Which one of the following advance/decline lines is the most bullish signal?

A. relatively flat

B. slightly upward sloping

C. slightly downward sloping

D. steeply upward sloping

E. steeply downward sloping

What is the percentage of a firm’s net income which is reinvested in the firm to support

future growth called?

A. payout ratio

B. distribution percentage

C. retention ratio

D. equity ratio

E. equity reinvestment

Which of the following issue exchange-listed option contracts?

I. CBOE

II. SEC

III. OCC

IV. NASDAQ

A. III only

B. IV only

C. I and III only

D. II and IV only

E. I, II, and III only

Explain the similarities and differences between the Sharpe and Treynor ratios. Also,

explain the most appropriate application for each.

Which one of the following had the highest risk premium for the period 1926-2012?

A. U.S. Treasury bills

B. long-term government bonds

C. large-company stocks

D. small-company stocks

E. intermediate-term government bonds

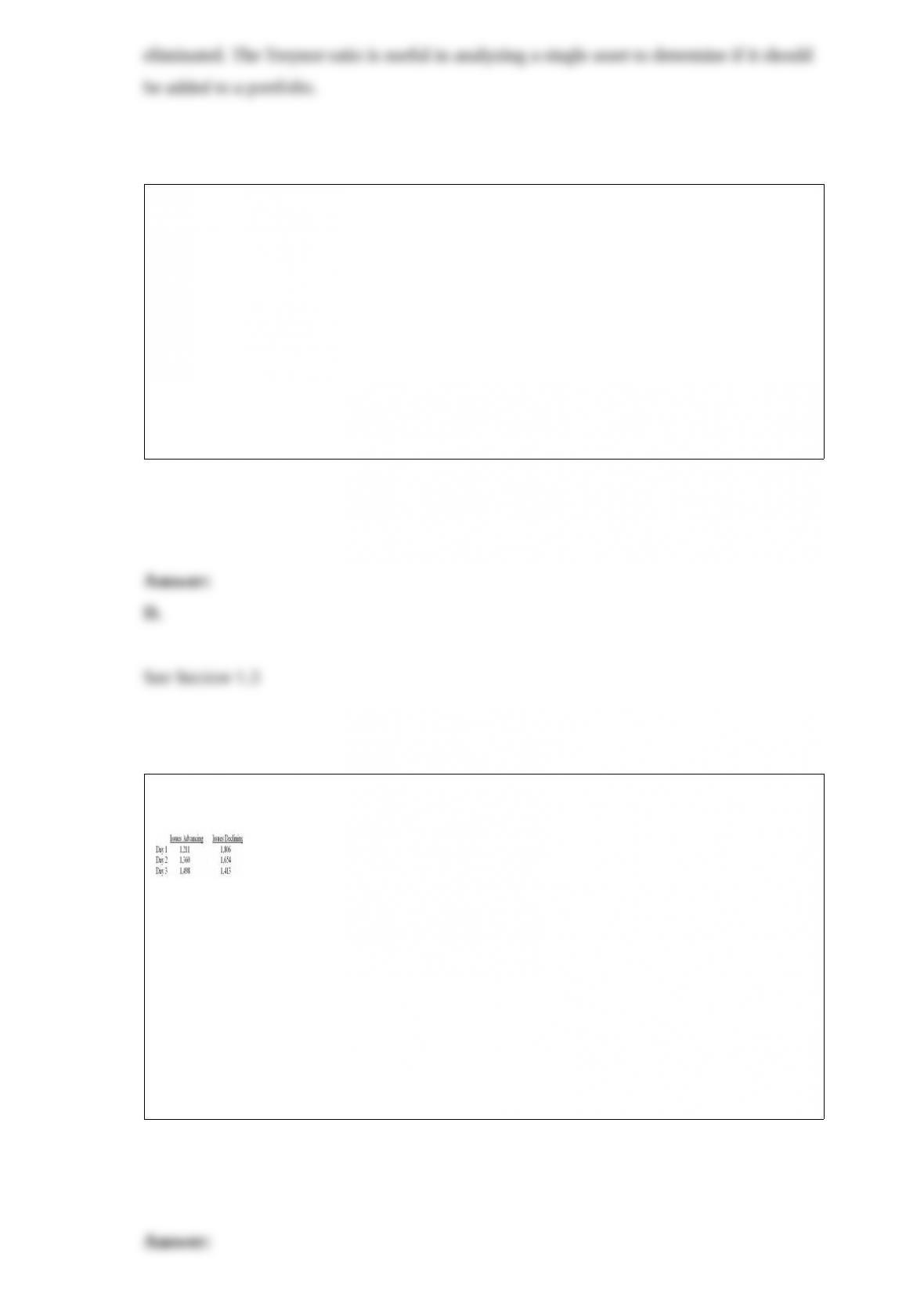

Given the following information, what is the value of the advance/decline line on the

second day of this 3-day period?

A. -889

B. -804

C. -294

D. +147

E. +402

Which one of the following is correct concerning the total payment amount on a PO

strip?

A. The total payment amount equals the bond’s par value.

B. The total payment amount will either equal or exceed the bond’s par value.

C. The total payment will vary based on the PSA schedule.

D. The total payment amount will increase if interest rates decline.

E. The total payment amount will vary if the prepayment rate varies.

A diversified portfolio has a beta of 1.47 and a raw return of 14.28 percent. The market

return is 11.74 percent and the market risk premium is 7.85 percent. What is Jensen’s

alpha of the portfolio?

A. -1.15 percent

B. -0.86 percent

C. -0.29 percent

D. 0.48 percent

E. 0.62 percent

When the price of newly issued shares is determined by competitive bidding the

underwriting is known as a _____ underwriting.

A. Dutch auction

B. market-priced

C. seasoned

D. best efforts

E. rights

A stock sold for $25 at the beginning of the year. The end of year stock price was

$25.70. What is the amount of the annual dividend if the total return for the year was

7.7 percent?

A. $1.23

B. $1.38

C. $1.60

D. $1.81

E. $2.31

What is the document called that is distributed to potential bondholders and provides

detailed information on the financial position and operations of the bond issuer?

A. indenture summary

B. prospectus

C. trust statement

D. 10K

E. 10Q

Allan purchased 800 shares of stock on margin for $31 a share and sold the shares five

months later for $33.50 a share. The initial margin requirement was 65 percent and the

maintenance margin was 30 percent. The interest rate on the margin loan was 7.5

percent. He received no dividend income. What was his holding period return?

A. 7.05 percent

B. 8.45 percent

C. 9.88 percent

D. 10.76 percent

E. 11.82 percent

You are comparing three securities and discover they all have identical Treynor ratios.

Given this information, which one of the following must be true regarding these three

securities?

A. They have identical betas.

B. They have the same rates of return.

C. They earn identical rewards per unit of total risk.

D. They earn identical rewards per unit of systematic risk.

E. They have identical Sharpe ratios also.

Which one of the following statements correctly relates to GNMA securities?

A. The primary risk associated with GNMAs is default risk.

B. The minimal denomination of a GNMA when issued is $10,000.

C. GNMA mortgages are guaranteed solely by the FHA.

D. GNMAs were originally established as an agency within the Department of Veteran’s

Affairs.

E. If you buy a GNMA you are accepting the risk of prepayment.

GH Enterprises has annual sales of $5.2 million, depreciation of $350,000, operating

expenses of $390,000, and cost of goods sold of $3.1 million. What is the gross profit?

A. $460,000

B. $850,000

C. $2,100,000

D. $2,650,000

E. $3,710,000

Which one of the following statements concerning the relationship between time to

option maturity and call and put prices is correct?

A. Put and call prices increase at the same rate as the time to option maturity increases.

B. Put prices and time to maturity are inversely related.

C. Call prices tend to increase faster than put prices as the time to option maturity

increases.

D. Put prices increase while call prices remain constant as the time to option maturity

increases.

E. Call prices are inversely related to time to maturity.

You want to purchase a security that will pay you $1,000 seven years from now. If you

want to earn an annual nominal rate of 6.5 percent, how much should you pay for this

investment today?

A. $627.41

B. $630.17

C. $641.41

D. $643.51

E. $662.01

Russ paid a total of $75 to purchase 5 call options with a strike price of $17.50. What is

the break-even stock price?

A. $0.15

B. $0.30

C. $17.35

D. $17.65

E. $32.50

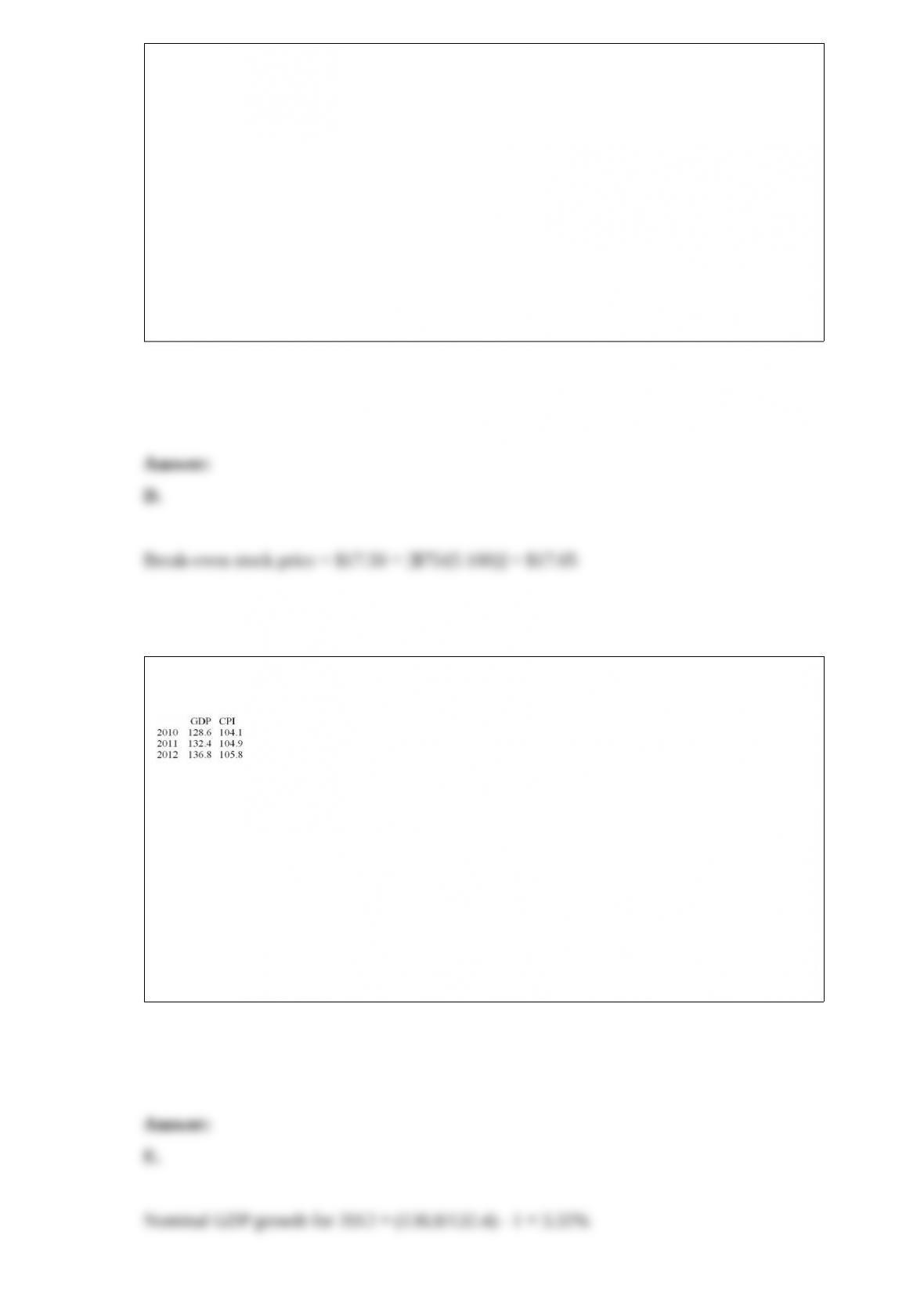

Consider the following information on GDP and CPI for an economy over the last 3

years. Calculate nominal GDP growth for 2012.

A. 2.15%

B. 2.56%

C. 2.95%

D. 3.15%

E. 3.32%

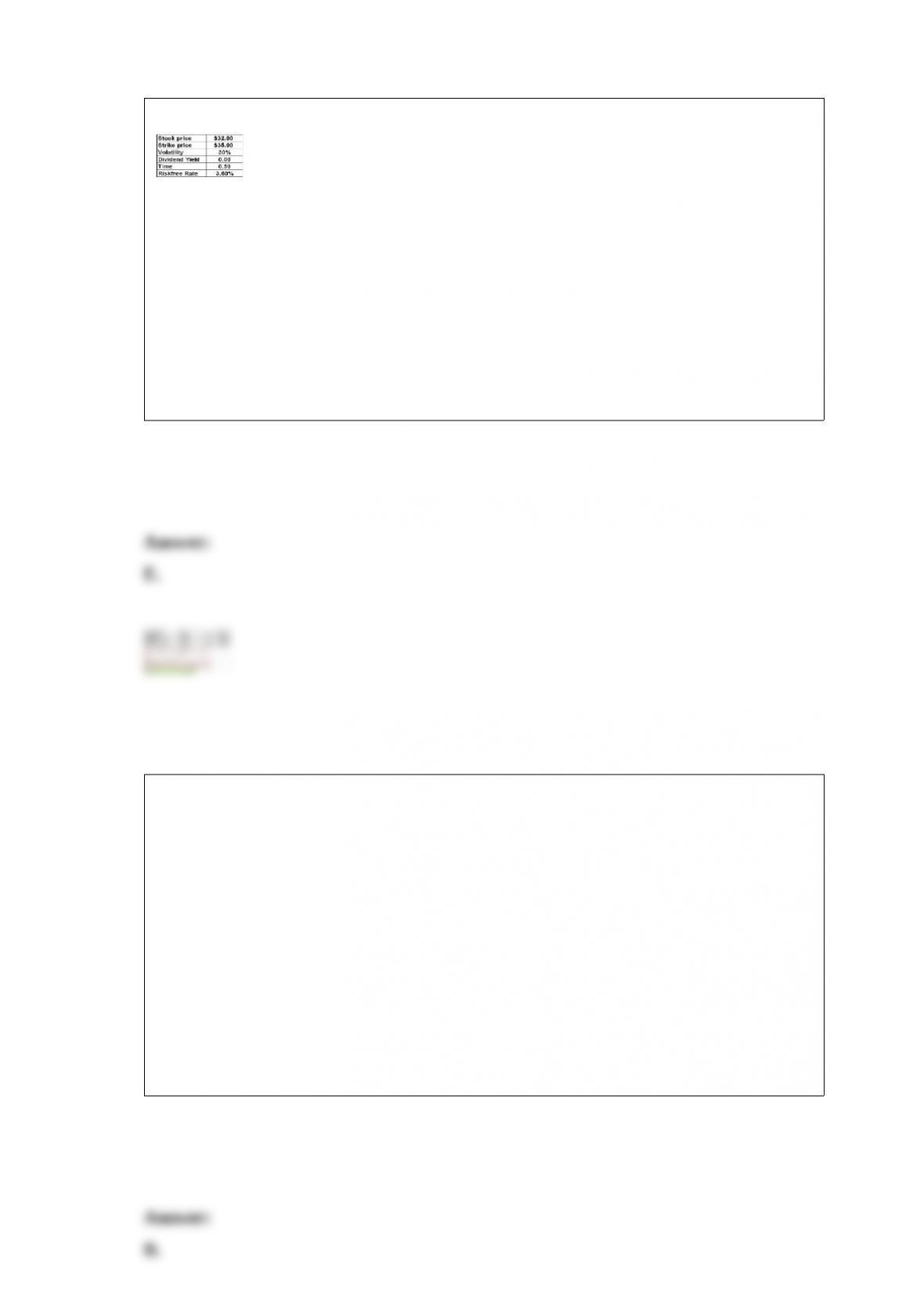

What is the put option premium given the following information?

A. $1.58

B. $2.01

C. $2.59

D. $3.63

E. $4.15

The spot rate on a non-dividend-paying stock is $15.70. The risk-free rate is 3.15

percent and the market rate is 10.75 percent. What is the three-month futures rate if

spot-futures parity exists?

A. $15.48

B. $15.82

C. $16.01

D. $16.13

E. $16.24

Recently, you sold 500 shares of stock for $16.60 a share. The sale was a short sale with

an initial margin requirement of 70 percent. The maintenance margin is 35 percent. The

stock is currently trading at $17.80 a share. What is your current short position in this

stock?

A. $4,916

B. $6,830

C. $8,900

D. $10,362

E. $11,976

A firm has net income of $22,500 and a book value per share of $3.10. The firm has

30,000 shares of stock outstanding and a price-earnings ratio of 15.9. What is the

price-book ratio?

A. 1.7

B. 2.4

C. 2.7

D. 3.8

E. 4.3

A 4-month, $25 call option on Teller stock has an option premium of $0.25. The

4-month, $25 put option has an option premium of $0.80. The risk-free rate is 3 percent.

The options are European-style. What is the price of Teller stock?

A. $24.20

B. $24.53

C. $24.62

D. $25.97

E. $26.08

A mortgage-backed security that has only a subordinate claim to principal payments is

referred to as which type of bond?

A. subsidiary

B. sequential

C. PAC support

D. secondary

E. subordinate

A portfolio has a standard deviation of 14.1 percent, a beta of 1.30 and a Treynor ratio

of .094. The risk-free rate is 3.2 percent. What is the portfolio’s expected rate of return?

A. 14.83 percent

B. 15.25 percent

C. 15.42 percent

D. 16.41 percent

E. 16.56 percent

You have a portfolio which has an average return of 10.3 percent. In any given year,

you have a 2.5 percent probability of earning either a zero or a negative annual return.

What is the approximate standard deviation of your portfolio?

A. 5.26 percent

B. 6.43 percent

C. 6.94 percent

D. 7.60 percent

E. 8.14 percent

The U.S. makes up approximately what percent of the global equity market

capitalization?

A. 20%

B. 25%

C. 30%

D. 35%

E. 40%

An initial investment of $35,000 forty nine years ago is worth $1,533,913 today. What

is the geometric average return on this investment?

A. 7.47 percent

B. 8.02 percent

C. 9.23 percent

D. 10.47 percent

E. 11.08 percent

Which form of market efficiency exists if the market is efficient only in regard to

historical information?

A. mild-form

B. weak-form

C. historical-form

D. semistrong-form

E. strong-form