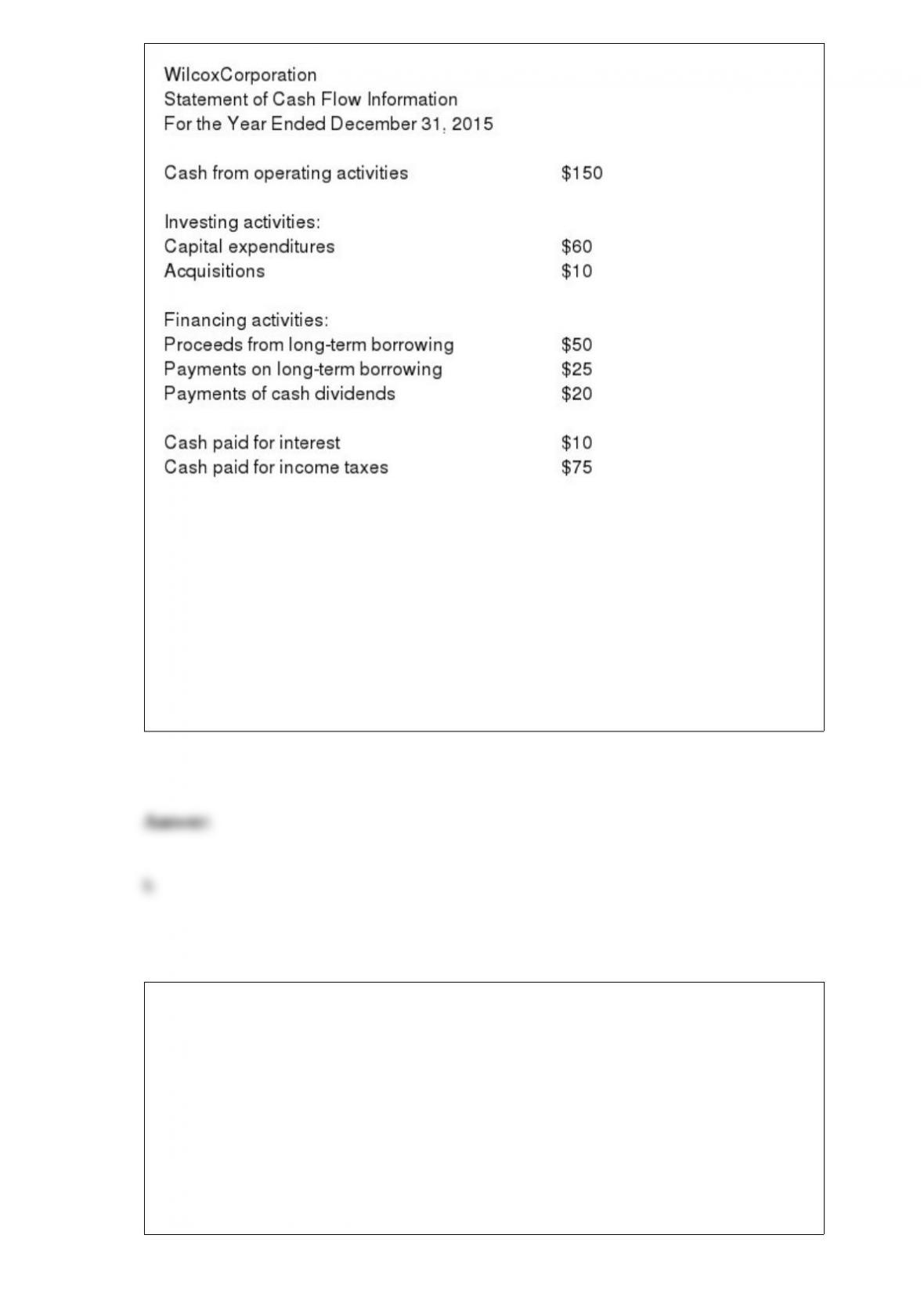

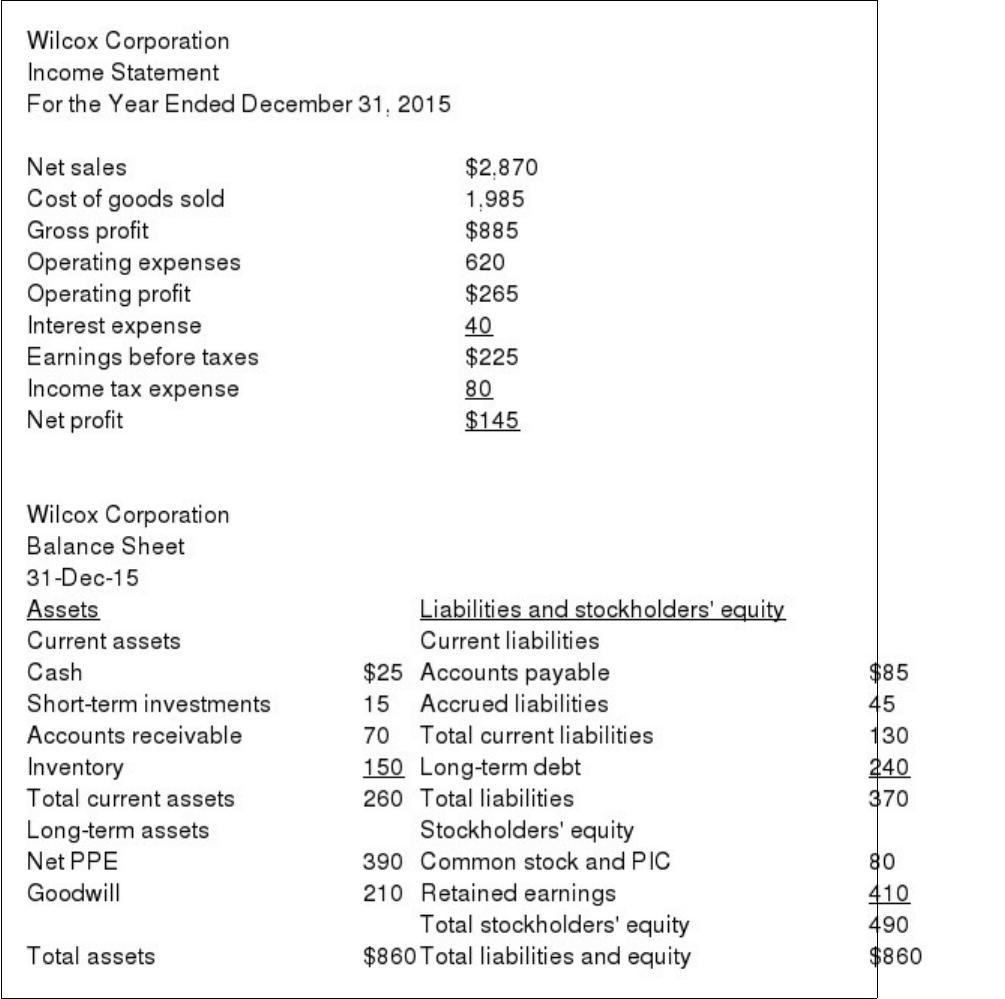

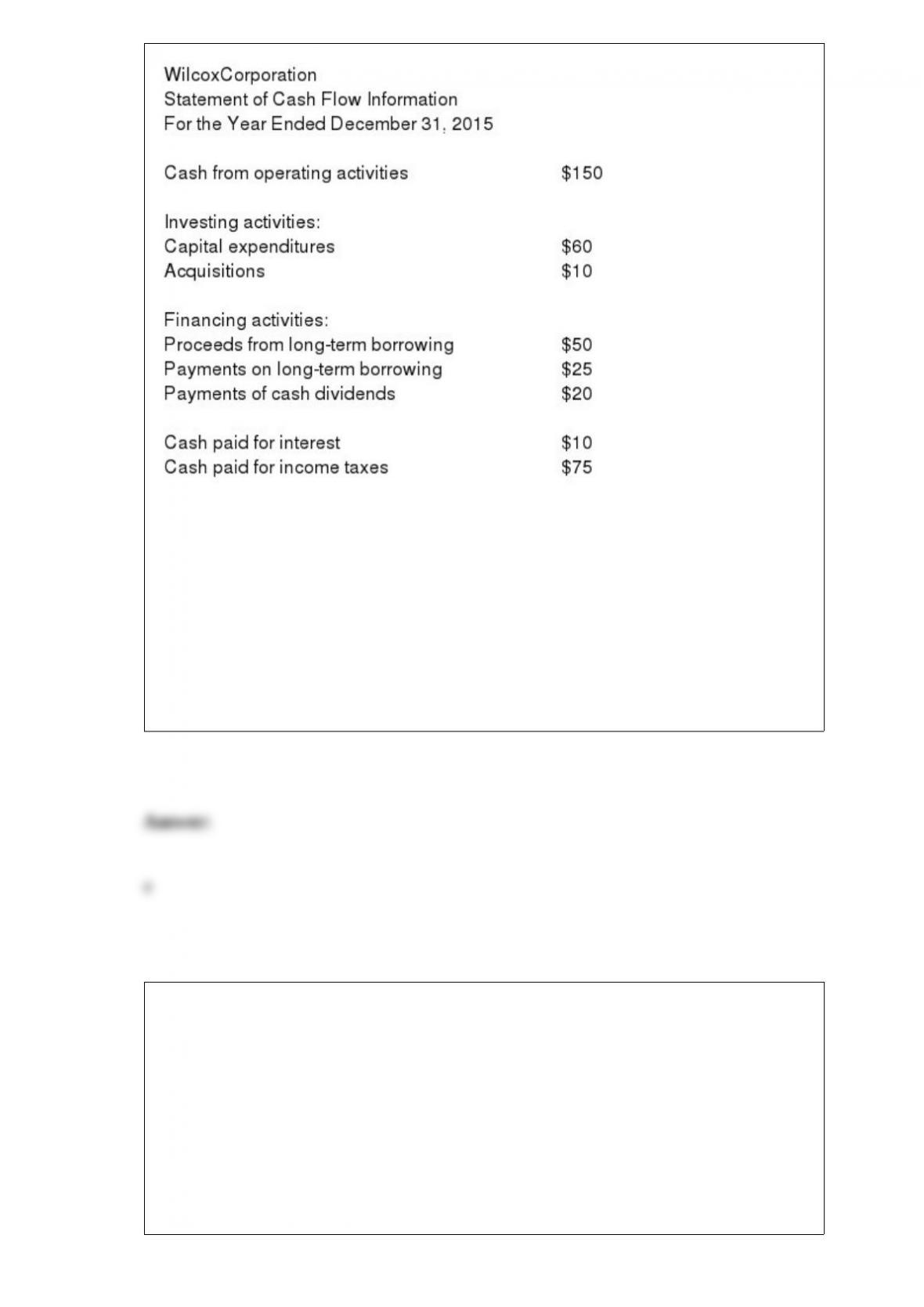

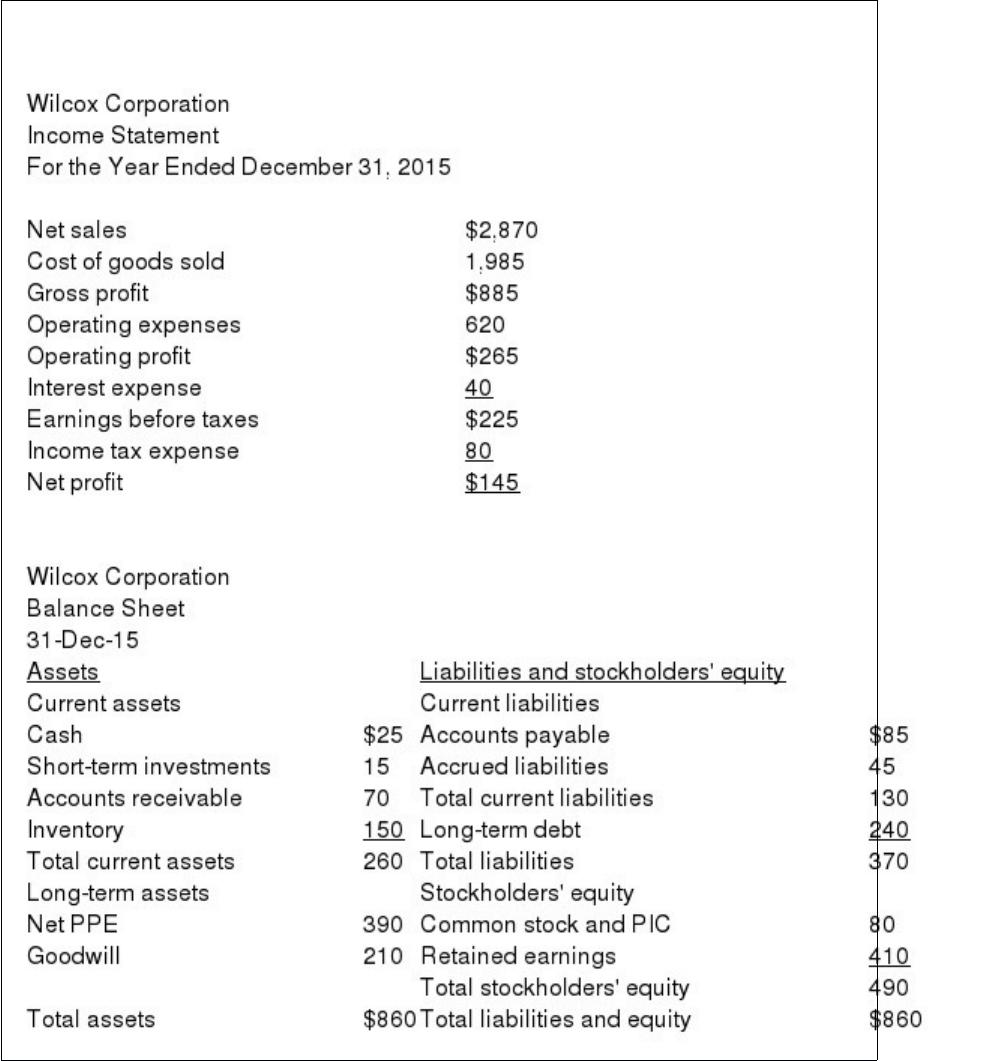

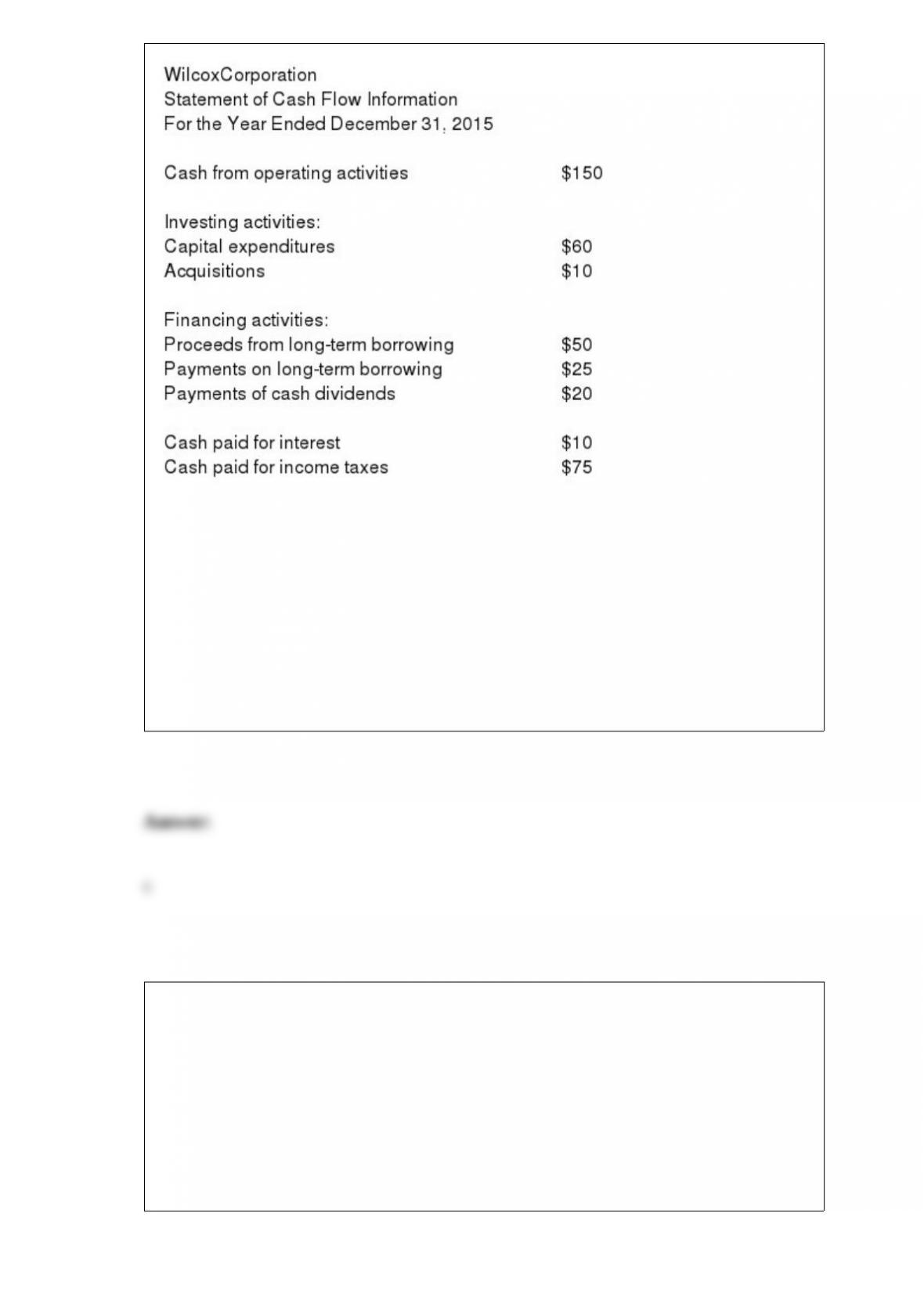

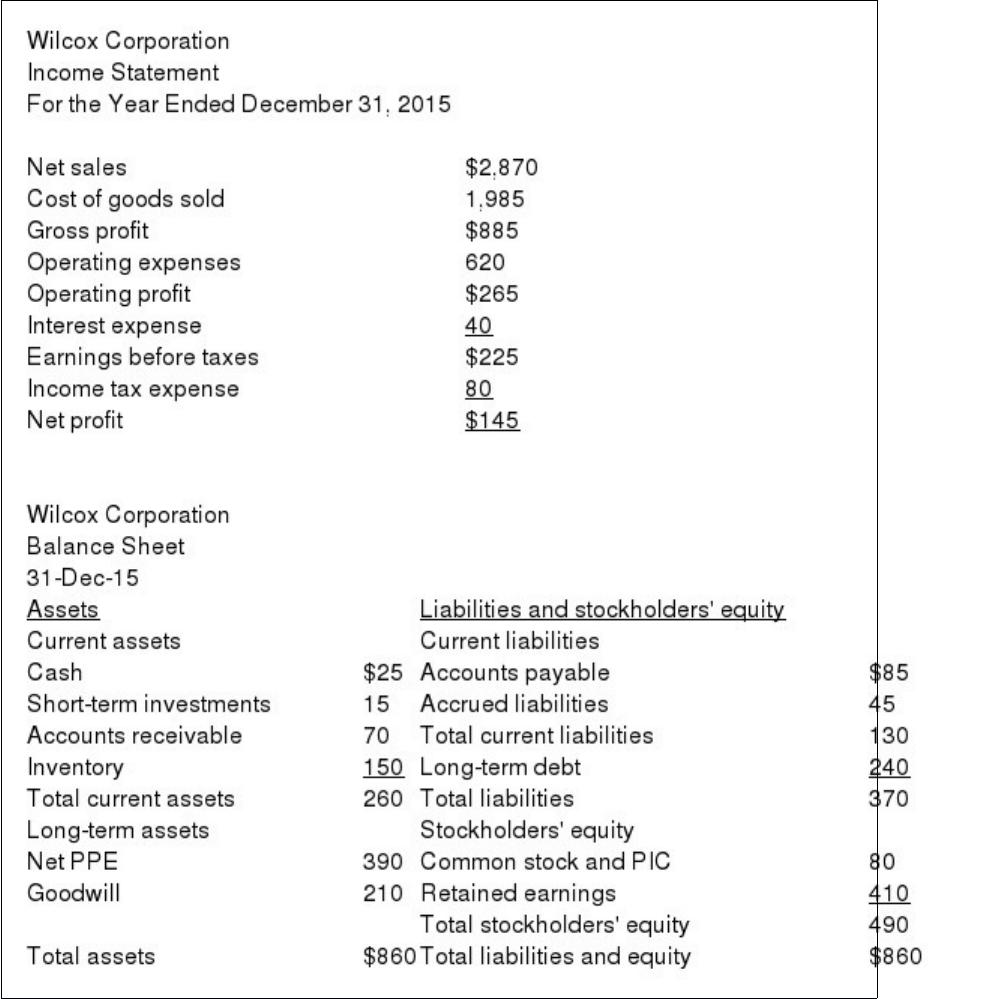

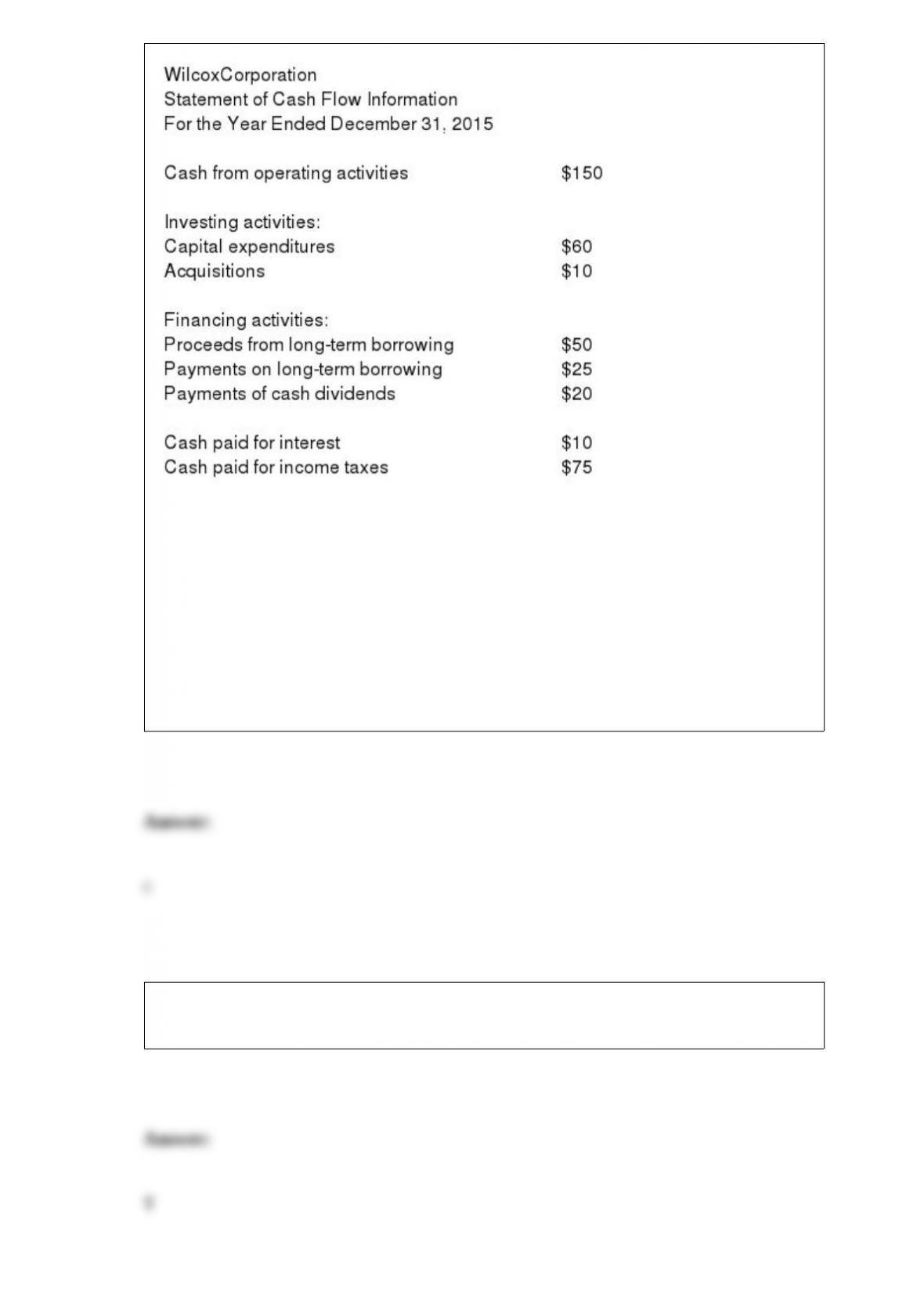

Wilcox’s debt ratio is:

a. 40.11%

b. 43.02%

c. 55.80%

d. 56.32%

Which of the following is not a condition that must be met for an item to be recorded as

revenue?

a. Revenues must be earned.

b. The amount of the revenue must be measurable.

c. The revenue must be received in cash.

d. The costs of generating the revenue can be determined.

Identify the following as operating (O), financing (F), or investing (I) activities:

a. Proceeds from borrowing

b. Purchases of property, plant and equipment

c. Cash from sale of a business segment

d. Interest payments to lenders

e. Cash from sales of goods and services

f. Payment of dividends

g. Payments for purchase of inventory

h. Payments for taxes

i. Repurchase of a firm’s own shares

j. Cash collections from loans to others

All of the following are steps of a financial statement analysis except:

a. Establish objectives of the analysis.

b. Prepare pro forma statements.

c. Study the industry in which the firm operates.

d. Develop knowledge of the firm and the quality of management.

The Breakfast Company purchases equipment for $100,000. Management estimates that

the equipment will have a useful life of eight years and no salvage value.

a. Calculate depreciation expense and the book value of the equipment at the end of the

first year using the straight-line method of depreciation.

b. Calculate depreciation expense and the book value at the end of the first year using

the double-declining balance method of depreciation.

Wilcox’s cash flow margin is:

a. 5.23%

b. 5.85%

c. 6.24%

d. 6.67%

How does the equity method distort earnings?

a. Income is recognized even though cash may never be received.

b. Equity earnings are recorded even if the investor cannot exercise influence over the

investee’s policies.

c. Equity earnings are only recorded on a cash basis of accounting.

d. Equity earnings are recorded when investment ownership is 100%.

According to Section 302 of the Sarbanes-Oxley Act, who must certify the accuracy of

the financial statements of a public company?

a. Public Company Accounting Oversight Board.

b. SEC.

c. External auditor.

d. CEO and CFO.

RBO Company purchased 25% of the voting common stock of YJD Company on

January 1 and paid $800,000 for the investment. YJD Company reported $50,000 of

earnings for the year and paid $10,000 in cash dividends. Calculate investment income

and the balance sheet investment account balance for RBO Company using the

following methods:

a. Cost method.

b. Equity method.

Which of the following items should alert the analyst to the potential for manipulation

when analyzing accounts receivable and the allowance for doubtful accounts?

a. Sales, accounts receivable and the allowance for doubtful accounts are all growing at

approximately the same rate.

b. A company lowers its credit standards and also increases the balance in the allowance

for doubtful accounts.

c. Accounts receivable is growing at a large rate and the allowance for doubtful

accounts is decreasing.

d. An analysis of the ‘Valuation and Qualifying Accounts’ schedule required in the Form

10-K reveals that the amounts recorded for bad debt expense are close in amount to the

actual amounts written off each year.

The following categories of ratios are used in financial statement analysis:

a. Liquidity

b. Operating efficiency (also referred to as Activity)

c. Leverage

d. Profitability

e. Market measures

Classify the following ratios according to the above categories:

(1) Dividend payout

(2) Fixed charge coverage

(3) Cash flow margin

(4) Days inventory held

(5) Times interest earned

(6) Net profit margin

(7) Earnings per share

(8) Fixed asset turnover

(9) Total asset turnover

(10) Current ratio

Wilcox’s times interest earned ratio is:

a. 1.50

b. 4.50

c. 6.63

d. 8.60

How is a common-size income statement prepared?

a. Each income statement item is expressed as a percentage of total assets.

b. Each income statement item is expressed as a percentage of net sales.

c. Each income statement item is expressed as a percentage of net income.

d. Each income statement item is expressed as a percentage of cash flow.

Which of the following would increase cash from operating activities?

a. Increasing accounts receivable.

b. Increasing inventories.

c. Decreasing accounts payable.

d. Decreasing accounts receivable.

Which of the following is an external source of liquidity?

a. Sales of services.

b. Repurchase of stock.

c. Borrowing.

d. Sales of products.

Which group of people would be the most concerned about the ability of a firm to make

interest and principal payments?

a. Auditors.

b. Customers.

c. Creditors.

d. Investors.

What is amortization?

a. The process used to allocate the cost of natural resources.

b. The process used to allocate the cost of tangible fixed assets.

c. The process used to allocate the cost of capital leases, leasehold improvements and

intangible assets.

d. The process used to allocate the cost of oil, gas, minerals and standing timber.

Wilcox’s return on equity is:

a. 20.62%

b. 25.50%

c. 29.59%

d. 28.49%

Cash flow from operations represents the ‘cash’ income from the company’s business

operations.

The gross profit margin is increasing for a firm. Give three reasons that could explain

the increase.

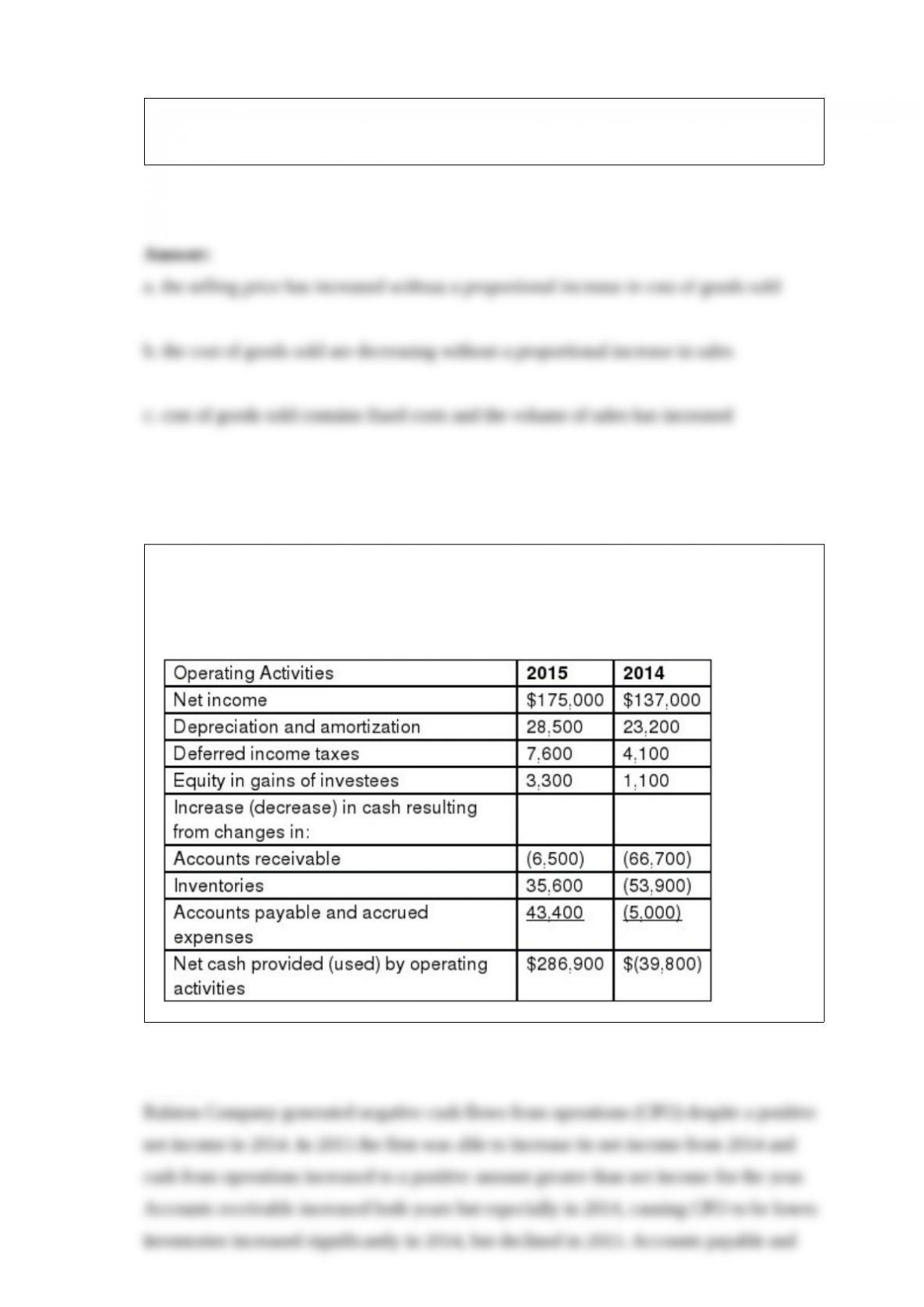

Using the excerpt from the Ralston Company statement of cash flows analyze

thoroughly the cash flow from operating activities. Be sure to offer possible reasons for

the changes identified.

Proceeds from borrowing are a financing cash outflow.

charges are the expenses recognized to record a decline in value of a long-term asset.

The statement of stockholders’ equity is an important link between the balance sheet

and the income statement.

GAAP-based financial statements are prepared according to the accrual basis of

accounting.

Articles from current business periodicals should not be used in financial statement

analysis as journalists are often biased.