Violation of the interest rate parity theorem would allow arbitrage profits.

Answer:

As a percent of assets, finance companies currently rely more heavily on commercial

paper as a source of financing than in 1977.

Answer:

A naked option is an option written that has no identifiable underlying asset or liability

position.

Answer:

According to economic theory involving economies of scale, larger and more

cost-efficient FIs should prevail over smaller, less cost-efficient FIs.

Answer:

Market value accounting is likely to increase the variability of earnings of an FI.

Answer:

An adjustment for basis risk with a value of “br” less than one means that the percent

change in the spot rates is greater than the change in rate in the deliverable bond in the

futures market.

Answer:

Sustained credit quality problems can drain an FI’s capital and net worth.

Answer:

Which of the following is TRUE concerning an assumable mortgage?A. The aggregate

percent of the mortgage pool that has been prepaid prior to the month under

consideration.

B. The mortgage contract is transferred from the seller to the buyer of a house.

C. The required interest spread of a pass-through security over a treasury when

prepayment risk is taken into account.

D. A mortgage-backed bond issued in multiple classes or tranches.

E. Bonds collateralized by a pool of assets.

Answer:

Which of the following observations concerning repurchase agreements is NOT TRUE?

A. They can be viewed as collateralized federal funds transactions.

B. The RP market is a highly liquid and flexible source of funds for DIs needing to

increase their liabilities and to offset deposit withdrawals.

C. Unlike fed funds, these transactions cannot be rolled over each day.

D. It is difficult to transact an RP borrowing late in the day.

E. Negotiations over the collateral package can delay RP transactions.

Answer:

Large size is an important characteristic in international banking because it gives a bank

a greater ability to diversify across borders.

Answer:

Default by a large corporation is seldom a problem for FIs since these corporations have

many different sources of borrowed funds.

Answer:

An originate-to-sell model when dealing with below investment grade companies is

considered an attractive alternative for FIs, which have specialized credit monitoring

skills, as compared with keeping the loans in their portfolio.

Answer:

In the past, data availability limited the use of sophisticated portfolio models to set

concentration limits.

Answer:

The largest 20 firms in the nondepository finance company industry account for more

than 65 percent of industry assets.

Answer:

Factoring is the process where accounts are purchased by a nonfinancial company at a

discount from their face value in exchange for the responsibility of collection.

Answer:

Residential mortgages are the smallest component of bank real estate loan portfolios.

Answer:

Individuals have an advantage over FIs in that individuals more easily can diversify

away some of the credit risk of their asset portfolios.

Answer:

The payoff function of a loan to a debt holder is similar to writing a call option on the

value of the borrower’s assets with the face value of the debt as the exercise price.

Answer:

Cash management accounts were an early attempt by commercial banks to provide

investment banking services to individuals.

Answer:

Pricing insurance premiums in an actuarially fair manner involves assessing the

risk-taking profile of the financial institution.

Answer:

In the U.S., excess reserves held at the central bank pay interest to the DI.

Answer:

Off-balance-sheet items can generate cash flows that immediately impact the bank’s

financial performance.

Answer:

Recent Federal Reserve policy for measuring credit concentration risk favors technical

models over subjective analysis.

Answer:

The underlying cause of foreign exchange volatility reflects fluctuations in the demand

and supply of a country’s currency.

Answer:

Under the Financial Services Modernization Act of 1999, commercial banks can own

and actively manage nonfinancial corporations.

Answer:

Employers that sponsor non-contributory group life insurance require the employee to

pay the insurance premiums.

Answer:

Even with liquidity planning, net deposit withdrawals and/or the exercise of loan

commitments can pose significant liquidity problems for banks.

Answer:

Sales finance companies do not directly compete with depository institutions for

consumer loans.

Answer:

The growth of the commercial paper market as well as the increased ability of banks to

underwrite commercial paper has reduced the importance of short-term segment of the

loan sales market.

Answer:

The dual banking system in the U.S. refers to the operation and establishment of large

regional as well as small community banks.

Answer:

Under market value accounting methods, FIs A. must write down the value of their

assets to fully reflect market values.

B. have a great deal of discretion in timing the write downs of problem loans.

C. must conform to regulatory write-down schedules.

D. have an incentive to fully reflect problem assets as they become known.

E. are required to invest in expensive computerized bookkeeping systems.

Answer:

Which of the following refers to a period when a borrower is unable to meet a payment

obligation to lenders and other creditors? A. Window.

B. Financial distress.

C. Foreclosure.

D. Recession.

E. Assignment.

Answer:

The covariance of the change in spot exchange rates and the change in futures exchange

rates is 0.6606, and the variance of the change in futures exchange rates is 0.6060. The

variance of the change in spot exchange rates is 0.9090. What is the degree of hedging

effectiveness? A. 0.61.

B. 0.90.

C. 0.87.

D. 0.82.

E. 0.79.

Answer:

Economically speaking, OBS activities are contractual claims that A. may or may not

occur.

B. if the contingency does occur, the asset or liability is transferred onto the FI’s

balance sheet.

C. impact the economic value of the equity.

D. if the contingency never occurs, there is virtually no economic meaning to the OBS

activity.

E. all of the above.

Answer:

For a DI, what does a high ratio of loans to deposits indicate? A. DI relies heavily on

the short-term money market to fund loans.

B. High degree of loan commitments.

C. DI has large amounts of asset-side liquidity.

D. Liquidity concerns are at a bare minimum for the FI.

E. DI relies heavily on core deposits to fund loans.

Answer:

Match the following pieces of legislation with the function achieved by each regulation

as stated in question

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Advisers Act

D. Investment Company Act

E. Insider Trading and Securities Fraud Enforcement Act of 1988

F. Market Reform Act of 1990

G. National Securities Markets Improvement Act of 1996

Regulates the activities of mutual fund advisors.

Answer:

Match the following pieces of legislation with the function achieved by each regulation

as stated in question

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Advisers Act

D. Investment Company Act

E. Insider Trading and Securities Fraud Enforcement Act of 1988

F. Market Reform Act of 1990

G. National Securities Markets Improvement Act of 1996

Provides for the supervision of mutual fund share distributions.

Answer:

Spruce Bank is planning to automate some of its back office functions and reduce

operating costs. The installation of new computers and software will require an initial

investment of $1,000,000. The savings generated because of reduced personnel cost is

$200,000 per year. The bank uses an 8 percent rate of discount to evaluate cost saving

projects which are expected to last 10 years.

Should the bank undertake the project given the above information? A. Yes, because

the NPV of the project is $500,000.

B. Yes, because the NPV of the project is $342,016.

C. No, because the NPV of the project is -$500,000.

D. No, because the NPV of the project is -$201,458.

E. No, because the IRR of the project is lower than 12 percent.

Answer:

Which of the following is NOT a primary source of liquidity? A. Excess cash reserves

over and above regulatory reserve requirements.

B. Borrowings in the money market.

C. Borrowings in the purchased funds market.

D. Capital notes and other long-term financing alternatives.

E. Cash-type assets that can be sold with little price risk and low transaction costs.

Answer:

Discount window loans from the Federal Reserve are used as A. Non-permanent

short-term funds.

B. Funds to meet seasonal liquidity needs.

C. Funds to meet unexpected deposit drain.

D. Funds to meet reserve requirement.

E. All of the above.

Answer:

As of the end of 2012, the total worldwide assets of the shadow banking system was

approximately A. $12 trillion

B. $37 trillion

C. $52 trillion

D. $67 trillion

E. $91 trillion

Answer:

The U.S. banking industry built up record levels of capital in the early 2000s because

A. the economy went through a downturn.

B. problem loans increased.

C. the regulators required higher amounts of equity sales.

D. of record high levels of profitability.

E. of mergers between large banks.

Answer:

The calculation of the risk-adjusted asset values of OBS market contractsA. nearly

always equals zero because the exchange over which the contract initially traded

assumes all of the risk.

B. requires multiplication of the credit equivalent amounts by the appropriate risk

weights.

C. requires the calculation of a conversion factor to create credit equivalent amounts.

D. All of the above.

E. Answers B and C only.

Answer:

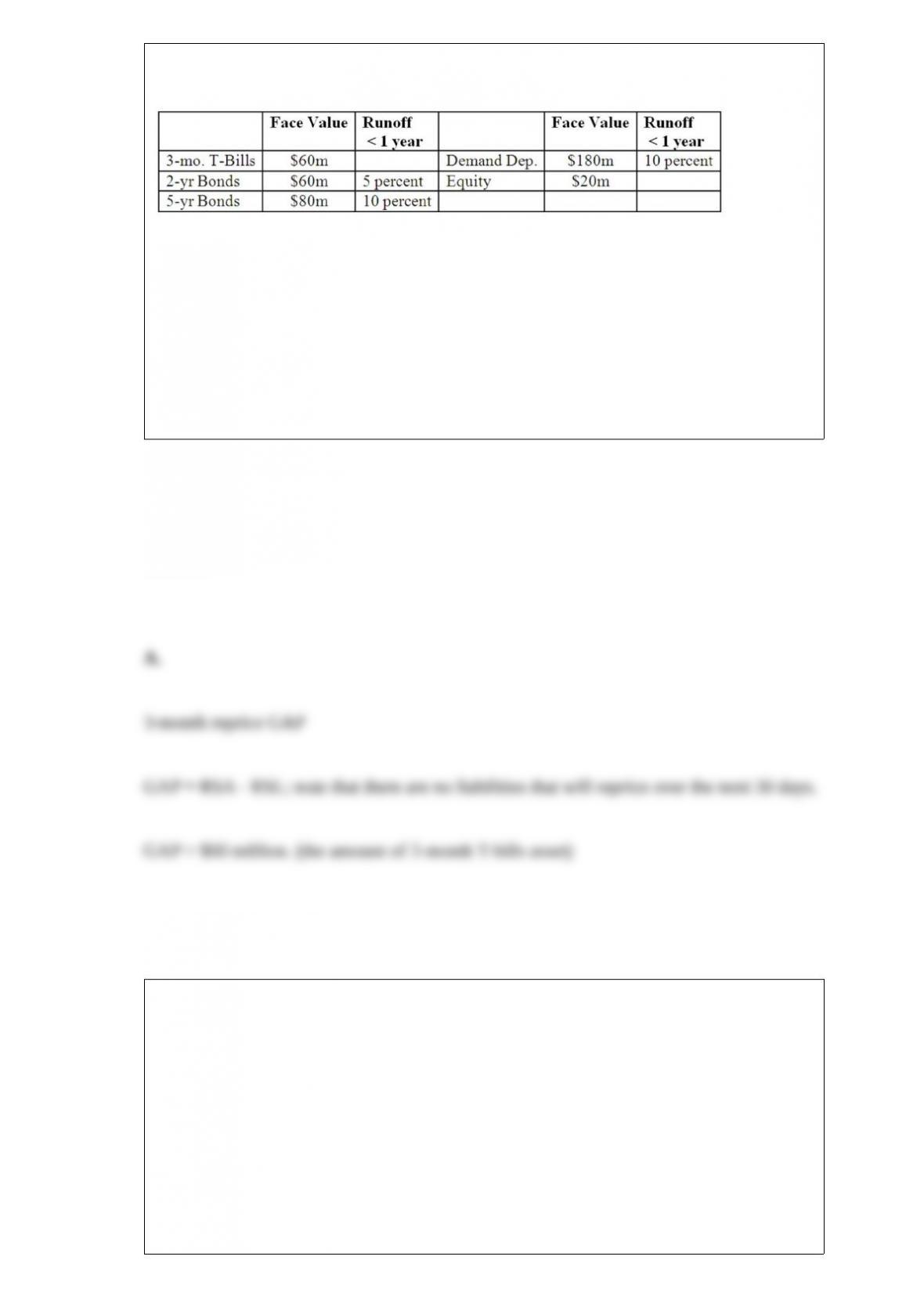

The following is the balance sheet of Boston Bank. The average maturity of demand

deposits is estimated at 2 years.

What is

the repricing gap if a 0 to 3 month maturity gap is used? Ignore runoffs. A. $60 million.

B. $40 million.

C. -$80 million.

D. -$120 million.

E. -$180 million.

Answer:

One hundred identical mortgages are pooled together into a pass-through security. Each

mortgage has a $150,000 principal, a fixed annual interest rate of 8 percent (paid

monthly), and is fully amortized over a term of 30 years.

What is the monthly payment on the mortgage pass-through? A. $100,000.

B. $110,065.

C. $12,000.

D. $12,000,000.

E. $80,000.

Answer:

At the end of the year 2, the exchange rate is €1/$. What are the losses and gains to each

bank as a result of this swap. Ignore principal payments and compare it to the scenario

where it did not engage in the swap.A. With the agreement, Bank Dresdner pays €2.5

million less while Bank USA pays $1.25 more.

B. With the agreement, Bank Dresdner pays €2.5 million more while Bank USA pays

$2.5 million less.

C. With the agreement, Bank USA pays $3.75 million less while Bank Dresdner pays

€7.5 million more.

D. With the agreement, Bank USA pays $3.75 million more while Bank Dresdner pays

€7.5 million less.

E. Each bank pays the same because the exchange rate affects both parties equally.

Answer:

A bank with a strong positive leverage adjusted duration gap can hedge their exposure

to interest rate increases by entering into A. a currency swap agreement to receive the

fixed rate payment.

B. an interest rate swap agreement to make the fixed-rate payment side of the swap.

C. a credit swap agreement to receive the floating rate payment.

D. a commodity swap agreement to make the fixed-rate payment side of the swap.

E. an equity swap agreement to make the floating-rate payment side of the swap.

Answer:

The repricing model ignores information regarding the distribution of assets and

liabilities within maturity buckets. This limitation of the model refers to A. market

value effect.

B. overaggregation.

C. runoffs and pre-payments.

D. OBS activities.

E. the spread effect.

Answer:

The potential exposure component of the credit equivalent amount of OBS derivative

items reflects A. the probability of an adverse price movement in contracts.

B. the cost of replacing a contract if a counterparty defaults today.

C. the probability today of a counterparty contract default in the future.

D. the maximum price loss for any given position.

E. Answers A and D only.

Answer:

Servicing a pass-through security refers to A. an FI processing of all payments.

B. an FI provision of clearing services to set up the pass-through.

C. broker/dealer services provided by the FI to the ultimate holders of the

pass-through.

D. guarantee by the FI of all principal and interest payments.

E. an FI provision of liquidity services to the ultimate holders of the pass-through.

Answer:

From the lender’s point of view, debt can be evaluated as A. writing a call option on the

borrower’s assets with the exercise price equal to the face value of the debt.

B. buying a call option on the borrower’s liabilities with the exercise price equal to the

market value of the debt.

C. buying a put option on the borrower’s assets with the exercise price equal to the face

value of the debt.

D. writing a put option on the borrower’s assets with the exercise price equal to the face

value of the debt.

E. writing a put option on the borrower’s liabilities with the exercise price equal to the

market value of the debt.

Answer:

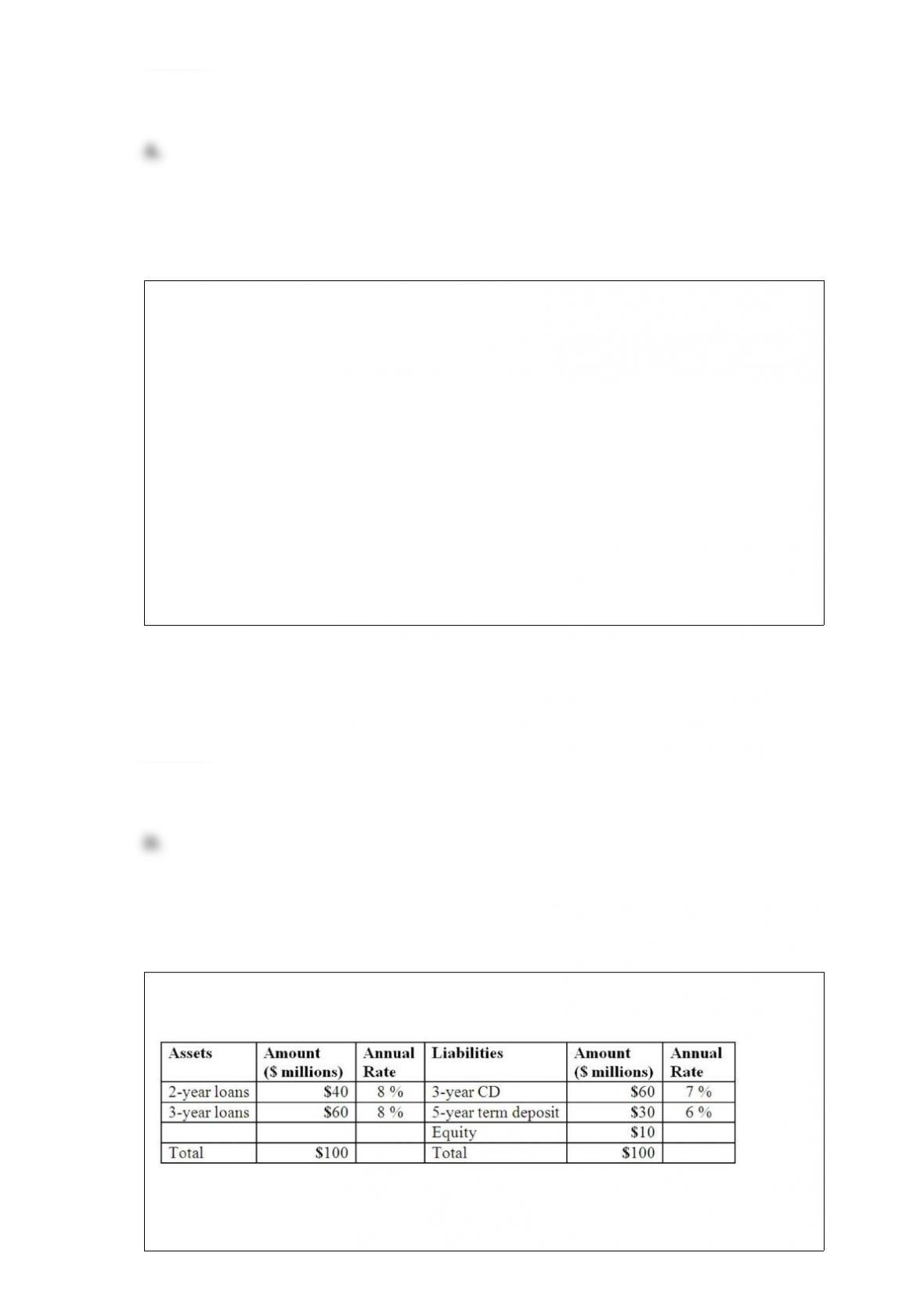

Duration Bank has the following assets and liabilities as of year-end. All assets and

liabilities are currently priced at par and pay interest annually.

What is

the weighted average maturity of the assets of the FI? A. 2.0 years.

B. 2.3 years.

C. 2.5 years.

D. 2.6 years.

E. 3.0 years.

Answer:

In the Moody’s Analytics portfolio model, the expected return on a loan is the A.

annual all-in-spread minus the expected loss on the loan.

B. annual all-in-spread minus expected probability of the borrower defaulting over the

next year.

C. annual all-in-spread minus the loss given default.

D. the interest and fees paid by the borrower minus the interest paid by the FI to fund

the loan.

E. the interest and fees paid by the borrower minus the expected loss on the loan.

Answer:

If a bank’s concentration limit (as a percentage of capital) is 25.0 percent, and it does

not permit a loss of any loan to impact more than 10 percent of its capital, what is the

expected recovery on loans that are defaulted? A. 20 percent.

B. 30 percent.

C. 40 percent.

D. 50 percent.

E. 60 percent.

Answer:

Bank of the Atlantic has liabilities of $4 million with an average maturity of two years

paying interest rates of 4.0 percent annually. It has assets of $5 million with an average

maturity of 5 years earning interest rates of 6.0 percent annually.

What is the bank’s net interest income for the current year? A. $300,000.

B. $140,000.

C. $160,000.

D. $280,000.

E. $80,000.

Answer:

The banking industry in the U.S. has faced increased competition A. on the liability

side of the balance sheet from the commercial paper market.

B. on the asset side of the balance sheet from money market mutual funds.

C. on the liability side of the balance sheet from money market mutual funds.

D. on the asset side of the balance sheet from the commercial paper market.

E. Answers C and D only.

Answer:

The debate and research regarding the advantages of load funds versus no-load funds

has revealed that A. the proportion of total assets invested in load funds has decreased

over the last 20 years and became less than the assets in no-load funds in 2002.

B. the cost of the load may not be worth the attention and advice given to investors.

C. most mutual fund companies offer the majority of their funds as no-load funds.

D. a load fee should be annualized over the holding period of the fund shares.

E. All of the above.

Answer:

An organization form that establishes bank subsidiaries rather than branches to expand

isA. an unit bank.

B. a multibank holding company.

C. a one-bank holding company.

D. a representative office.

E. a nonbank bank.

Answer:

Migration analysis is a tool to measure credit concentration risk and refers to A. the

identification of problem loans in sectors by observing periodic migration of industries.

B. the identification of credit concentration by observing trends in market borrowing

by different sectors of the industry.

C. the identification of credit concentration by observing the downgrading or

upgrading of credit ratings on securities in different sectors of industry by public rating

agencies.

D. the identification of borrowing patterns such as long or short term debt by different

sectors of industry.

E. the identification of shifts in debt/asset ratios of firms in specific industries.

Answer:

The current price of June $100,000 T-Bonds trading on the Chicago Board of Trade is

109-24. What is the price to be paid if the contract is delivered in June? A. $107,240.

B. $109,240.

C. $109,750.

D. $110,250.

E. $115,760.

Answer:

Identify the legislation that restricted the branching of nationally-chartered banks to the

same guidelines as allowed to state-chartered banks. A. Bank Holding Company Act.

B. McFadden Act.

C. Garn-St. Germain Act.

D. Glass-Steagall Act.

E. Competitive Equality in Banking Act.

Answer:

Large-scale investment projects that lead to excess capacity and integration problems

that create cost overruns and control problems are examples ofA. diseconomies of

scale.

B. economies of scale.

C. economies of scope.

D. diseconomies of scope.

E. constant returns to scale.

Answer:

The portfolio manager for Conyers Bank wishes to sell the entire issue of Treasury

bonds at a current price of 87-05/32nds. What will be the gain or loss on the cash

position since the futures contract was placed? (That is, since the bonds were valued at

$28,387,500.) A. Loss of $3,834,375.

B. Loss of $3,853,125.

C. Gain of $2,240,625.

D. Gain of $3,853,125.

E. Loss of $2,240,625.

Answer:

In financing their asset growth, finance companies A. have relied more on bank loans

over time.

B. rely heavily on short-term commercial paper.

C. use less equity capital than commercial banks.

D. do not issue demand deposits, but can issue time deposits.

E. use very small amounts of long-term debt and bonds.

Answer:

If interest rates increase by 20 basis points, what is the approximate change in the

market price using the duration approximation? A. -$7.985

B. -$7.941

C. -$3.990

D. +$3.990

E. +$7.949

Answer: