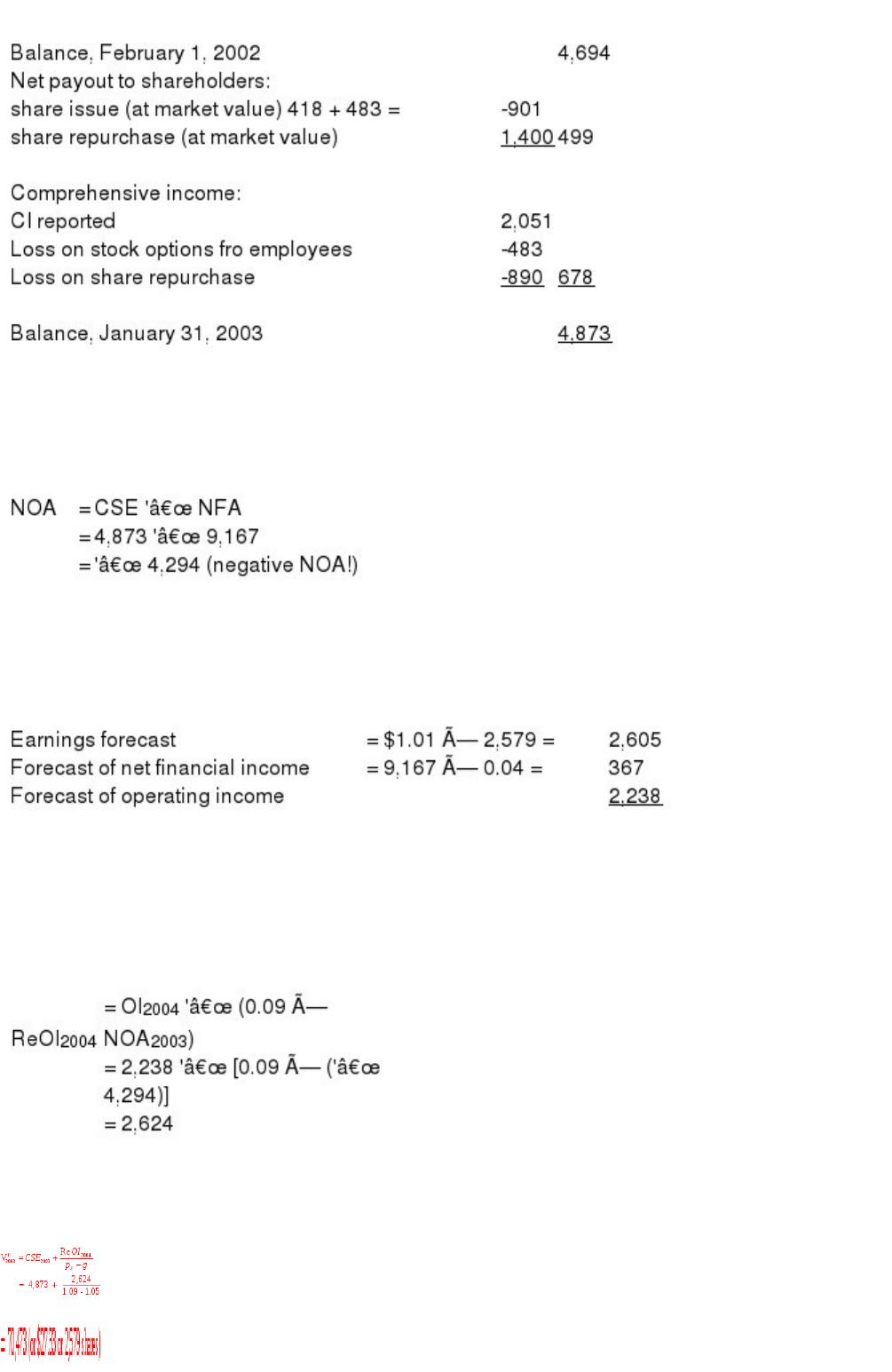

Prepare a reformulated statement of shareholders’ equity for 2003 for Dell Computer

Corporation. The reformulated statement should identify comprehensive income.

Part B

The following is extracted from Dell’s balance sheet at January 31, 2003 (in millions of

dollars):

Analysts are forecasting consensus earnings per share of $1.01 for the year ending

January 31, 2004.

a. Calculate net operating assets at January 31, 2003.

b. Net financial assets are expected to earn an after-tax return of 4% in 2004. What is

the forecast of operating income implicit in the analysts’ eps forecast?

c. Forecast the residual operating income for 2004 that is implicit in the analysts’

forecast. Use a required annual return for operations of 9%.

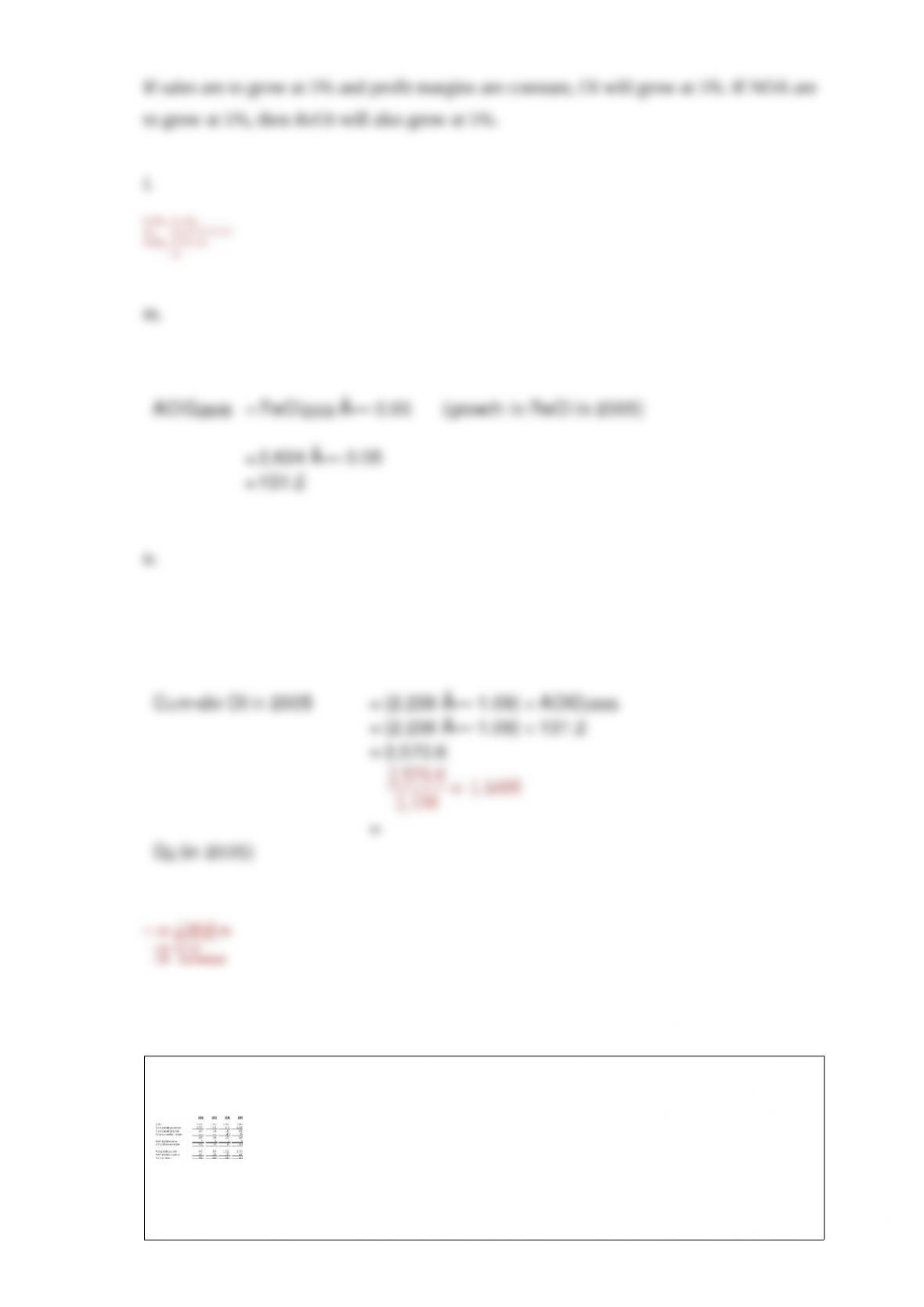

d. Dell’s shares are currently trading at $34 each. With the above information, value the

shares under the following set of scenarios using residual income methods:

(i) Sales will grow at 5% per year after 2004.

(ii) Operating assets and operating liabilities with both grow at 5% per year after 2003.

(iii) Operating profit margins (after tax) will be the same as these forecasted for 2004.

e. Under the same scenarios, forecast free cash flow for 2004.

f. Under the same scenarios, forecast abnormal growth in operating income for 2005.

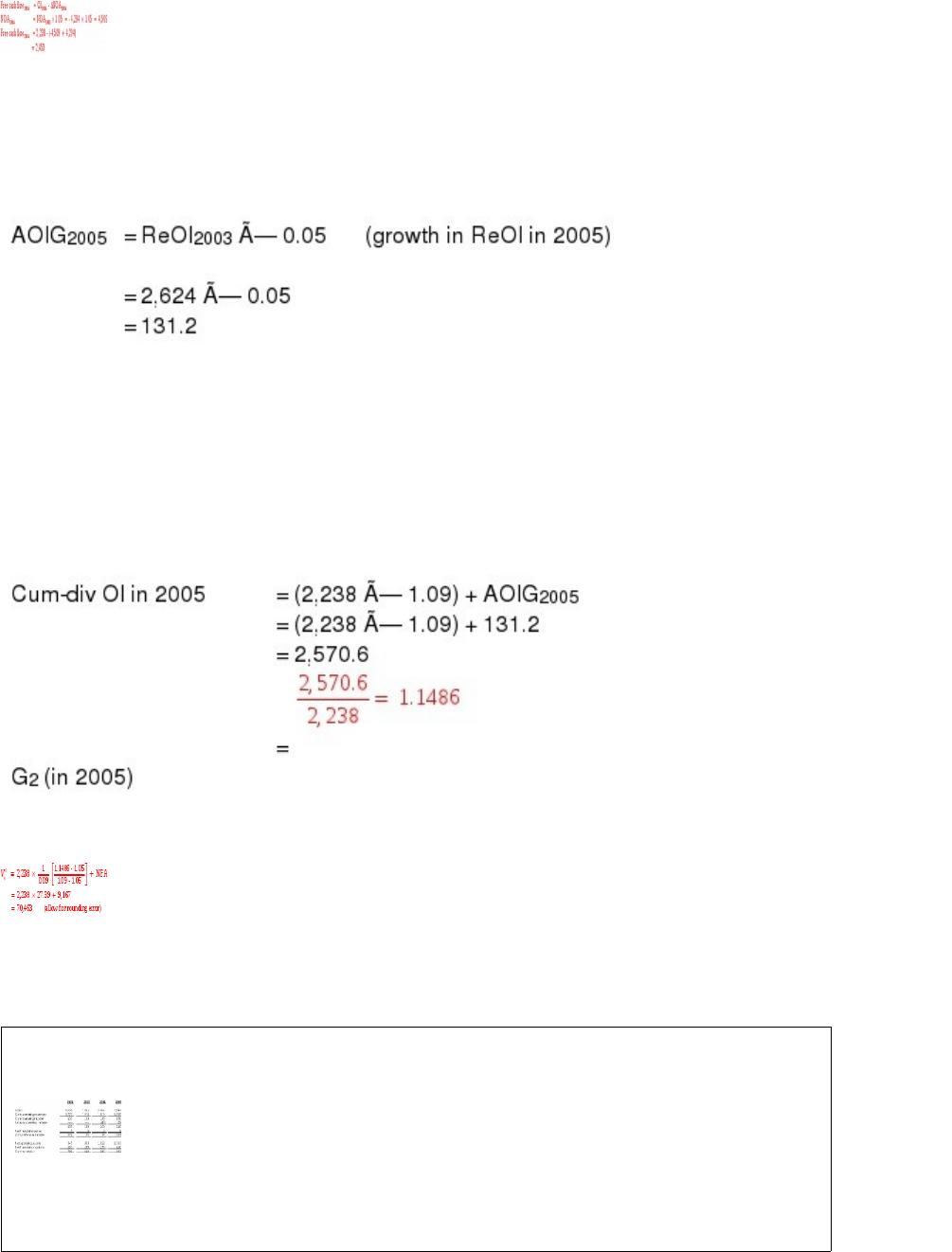

g. Show that, with a long term growth rate of 5%, the following formula will give the

same value as that in part (d) of the question:

where G2 is the (one plus) cum-dividend growth rate in operating income two years

ahead and g is (one plus) the long-term growth rate.

The following are summary income statement and balance sheet numbers for a firm (in

millions of dollars). The firm has a required return for operations of 9%.

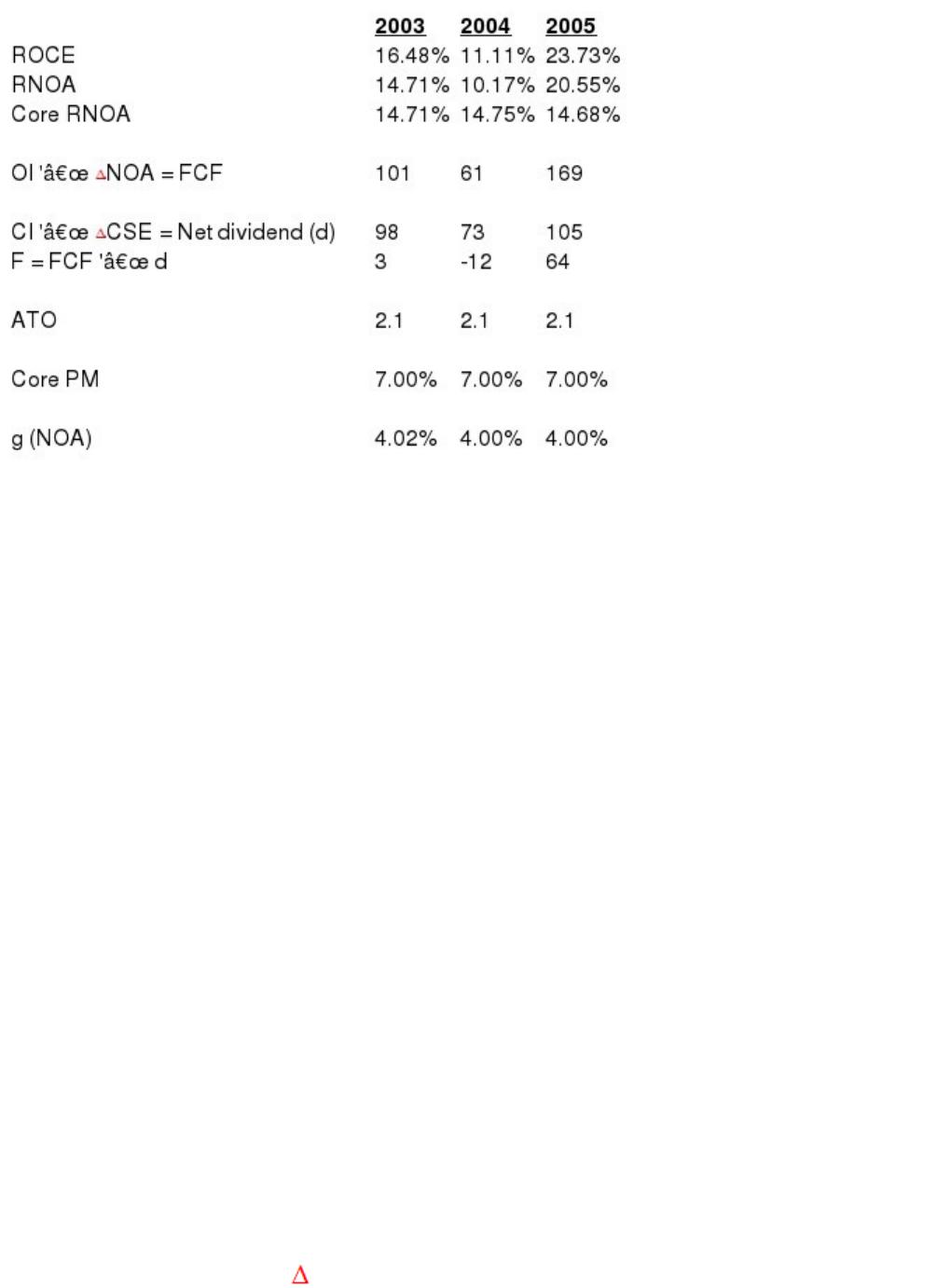

(a) Prepare a table on the next page giving the following for 2003- 2005. Use

beginning-of-period balance sheet numbers in denominators.

 Return on common equity (ROCE)

 Return on net operating assets (RNOA)

 Core return on net operating assets (Core RNOA)

 Free cash flow

 Net payments to common shareholders

 Net payments to net debt holders

 Asset turnover

 Core profit margin

 Growth rate for net operating assets

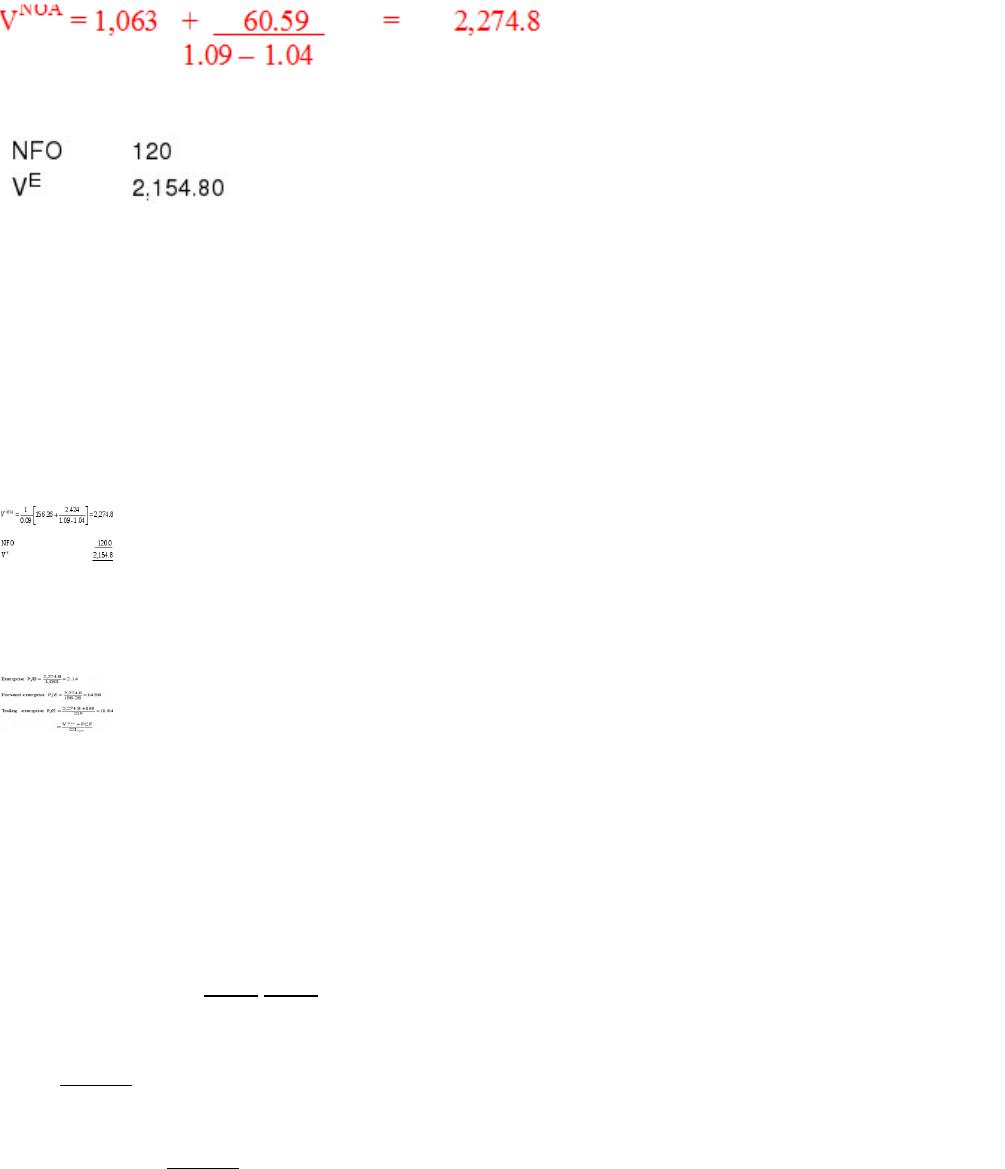

(b) On the basis of these financial statements, forecast

(i) Residual operating income for 2006 and 2007.

(ii) Abnormal operating income growth for 2007.

(c) Value the equity using two methods:

(i) Residual operating income valuation

(ii) Abnormal operating income growth valuation

(d) Calculate the enterprise price-to-book ratio implied by your valuation. Also,

calculate the enterprise trailing and forward P/E ratios implied by your valuation.

(e) After making your valuation you discover (in footnotes) that the firm has 37 million

employee stock options outstanding, valued at $10 per option. The firm’s tax rate is

35%.

How does this information modify your calculation of the enterprise price-to-book

ratio?

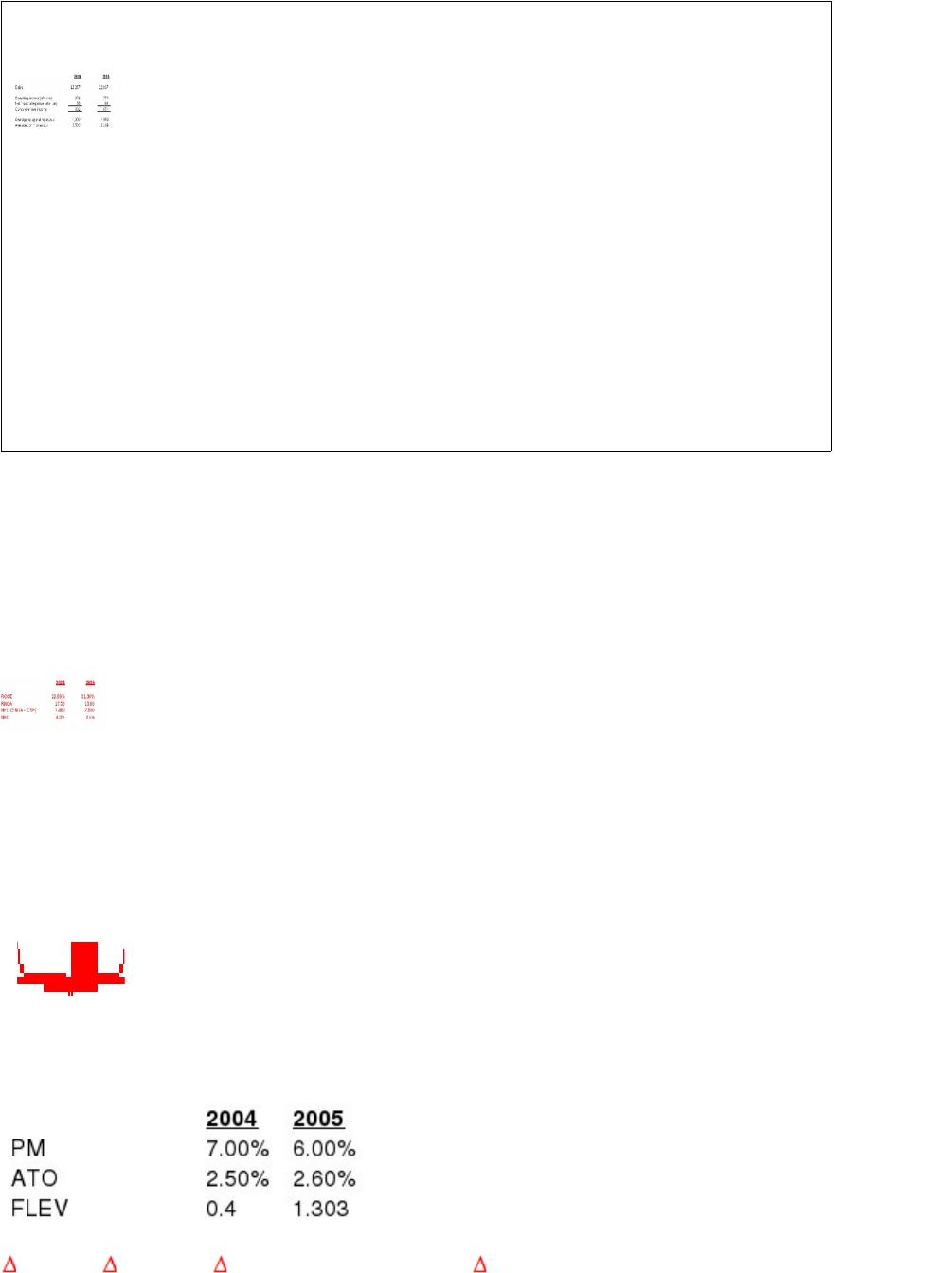

Below are some summary numbers for a firm for fiscal years 2004 and 2005 (in

millions of dollars).

(a) Calculate return on common equity (ROCE), return on net operating assets

(RNOA), and net borrowing cost (NBC) for the two years.

(b) How much of the change in ROCE over the two years is due to:

(I) Change in profit margin

(II) Change in asset turnover

(III) Change in financial leverage

(IV) Change in borrowing costs?

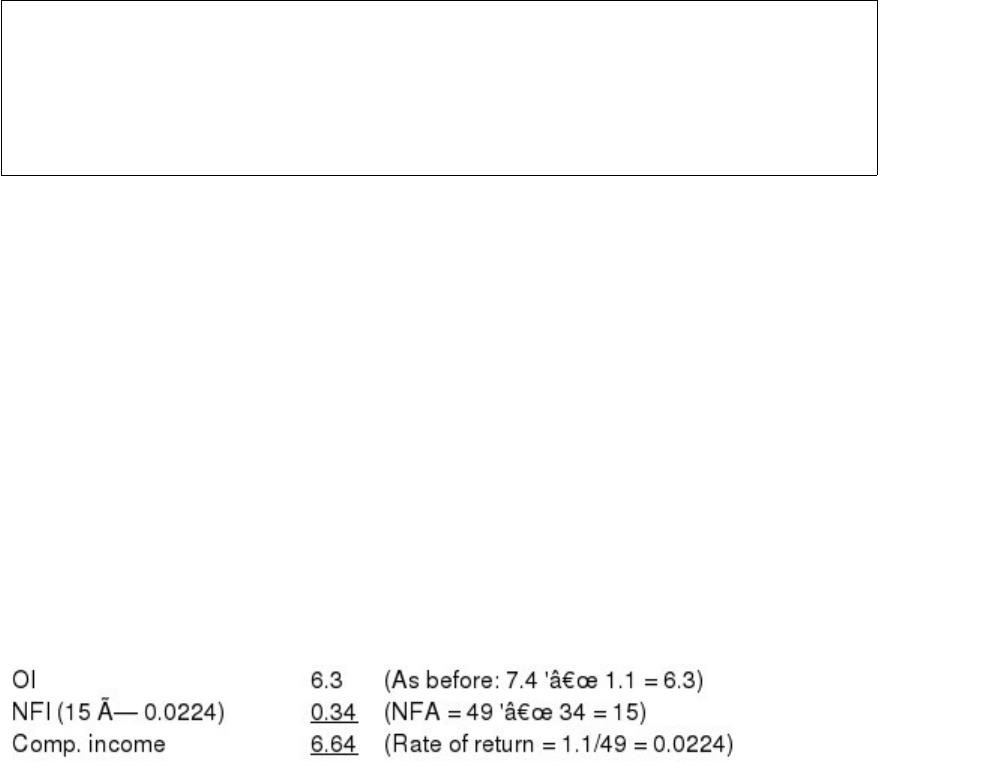

At the end of the fiscal year ending June 30, 2003, Microsoft reported common equity

of $64.9 billion on its balance sheet, with $49.0 billion invested in financial assets (in

the form of cash equivalents and short term investments) and no financing debt. For

fiscal year 2004, the firm reported $7.4 billion in comprehensive income, of which $1.1

billion was after-tax earnings on the financial assets.

This month Microsoft is distributing $34 billion of financial assets to shareholders in

the form of a special dividend.

a. Calculate Microsoft’s return on common equity (ROCE) for 2004.

b. Holding all else constant what would Microsoft’s ROCE be after the payout of $34

billion?

c. Would you expect the payout to increase or decrease earnings growth in the future?

Why?

d. What effect would you expect the payout to have on the value of a Microsoft share?

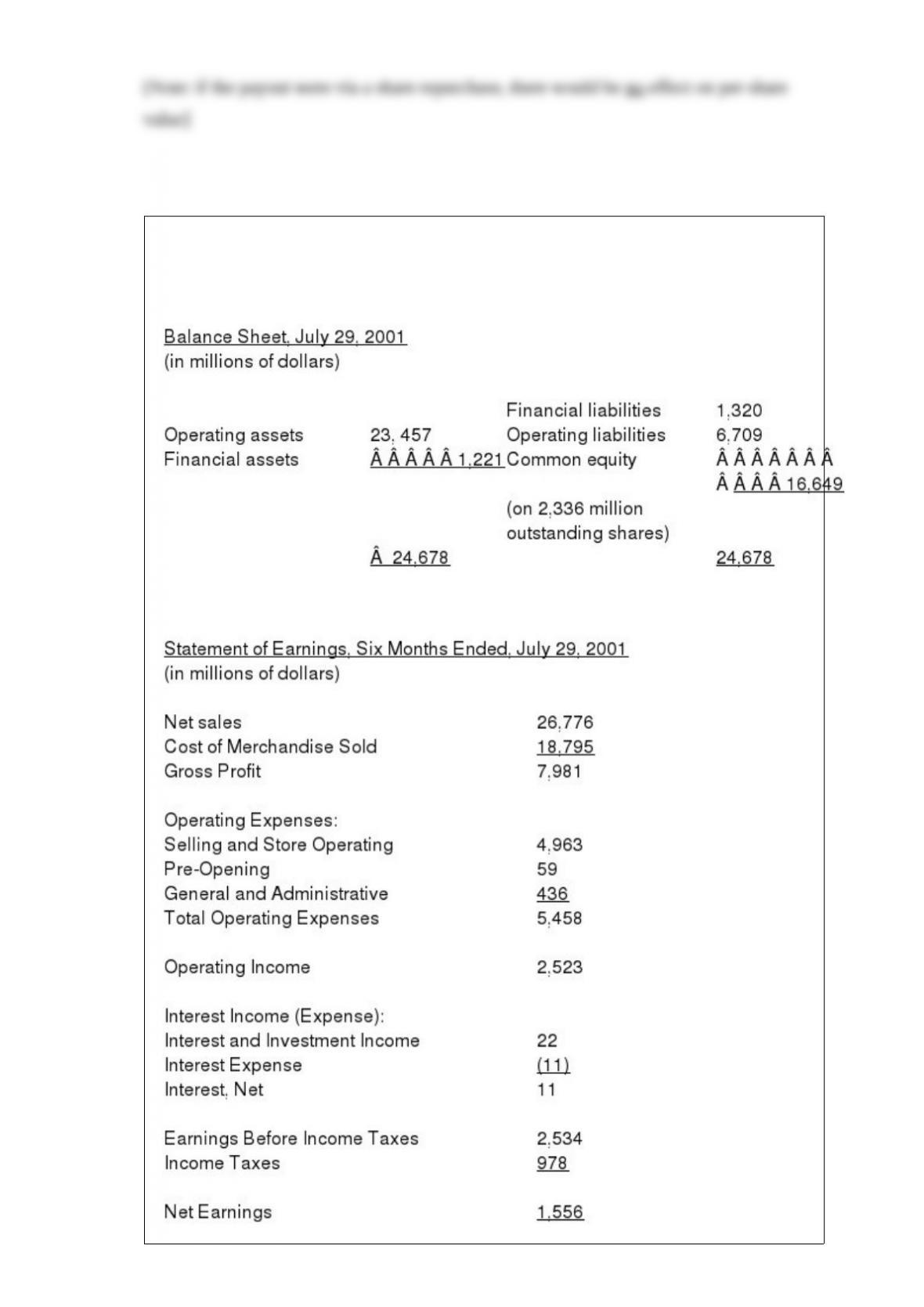

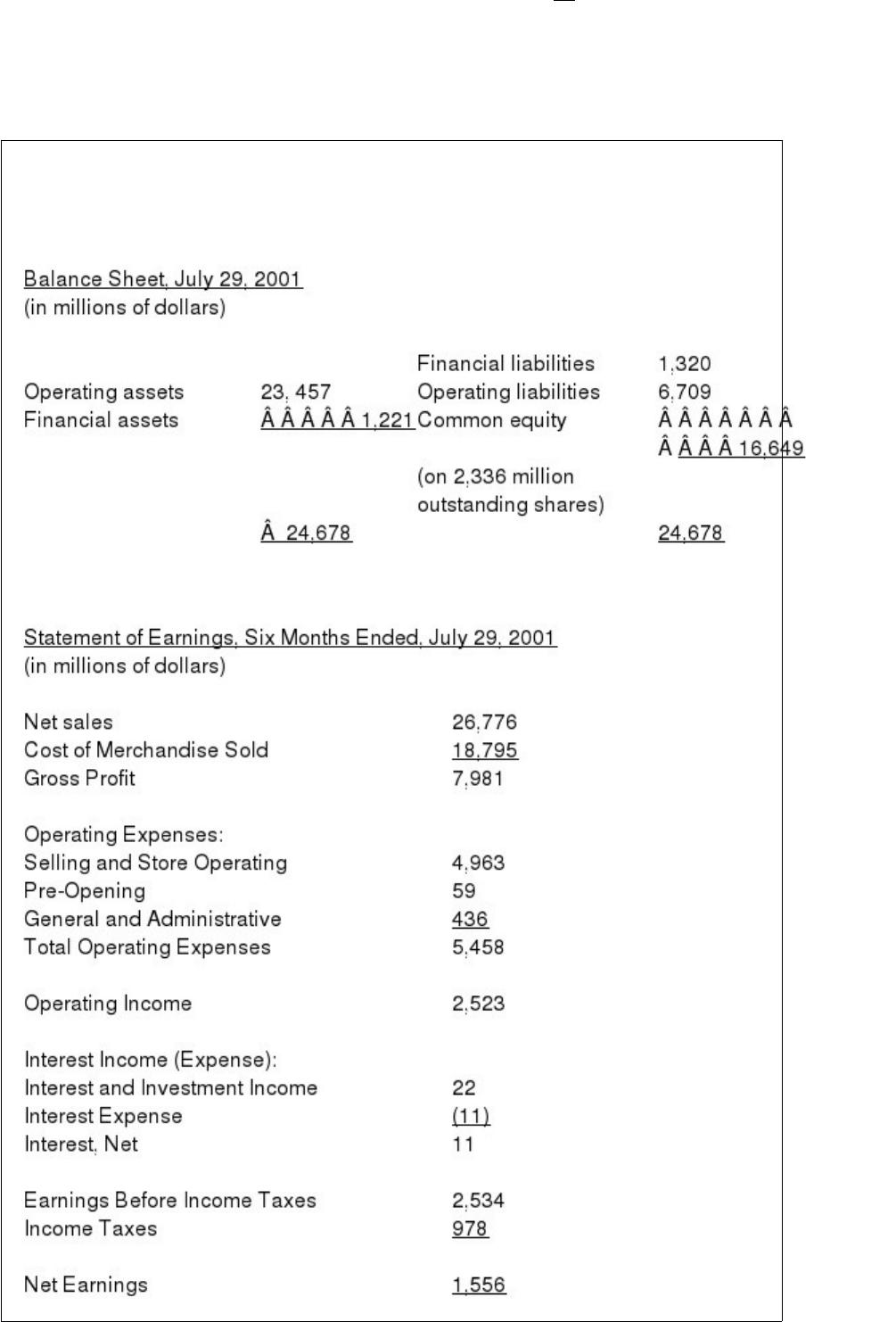

At the time that of its 10-Q filing of financial statements for the first half of its January

2002 fiscal year, Home Depot’s shares traded at $50 per share. The following are

summaries from those financial statements.

According to financial statement footnotes, Home Depot’s statutory tax rate (combined

Federal and State rates) is 39%. Other comprehensive income (not in net earnings

above) is negligible. Use a required six-month return for operations of 4% in

calculations below.

(a)

Calculate the following from these statements:

1> Financial leverage

2> Operating liability leverage

3> After-tax profit margin

(b) Home Depot earned a return on beginning net operating assets (RNOA) of 9.3% for

the six months ending July 29, 2001.

1> What was the asset turnover during these six months?

2> What was the residual operating income over the six months?

(c) Calculate the free cash flow generated by operations during the six months.

(d) At the current market price of $50 per share, what growth rate for residual operating

income does the market forecast for the future?

(e) Calculate Home Depot’s price-to-sales ratio for trailing six-month sales.

(f) If both profit margin and asset turnover are expected to continue at their current

levels in the future, what is the sales growth rate forecast implied in the price-to-sales

ratio?

A firm with a return on common equity (ROCE) of 30% has financial leverage of

37.5% and a net after-tax borrowing cost of 5% on $240 million of net debt.

(a) What rate of return does this firm earn on its operations?

(b) The firm is considering repurchasing $150 million of its stock and financing the

repurchase with further borrowing at a 5% after-tax borrowing cost. What effect will

this transaction have on the firm’s return on common equity if the same level of

operating profitability is maintained?

(c) Will this repurchase change the per share intrinsic value of the equity? Why?

(d) Will the normal P/E ratio for this firm change because of this transaction? Why?

(e) The firm had an unlevered price-to-book ratio (P/B) of 1.8 prior to the transaction.

What will be the effect of the repurchase on the levered price-to-book ratio?

(f) Would you expect the earnings-per-share growth rate to change after the repurchase

transaction? Why?

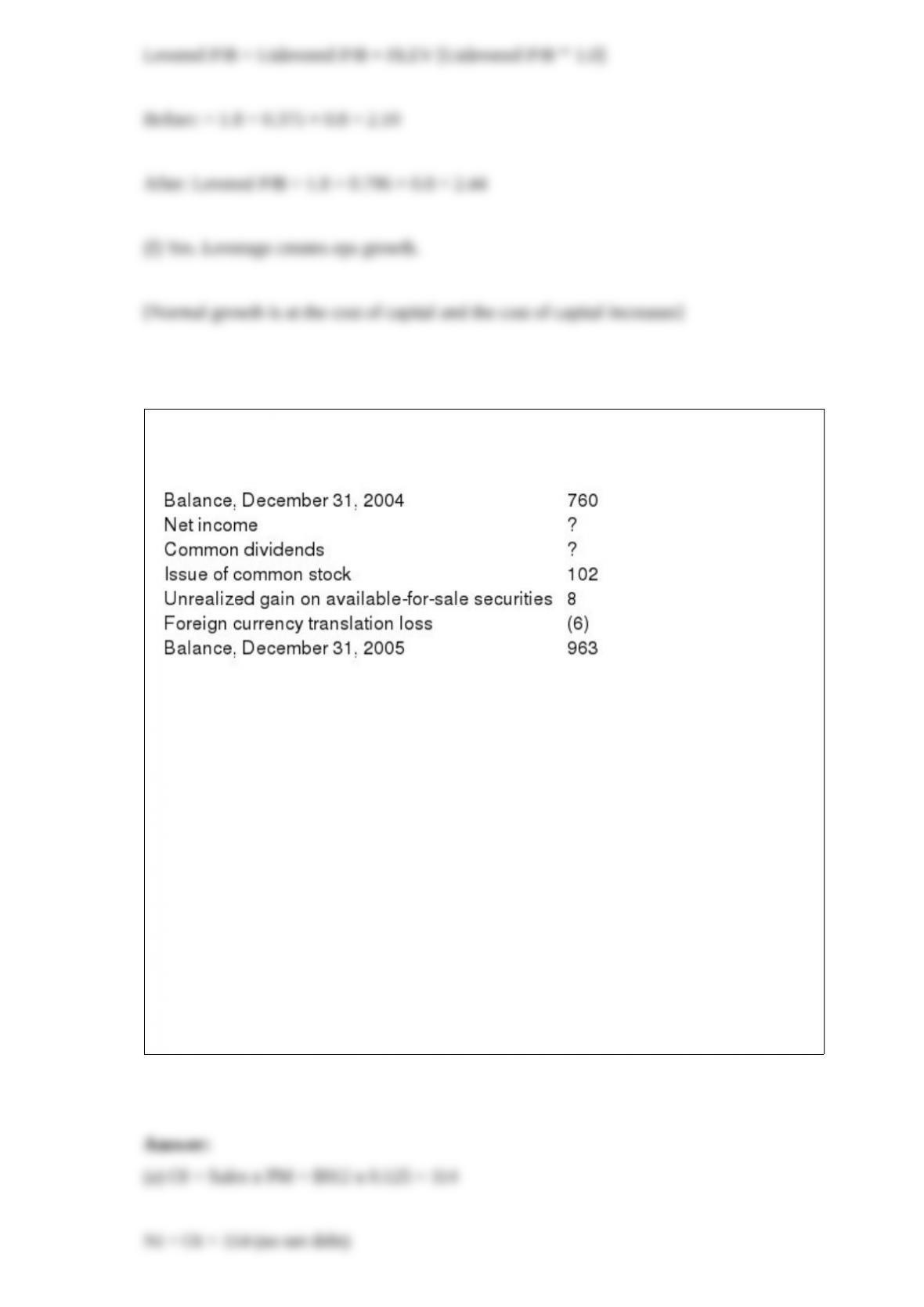

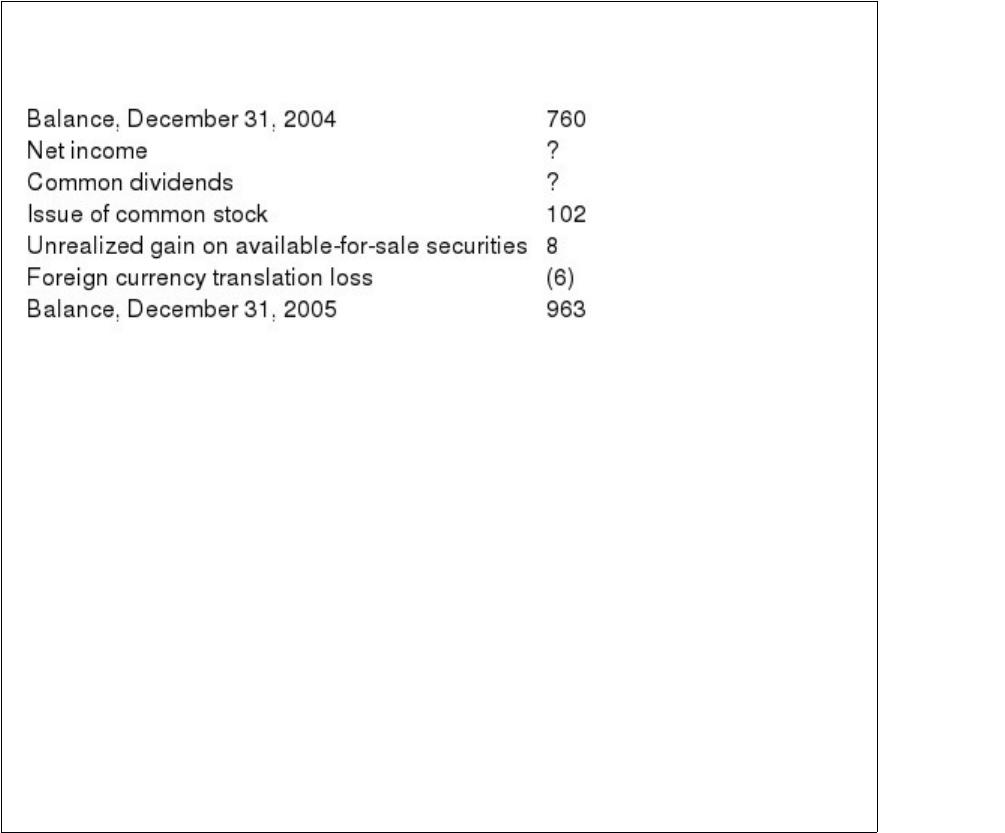

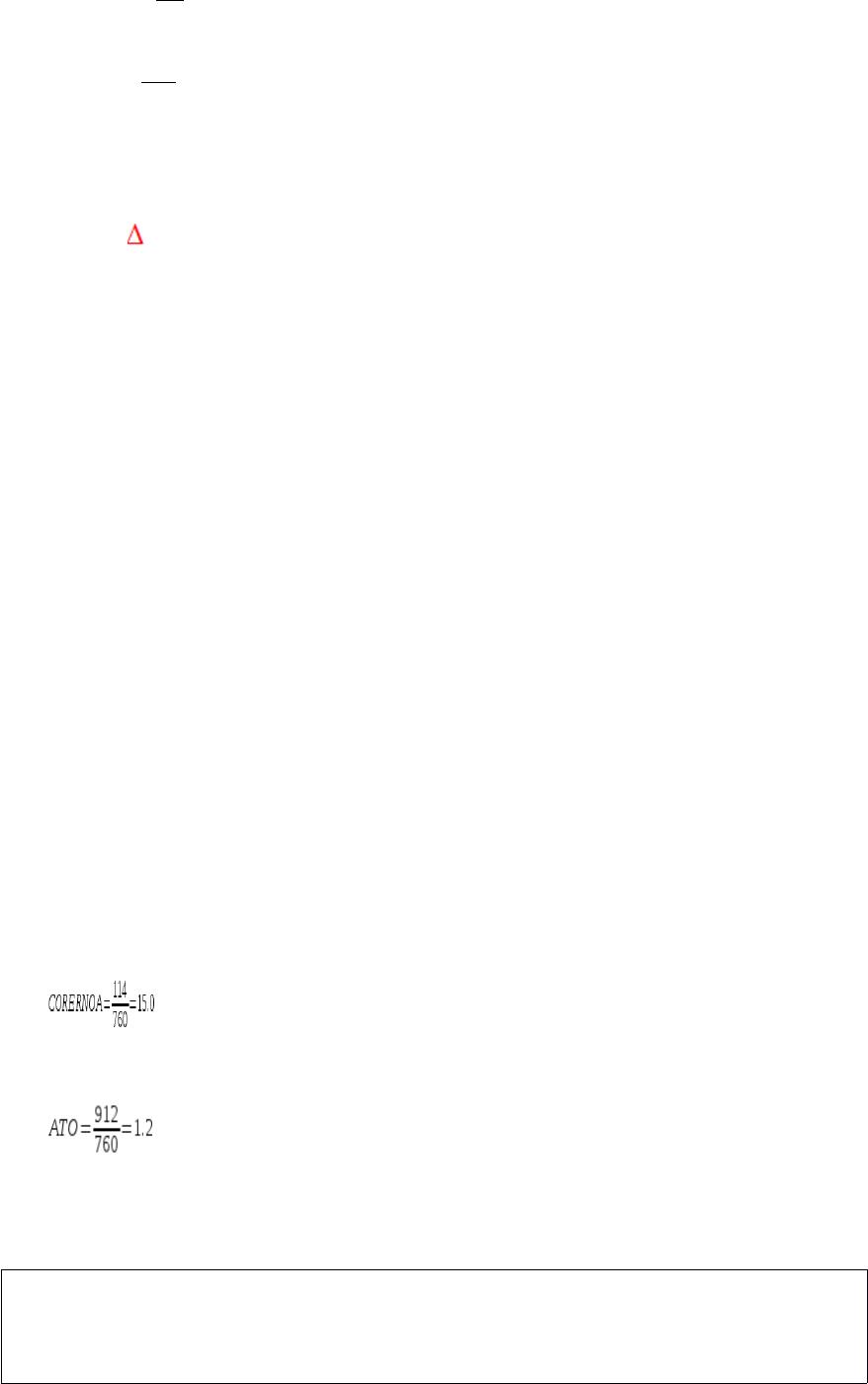

The following is an incomplete statement of common shareholders’ equity (in millions

of dollars).

The firm has no net debt (a pure equity firm) and reported an after-tax operating profit

margin of 12 ½% on sales of $912 million in its income statement for 2005. All

operating expenses in the income statement are involved in generating core income.

Calculate the following for 2005:

(a) Net income and comprehensive income

(b) Free cash flow

(c) Dividends paid to common shareholders

(d) Core return on net operating assets (on beginning-of-year balance sheet)

(e) Asset turnover

Explain in no more than 50 words why it is common that firms with higher return on

net operating assets (RNOA) also have negative free cash flow. Also explain why such

firms tend to have above-average forward P/E.

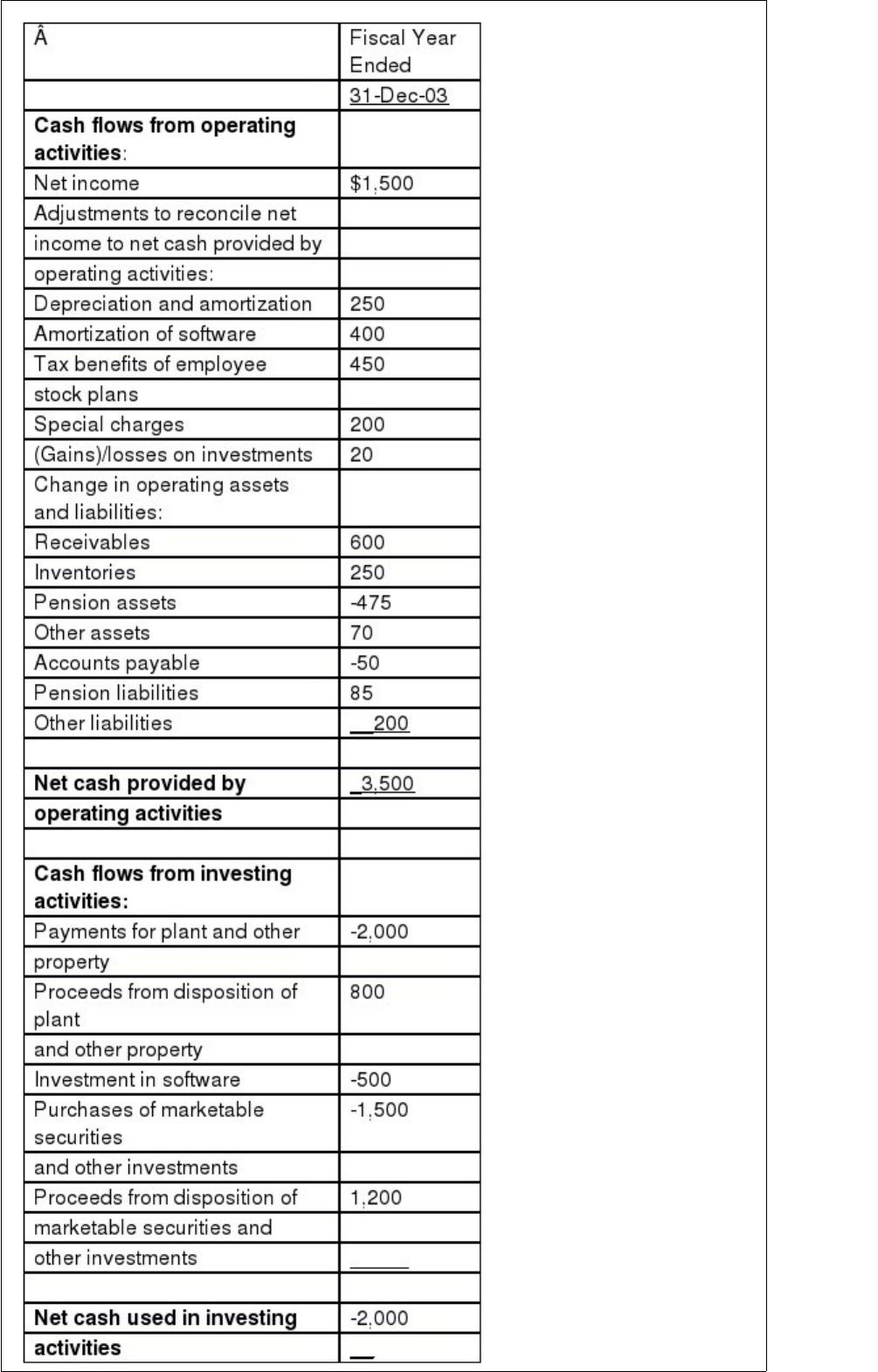

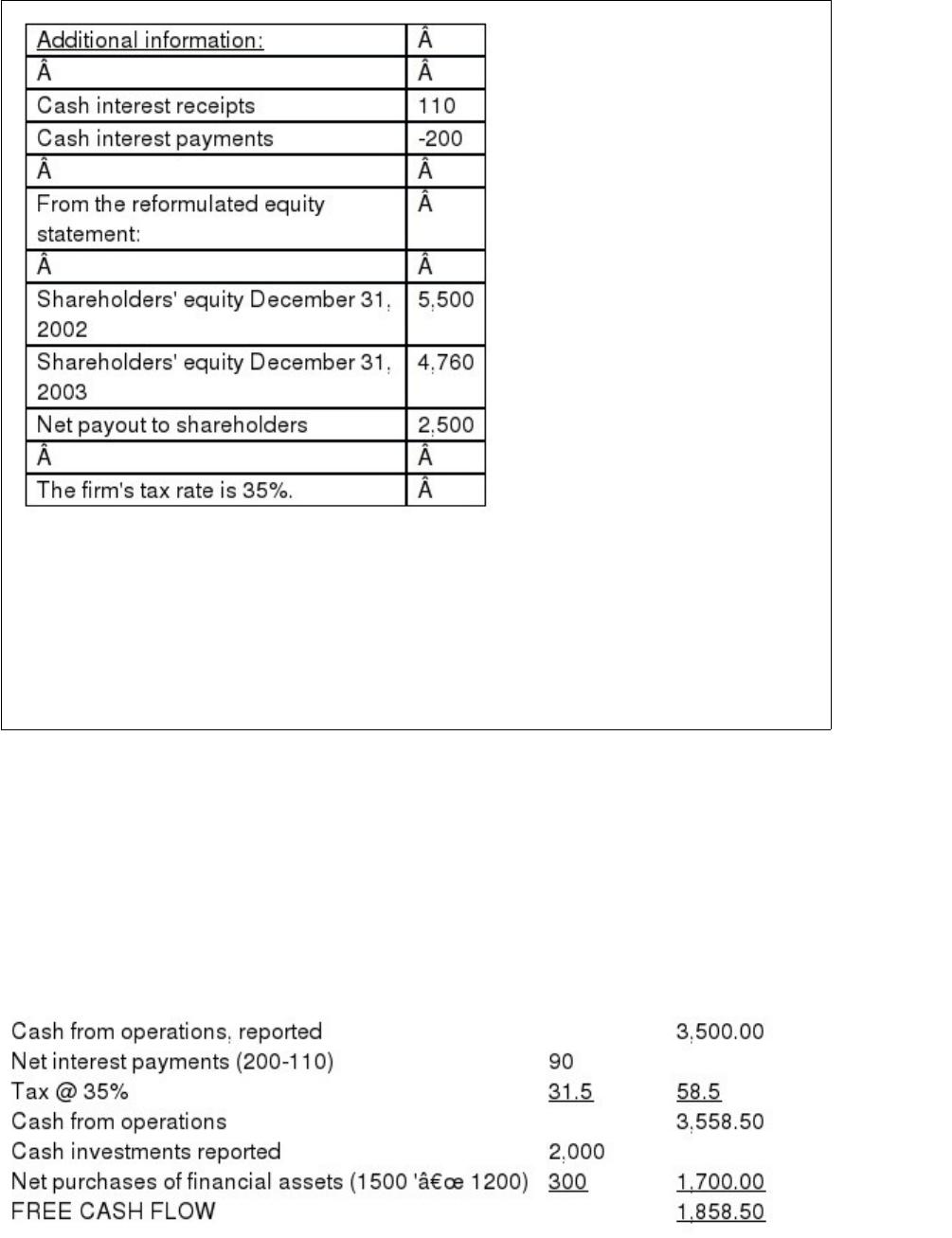

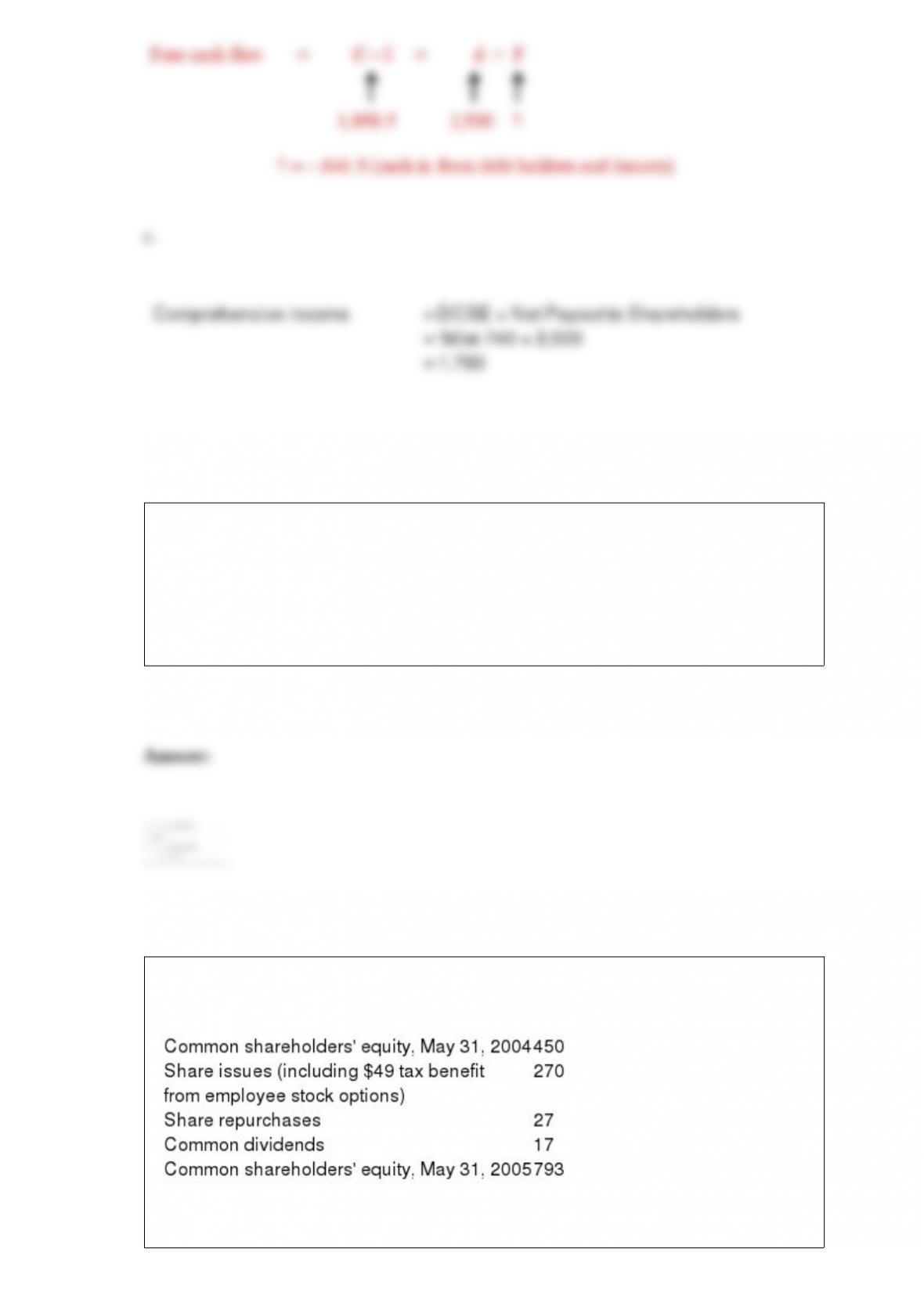

Below is an excerpt from the cash flow statement of a firm for fiscal year 2003:

Required:

a. Calculate free cash flow for 2003.

b. Calculate net payments to debt holders and issuers for 2003.

c. Calculate comprehensive income for 2003.

A firm whose equity traded at $41.67 per share at the end of 2004 in expected to earn

$2.50 per share in 2005 and $2.85 in 2006. The firm pays no dividends.

Set the long-term growth rate for residual earnings equal to the GDP growth rate of 4

percent. Given these forecasts, what is the rate of return you expect to earn from buying

the shares?

From the following information, calculate comprehensive income for fiscal year 2005.

Amounts are in millions of dollars.

The firm’s statutory tax rate is 35%.

Cisco Systems traded at $20 per share on December 3, 2001. Analysts are forecasting

earnings per share of 0.22 for 2002 and 0.39 for 2003. The firm does not pay dividends.

Value Cisco on the assumption that abnormal earnings growth forecasted for 2003 will

continue at the same level into the future. Use a cost of equity capital of 10%.

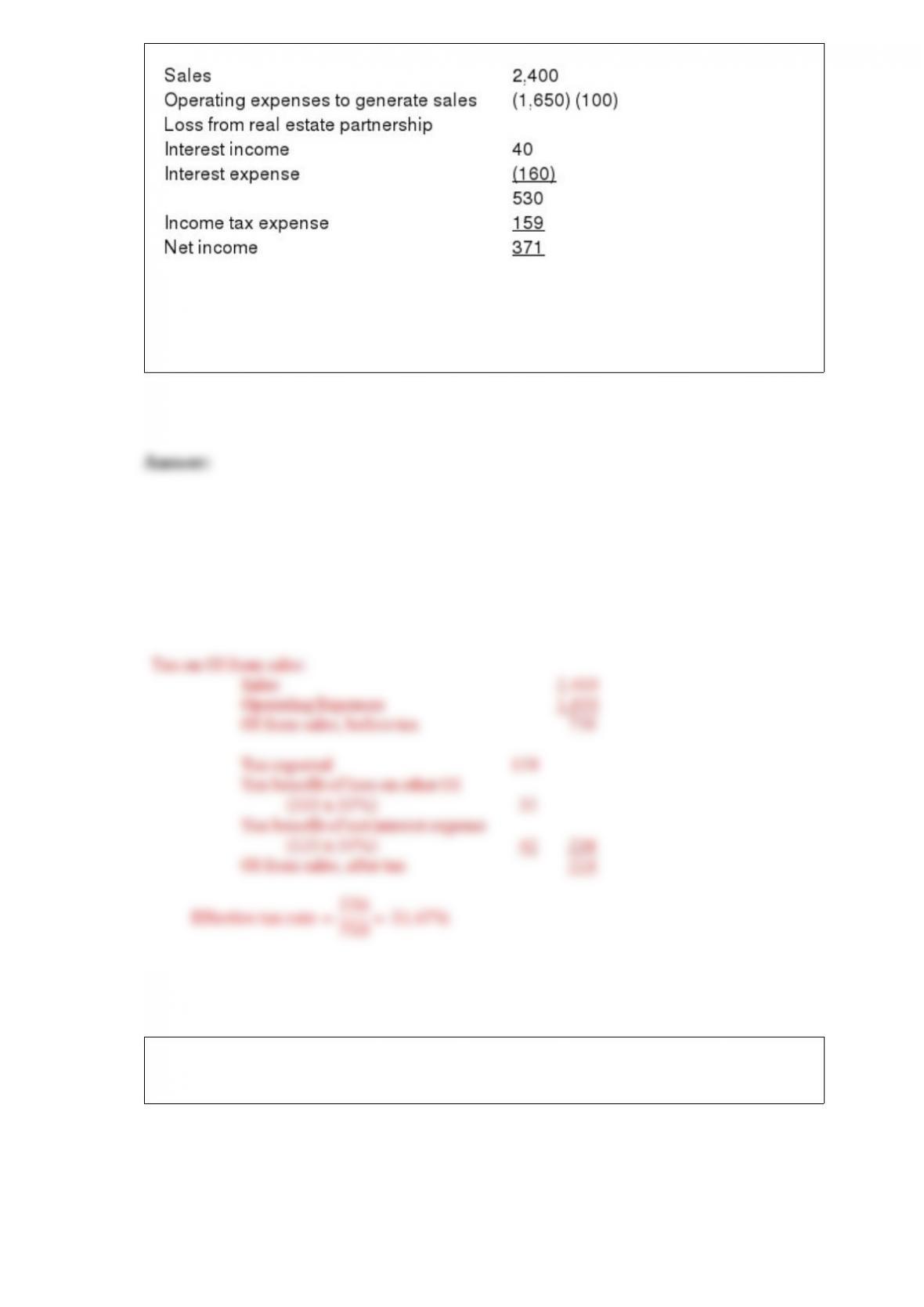

Reformulate the following income statement (in millions of dollars):

The firm’s statutory tax rate is 35%.

What is the effective tax rate on operating income from sales?

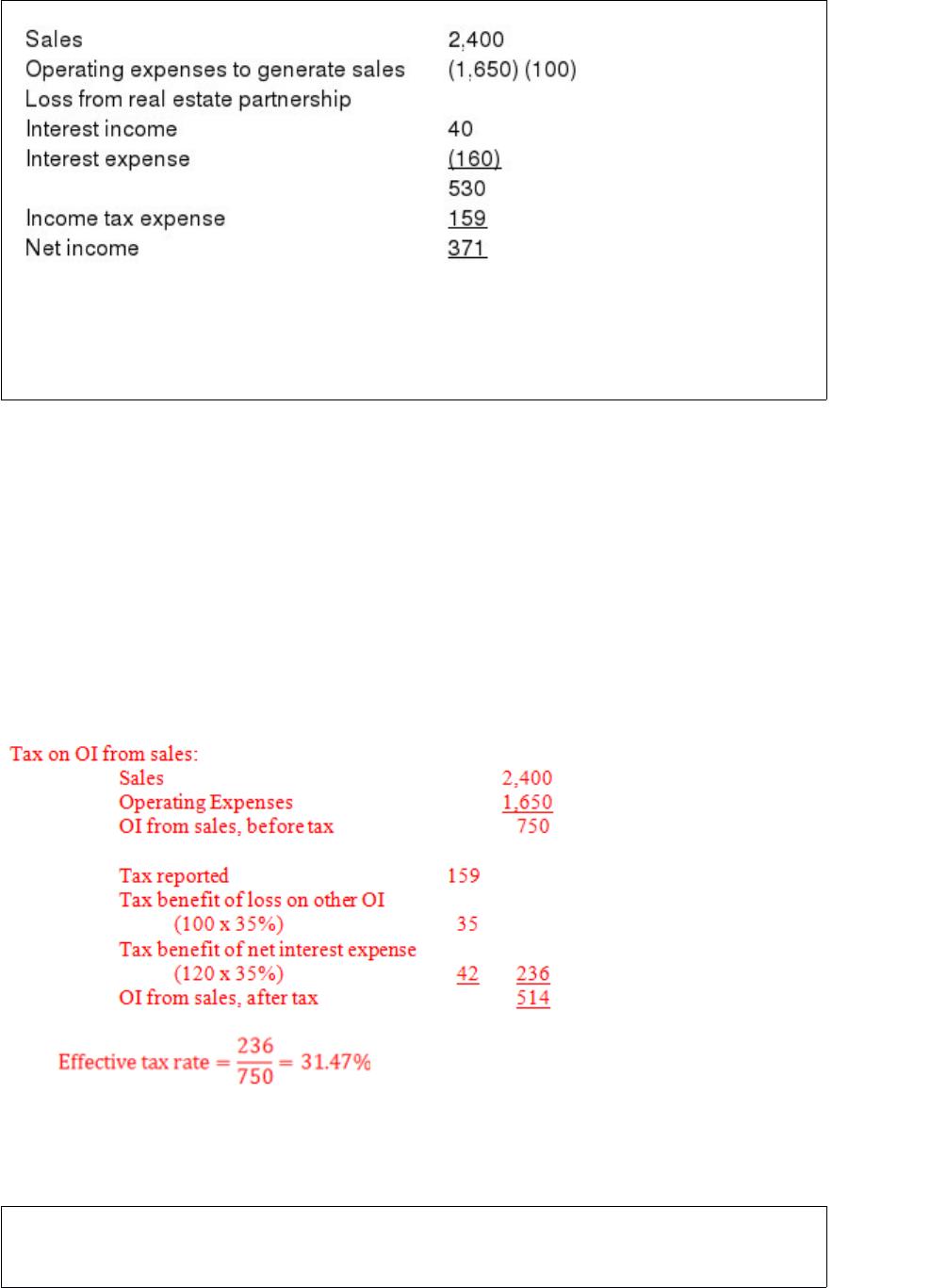

The following is from the statement of shareholders’ equity for Intel Corporation for

2000 (in millions of dollars). Intel faces a 38% tax rate.

Calculate comprehensive income to Intel’s shareholders for 2000, being sure to include

any hidden dirty surplus expenses.