Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1) Exhibit 22.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

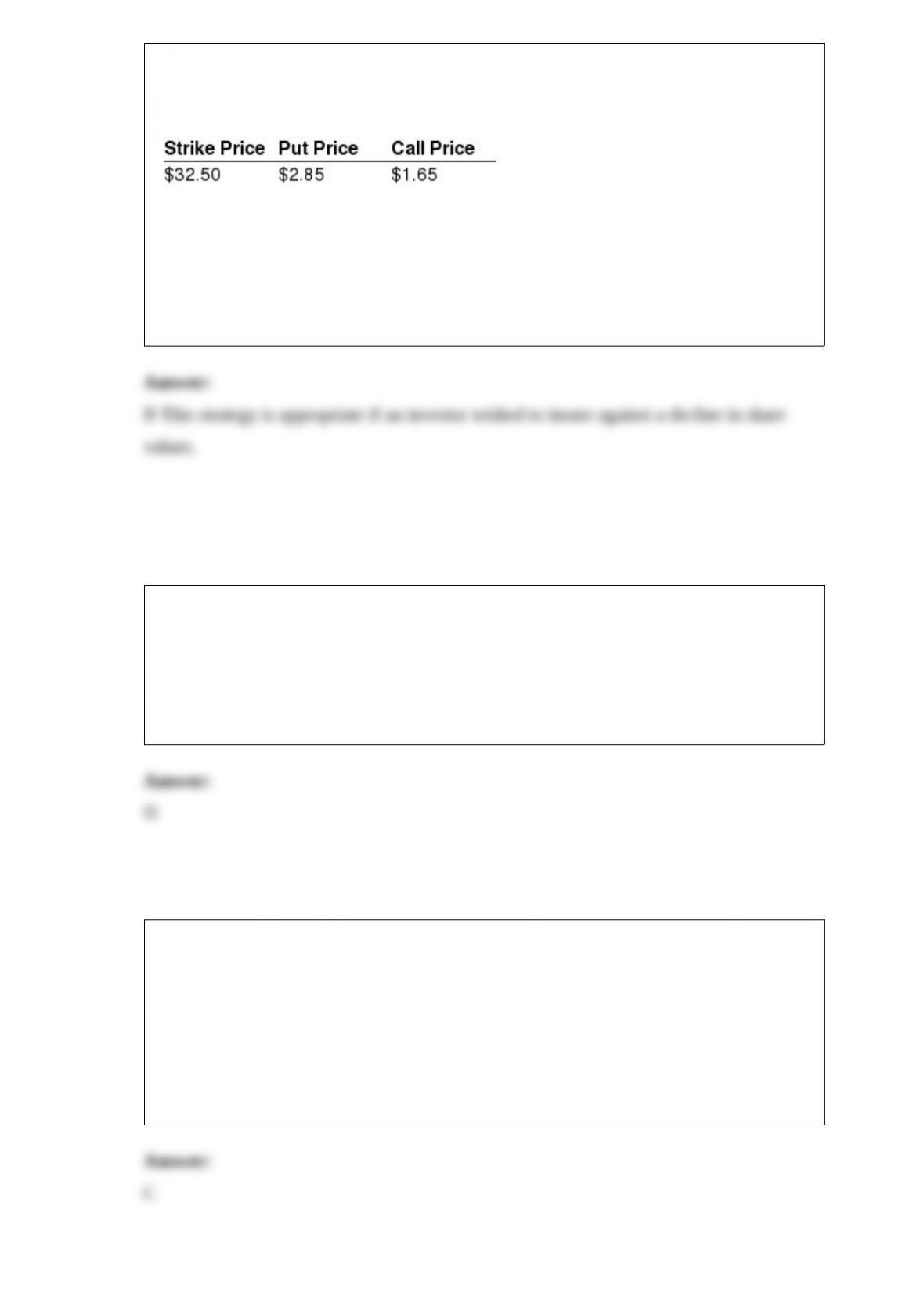

Consider the following information on put and call options for Citigroup

A protective put is an appropriate strategy if

a. An investor wishes to generate additional income.

b. An investor wished to insure against a decline in share values.

c. An investor expected share prices to be volatile.

d. An investor expected share prices to remain in a trading range.

e. An investor expected share prices to be volatile, but was inclined to be bullish.

2) Revenue bonds are

a. U.S. Treasury bonds backed by the full faith and credit of the issuer.

b. U.S. Treasury bonds backed by income generated form specific projects.

c. Municipal bonds backed by the full faith and credit of the issuer.

d. Municipal bonds backed by income generated from specific projects.

e. A type of U.S. agency security.

3) Superior analysts are encouraged to concentrate their efforts in "middle tier" stocks.

This is recommended because

a.it works to minimize taxes for the client.

b.only individuals deal in the middle tier stocks.

c.prices may not adjust quite as rapidly for middle tier stocks as they do in the top tier;

therefore, the chances of temporarily undervalued securities are greater.

d.it includes companies too small to be considered by institutions.

e.technical analysts never look at "middle tier" stocks.

4) Exhibit 23.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The Skalmory Corporation has entered into a 3-year interest rate swap, with semiannual

settlement, to pay a fixed rate of 7.5% per year and receive 6-month LIBOR. The

notional principal is $10,000,000.

Assume that one year later the fixed rate on a new 2-year receive fixed pay floating

LIBOR swap has fallen to 7% per year. Settlement is on a semiannual basis. Calculate

the market value of the FRN based on $100 face value.

a. $101.33

b. $100.58

c. $100.00

d. $98.67

e. $95.83

5) In ____ asset allocation, the investor's risk tolerance and constraints are assumed to

be constant over time. However, changes in capital market conditions result in changes

in the portfolio's stock-bond mix.

a. Integrated

b. Strategic

c. Tactical

d. Insured

e. None of the above.

6) The goal of the passive portfolio manager is to minimize

a. Alpha

b. Beta

c. Standard error

d. Tracking error

e. Portfolio risk

7) An investor who purchases a put option:

a.Has the right to buy a given stock at a specified price during a designated time period.

b.Has the right to sell a given stock at a specified price during a designated time period.

c.Has the obligation to buy a given stock at a specified price during a designated time

period.

d.Has the obligation to sell a given stock at a specified price during a designated time

period.

e.None of the above.

8) Exhibit 12.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

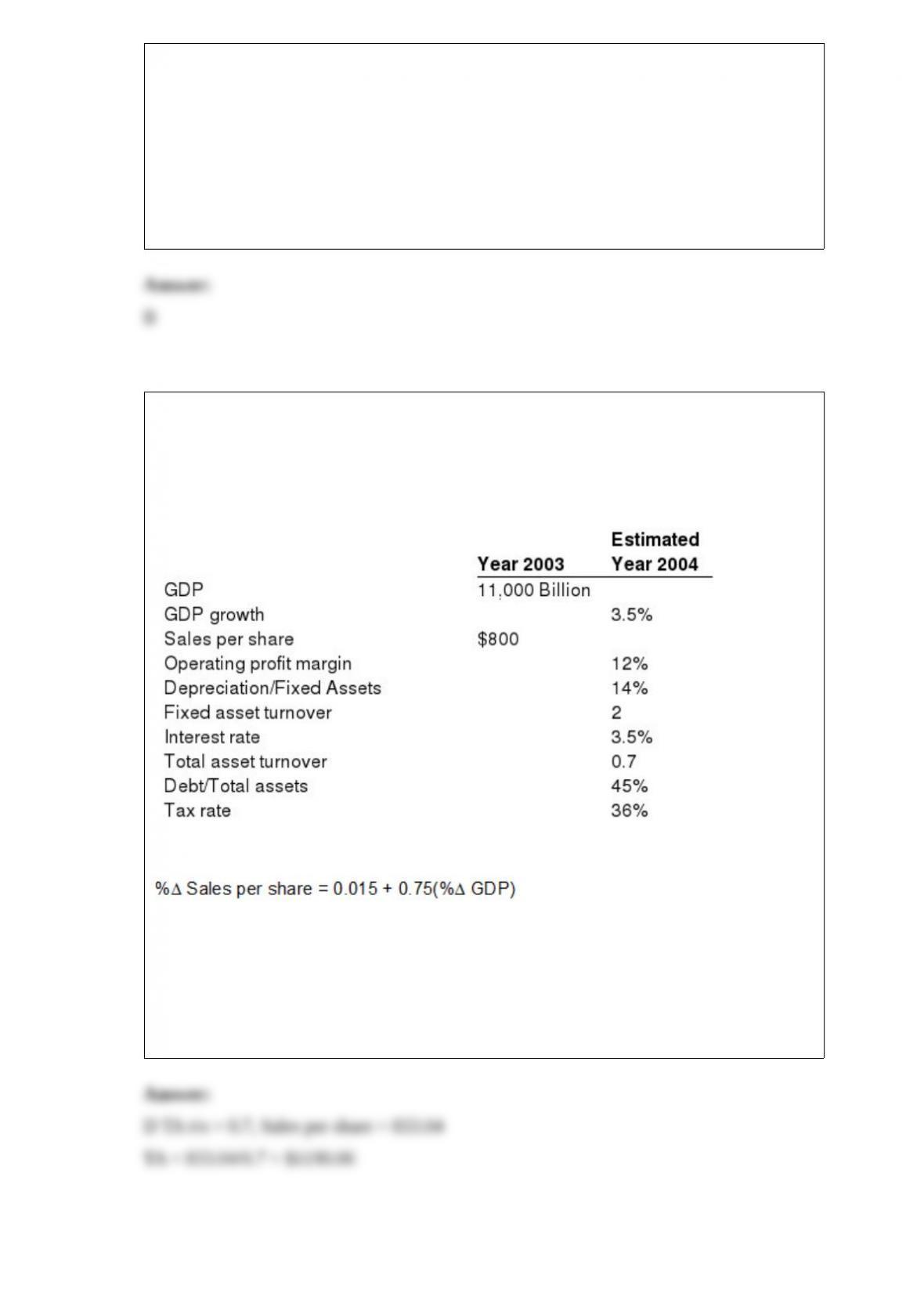

Consider the following information that you propose to use to obtain an estimate of

year 2004 EPS for the MacLog Company.

In addition a regression analysis indicates the following relationship between growth in

sales per share for MacLog and GDP growth is

Calculate the firm's level of Total Assets per share for the year 2004.

a. $1050.65

b. $1065.67

c. $1113.58

d. $1190.06

e. $1385.77

9) Exhibit 21.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

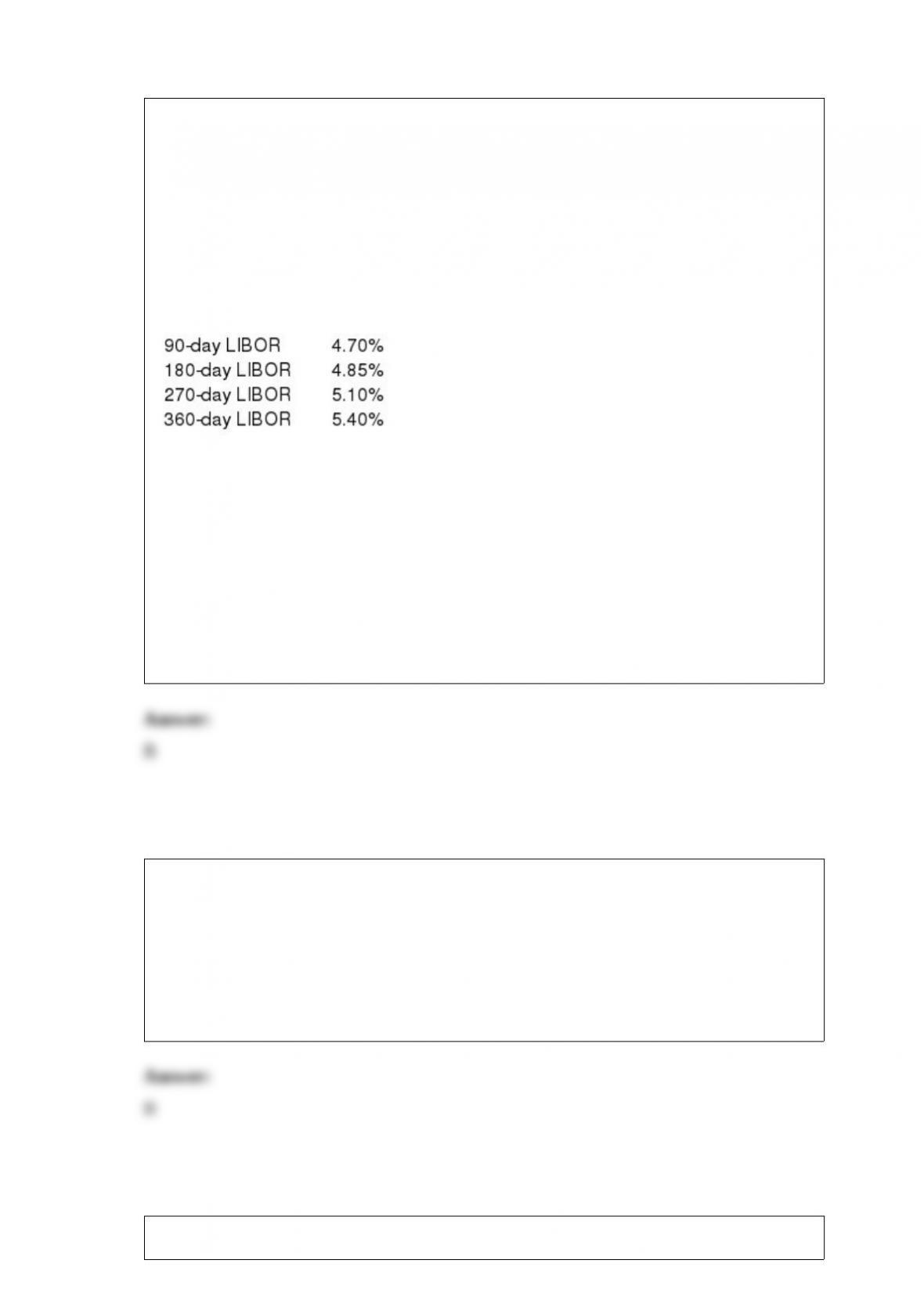

As a relationship officer for a money-center commercial bank, one of your corporate

accounts has just approached you about a one-year loan for $3,000,000. The customer

would pay a quarterly interest expense based on the prevailing level of LIBOR at the

beginning of each quarter. As is the bank's convention on all such loans, the amount of

the interest payment would then be paid at the end of the quarterly cycle when the new

rate for the next cycle is determined. You observe the following LIBOR yield curve in

the cash market:

If the bank wanted to hedge its exposure to falling LIBOR on this loan commitment,

describe the sequence of transactions in the futures markets it could undertake.

a. Buy 3 Eurodollar futures contracts that expire at the end of the first quarter.

b. Buy 3 Eurodollar futures contracts that expire at the end of the first quarter, 3 that

expire at the end of the second quarter, and 3 that expire at the end of the third quarter.

c. Sell 3 Eurodollar futures contracts that expire at the end of the year.

d. Sell one Eurodollar futures contract that expires at the end of the first quarter, one

that expires at the end of the second quarter, and one that expires at the end of the third

quarter.

e. Buy 3 Eurodollar futures contracts that expire at the end of the year.

10) The payment of any compensation for loss is contingent on the actual occurrence of

a credit-related event under a

a. Total return swap.

b. Credit default swap.

c. Collar.

d. Forward rate agreement.

e. Swap agreement.

11) Exhibit 21.11

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider a portfolio manager with a $10,000,000 equity portfolio under management.

The manager wishes to hedge against a decline in share values using stock index

futures. Currently a stock index future is priced at 1350 and has a multiplier of 250. The

portfolio beta is 1.50.

Assume that a month later the equity portfolio has a market value of $10,000,000 and

the stock index future is priced at 1300 with a multiplier of 250. Calculate the profit

(loss) on the stock index futures position.

a. -$1,050,000

b. -$550,000

c. -$50,000

d. $550,000

e. $1,050,000

12) Structural changes occur when the economy undergoes a major organizational

change or how it functions.

13) The growth of business depends on the percentage of earnings reinvested and the

return on equity.

14) A futures contract eliminates uncertainty about the future spot price that an

individual can expect to pay for an asset at the time of delivery.

15) Term life insurance provides both a death benefit and a savings plan.

16) Completeness funds are portfolios designed to complement active portfolios that do

not cover the entire market.

17) The majority of a pension fund's return is explained by asset allocation.

18) The standardization of option contracts and the creation of the Options Clearing

Corporation are two important results of the opening of the Chicago Board of Options

Exchange.

19) Forward contracts are individually designed agreements, and can be tailored to the

specific needs of the ultimate end-user.