A limit order

A. Is an order to trade up to a certain number of futures contracts at a certain price

B. Is an order that can be executed at a specified price or one more favorable to the

investor

C. Is an order that must be executed within a specified period of time

D. None of the above

Which of the following can be valued without using a numerical procedure such as a

binomial tree?

A. American put options on a non-dividend paying stock

B. American call options on a non-dividend paying tock

C. American call options on a currency

D. American put options on futures

The yield on a company’s five-year bonds is 5%. The five year swap rate is 4.5% and

the five-year Treasury rate is 4%. What would be closest to your best estimate of the

five-year CDS spread

A. 200 basis points

B. 150 basis points

C. 100 basis points

D. 50 basis points

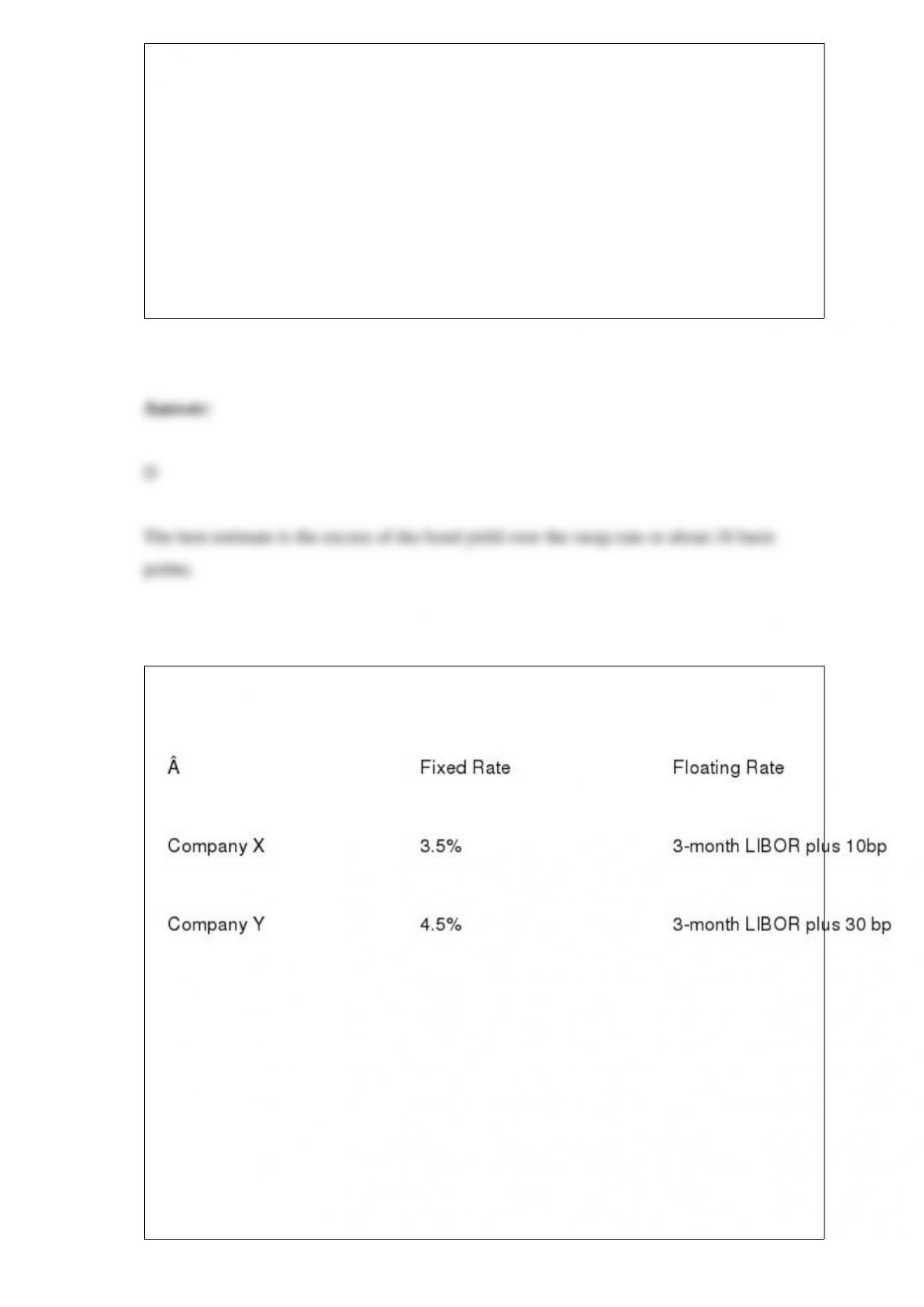

Company X and Company Y have been offered the following rates

Suppose that Company X borrows fixed and company Y borrows floating. If they enter

into a swap with each other where the apparent benefits are shared equally, what is

company X’s effective borrowing rate?

A. 3-month LIBOR-30bp

B. 3.1%

C. 3-month LIBOR-10bp

D. 3.3%

The parameters in a GARCH (1,1) model are: omega =0.000002, alpha = 0.04, and beta

= 0.95. The current estimate of the volatility level is 1% per day. If we observe a change

in the value of the variable equal to 2%, how does the estimate of the volatility change

A. 1.26%

B. 1.16%

C. 1.06%

D. 1.03%

Which of the following describes the waterfall typically used for mortgages pre-crisis?

A. A distribution of cash flows to tranches with priority given to tranche with the

highest rating

B. A distribution of cash flows to tranches in proportion to their outstanding principals

C. A distribution of losses to tranches so that tranches bear losses in proportion to their

outstanding principals

D. None of the above

Which of the following is true when the stock price follows geometric Brownian

motion

A. The future stock price has a normal distribution

B. The future stock price has a lognormal distribution

C. The future stock price has geometric distribution

D. The future stock price has a truncated normal distribution

Which of the following is acquired (in addition to a cash payoff) when the holder of a

call futures exercises?

A. A long position in a futures contract

B. A short position in a futures contract

C. A long position in the underlying asset

D. A short position in the underlying asset

Which of the following is true?

A. The volatility skew for equities is much more pronounced now than it was in 1985.

B. The volatility skew for equities has a positive gradient

C. The volatility skew for equities is consistent with the Black-Scholes-Merton model.

D. The volatility skew for equities is similar to that for foreign currencies.

A European at-the-money put option on a currency has four years until maturity. The

exchange rate volatility is 10%, the domestic risk-free rate is 2% and the foreign

risk-free rate is 5%. The current exchange rate is 1.2000. What is the value of the

option?

A. 1.11N(0.7)-0.98N(0.5)

B. 1.11N(-0.7)-0.98N(-0.5)

C. 1.11N(0.7)-0.98N(0.4)

D. 1.11N(-0.06)-0.98N(-0.10)

Which of the following describes a futures-style option?

A. An option on a futures

B. An option on spot with daily settlement

C. A futures on an option payoff

D. None of the above

Which of the following is NOTtrue in a risk-neutral world?

A. The expected return on a call option is independent of its strike price

B. Investors expect higher returns to compensate for higher risk

C. The expected return on a stock is the risk-free rate

D. The discount rate used for the expected payoff on an option is the risk-free rate

Which of the following is acquired (in addition to a cash payoff) when the holder of a

put futures exercises?

A. A long position in a futures contract

B. A short position in a futures contract

C. A long position in the underlying asset

D. A short position in the underlying asset

A bank enters into a 3-year swap with company X where it pays LIBOR and receives

3.00%. It enters into an offsetting swap with company Y where is receives LIBOR and

pays 2.95%. Which of the following is true:

A. If company X defaults, the swap with company Y is null and void

B. If company X defaults, the bank will be able to replace company X at no cost

C. If company X defaults, the swap with company Y continues

D. The bank’s bid-offer spread is 0.5 basis points

The chapter discusses an alternative to the Cox, Ross, Rubinstein tree. In this

alternative, which of the following are true:

A. The relationship between u and d is: u=1/d

B. The relationship between u and d is: u-1=1-d

C. The probabilities on the tree are all 0.5

D. None of the above

A silver mining company has used futures markets to hedge the price it will receive for

everything it will produce over the next 5 years. Which of the following is true?

A. It is liable to experience liquidity problems if the price of silver falls dramatically

B. It is liable to experience liquidity problems if the price of silver rises dramatically

C. It is liable to experience liquidity problems if the price of silver rises dramatically or

falls dramatically

D. The operation of futures markets protects it from liquidity problems

If the CDS-bond basis is X minus Y, what are X and Y?

A. X is the CDS spread and Y is the excess of the bond yield over the swap rate

B. X is the excess of the bond yield over the swap rate and Y is the CDS spread

C. X is the CDS spread and Y is the excess of the bond yield over the Treasury rate

D. X is the excess of the bond yield over the Treasury rate and Y is the CDS spread

Which of the following best describes the intrinsic value of an option?

A. The value it would have if the owner had to exercise it immediately or not at all

B. The Black-Scholes-Merton price of the option

C. The lower bound for the option€s price

D. The amount paid for the option