Forward contracts in FX are typically written for periods exceeding 6 months.

Answer:

As of January 2012, credit cards used in either a credit or debit function accounted for

less than 5 percent of the dollar value of payments made in the U.S.

Answer:

Which of the following observations concerning credit unions is NOT TRUE?A. They

invest heavily in corporate securities.

B. Member loans constitute a majority of their total assets.

C. They tend to invest more of their assets in U.S. Treasuries than other DIs.

D. They engage in off-balance-sheet activities.

E. They focus more on providing services and less on profitability.

Answer:

Wholesale and retail motor vehicle loans and leases constitute the largest subcategory

of business loans.

Answer:

The repricing gap model is a book value accounting based model.

Answer:

Compared to the average commercial bank, credit unions tend to have higher overhead

expenses per dollar of assets.

Answer:

Finance companies generally have higher overhead than do commercial banks.

Answer:

Which of the following is NOT TRUE?A. FI bearing the credit risk of a loan is often

different from the FI that issued the loan.

B. The buyer of a credit swap makes periodic payments to the seller until the end of the

life of the swap.

C. Banks have been more willing than the insurance companies to bear credit risk.

D. The settlement of the swap in the event of a default involves either physical delivery

of the bonds or a cash payment.

E. Credit swap specifies the number of different bonds that can be delivered in the

event of a default.

Answer:

All of the following are relevant determinants of sovereign risk exposure: the rate of

domestic money supply growth; the variance of export revenue, and the size of the

population.

Answer:

Fed funds are short-term uncollateralized loans with maturities that typically do not

exceed one day.

Answer:

In international finance, the investment ratio measures the amount of real investment

relative to the gross national product of the country.

Answer:

Mortgage pools that are assumed to prepay at a rate of speed that is more rapid than the

PSA model would indicate, are said to prepay at less than 100 percent PSA behavior

because the mortgage life and balance will exist for a longer time.

Answer:

Interstate banking barriers have deteriorated in part because of the decisions to deal

with the failing thrift industry by allowing acquiring firms to cross state lines.

Answer:

Usury ceilings are maximum rates imposed by federal legislation that FIs can charge on

consumer and mortgage debt.

Answer:

The primary sellers of domestic loans are medium-sized regional banks.

Answer:

Purchased liquidity management carries the potential risk of significant increases in the

cost of funds during periods of high interest rate volatility.

Answer:

By 2008, the insurance company AIG had more than $440 billion in credit default

swaps outstanding.

Answer:

Highly leveraged transaction (HLT) loans are typically unsecured, short term and have

fixed rates.

Answer:

Securitized mortgage assets are used as collateral backing secondary market securities.

Answer:

The process of using lending power to coerce a loan customer to use products sold by a

securities affiliate is called information transfer.

Answer:

During the financial crisis of 2008-2009, deposit balances at DIs increased.

Answer:

Generally, at the retail level, an FI controls credit risks solely by using a range of

interest rates or prices and not by credit rationing.

Answer:

A disadvantage to international bank expansion is the potential increase in the

monitoring and information collection costs in some overseas markets.

Answer:

FIs that make loans or buy bonds with long maturity liabilities are more exposed to

interest rate risk than FIs that make loans or buy bonds with short maturity liabilities.

Answer:

The cash surrender value of a life insurance policy represents the payment to the

insured’s beneficiaries at the time of death.

Answer:

One advantage of swapping a sovereign loan for a bond is the capability to sell the bond

in the secondary market.

Answer:

Which of the following observations concerning hedge funds is NOT TRUE?A. They

are pooled investment vehicles.

B. Historically, they were not required to register with the SEC.

C. Historically, they were subject to virtually no regulatory oversight.

D. They usually take significant risk.

E. They have to disclose their activities to third parties.

Answer:

On September 7, 2008, FNMA and FHLMC were placed under conservatorship and

both are controlled by a federal government agency.

Answer:

The export revenue variance (VAREX) ratio tends to have high systematic risk elements

in a CRA analysis.

Answer:

Credit derivatives allow FIs to hedge credit risk on individual assets, but not on

portfolios of assets.

Answer:

The ability to form financial holding companies for the purpose of creating full-service

financial institutions has caused an increase in affiliate risk.

Answer:

The use of futures contracts by banks is subject to risk-based capital guidelines through

the off-balance-sheet risk calculations for risk-based capital.

Answer:

A charge reflecting the risk of the decline in the liquidity or credit risk quality of the

trading portfolio is the general market risk charge in the BIS framework.

Answer:

Whether fixed-rate or floating-rate, a swap arrangement can be designed to be

equivalent to a similar maturity bond.

Answer:

Finance companies are subject to regulations that restrict the types of products and

services they can offer to small business customers.

Answer:

FIs may increase fee income by serving as a counterparty for other entities wanting to

hedge risk on their own balance sheet.

Answer:

Finance companies generally attract less risky customers than do commercial banks.

Answer:

The SEC now requires mutual fund portfolio managers to report their personal trading

in individual stocks, but not in the portfolios they manage.

Answer:

Which of the following is NOT TRUE of an R class CMO issue?A. It is treated as

“garbage class.”

B. It is a high-risk investment class.

C. It gives the investor the rights to the over-collateralization and reinvestment income

on the cash flows in the CMO trust.

D. Returns increase when interest rates increase.

E. It has a positive duration.

Answer:

All bonds that are deliverable under a Treasury bond futures contract have a maturity of

20 years and an interest rate of 8 percent.

Answer:

When banks use stored liquidity management, they A. must pay interest on the funds

that are stored.

B. store the funds at the U.S. Treasury.

C. necessarily increase the asset side of the balance sheet.

D. may shrink the balance sheet if cash is used as the liquidity adjustment mechanism.

E. threaten the capital position of the institution.

Answer:

Which of the following transactions does NOT meet the legal definition of a highly

leveraged transaction (HLT)? A. A buyout that increases debt from $100 million to

$150 million resulting in a 55 percent leverage ratio.

B. A recapitalization that increases debt from $100 million to $250 million resulting in

a 55 percent leverage ratio.

C. An acquisition that increases debt from $100 million to $250 million resulting in a

65 percent leverage ratio.

D. An acquisition that increases debt from $100 million to $150 million resulting in an

80 percent leverage ratio.

E. An acquisition that results in an 80 percent leverage ratio.

Answer:

The following question are based on material in Appendix 8B

The unbiased expectations theory of the term structure of interest rates A. assumes that

long-term interest rates are an arithmetic average of short-term rates.

B. assumes that the yield curve reflects the market’s current expectations of future

short-term interest rates.

C. recognizes that forward rates are perfect predictors of future interest rates.

D. assumes that risk premiums increase uniformly with maturity.

E. None of the above.

Answer:

If the loan portfolio consists of five-year, 10 percent annual coupon par value loans,

what is the market, or economic, value of capital if interest rates decrease 2 percent?A.

$35 million.

B. $96 million.

C. $60 million.

D. -$7 million.

E. $0.

Answer:

In contrast to earlier periods in the finance company industry, during the middle 2000s,

A. regulatory reform led to decreasing profits.

B. mortgages originated were generally not securitized.

C. new car loan rates charged by finance companies were been lower than those of

commercial banks.

D. mortgage lending become less important to the industry.

E. finance companies were required to offer time deposit products to their customers.

Answer:

If interest rates increase 75 basis points for an FI that has a gap of -$15 million, the

expected change in net interest income is A. -$112,500.

B. +$112,500.

C. +$1,125,0000.

D. -$1,125,0000.

E. -$150,000.

Answer:

Which of the following is the most important source of funds for savings institutions?

A. Borrowings from the Federal Home Loan Bank.

B. Small time and savings deposits.

C. Repurchase agreements.

D. Direct federal fund borrowings.

E. Negotiable certificates of deposit.

Answer:

For put options, the delta has a negative sign A. since the value of the put option falls

when bond prices rise.

B. since the value of the put option rises when bond prices rise.

C. since the value of the put option falls when bond prices fall.

D. since the change in interest rates is equal to the change in the interest rate on the

bond underlying the option contract.

E. to adjust for basis risk.

Answer:

What is overhedging? A. Selectively hedging a proportion of an FI’s balance sheet

position.

B. Choosing to bear some interest rate risk as well as credit and FX risks.

C. Reducing the risk to the lowest level possible.

D. Using more hedge vehicles than is necessary to offset the risk in the cash asset.

E. Partially hedging the individual assets and liabilities.

Answer:

The delta of an option isA. a measure of the option’s price volatility.

B. calculated by dividing the price of the underlying security by the change in the

option’s price.

C. equal to the option premium.

D. calculated by multiplying the change in the price of the underlying security by the

change in the option’s price.

E. usually negative.

Answer:

Using Z = 1.682 as the cut-off rate, what should be the debt to asset ratio of the firm in

order for the bank to approve the loan?A. 40.0 percent.

B. 46.5 percent.

C. 51.5 percent.

D. 54.0 percent.

E. 65.0 percent.

Answer:

The difference between the market value of assets and liabilities is the definition of the

A. accounting value of capital.

B. regulatory value of capital.

C. economic value of capital.

D. book value of net worth.

E. adjusted book value of net worth.

Answer:

Chinese Walls are A. internally imposed barriers that limits the flow of confidential

client information among departments or areas.

B. regulatory barriers that are introduced to insulate the bank against losses.

C. regulations that prohibit a bank from lending anything at all to its securities

affiliates.

D. restrictions on a bank holding company that prevents the use of subsidiary funds to

support ailing affiliates.

E. hurdles created by excessive drain in the form of dividends and fees from a bank.

Answer:

Match the following pieces of legislation with the function achieved by each regulation

as stated in question

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Advisers Act

D. Investment Company Act

E. Insider Trading and Securities Fraud Enforcement Act of 1988

F. Market Reform Act of 1990

G. National Securities Markets Improvement Act of 1996

Exempts mutual fund sellers from oversight by state securities regulators.

Answer:

A type of company that specializes in distressed loans is A. a bank loan mutual fund.

B. a domestic bank.

C. a foreign bank.

D. an investment bank.

E. a vulture fund.

Answer:

A negative net exposure position in FX implies that the FI is A. net long in a currency

and exposed to depreciation of the foreign currency.

B. net short in a currency and exposed to depreciation of the foreign currency.

C. net long in a currency and exposed to appreciation of the foreign currency.

D. net short in a currency and exposed to appreciation of the foreign currency.

E. neither long nor short in a currency.

Answer:

Which of the following are normally traded at very deep discounts from 100 percent?

A. Restructured loans.

B. Brady bonds.

C. Sovereign bonds.

D. Performing loans.

E. Nonperforming loans.

Answer:

What is the expected return on the loan to the bank if 50 percent of the loan is drawn

immediately and there are no reserve requirements on demand deposits? Do not take

future values of fees or interest income received. A. 13.45 percent.

B. 13.57 percent.

C. 13.60 percent.

D. 13.72 percent.

E. 13.90 percent.

Answer:

Which of the following is a benefit to the borrower in a loan rescheduling? A. The FI

may receive tax benefits.

B. Rescheduling may close the market for future loans.

C. Rescheduling may create interruptions in the flow of international trade since letters

of credit may be more difficult to acquire.

D. Rescheduling may lower the present value of future payments in hard currencies.

E. The FI may receive additional fees, collateral, and option features on the loan.

Answer:

Which of the following describes debt rescheduling? A. Outright cancellation of all

current and future debt obligations.

B. Changing the contractual terms of a loan, such as its maturity and interest payments.

C. Direct nationalization of private sector assets.

D. Automatic default of all international loans upon default of any one loan.

E. Debt conversion schemes of debtor countries that signal creditworthiness.

Answer:

Which of the following is NOT a social welfare effect of bank runs? A. Discipline of

incompetent managers.

B. Negatively affecting the payments function of DIs.

C. Reduced availability of credit.

D. Potential decrease in the money supply.

E. Inability to perform intergenerational wealth transfers.

Answer:

How can interest expense of an FI be reduced by improved technological efficiency?

A. By improving the efficiency of management of information flows.

B. By obtaining access to low cost sources of funds.

C. By linking services to the quality of the FI’s technology.

D. By innovating new interest earning products.

E. By complying with all government regulations.

Answer:

Which of the following variables can have a negative impact on the probability of

rescheduling in the credit scoring model to estimate sovereign country risk exposure?

A. The debt service ratio.

B. The import ratio.

C. The variance of export revenue.

D. The investment ratio.

E. Domestic money supply growth.

Answer:

An FI has purchased (borrowed) a one-year $10 million Eurodollar deposit at an annual

interest rate of 6 percent. It has invested these proceeds in one-year Euro (€) bonds at an

annual rate of 6.5 percent after converting them at the current spot rate of €1.75/$. Both

interest and principal are paid at the end of the year.

What is the spread earned by the bank at the end of the year if the exchange rate

remains at €1.75/$? A. 0.50 percent.

B. 1.00 percent.

C. 1.5 percent.

D. 2.0 percent.

E. 2.5 percent.

Answer:

91-day Treasury bill rates = 9.71 percent

91-day Treasury bill futures rates = 9.66 percent

(Reminder: Treasury bill prices are calculated using the following formula:

P = FV * (1 – dt/360)

where P = price, FV = face value, d = discount yield, and t = days until maturity.)

What is the basis on the T-bill futures contract? A. 19 basis points.

B. 21 basis points.

C. 5 basis points.

D. 2 basis points.

E. Insufficient information.

Answer:

What is the defining characteristic of the dual banking system?A. Coexistence of

parent and holding companies.

B. Coexistence of both nationally chartered and state chartered banks.

C. Control of nationally chartered and state chartered banks by the state regulators.

D. Control of nationally chartered banks by both FRS and State bank regulators.

E. Nonbanking companies carrying out both banking and other activities.

Answer:

The buyer of a bond call option A. receives a premium in return for standing ready to

sell the bond at the exercise price.

B. receives a premium in return for standing ready to buy bonds at the exercise price.

C. pays a premium and has the right to sell the underlying bond at the agreed exercise

price.

D. pays a premium and has the right to buy the underlying bond at the agreed exercise

price

E. pays a premium and has the obligation to buy the underlying bond at the agreed

exercise price

Answer:

An investment banker agrees to underwrite an issue of 5 million shares of stock for

NetChoice, Inc. on a best-efforts basis. The investment banker is able to sell 4.5 million

shares for $31.00 per share and it charges NetChoice, Inc. $0.375 per share sold.

If the investment bank were able to sell all 5 million shares for $35, how much money

would NetChoice, Inc. receive? A. $195,675,000.

B. $187,500,000.

C. $130,250,000.

D. $175,000,000.

E. $173,125,000.

Answer:

Failure to meet the capital conservations buffer and the countercyclical buffer

guidelines instituted under Basel III will result in limits to all of the following except

A. bonuses paid to executives of the institution.

B. regularly scheduled dividends paid to stockholders.

C. special dividends meant to distribute retained earnings to stockholders.

D. lending to international entities.

E. buyback programs of common stock.

Answer:

Which of the following is a centralized collection service for corporate payments that

helps reduce the float? A. Funds concentration.

B. Electronic billing.

C. Treasury management.

D. Controlled disbursement accounts.

E. Wholesale lockbox.

Answer:

Regulatory-defined capital and required leverage ratios are based in whole or in part on

A. market value accounting concepts.

B. book value accounting concepts.

C. the net worth concept.

D. the economic meaning of capital.

E. None of the above.

Answer:

Use the following two choices to identify whether each intermediary or entity is a net

buyer or net seller of credit derivative securities.

a. Net buyer (typically)

b. Net seller (typically)

Mutual funds

Answer:

Match each of the following potential conflicts of interest with their corresponding

definition or description.

A/ When a bank suggests the issuance of capital market debt for the purpose of

reducing bank loans under conditions of deteriorating or questionable firm financial

health.

B/ The use of inside information about customers or rivals that can be useful in setting

securities prices or distributing securities offerings.

C/ When banks have the power to sell nonbank products, employees may no longer

give dispassionate, or unbiased, advice to customers.

D/ To avoid being exposed to potential losses in a securities offering, a bank may place

the securities in the accounts of customers in the trust department or other areas over

which it has discretionary investment powers.

E/ The approval of cheap loans to an investor under the implicit condition that the loan

proceeds are to be used to purchase securities underwritten by a securities affiliate.

F/ Using lending power to coerce a customer to purchase or use the products sold by an

affiliate.

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

The risk-based capital requirements have received several types of criticism. Please

match the criticism headings below (as stated in the text) with the appropriate

criticism.1. Excessive complexity2. DI specialness3. Impact on capital

requirements4. Other risks

5. Pillar 2 may ask too

much of regulators6. Risk weights based on

external credit rating agencies7. Competition8. Portfolio aspects9. Risk weights

A/ Because of different tax, accounting, and safety-net rules and the application of the

new Basel III rules to different industries, a level playing field across banks in different

countries will not occur.B/ Because DIs may have little incentive to make high risk

commercial loans, one important aspect of intermediation may be somewhat

curtailed.C/ The benefits may not support the significant cost of developing and

implementing new risk management systems.D/ Banks in the U.S. likely would

need additional capital to meet the new minimum standards.E/ Interest rate and liquidity

risks are not yet included in the proposed Basel III plan.F/ Regulators may not be

trained or willing to make the necessary decisions that may rely heavily on judgment.G/

The BIS plans largely ignore the covariance among asset risks between different

parties.H/ The four (five) risk weight categories in Basel I (Basel II) may not reflect the

true credit risk.I/ Because rating agencies often lag rather than lead the business cycle,

risk weights based on a loan’s credit

rating may not accurately measure the relative risk exposure of individual borrowers.

Answer:

Answer:

Answer:

Answer:

Answer:

Use the following two choices to identify whether each intermediary or entity is a net

buyer or net seller of credit derivative securities.

a. Net buyer (typically)

b. Net seller (typically)

Insurance companies

Answer:

Answer:

Use the following two choices to identify whether each intermediary or entity is a net

buyer or net seller of credit derivative securities.

a. Net buyer (typically)

b. Net seller (typically)

Securities firms

Answer:

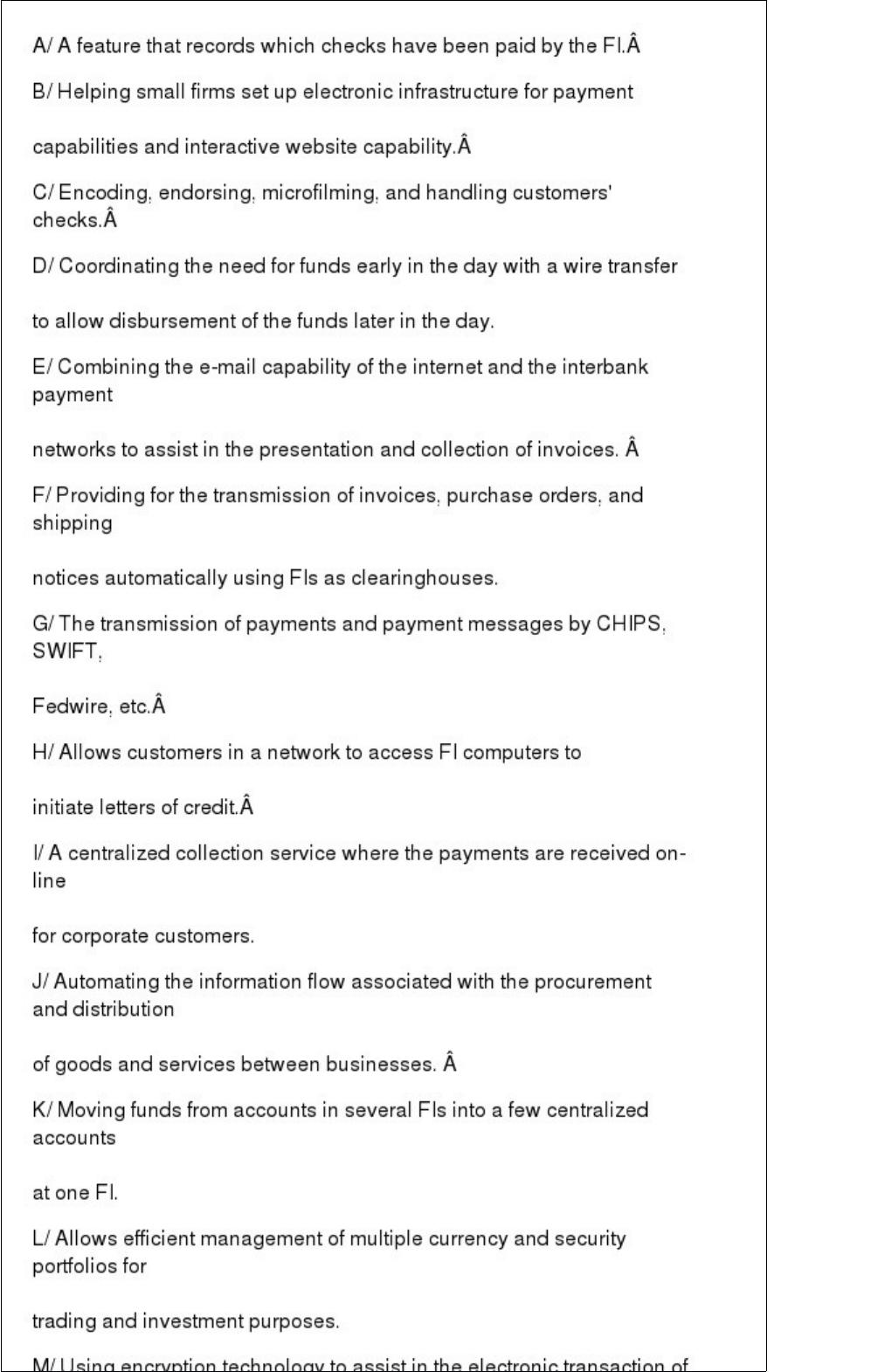

Choose among the following services provided by modern FIs.1. Funds

concentration2. Electronic initiation of letters of credit3. Check deposit

services4. Account reconciliation5. Treasury management software6. Facilitating

business-to-business e-commerce7. Electronic lockbox8. Assisting small business

entries into e-commerce9. Electronic billing10. Electronic data

interchange11. Wholesale lockbox

12. Electronic funds transfer13. Verifying identities14. Controlled disbursement

accounts

Answer:

Answer: