A mutual fund objective statement provides general information about the types of

securities a mutual fund will hold as assets.

Answer:

The safety and soundness of a holding company that has both a bank subsidiary and a

securities affiliate can be enhanced over time by the product diversification benefits of a

more stable earnings stream caused by having well-diversified financial services.

Answer:

Government securities represent the reserve asset fund for life insurance companies.

Answer:

Although a loan sale strategy for an FI may reduce or eliminate credit risk, the strategy

does not affect the FI’s liquidity risk.

Answer:

As of 2012, which of the following is TRUE concerning payday lending?A. The

typical borrower earns less than $25,000.

B. Payday lending has been effectively banned in 18 states.

C. Interest rate on payday loans were capped at an annual interest rate of 30% by

federal legislation.

D. Less than $30 billion of payday loans were generated by the industry.

E. Payday lenders were banned from forming relationships with nationally chartered

banks.

Answer:

Interest rate futures options are preferred to bond options because they have more

favorable liquidity, credit risk, and market-to-market features.

Answer:

The net asset value of a mutual fund is determined four times each business day.

Answer:

The primary role of capital for an FI is to assure the highest possible return on equity

for its shareholders.

Answer:

When an FI functions as a broker, they are selling a financial asset that they have

created and will continue to hold on their balance sheet.

Answer:

Marking-to-market accounting is a market value accounting method that reflects the

purchase prices of assets and liabilities.

Answer:

More FIs fail as a result of credit risk exposures than either interest rate or FX risk

exposure.

Answer:

The amount of security or collateral on a loan and the interest rate or risk premium on a

loan normally are negatively related.

Answer:

Writing an interest rate call option may hedge an FI when rates rise and bond prices

fall.

Answer:

Most HLT loans are very heterogeneous with respect to the size of the issue, the interest

payment date, interest indexing, and prepayment features.

Answer:

Lenders often are willing to reschedule debt payments to avoid forcing the borrower

into outright bankruptcy.

Answer:

Appropriate technology may allow an FI to achieve lower-cost funding.

Answer:

The proportionate mix of total assets invested in long-term versus short-term mutual

funds has varied over the last twenty years.

Answer:

Loss adjustment expenses refer to the costs surrounding the loss settlement process.

Answer:

When interest rates rise, writing a bond call option may cause profits to offset the loss

on an FI’s bonds.

Answer:

Loan commitment activities increase the insolvency exposure of FIs that engage in such

activities.

Answer:

A principal only (PO) mortgage-backed strip is attractive to investors who wish to

speculate about decreasing interest rates.

Answer:

If an FI is a counterparty to a swap arrangement, it must record the notational value of

the swap as the market value.

Answer:

Foreign exchange rate risk occurs because foreign exchange rates are volatile and can

impact banks with exposed foreign assets and/or liabilities.

Answer:

A significant disadvantage for credit unions in competing with commercial banks is the

severe restriction in the variety of products and services that they can offer.

Answer:

Historically, FNMA has had a secured line of credit with the U.S. Treasury.

Answer:

A term life policy allows the policyholder to vary the maturity of the policy.

Answer:

The parent institution provides a large portion of the debt that a captive finance

company will use to generate personal loans.

Answer:

Hedging foreign exchange risk in the futures market may involve uncertainty about all

of the transactions necessary to achieve the hedge to fulfillment.

Answer:

Commercial paper typically is secured by specific assets of the borrower.

Answer:

A credit forward agreement specifies a credit spread on a benchmark U.S. Treasury

bond.

Answer:

The sensitivity of the price of a futures contract depends on the duration of the

deliverable asset underlying the contract.

Answer:

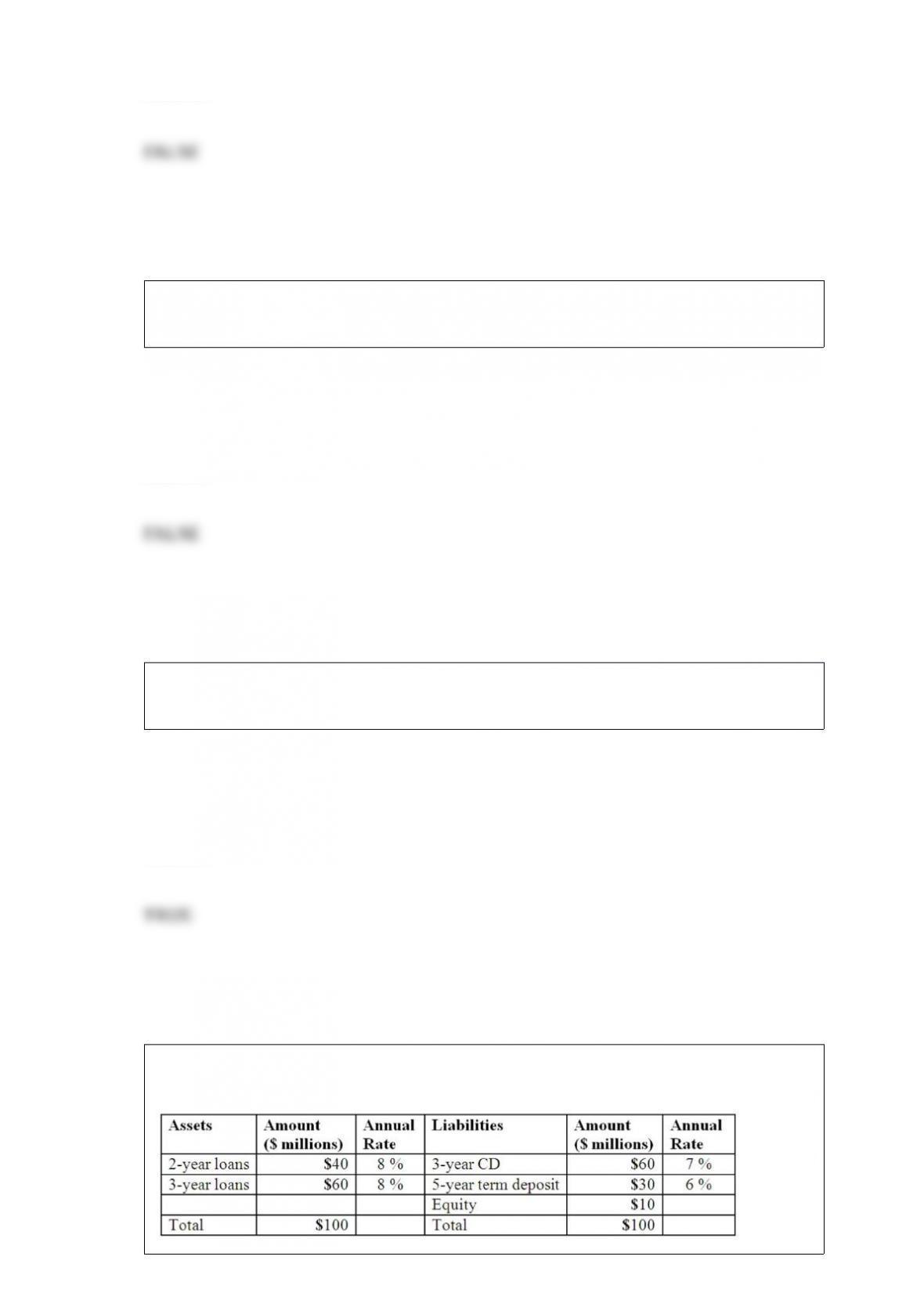

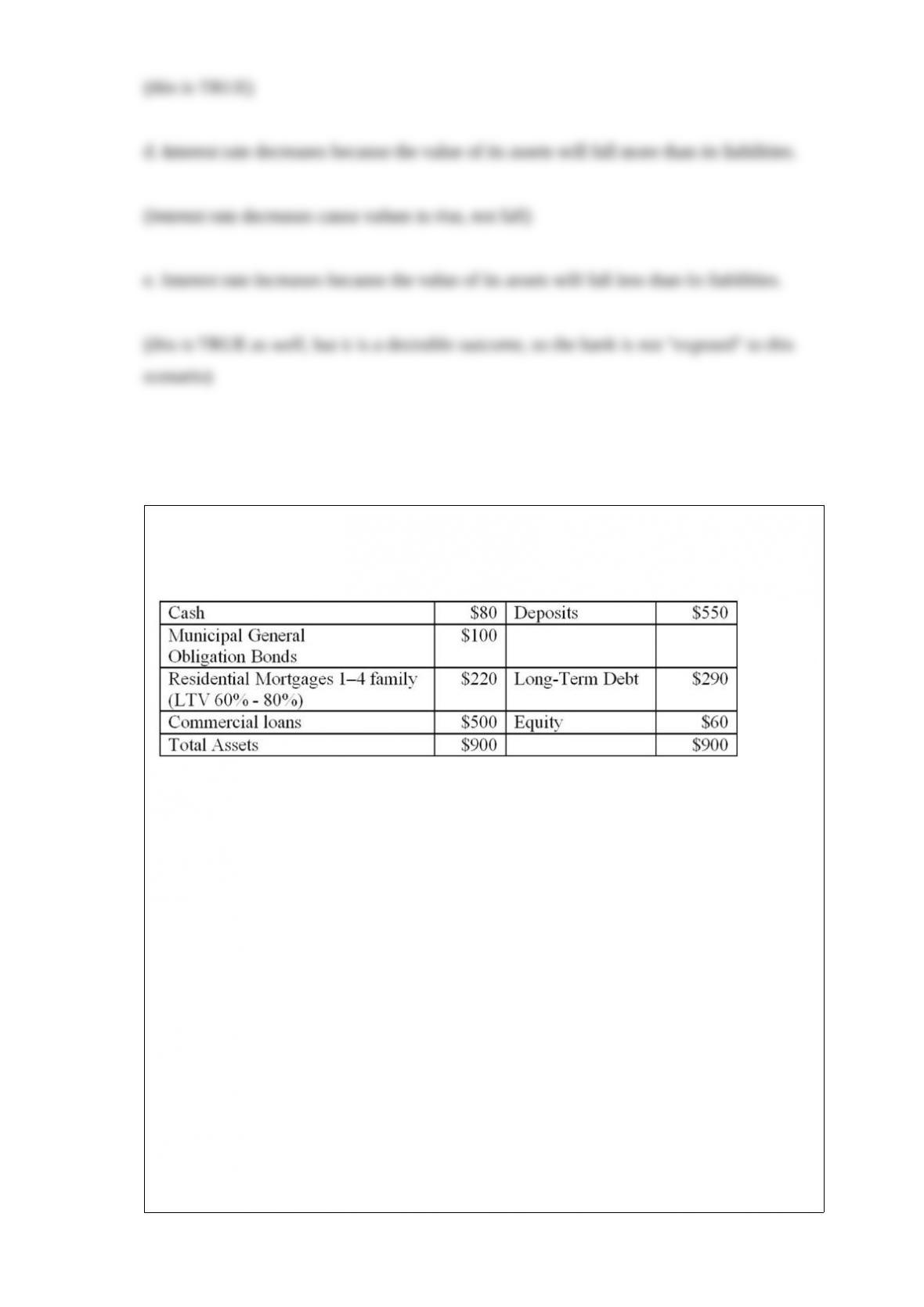

Duration Bank has the following assets and liabilities as of year-end. All assets and

liabilities are currently priced at par and pay interest annually.

What is

the weighted average maturity of the liabilities of the FI? A. 3.67 years.

B. 3.30 years.

C. 3.00 years.

D. 5.00 years.

E. 4.33 years.

Answer:

The National Credit Union Administration (NCUA) is an independent federal agency

that insures credit union deposits.

Answer:

The buyer of a bond put option A. receives a premium in return for standing ready to

sell the bond at the exercise price.

B. receives a premium in return for standing ready to buy bonds at the exercise price.

C. pays a premium and has the right to sell the underlying bond at the agreed exercise

price.

D. pays a premium and has the right to buy the underlying bond at the agreed exercise

price

E. pays a premium and has the obligation to buy the underlying bond at the agreed

exercise price

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation streamlined bank holding company supervision, with the Federal

Reserve as the umbrella holding company supervisor.

Answer:

When will the estimated hedge ratio be greater than one? A. When spot rate changes

are greater than futures rate changes.

B. When spot rate changes are less sensitive than futures price changes over time.

C. When spot rate changes are equally sensitive as futures price changes over time.

D. When basis risk is absent.

E. When the spot and future exchange rates are expected to move perfectly together.

Answer:

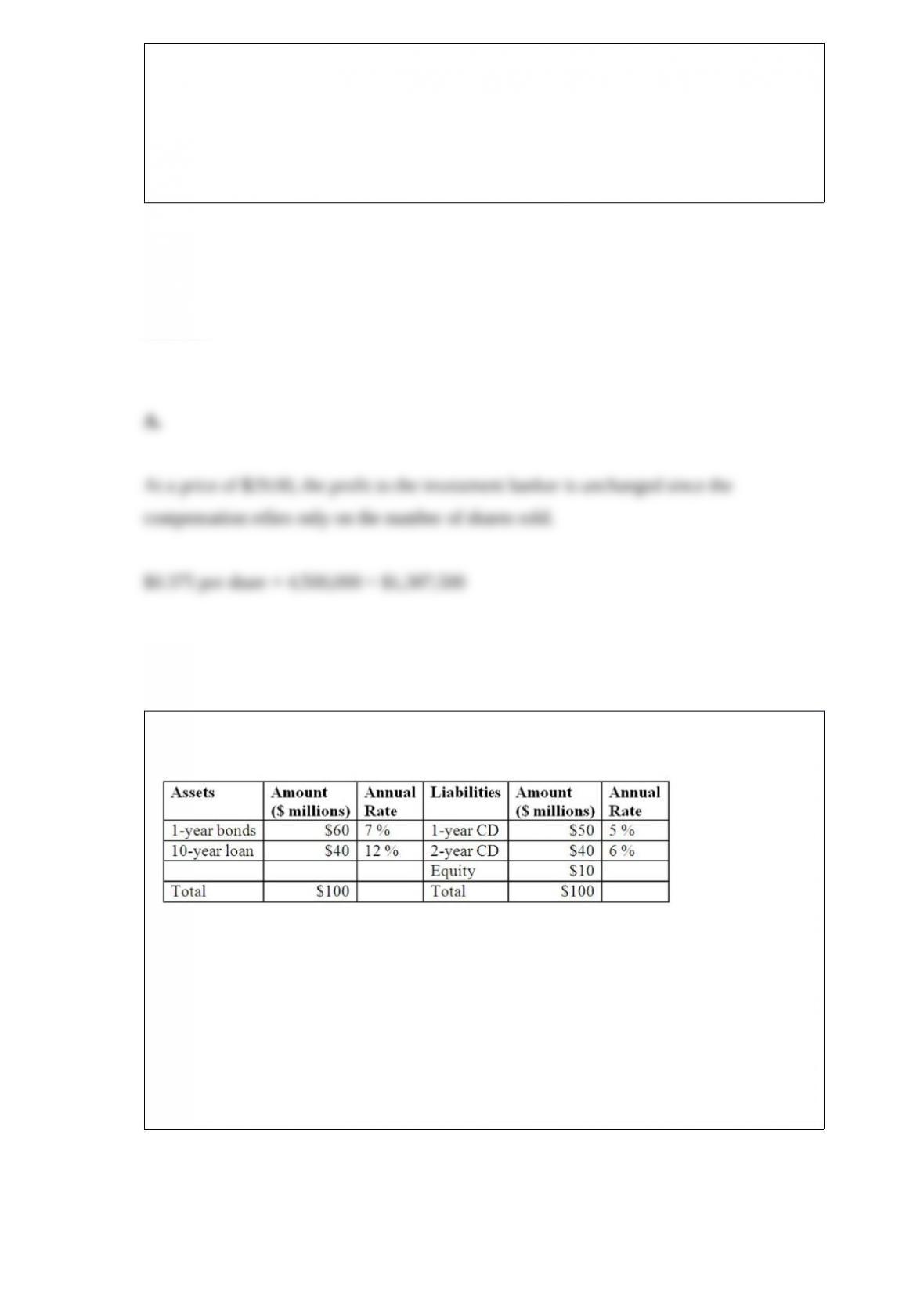

An investment banker agrees to underwrite an issue of 5 million shares of stock for

NetChoice, Inc. on a best-efforts basis. The investment banker is able to sell 4.5 million

shares for $31.00 per share and it charges NetChoice, Inc. $0.375 per share sold.

What is the profit to the investment banker it sells 4.5 million shares for $29 per share?

A. Profit of $1,687,500.

B. Loss of $2,487,500.

C. Profit of $1,875,000.

D. Loss of $3,125,000.

E. Profit of $3,125,500.

Answer:

Hadbucks National Bank current balance sheet appears below. All assets and liabilities

are currently priced at par and pay interest annually.

What is this FI’s

maturity gap? A. 4.00 years.

B. 4.28 years.

C. 3.16 years.

D. 4.06 years.

E. 5.10 years.

Answer:

Prior to the International Banking Act of 1978, foreign banks operating with state

licensesA. were not subject to the Federal Reserve’s reserve requirements.

B. were not subject to interstate branching restrictions.

C. were not subject to restrictions on corporate securities underwriting.

D. All of the above.

E. Answers A and B only.

Answer:

The following market value balance sheet of a failed bank ($ millions)

If the insured depositor transfer resolution method is utilized, what is the

cost to uninsured depositors of bank failure resolution?A. $0.

B. -$200 million.

C. $67 million.

D. $133 million.

E. $200 million.

Answer:

The capital requirements of internally generated market risk exposure estimates can be

met A. only with two types of capital.

B. only with Tier 1, Tier 2, or Tier 3 capital.

C. with retained earnings and common stock only.

D. only with retained earnings, common stock, and long-term subordinated debt.

E. only with short- or long-term subordinated debt.

Answer:

As part of measuring unobservable default risk between borrowers, the Moody’s

Analytics model decomposes asset returns into A. credit risk and market risk.

B. systematic risk and unsystematic risk.

C. market risk and sovereign risk.

D. regional risk and maturity risk.

E. systematic risk and default risk.

Answer:

In April 2012, an FI bought a one-month sterling T-bill paying £100 million in May

2012. The FI’s liabilities are in dollars, and current exchange rate is $1.6401/£1. The

bank can buy one-month options on sterling at an exercise price of $1.60/£1. Each

contract has a size of £31,250, and the contracts currently have a premium of $0.014

per £. Alternatively, options on foreign currency futures contracts, which have a size of

£62,500, are available for $0.0106 per £.

What is the foreign exchange risk that the FI is facing, and what type of currency option

should be purchased to hedge this risk? A. The FI should use put options to hedge the

depreciation of the dollar.

B. The FI should use call options to hedge the depreciation of the pound sterling.

C. The FI should use put options to hedge the depreciation of the pound sterling.

D. The FI should use call options to hedge the depreciation of the dollar.

E. The FI should use put options to hedge the appreciation of the pound sterling.

Answer:

What are the two major liquidity risk insulation devices available? A. Deposit

insurance and discount window.

B. Liquidity planning and maturity ladder.

C. Scenario analysis and liquidity index.

D. Financing gap and the financing requirement.

E. Secondary credit and seasonal credit.

Answer:

An FI issued $1 million of 1-year maturity floating rate commercial paper. The

commercial paper is repriced every three months at the 91-day Treasury bill rate plus 2

percent. What is the FI’s interest rate risk exposure and how can it use financial futures

and options to hedge that risk exposure? A. The FI can hedge its exposure to interest

rate increases by selling financial futures.

B. The FI can hedge its exposure to interest rate decreases by selling financial futures.

C. The FI can hedge its exposure to interest rate increases by buying financial futures.

D. The FI can hedge its exposure to interest rate increases by buying call options.

E. The FI cannot hedge its exposure to interest rate increases or decreases using

financial futures

Answer:

Which of the following best describes economies of scope? A. They occur when the

average cost of production decreases as the level of output increases.

B. They are effects on costs related to managerial ability and other hard-to-quantify

factors.

C. They occur when cost savings are realized from using many of the same inputs to

produce multiple products.

D. They occur when the average cost of production increases as the level of output

increases.

E. They occur when cost increases are realized from using many of the same inputs to

produce multiple products.

Answer:

Which of the following is not a Least-Cost Resolution (LCR) requirement under

FDICIA? A. Consider and evaluate all possible resolution alternatives by computing

and comparing their costs on a present value basis, using realistic discount rates.

B. Place a bank or thrift into receivership as soon as its capital falls below some

positive book value level.

C. Document the evaluation and the assumption on which it is based.

D. Retain documentation for at least five years.

E. Select the least costly alternative based on the evaluation.

Answer:

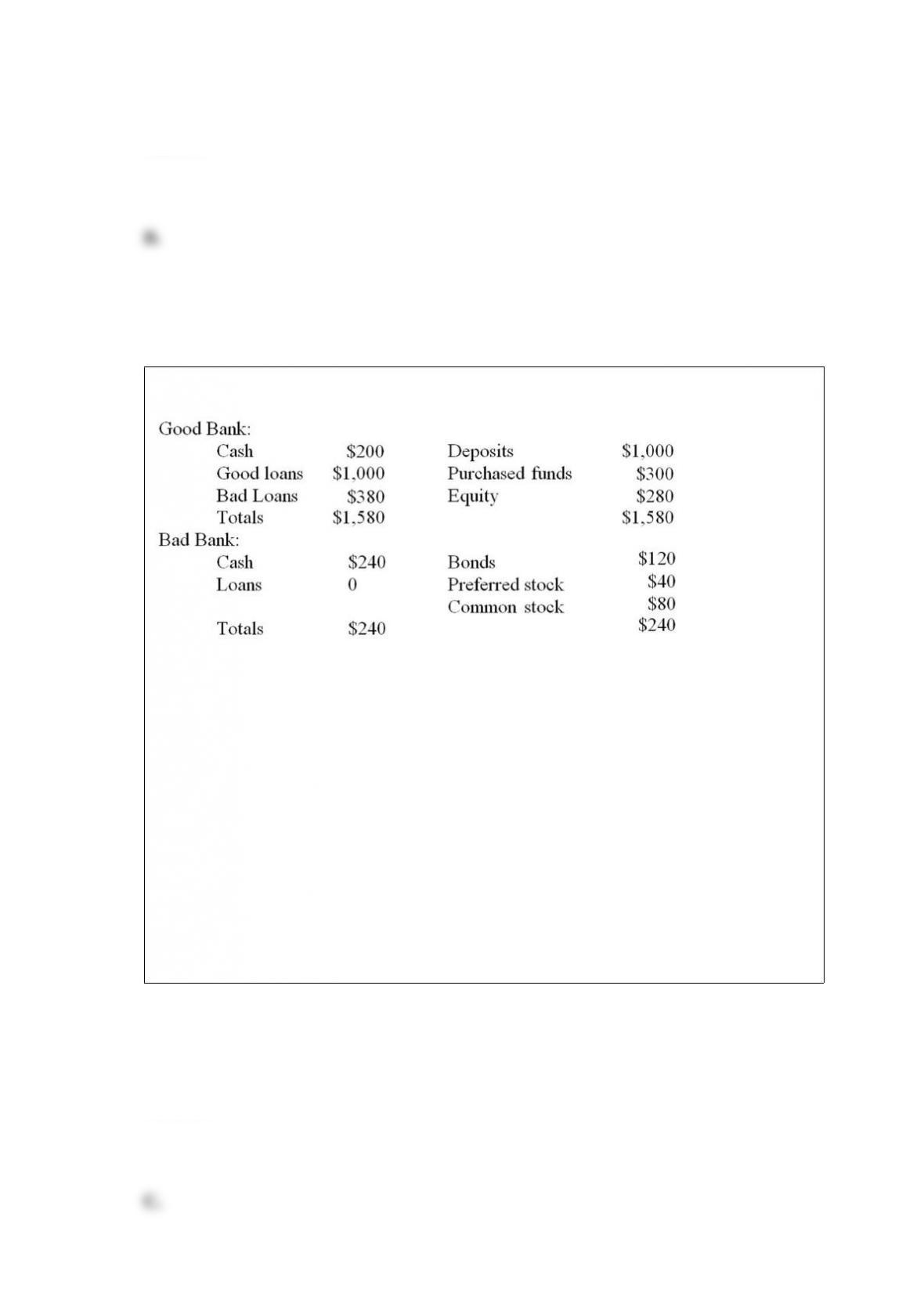

Bad Bank buys the bad loans for $232. The proceeds of the loan sale are used by Good

Bank to pay off purchased funds.

What will be the amount of equity on the balance sheet of Good Bank after the sale of

the loans? A. $1,200.

B. $232.

C. $132.

D. $68.

E. $0.

Answer:

What is the maximum yield change expected if a 95 percent confidence (one-tailed)

limit is used? A. 3.30%.

B. 20.0%.

C. 33.0%.

D. 39.2%.

E. 46.6%.

Answer:

The definition of a highly leveraged transaction (HLT) loan as adopted by U.S. bank

regulators in 1989 includesA. doubling the borrower’s liabilities which results in a

leverage ratio higher than 50 percent.

B. involving a buyout, acquisition, or recapitalization.

C. results in a leverage ratio higher than 75 percent.

D. All of the above.

E. Only two of the above.

Answer:

Pure arbitrage trading involvesA. buying blocks of securities in anticipation of some

information release.

B. purchase of stock in a company being acquired and the sale of stock in the acquiring

company.

C. exploitation of a difference between a company’s current value and its estimated

liquidation value.

D. buying an asset in one market at one price and selling it immediately in another

market at a higher price.

E. simultaneous purchase and sale of similar shares in a single market.

Answer:

An FI that finances long-term fixed rate mortgages with short-term deposits is exposed

toA. increases in net interest income and decreases in the market value of equity when

interest rates fall.

B. decreases in net interest income and decreases in the market value of equity when

interest rates fall.

C. decreases in net interest income and decreases in the market value of equity when

interest rates rise.

D. increases in net interest income and decreases in the market value of equity when

interest rates rise.

E. increases in net interest income and increases in the market value of equity when

interest rates rise.

Answer:

Which of the following is NOT a contractual mechanism used by FIs to control credit

risks? A. Diversifying across different types of risky borrowers.

B. Requiring higher interest rate spreads for higher risk borrowers.

C. Requiring more collateral for the bank over the assets of more risky borrowers.

D. Making lending decisions only in centralized locations.

E. Placing more restrictive covenants on the actions of more risky borrowers.

Answer:

What is the IRR for this investment?A. 11.18 percent.

B. 12.98 percent.

C. 15.24 percent.

D. 12.00 percent.

E. 18.00 percent.

Answer:

Which act appointed the National Association of Securities Dealers (NASD) to

supervise mutual fund share distributions? A. Securities Act of 1933.

B. Securities Exchange Act of 1934.

C. Investment Advisers Act.

D. Investment Company Act.

E. Market Reform Act of 1990.

Answer:

In the event of financial distress, open-ended mutual fund investors A. have an

incentive to cash in their shares quickly since they are paid on a first come, first served

basis.

B. have an incentive to avoid a run since that will deplete the fund net asset value.

C. have an incentive to cash in their shares quickly since that will increase the fund’s

net asset value.

D. will switch into low risk bank deposits.

E. have an incentive to avoid a run since the Federal Reserve guarantees mutual fund

holdings.

Answer:

Can an FI immunize itself against interest rate risk exposure even though its maturity

gap is not zero?A. Yes, because with a maturity gap of zero the change in the market

value of assets exactly offsets the change in the market value of liabilities.

B. No, because with a maturity gap of zero the change in the market value of assets

exactly offsets the change in the market value of liabilities.

C. Yes, because the maturity model does not consider the timing of cash flows.

D. No, because the timing of cash flows is relevant to immunization against interest

rate risk exposure.

E. No, because a representative bank will always have a positive maturity gap.

Answer:

Which of the following wholesale services offered by FIs allows businesses to transfer

and transact invoices, purchase orders, and shipping notices automatically? A.

Electronic data exchange.

B. E-commerce facilitation.

C. Electronic billing.

D. Electronic funds transfer.

E. Account reconciliation.

Answer:

These interstate banking laws allowed an out-of-state bank to acquire an in-state target

bank even if the acquirer’s home state did not give banks from the target’s state similar

acquisition powers.A. Nationwide laws.

B. Nationwide reciprocal.

C. Regional reciprocal.

D. All of the above.

E. Answers A and B only.

Answer:

Is the bank exposed to interest rate increases or decreases and why?A. Interest rate

increases because the value of its assets will rise more than its liabilities.

B. Interest rate increases because the value of its assets will fall more than its

liabilities.

C. Interest rate decreases because the value of its assets will rise less than its liabilities.

D. Interest rate decreases because the value of its assets will fall more than its

liabilities.

E. Interest rate increases because the value of its assets will fall less than its liabilities.

Answer:

Fifth Bank has the following balance sheet with values stated in millions of dollars. All

assets are associated with corporate customers (not governments or sovereigns). Refer

to Table 20-8 for associated risk weights.

In

addition, Fifth Bank has off-balance sheet items as follows: (Refer to Tables 20-10 and

20-11)

$50 million in commercial letters of credit (LCs),

$300 million in 3-year interest rate swaps that are in-the-money by $2 million

$50 million in 4-year forward FX contracts that are out-of-the money by $2 million

What is the amount of risk adjusted on-balance-sheet assets of the bank as defined

under the Basel II standards? A. $130.0 million.

B. $685.0 million.

C. $720.0 million.

D. $630.0 million.

E. $900.0 million.

Answer:

Underwriting risk faced by property-casualty insurance companies may result from

unexpected A. increases in loss rates.

B. decreases in loss adjustment expenses.

C. increases in investment yields.

D. cancellations of policies by customers.

E. increases in policy premiums.

Answer:

The largest asset class on FDIC-insured savings institutions’ balance sheet as of

year-end 2012 was A. mortgage loans.

B. cash.

C. investment securities.

D. deposits.

E. non-mortgage Loans.

Answer:

What is the end-of-year profit or loss on the bank’s cash position if in one year both

Canadian bond rates increase to 7.5 percent and the exchange rate falls to US $0.765

per Canadian dollar (Assume no change in U.S. interest rates.) (Choose the closest

answer)A. Loss of US $12,000.

B. Loss of US $75,000.

C. Profit of C $9,000.

D. Profit of US $50,000.

E. Loss of C $119,000.

Answer: