Fiscal policy is difficult to implement quickly because

A. it requires political negotiations.

B. much of government spending is nondiscretionary and cannot be changed.

C. increases in tax rates affect consumer spending gradually.

D.-it requires political negotiations, and much of government spending is

nondiscretionary and cannot be changed.

E. it requires political negotiations, and increases in tax rates affect consumer spending

gradually.

The stage an individual is in his/her life cycle will affect his/her

A. return requirements.

B. risk tolerance.

C. asset allocation.

D. return requirements and risk tolerance.

E. All of the options are correct.

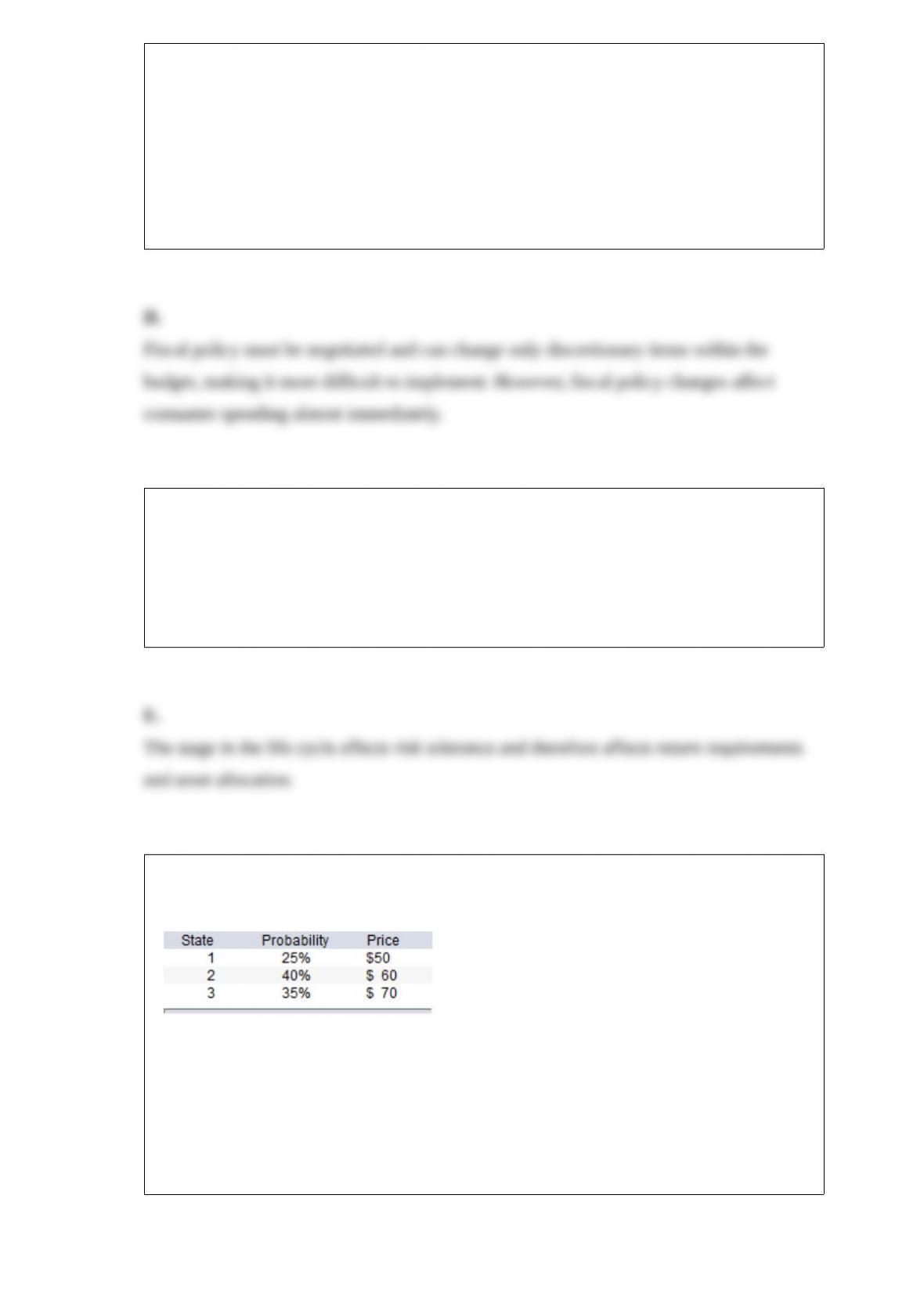

Toyota stock has the following probability distribution of expected prices one year from

now:

If you buy Toyota today for $55 and it will pay a dividend during the year of $4 per

share, what is your expected

holding-period return on Toyota?

A. 17.72%

B. 18.89%

C. 17.91%

D. 18.18%

Common size income statements make it easier to compare firms

A. that use different inventory valuation methods (FIFO vs. LIFO).

B. in different industries.

C. with different degrees of leverage.

D. of different sizes.

Light Construction Machinery Company has an expected ROE of 11%. The dividend

growth rate will be _______ if the firm follows a policy of paying 25% of earnings in

the form of dividends.

A. 3.0%

B. 4.8%

C. 8.25%

D. 9.0%

Efficient portfolios of N risky securities are portfolios that

A. are formed with the securities that have the highest rates of return regardless of their

standard deviations.

B. have the highest rates of return for a given level of risk.

C. are selected from those securities with the lowest standard deviations regardless of

their returns.

D. have the highest risk and rates of return and the highest standard deviations.

E. have the lowest standard deviations and the lowest rates of return.

Portfolio A consists of 150 shares of stock and 300 calls on that stock. Portfolio B

consists of 575 shares of stock. The call delta is 0.7. Which portfolio has a higher dollar

exposure to a change in stock price?

A. Portfolio B

B. Portfolio A

C. The two portfolios have the same exposure.

D. Portfolio A if the stock price increases and portfolio B if it decreases

E. Portfolio B if the stock price increases and portfolio A if it decreases

Kandel and Stambaugh (1995) expanded Roll’s critique of the CAPM by arguing that

tests rejecting a positive relationship between average return and beta are demonstrating

A. the inefficiency of the market proxy used in the tests.

B. that the relationship between average return and beta is not linear.

C. that the relationship between average return and beta is negative.

D. the need for a better way of explaining security returns.

E. None of the options are correct.

Variable life insurance

A. combines life insurance with a taxdeferred annuity.

B. provides a minimum death benefit that increases subject to investment performance.

C. can be converted to a stream of income.

D. All of the options are correct.

E. None of the options are correct.

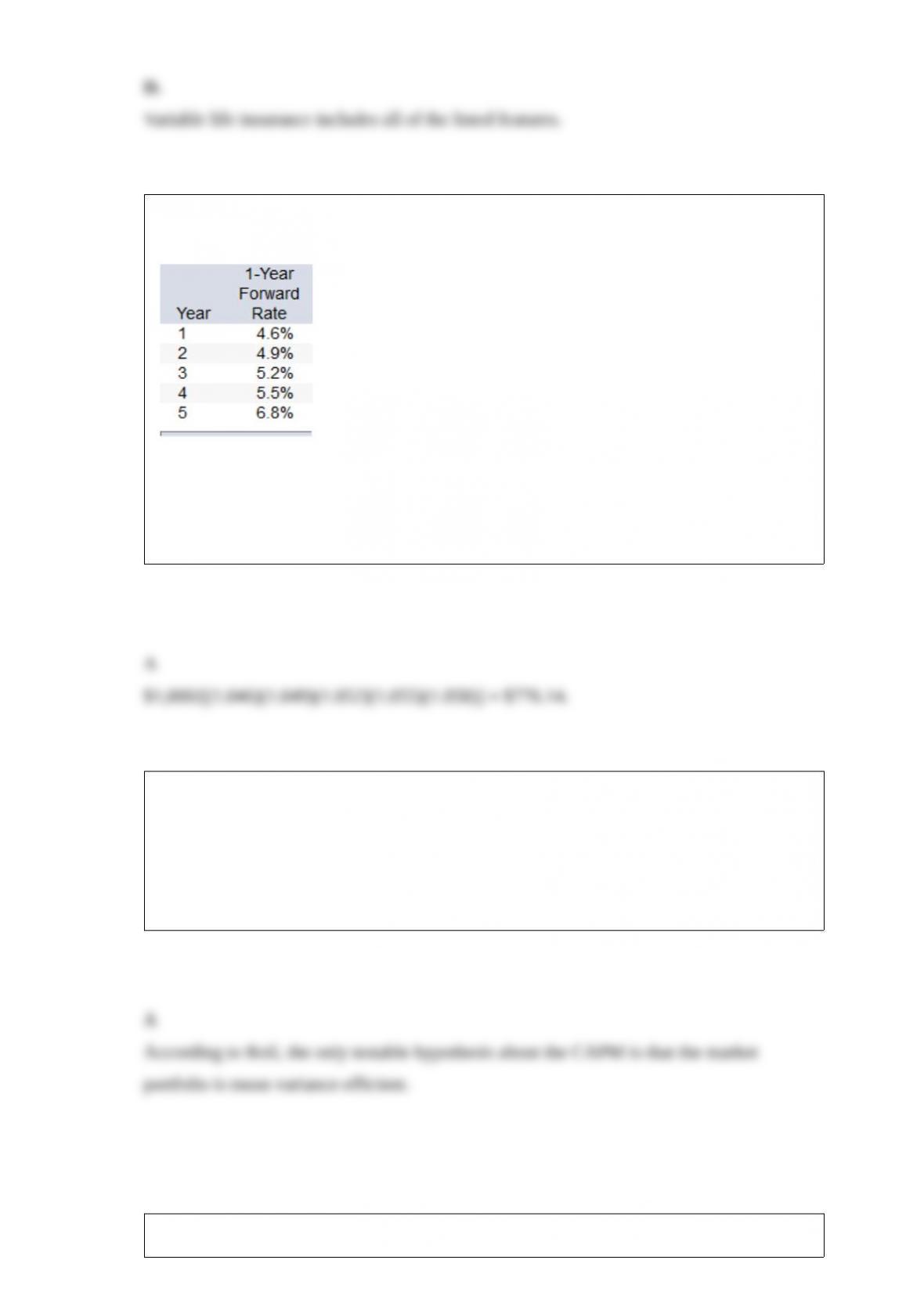

What should the purchase price of a 5-year zero-coupon bond be if it is purchased today

and has face value of $1,000?

A. $776.14

B. $721.15

C. $779.54

D. $756.02

E. $766.32

According to Roll, the only testable hypothesis associated with the CAPM is

A. the number of ex post mean variance efficient portfolios.

B. the exact composition of the market portfolio.

C. whether the market portfolio is mean variance efficient.

D. the SML relationship.

E. None of the options are correct.

When a distribution is negatively skewed,

A. standard deviation overestimates risk.

B. standard deviation correctly estimates risk.

C. standard deviation underestimates risk.

D. the tails are fatter than in a normal distribution.

Nondiversifiable risk is also referred to as

A. systematic risk or unique risk.

B. systematic risk or market risk.

C. unique risk or market risk.

D. unique risk or firm-specific risk.

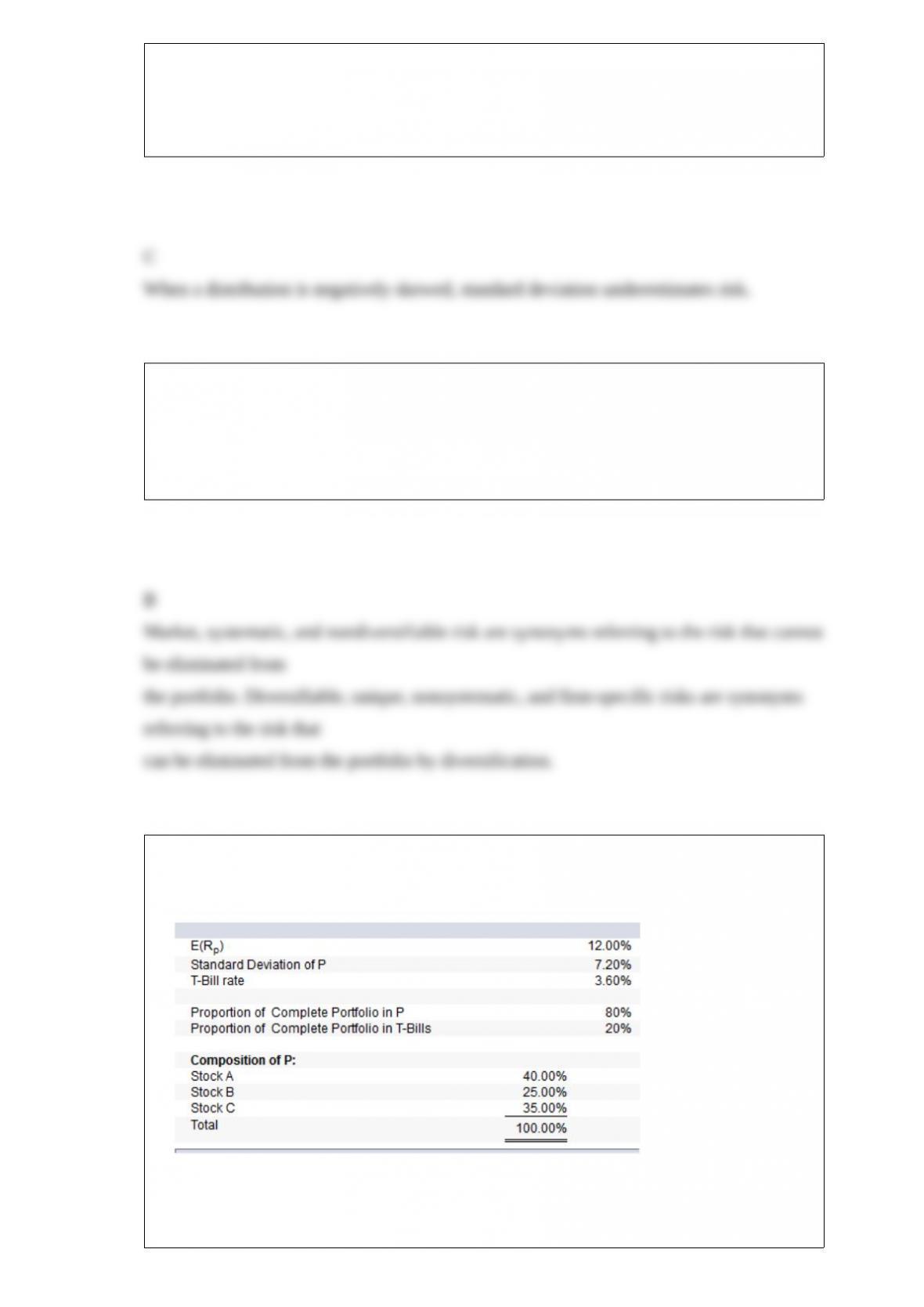

Your client, Bo Regard, holds a complete portfolio that consists of a portfolio of risky

assets (P) and T-Bills. The information below refers to these assets.

What is the standard deviation of Bo’s complete portfolio?

A. 7.20%

B. 5.40%

C. 6.92%

D. 4.98%

E. 5.76%

To maximize her expected utility, which one of the following investment alternatives

would she choose?

Assume an investor with the following utility function: U = E(r) 3/2(s2).

A. A portfolio that pays 10% with a 60% probability or 5% with 40% probability.

B. A portfolio that pays 10% with 40% probability or 5% with a 60% probability.

C. A portfolio that pays 12% with 60% probability or 5% with 40% probability.

D. A portfolio that pays 12% with 40% probability or 5% with 60% probability.

Holding other factors constant, the interest-rate risk of a coupon bond is lower when the

bond’s

A. term to maturity is lower.

B. coupon rate is higher.

C. yield to maturity is lower.

D. term to maturity is lower and coupon rate is higher.

E. All of the options are correct.

Liquidity embodies several characteristics, such as

A. trading costs.

B. ease of sale.

C. market depth.

D. necessary price concessions to effect a quick transaction.

E. All of the options are correct.

A firm has a (net profit/pretax profit) ratio of 0.6, a leverage ratio of 2, a (pretax

profit/EBIT) of 0.6, an asset turnover ratio of 2.5, a current ratio of 1.5, and a return on

sales ratio of 4%. The firm’s ROE is

A. 4.2%.

B. 5.2%.

C. 6.2%.

D. 7.2%.

E. None of the options are correct.

The most popular approach to forecasting the overall stock market is to use

A. the dividend multiplier.

B. the aggregate return on assets.

C. the historical ratio of book value to market value.

D. the aggregate earnings multiplier.

E. Tobin’s Q.

If covered interest arbitrage opportunities do not exist,

A. interest rate parity does not hold.

B. interest rate parity holds.

C. arbitragers will be able to make risk-free profits.

D. interest rate parity does not hold, and arbitragers will be able to make risk-free

profits.

E. interest rate parity holds, and arbitragers will be able to make risk-free profits.

The global minimum variance portfolio formed from two risky securities will be

riskless when the correlation

coefficient between the two securities is

A. 0.0.

B. 1.0.

C. 0.5.

D. –1.0.

E. any negative number.

Absent research, you should assume the alpha of a stock is

A.zero.

B. positive.

C. negative.

D. not zero.

E. zero or positive.

Studies of mutual-fund performance

A. indicate that one should not randomly select a mutual fund.

B. indicate that historical performance is not necessarily indicative of future

performance.

C. indicate that the professional management of the fund insures above market returns.

D. indicate that one should not randomly select a mutual fund and indicate that

historical performance is not necessarily indicative of future performance.

E. indicate that historical performance is not necessarily indicative of future

performance and indicate that the professional management of the fund insures above

market returns.

A coupon bond pays annual interest, has a par value of $1,000, matures in 12 years, has

a coupon rate of 8.7%, and has a yield to maturity of 7.9%. The current yield on this

bond is

A. 8.39%.

B. 8.43%.

C. 8.83%.

D. 8.66%.

E. None of the options are correct.

Consider a single factor APT. Portfolio A has a beta of 1.0 and an expected return of

16%. Portfolio B has a beta of 0.8 and an expected return of 12%. The risk-free rate of

return is 6%. If you wanted to take advantage of an arbitrage opportunity, you should

take a short position in portfolio __________ and a long position in portfolio _______.

A. A; A

B. A; B

C. B; A

D. B; B

E. A; the riskless asset

Consider the multifactor model APT with two factors. Portfolio A has a beta of 0.75 on

factor 1 and a beta of 1.25 on factor 2. The risk premiums on the factor-1 and factor-2

portfolios are 1% and 7%, respectively. The risk-free rate of return is 7%. The expected

return on portfolio A is __________ if no arbitrage opportunities exist.

A. 13.5%

B. 15.0%

C. 16.5%

D. 23.0%

The curvature of the price yield curve for a given bond is referred to as the bond’s

A. modified duration.

B. immunization.

C. sensitivity.

D. convexity.

E. tangency.

__________ center on the tradeoff between the return the investor wants and how much

risk the investor is willing to assume.

A. Investment constraints

B. Investment objectives

C. Investment policies

D. All of the options are correct.

E. None of the options are correct.

The price of a stock put option is __________ correlated with the stock price and

__________ correlated with the strike price.

A. positively; positively

B. negatively; positively

C. negatively; negatively

D. positively; negatively

E. not; not

A year ago, you invested $1,000 in a savings account that pays an annual interest rate of

4.3%. What is your

approximate annual real rate of return if the rate of inflation was 3% over the year?

A. 4.3%

B. –1.3%

C. 7.3%

D. 3%

E. None of the options.

Midwest Airline is expected to pay a dividend of $7 in the coming year. Dividends are

expected to grow at the rate of 15% per year. The risk-free rate of return is 6%, and the

expected return on the market portfolio is 14%. The stock of Midwest Airline has a beta

of 3.00. The return you should require on the stock is

A. 10%.

B. 18%.

C. 30%.

D. 42%.

Studies of negative earnings surprises have shown that there is

A. a negative abnormal return on the day that negative earnings surprises are

announced.

B. a positive drift in the stock price on the days following the earnings surprise

announcement.

C. a negative drift in the stock price on the days following the earnings surprise

announcement.

D. a negative abnormal return on the day that negative earnings surprises are announced

and a positive drift in the stock price on the days following the earnings surprise

announcement.

E. a negative abnormal return on the day that negative earnings surprises are announced

and a negative drift in the stock price on the