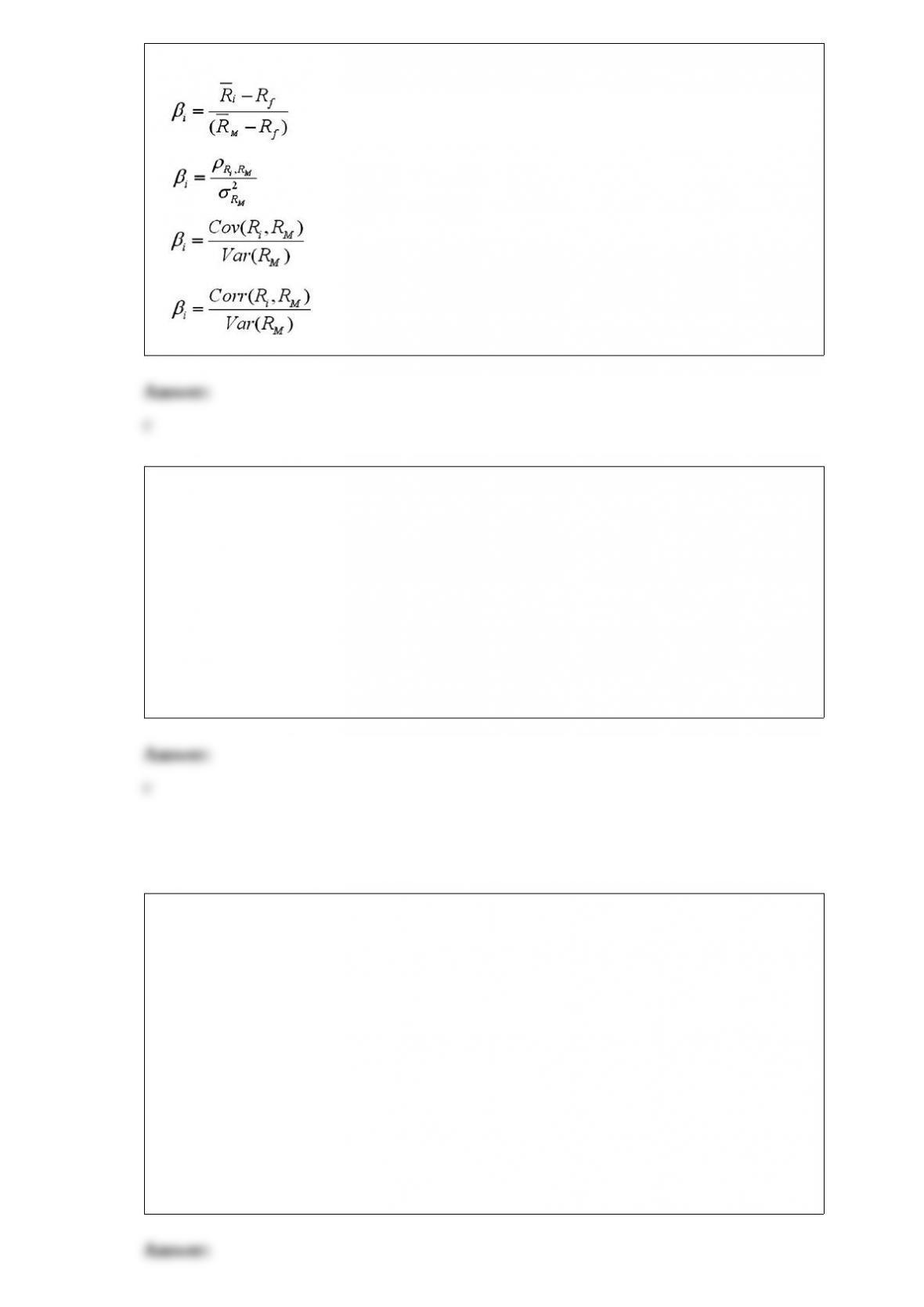

1) the formula for beta is:

a.

b.

c.

d.

2) suppose the face amount of a promissory note is $1,000,000 and the importer’s bank

charges an acceptance commission of 1.5 percent. the note is for 60 days. calculate the

amount of the acceptance commission that the bank will charge.

a.$997,500

b.$15,000 = $1,000,000 (0.015)

c.$2,500

d.none of the above

3) when designing an incentive contract,

a.it is important for the board of directors to set up an independent compensation

committee that can carefully design the contract and diligently monitor manager’s

actions

b.senior executives can be trusted to not abuse incentive contracts by artificially

manipulating accounting numbers since the auditors should look in to that

c.the presence of any incentive is enough, whether it is accounting based or stock-price

based

d.the board of directors should always give the managers a “heads i win, tails you lose”

type of option

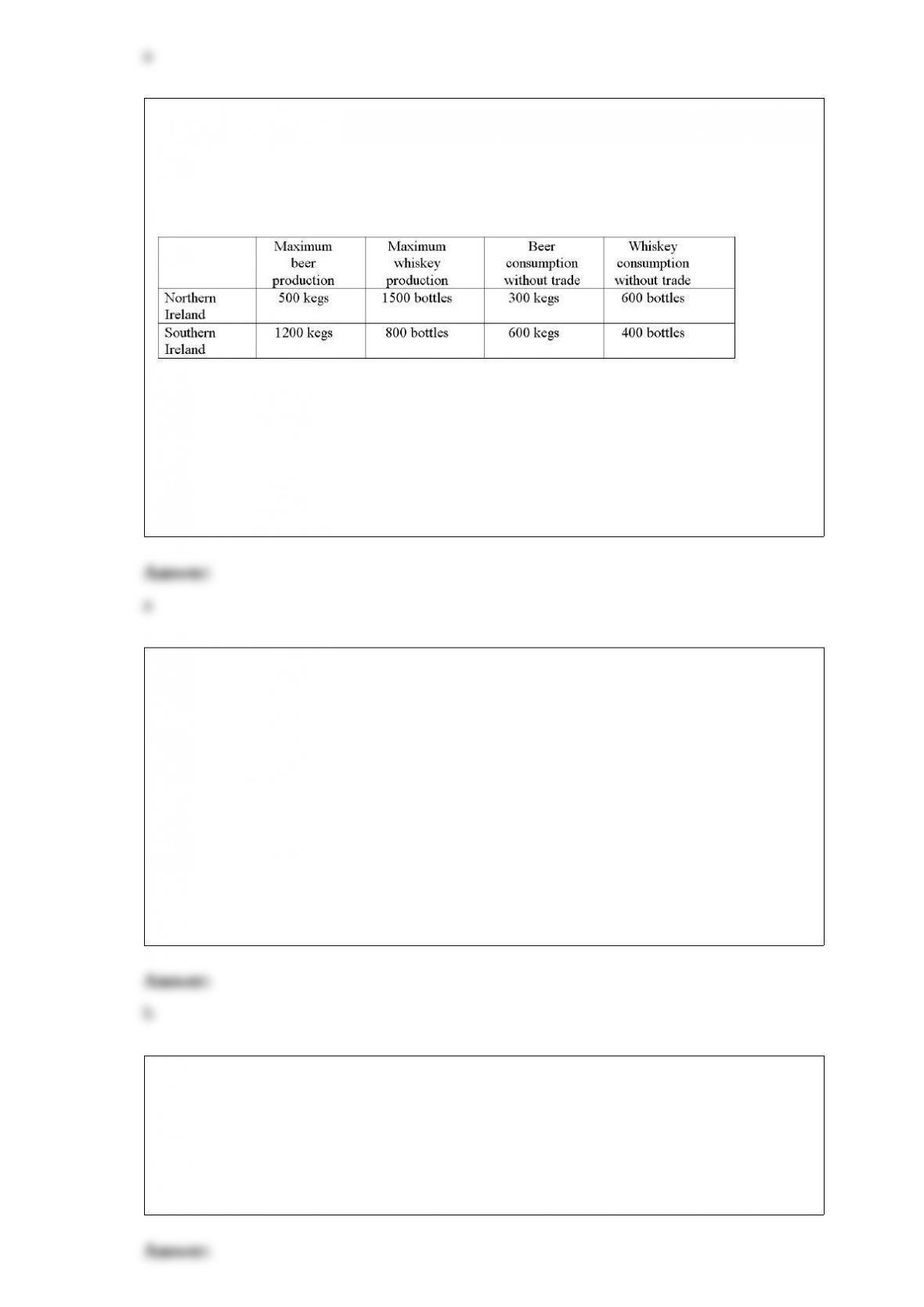

4) the first two columns give the maximum daily amounts of beer and whiskey that

southern ireland and northern ireland can produce when they completely specialize in

one or other product. the last two columns give each country’s consumption without

trade.

what is the increased amount of goods available in northern ireland after trade?

a.400 more bottles of whiskey and 200 more kegs of beer

b.1,000 more bottles of whiskey and 500 more kegs of beer

c.200 more bottles of whiskey and 400 more kegs of beer

5) considering the fact that many barriers to international portfolio investments have

been dismantled in recent years,

a.capital market imperfections as a motivating factor for fdi are likely to become more

important going forward

b.capital market imperfections as a motivating factor for fdi are likely to become less

relevant

c.labor market imperfections as a motivating factor for fdi are likely to become less

relevant

d.none of the above

6) the /$ spot exchange rate is $1.50/ and the 90-day forward premium is 10 percent.

find the 90-day forward price.

a.$1.65/

b.$1.5375/

c.$1.9125/

d.none of the above

7) the return and variance of return to a u.s. dollar investor from investing in individual

foreign security i are given by:

a.ri$ = (1 + ri)(1 + ei) – 1 and var(ri$) = var(ri)

b.ri$ = ri + ei and var(ri$) = var(ri) + var(ei)

c.ri$ = (1 + ri)(1 + ei) – 1 and var(ri$) = var(ri) + var(ei) + 2cov(ri,ei)

d.none of the above

8) under the terms of islamic finance (shari’ah law)

a.selling debt at a reduced value is strictly forbidden

b.charging interest is ok, but short selling stock is forbidden

c.buying low and selling high is forbidden

d.none of the above

9) suppose that the annual interest rate is 2.0 percent in the united states and 4 percent

in germany, and that the spot exchange rate is $1.60/ and the forward exchange rate,

with one-year maturity, is $1.58/. assume that an arbitrager can borrow up to

$1,000,000 or 625,000. if an astute trader finds an arbitrage, what is the net cash flow in

one year?

a.$238.65

b.$14,000

c.$46,207

d.$7,000

10) which factors fuel the sale of “yankee” stock offerings?

a.privatization by many latin american and eastern european government-owned

companies

b.the rapid growth in the economies of the developing world

c.the expected large demand for new capital by mexican companies now that nafta has

been approved

d.all of the above

11) suppose that the exchange rate is 1.25 = £1.00.

options (calls and puts) are available on the london exchange in units of 10,000 with

strike prices of £0.80 = 1.00. options (calls and puts) are available on the frankfurt

exchange in units of £10,000 with strike prices of 1.25 = £1.00. for a u.k. firm to hedge

a 100,000 receivable,

a.buy 10 call options on the euro with a strike in pounds sterling

b.buy 8 put options on the pound with a strike in euro

c.buy 10 put options on the euro with a strike in pounds sterling

d.buy 8 call options on the pound with a strike in euro

e.both a and b

f.both c and d

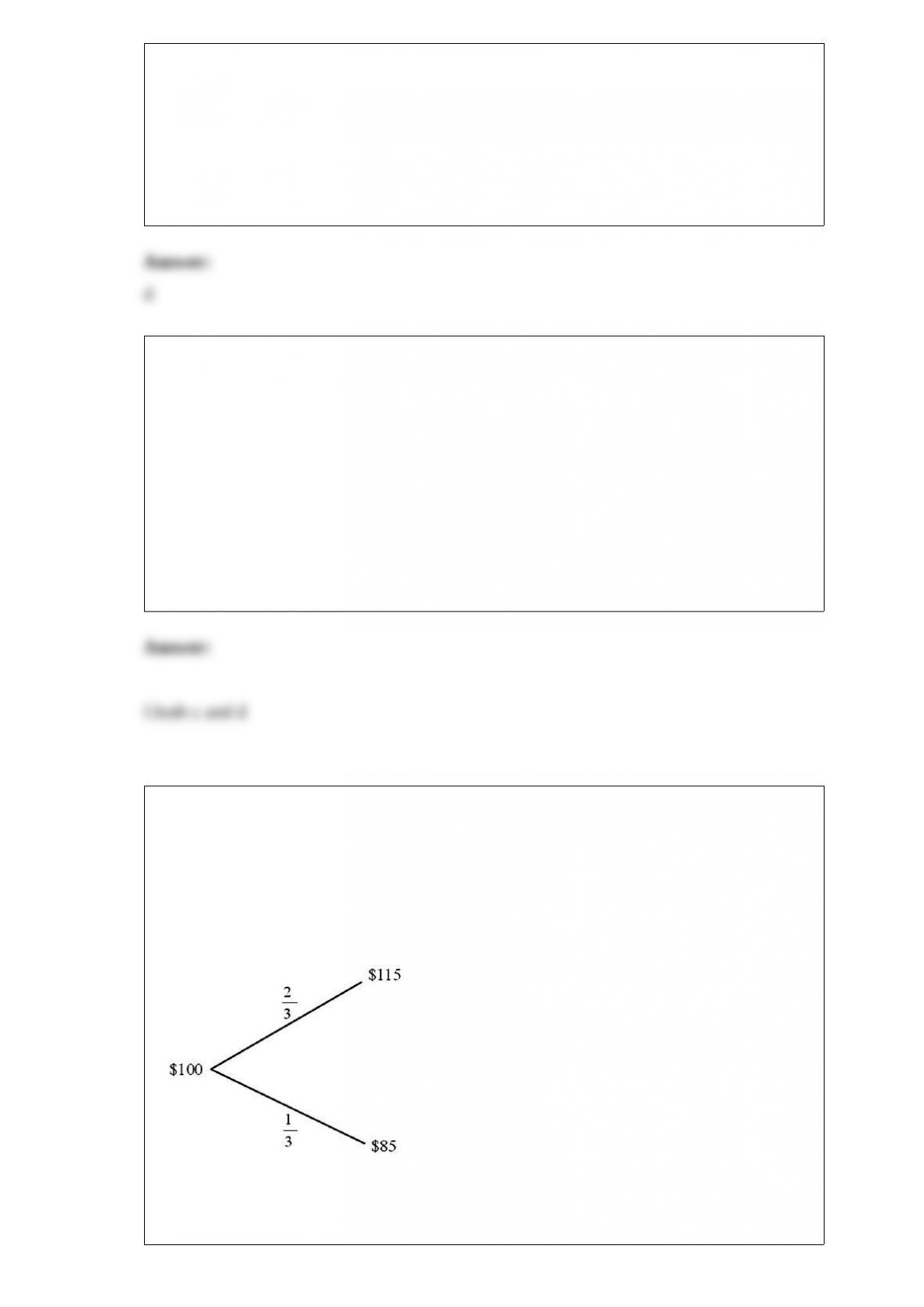

12) find the value of a call option written on 100 with a strike price of $1.00 = 1.00. in

one period there are two possibilities: the exchange rate will move up by 15% or down

by 15% (i.e. $1.15 = 1.00 or $0.85 = 1.00). the u.s. risk-free rate is 5% over the period.

the risk-neutral probability of dollar depreciation is 2/3 and the risk-neutral probability

of the dollar strengthening is 1/3.

a.$9.5238

b.$0.0952

c.$0

d.$3.1746

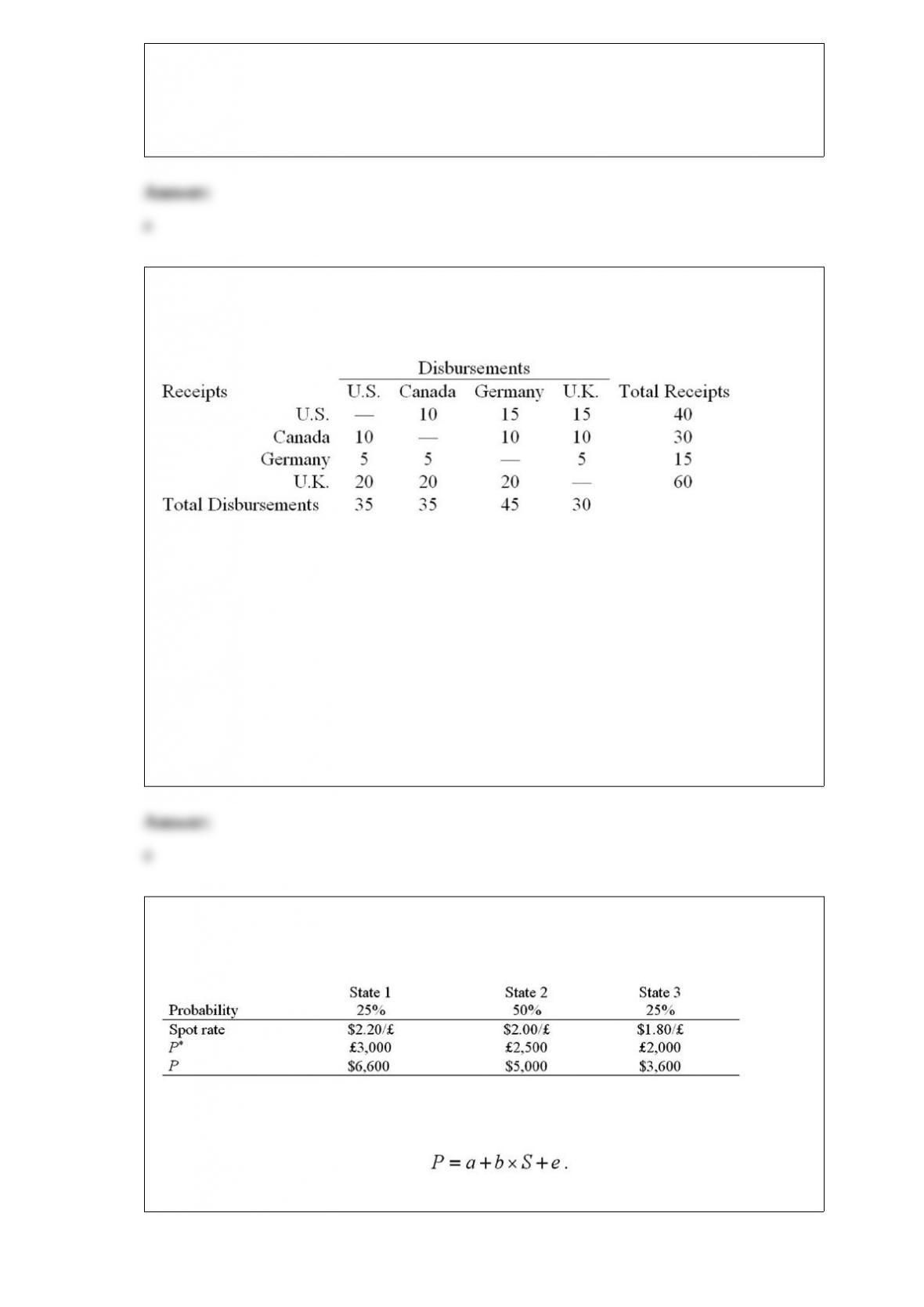

13) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

find the net cash flow for the entire firm

a.$0 in or out

b.$5,000 out

c.$30,000 in

d.$30,000 out

e.none of the above

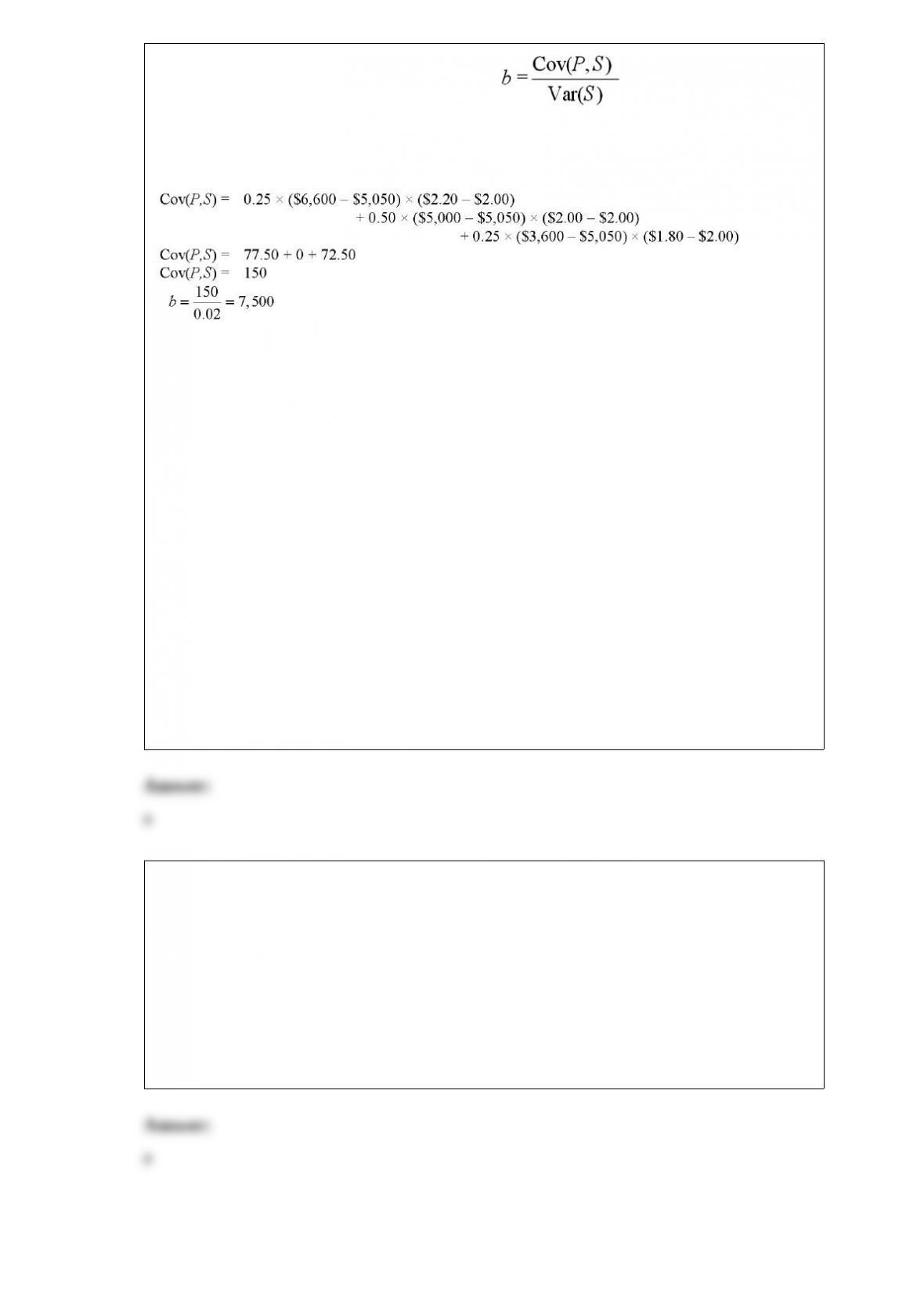

14) find an effective hedge financial hedge if a u.s. firm holds an asset in great britain

and faces the following scenario:

p* = pound sterling price of the asset held by the u.s. firm

p = dollar price of the same asset

the cfo runs a regression of the form

the regression coefficient beta is calculated as

where

the variance of the exchange rate is calculated as:

e(s) = 0.25 $2.20 + 0.50 $2.00 + 0.25 $1.80 = $.55 + $1 + $.45 = $2.00

var(s) = 0.25($2.20 – $2.00)2 + 0.50($2.00 – $2.00)2 + 0.25($1.80 – $2.00)2 = 0.01 + 0

+ 0.01

= 0.02

the expected value of the investment in u.s. dollars is:

e[p] = 0.25 $6,600 + 0.50 $5,000 + 0.25 $3,600 = $5,050

which of the following is the most effective hedge financial hedge?

a.sell £7,500 forward at the 1-year forward rate, f1($/£), that prevails at time zero

b.buy £7,500 forward at the 1-year forward rate, f1($/£), that prevails at time zero

c.sell £2,500 forward at the 1-year forward rate, f1($/£), that prevails at time zero

d.0.25 £3,000 + 0.50 £2,500 + 0.25 £2,000 = £2,500

15) the withholding tax on bond income was originally called the interest equalization

tax.

a.you can thank john f. kennedy for imposing this tax

b.you can thank ronald reagan for imposing this tax

c.you can thank jimmy carter for imposing this tax

d.you can thank george washington for imposing this tax