Select the correct statement from the following:

a. Consolidation worksheet adjustments are not entered on the accounting records of

either Parent or Sub.

b. Consolidation worksheet adjustments are entered on the accounting records of the

Parent but not the Sub.

c. Consolidation worksheet adjustments are entered on the accounting records of the

Sub but not the Parent.

d. Consolidation worksheet adjustments are entered on the accounting records of both

the Parent and the Sub.

A passive investment is one in which the owner

a. is not attempting to exert influence over the company.

b. owns between 15-25% of the company’s outstanding stock.

c. uses the equity method of accounting for the investment.

d. is gradually attempting to gain control over the company.

Which internal control activity is followed when the work of one department acts as a

check on the work of another?

a. segregation of duties

b. safeguarding of assets and records

c. checks on recorded amounts

d. clearly defined authority and responsibility

Refer to Academy Grill Supply. The effect on the company’s financial statements on

December 31, 2013is as follows

Academy Grill Supply

On October 1, 2013, the company received a $50,000 promissory note from a customer.

The annual interest rate is 6%. Principal and interest will be collected in cash at the

maturity date of September 30, 2013. a. assets and Stockholders’ equity increase.

b. assets and Stockholders’ equity decrease.

c. assets and liabilities increase.

d. no net change in assets.

On January 2, 2013, Kampai Sushi Bar sold $800,000 of bonds for $785,000. The

bonds will mature in 10 years and pay interest annually on December 31. The company

properly recorded the payment of interest and amortization of the discount using the

effective interest method. Which of the following statements is true about the carrying

value of the bonds and/or the unamortized discount at the end of 2013?

a. The carrying value will be less than $785,000.

b. The carrying value will be $785,000.

c. The carrying value will be greater than $785,000.

d. The unamortized premium will be more than $15,000.

Used to induce the customer to keep damaged goods

Select the term that matches each of the following descriptions.

a. Sales Discount

b. Trade Discount

c. Sales Allowance

d. Sales Returns

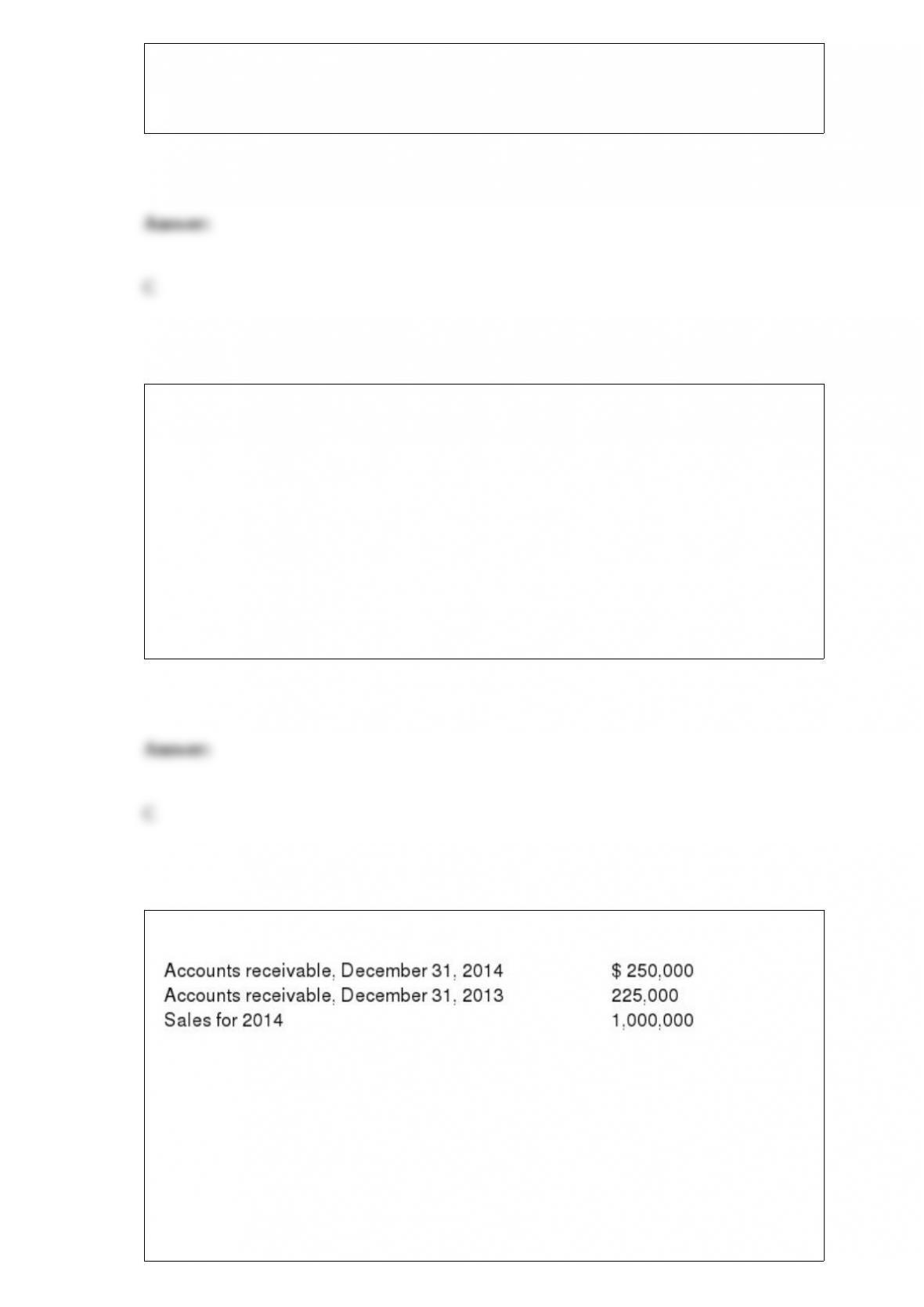

The following items were reported by Morris Plumbing Company:

What amount would be reported in the operating activities section of the statement of

cash flows for Collections from Customers under the direct method, assuming that all

sales are on credit?

a. $975,000

b. $1,025,000

c. $1,225,000

d. $1,250,000

The length of time a note is outstanding-the period of time between the date it is issued

and the date the note is due to be paid

Select the term that matches each of the following descriptions.

a. Interest

b. Maturity Value

c. Principal

d. Lender

e. Factoring

f. Fraction of year

g. Maturity date

h. Implicit

i. Maker

Which of the following statements is true regarding just-in-time inventory

management?

a. It requires a perpetual inventory system.

b. It requires an average cost inventory costing method.

c. It requires detailed information about profitability and the users of the company’s

financial statements.

d. It requires detailed information about order-to-delivery times, receiving-to-sales

times, and inventory quantities.

Which of the following types of information is not set forth within the corporate

charter?

a. Name and purpose of the corporation.

b. Names of those responsible for incorporating the business.

c. Dates of future dividend distributions.

d. Provisions describing how stock may be issued.

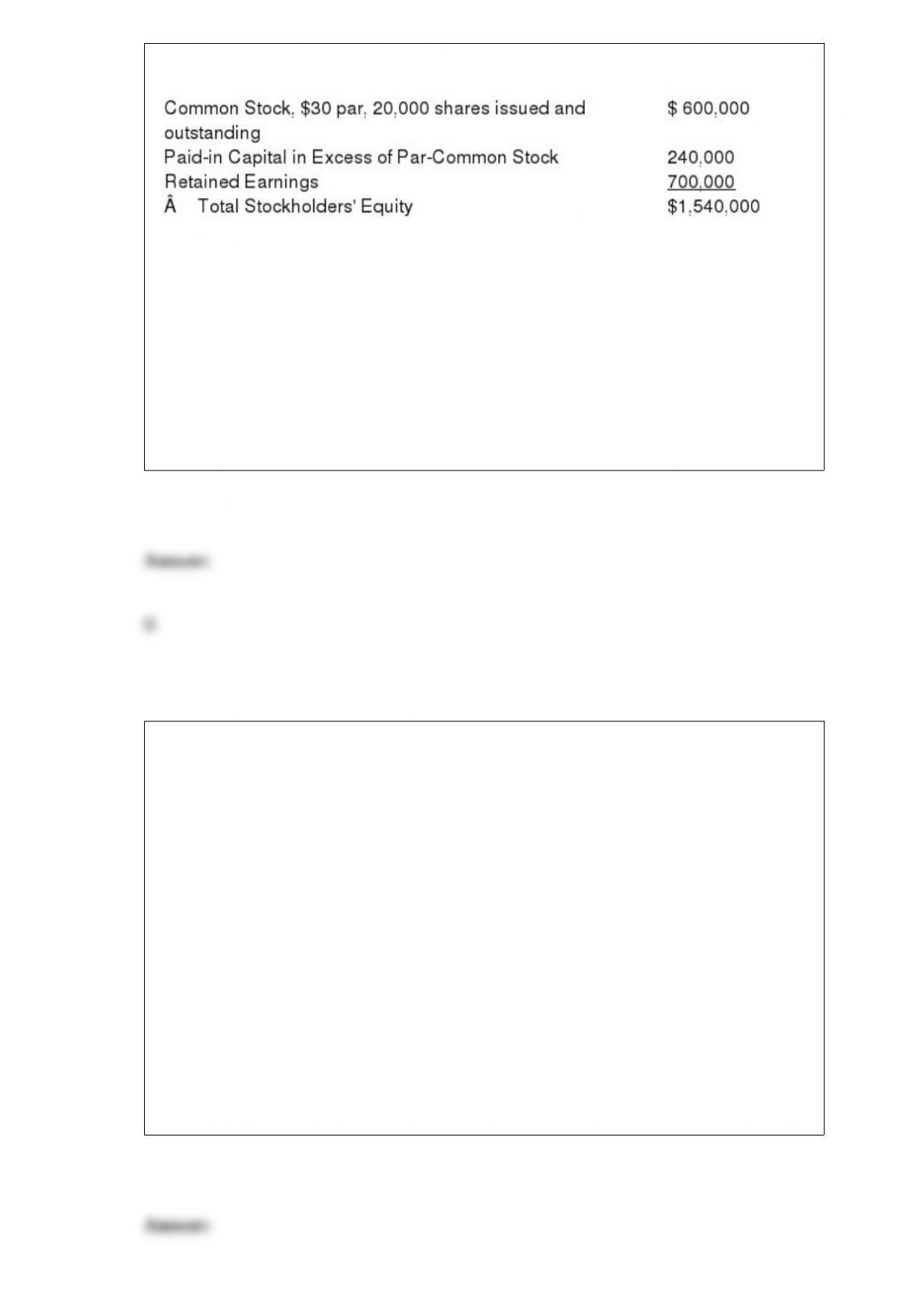

Refer to Ladder Distributors. Suppose the company reissued 1,000 shares of its treasury

stock on June 1, 2015, for $44 each. Which of the following is true regarding the entry

required to record this transaction?

Ladder Distributors

The stockholders’ equity section of the December 31, 2014, balance sheet is provided

below:

Assume that all of the 20,000 shares of stock that was issued as of December 31, 2014,

was issued for $42 per share. On March 1, 2015, the company reacquired 4,000 shares

of its common stock for $50 per share. a. A debit to treasury stock is required for

$44,000.

b. A credit to treasury stock is required for $50,000.

c. A credit to retained earnings is required for $6,000.

d. A debit to paid-in capital from treasury stock transactions is required for $6,000.

The following costs were incurred to acquire and prepare land for a new parking lot:

purchase price for land, cost to clear the land, cost of paving, cost of lighting for the

parking lot, and cost of landscaping for the parking lot. How should the company

determine which costs should be recorded as Land Improvements and which costs

should be recorded as Land?

a. The costs with an unlimited life are debited to Land, and the costs with a limited

useful life are debited to Land Improvements.

b. The costs with a limited life are debited to Land, and the costs with an unlimited

useful life are debited to Land Improvements.

c. The costs to be depreciated are debited to Land, and the costs that will not be

depreciated are debited to Land Improvements

d. Costs that are depreciable are debited to Land Improvements, while other costs are

expensed immediately because of a lack of definite life.

Cash flows from issuing and repurchasing stock or issuing and repaying debt are

classified as

a. operating activities.

b. investing activities.

c. financing activities.

d. borrowing activities.

Failure to record amounts earned for services provided to customers but not yet paid

results in which of the following?

a. Net income being overstated.

b. No effect on total assets.

c. Stockholders’ equity being overstated.

d. Total assets being understated.

When a corporation decides whether to pay a cash dividend, which of the following is

an important consideration?

a. The balances in the corporation’s cash and retained earnings accounts.

b. The number of authorized shares of the corporation’s stock.

c. The book value of the corporation’s stock.

d. The balance of paid-in capital in excess of par on the corporation’s stock accounts.

If a company accepts a major credit card such as VISA from a customer, then the

company is responsible for the amount of the sale in a case of nonpayment from a

cardholder.

When a company recognizes the portion of supplies used during a year, the effect is to

decrease net income.

When reconciling a bank account, the company has to prepare an adjusting entry for

outstanding checks.

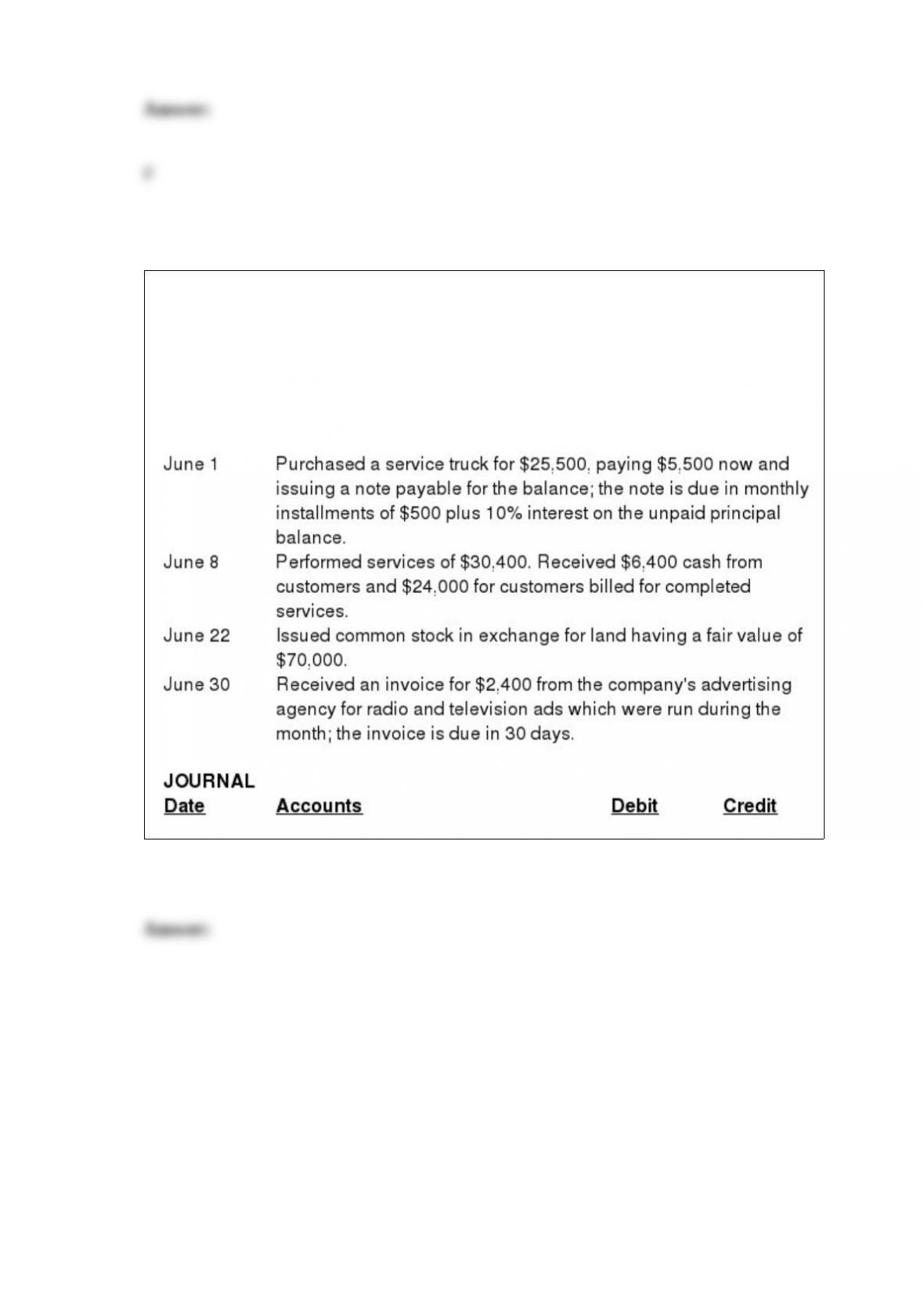

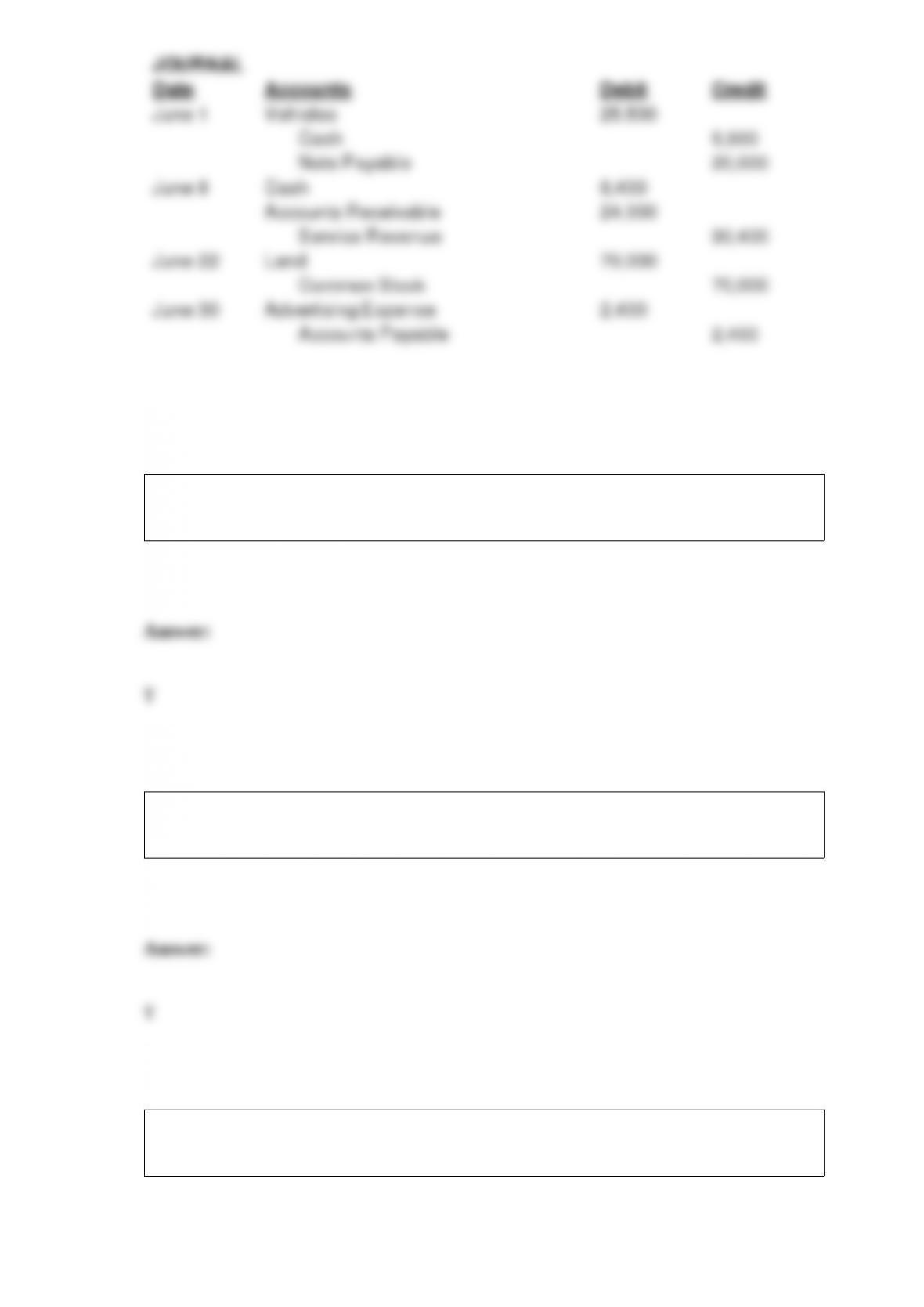

Refer to Hatcher Tool Service. Record each transaction in proper journal entry format in

the journal provided. A written explanation for each journal entry is not required.

Hatcher Tool Service

The following transactions occurred during June 2013:

Cash flows that are equal and occur multiple times, one period apart are called

Annuities.

The balance in the account, Rent Collected in Advance, is reported as a liability on the

balance sheet of the landlord.

If preferred stock is convertible, then the preferred shareholders have the option to trade

voting privileges for the dividend payment preference.

All intangible assets are subject to amortization.

A company with healthy cash flows from operating activities is in a good position to

repay its debts.