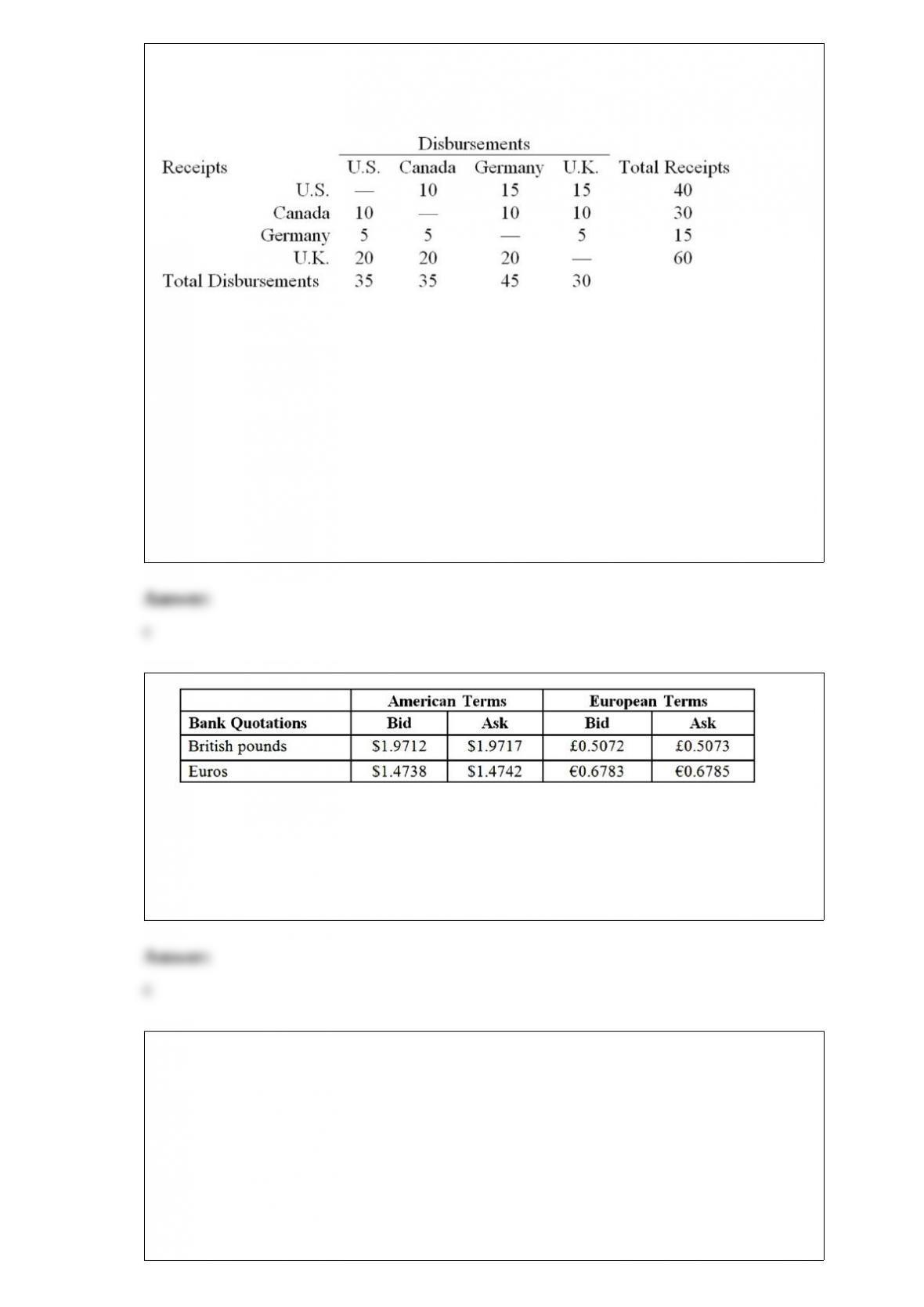

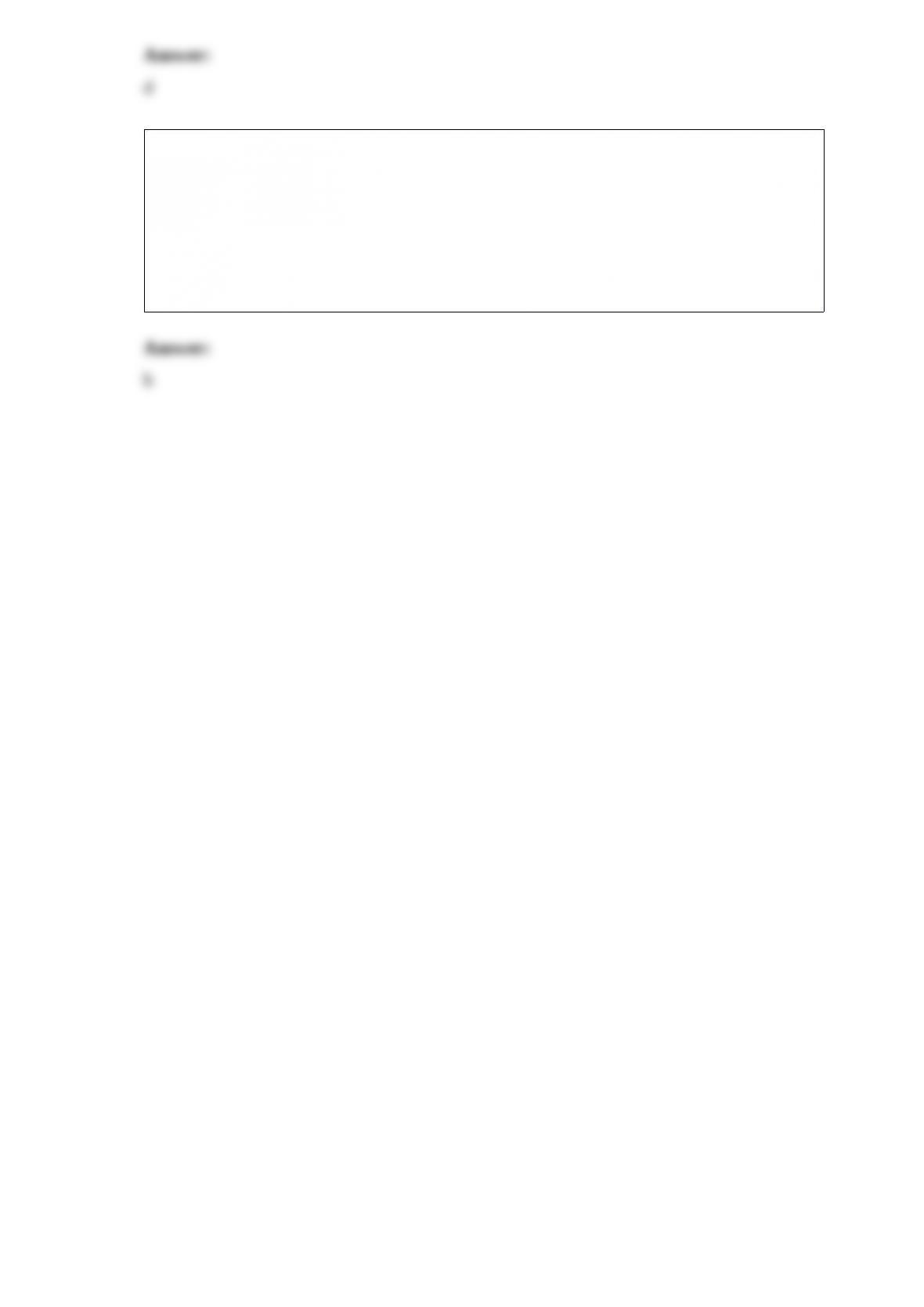

1) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

find the net cash flow in (out of) the german affiliate.

a.$5,000 in

b.$5,000 out

c.$30,000 out

d.$30,000 in

e.none of the above

2)

using the table above, what is the bid price of euro in terms of pounds?

a.1.3371/£

b.1.3378/£

c.£0.7475/

d.£0.7479/

3) when a country must make a net payment to foreigners because of a

balance-of-payments deficit, the central bank of the country

a.should do nothing

b.should run down its official reserve assets (e.g. gold, foreign exchanges, and sdrs)

c.should borrow anew from foreign central banks

d.either b or c will work

4) comparing “forward” and “futures” exchange contracts, we can say that

a.they are both “marked-to-market” daily

b.their major difference is in the way the underlying asset is priced for future purchase

or sale: futures settle daily and forwards settle at maturity

c.a futures contract is negotiated by open outcry between floor brokers or traders and is

traded on organized exchanges, while forward contract is tailor-made by an

international bank for its clients and is traded otc

d.both b and c

5) suppose the u.s. dollar substantially depreciates against the japanese yen. the change

in exchange rate

a.can have significant economic consequences for u.s. firms

b.can have significant economic consequences for japanese firms

c.can have significant economic consequences for both u.s. and japanese firms

d.none of the above

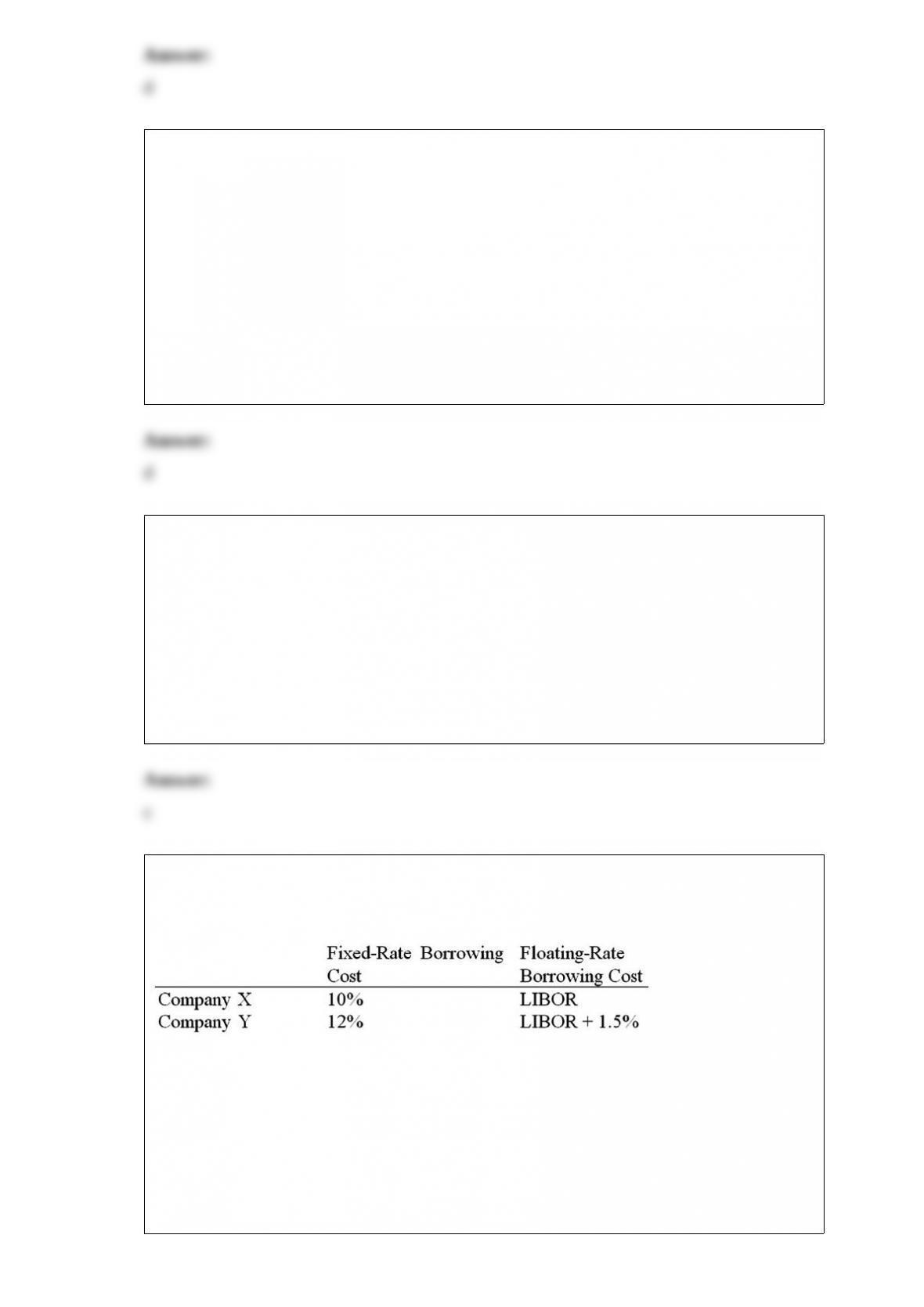

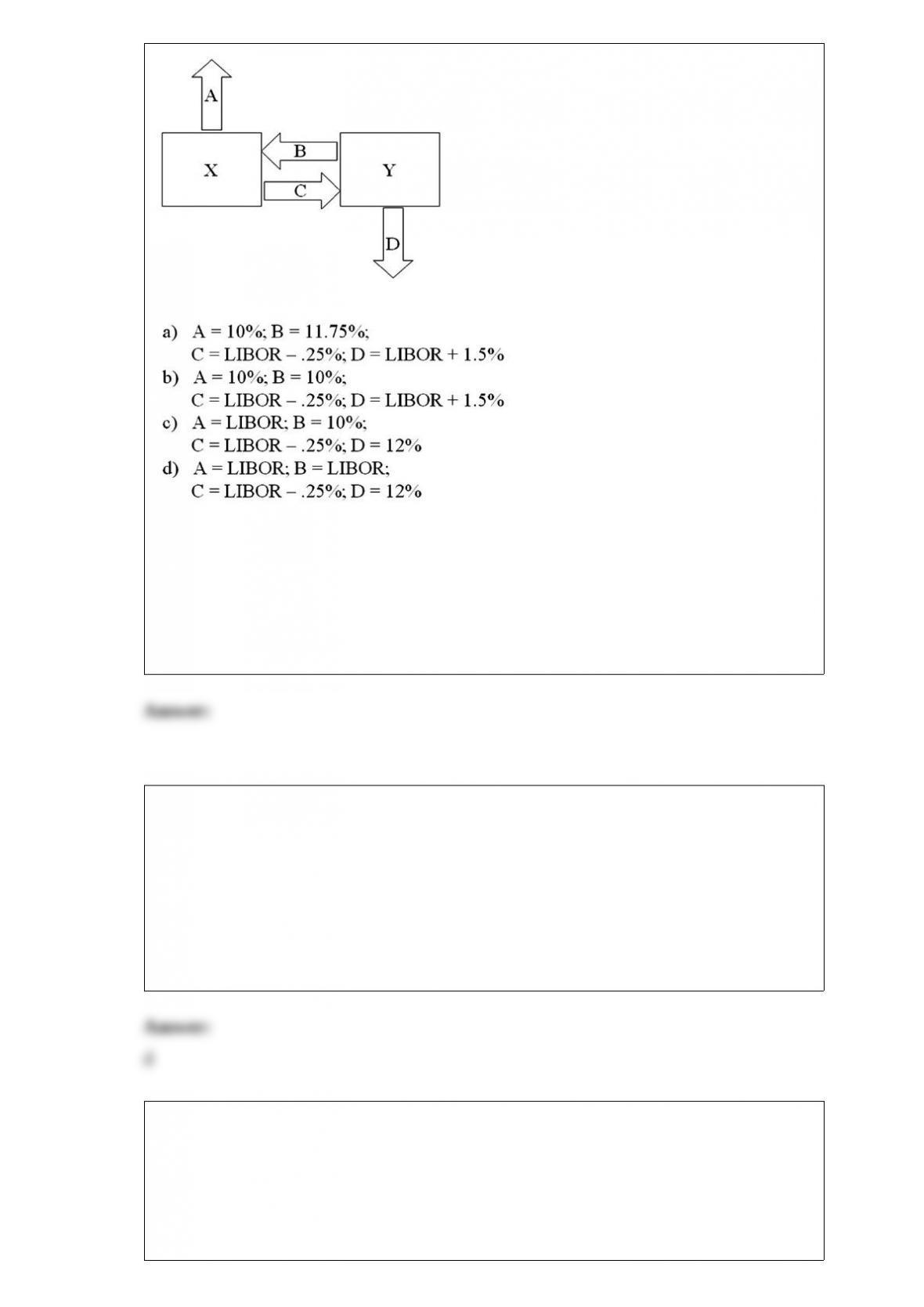

6) company x wants to borrow $10,000,000 floating for 5 years. company y wants to

borrow $10,000,000 fixed for 5 years. their external borrowing opportunities are:

design a mutually beneficial interest only swap for x and y with a notational principal of

$10 million by having appropriate values for

a = company x’s external borrowing rate

b = company y’s payment to x (rate)

c = company x’s payment to y (rate)

d = company y’s external borrowing rate

a.option a

b.option b

c.option c

d.option d

7) although irp tends to hold, it may not hold precisely all the time

a.due to transactions costs, like the bid ask spread

b.due to asymmetric information

c.due to capital controls imposed by governments

d.both a and c

8) with regard to operational hedging versus financial hedging,

a.operational hedging provides a more stable long-term approach than does financial

hedging

b.financial hedging, when instituted on a rollover basis, is a superior long-term

approach to operational hedging

c.since they both have the same goal, stabilizing the firm’s cash flows in domestic

currency, they are fungible in use

d.none of the above

9) a “good” (or ideal) international monetary system should provide

a.liquidity, elasticity, and flexibility

b.elasticity, sensitivity, and reliability

c.liquidity, adjustments, and confidence

d.none of the above

10) the turnover ratio percentages for 36 equity markets of emerging markets for the

five years beginning with 2002 were measured. many of the small equity markets in

each region (e.g., peru, venezuela, sri lanka, slovak republic, croatia, and zimbabwe)

have relatively low turnover ratios,

a.indicating poor liquidity at present

b.indicating good liquidity at present

c.indicating strong investment performance over the period

d.none of the above

11) if the interest rate in the u.s. is i$ = 5 percent for the next year and interest rate in

the u.k. is i£ = 8 percent for the next year, uncovered irp suggests that

a.the pound is expected to depreciate against the dollar by about 3 percent

b.the pound is expected to appreciate against the dollar by about 3 percent

c.the dollar is expected to appreciate against the pound by about 3 percent

d.both a and c

12) consider a trader who takes a long position in a six-month forward contract on the

euro. the forward rate is $1.75 = 1.00; the contract size is 62,500. at the maturity of the

contract the spot exchange rate is $1.65 = 1.00.

a.the trader has lost $625

b.the trader has lost $6,250

c.the trader has made $6,250

d.the trader has lost $66,287.88