It is easy to differentiate between political and economic risks, since they are generally

unrelated. True or False

Answer:

So-called permanent financing for an acquisition usually consists of long-term

unsecured debt. True or False

Answer:

So-called Morris Trust transactions tax code rules restrict how certain types of

corporate deals can be structured to avoid taxes. True or False

Answer:

Smaller creditors have little incentive to attempt to hold up the agreement unless they

receive special treatment.

Answer:

In the U.S., the Federal Trade Commission has the exclusive right to approve mergers

and acquisitions if they are determined to be potentially anti-competitive. True or False

Answer:

A disadvantage of a split-off is that they tend to increase the pressure on the spun-off

firm’s share price, because shareholders who exchange their stock are more likely to sell

the new stock. True or False

Answer:

The term capitalization refers to the conversion of a future income stream into a present

value, and it is a term often used by business appraisers when future income or cash

flows are not expected to grow or to grow at a constant rate. True or False

Answer:

A firm’s core competencies refer to those skills which are required to produce the firm’s

primary products but which have little or no application in producing related products.

True or False

Answer:

The justification for the adjusted present value (APV) method reflects the theoretical

notion that firm value should not be affected by the way in which it is financed.

However, recent studies empirical suggest that for LBOs, the availability and cost of

financing does indeed impact financing and investment decisions. True or False

Answer:

The empirical evidence shows that unrelated diversification is an effective means of

smoothing out the business cycle. True or False

Answer:

Valuing the assets separately in terms of what it would cost to replace them may

seriously overstate the firm’s true going concern value. True or False

Answer:

Empirical studies show that the business alliance announcements seldom have any

impact on the market value of their parent firms. True or False

Answer:

A standstill agreement is one in which the target firm agrees not to solicit bids from

other potential buyers while it is negotiating with the first bidder. True or False

Answer:

Private firms are likely to understate revenue and understate costs in order to minimize

their tax liabilities. True or False

Answer:

It is rarely useful to review more than one or two years of historical data for the

acquiring or target firms. True or False

Answer:

As part of a Chapter 15 proceeding, the U.S. bankruptcy court may authorize a trustee

to act in a foreign country on behalf of the U.S. Bankruptcy Court. True or False

Answer:

Financial ratio analysis is the calculation of performance ratios from data in a

company’s financial statements to identify the firm’s financial strengths and

weaknesses. True or False

Answer:

The major disadvantages of a sub-chapter S corporation are that the number of

shareholders is limited, corporate shareholders are excluded, it must distribute all of its

earnings, the liability of shareholders is limited, and it can issue only one class of stock.

True or False

Answer:

Restructuring actions may provide tax benefits that cannot be realized without

undertaking a restructuring of the business. True or False

Answer:

Real options, also called strategic management options, refer to management’s ability to

adopt and later revise corporate investment decisions. True or False

Answer:

When cash flow is temporarily depressed due to strikes, litigation, warranty claims, or

other one-time events, it is generally safe to assume that cash flow will recover in the

near term. True or False

Answer:

The actual purchase price paid for a target firm is determined doing the negotiation

process and is often quite different from the initial offer price stipulated in a letter of

intent. True or False

Answer:

International transactions tend to be highly challenging, as they typically involve

multiple tax and legal jurisdictions. True or False

Answer:

The purchase price may be fixed at the time of closing, subject to future adjustment, or

it may be contingent on future performance of the target business. True or False

Answer:

The cost of capital method attempts to adjust future cash flows for changes in the cost

of capital as the firm reduces its outstanding debt. True or False

Answer:

Many analysts use the cost of capital method because of its relative simplicity. True or

False

Answer:

Potential competitors include firms (both domestic and foreign) in the current market,

those in related markets, current customers, and current suppliers. True or False

Answer:

Family owned businesses account for about 89% of all businesses in the U.S. True or

False

Answer:

Membership or subscription businesses, such as health clubs and magazine publishers,

may inflate revenue by booking the full value of muliyear contracts in the first year of

the contract. True or False

Answer:

A firm should choose that strategy from among the range of reasonable alternatives that

enables it to achieve its stated objectives in an acceptable time period without regard for

resource constraints. True or False

Answer:

Prepackaged bankruptcies are less common today than in years past. True or False

Answer:

Foreign competitors are not relevant to antitrust regulators when trying to determine if a

merger of two domestic firms would create excessive pricing power. True or False

Answer:

In emerging countries where financial statements may be haphazard and gaining access

to the information necessary to adequately assess risk is limited, it may be impossible to

perform an adequate due diligence. Under these circumstances, acquirers may protect

themselves by including a put option in the agreement of purchase and sale. Such an

option would enable the buyer to require the seller to repurchase shares from the buyer

at a predetermined price under certain circumstances. True or False

Answer:

With the purchase of target stock, the acquirer retains the target’s tax attributes, but

there is no step up in the basis of the acquired assets unless the acquirer adopts a 338

election. True or False

Answer:

Because the firm’s cost of equity changes over time, the firm’s cumulative cost of equity

is used to discount projected cash flows. This reflects the fact that each period’s cash

flows generate a different rate of return. True or False

Answer:

Parent firms with a high tax basis in a business may choose to spin-off the unit as a

tax-free distribution to shareholders rather than sell the business and incur a substantial

tax liability. True or False

Answer:

An excessively long list of screening criteria used to develop a list of potential

acquisition targets can severely limit the number of potential candidates. True or False

Answer:

In a merger, the acquiring firm assumes all liabilities of the target firm. Assumed

liabilities include all but which of the following?

a. Current liabilities

b. Long-term debt

c. Warranty claims

d. Fully depreciated operating equipment

e. Off-balance sheet liabilities

Answer:

All of the following are often cited as factors critical to the ultimate success of the

integration effort except for

a. Plan carefully, act quickly

b. The use of project management techniques

c. Early communication from the top of the organization

d. Salary and benefit reductions for many employees of the acquired company in order

to realize cost savings

e. Making the tough decisions as early as possible

Answer:

Which of the following are true about the Sherman Antitrust Act?

a. Prohibits business combinations that result in monopolies.

b. Prohibits business combinations resulting in a significant increase in the pricing

power of a single firm.

c. Makes illegal all contracts unreasonably restraining trade.

d. A and C only

e. A, B, and C

Answer:

To determine which strategy to pursue, the failing firm’s management needs to

estimate which of the following:

a. Going concern value

b. Liquidation value

c. Selling price of the firm

d. A and B only

e. A, B, and C

Answer:

Acquiring Corp agrees to buy 100% of the outstanding shares of Target Corp in a

share for share exchange. How would Acquiring Corp determine how many new share

of its

stock it would have to issue?

a. Multiply the purchase price premium paid for Target’s stock by the number of shares

of target stock outstanding.

b. Multiply the share exchange ratio by the number of Acquirer shares outstanding.

c. Add the number of Acquirer and Target shares outstanding

d. Multiply the share exchange ratio by the number of Target shares outstanding.

e. Divide the share exchange ratio by the purchase price premium

Answer:

Restaurant chain, Camin Holdings, acquired all of the assets and liabilities of

Cheesecakes R Us. The

combined firm is known as Camin Holdings and Cheesecakes R Us no longer exists as

a separate entity. The

acquisition is best described as a:

a. Merger

b. Consolidation

c. Tender offer

d. Spinoff

e. Divestiture

Answer:

Which is true of the following? A white knight

a. Is a group of dissident shareholders which side with the bidding firm

b. Is a group of the target firm’s current shareholders which side with management

c. Is a third party that is willing to acquire the target firm at the same price as the bidder

but usually removes the target’s management

d. Is a firm which is viewed by management as a more appropriate suitor than the

bidder

e. Is a firm that is willing to acquire only a large block of stock in the target firm

Answer:

Which of the following are not true of net operating loss carrybacks and carryforwards?

a. Net operating loss carrybacks enable firms to recover previous taxes paid.

b. Net operating loss carryforwards enable firms to shelter future taxable income.

c. Net operating loss carryforwards may be applied to income up to 5 years into the

future..

d. Loss corporations” cannot use a net operating loss carry forward unless they remain

viable and in essentially the same business for at least 2 years following the closing of

the acquisition.

e. None of the above

Answer:

In a tender offer, which of the following is true?

a. Both acquiring and target firms are required to disclose their intentions to the SEC

b. The target’s management cannot advise its shareholders how to respond to a tender

offer until has disclosed certain information to the SEC

c. Information must be disclosed only to the SEC and not to the exchanges on which the

target’s shares are traded

d. A and B

e. A, B, and C

Answer:

SABMiller in Joint Venture with Molson Coors

On October 10, 2007, SABMiller (SAB) and Molson Coors (Coors) agreed to combine

their U.S. brewing operations into a joint venture corporation. The stated objective was

to create a rival capable of competing with Anheuser-Busch, the maker of Budweiser

beer. SAB and Coors, the second and third largest breweries, respectively, in the United

States in terms of market share, have equal voting rights in the newly formed entity.

Each firm has five representatives on the board. In terms of ownership, SAB, the larger

of the two in terms of sales and profits, has a 58-percent stake and Coors a 42-percent

position. The combined operation, named MillerCoors, has about a 30 percent market

share versus Anheuser’s 48 percent. Leo Kiely, chief executive at Coors, became the

chief executive officer of MillerCoors and Tom Long, head of the SAB business in the

United States, became the president and chief commercial officer. Peter Coors, vice

chairman of Coors, was tapped as the chairman and Graham Mackey, SAB’s chief

executive officer, the vice chairman of MillerCoors. Both Coors and SAB continue to

operate separate global businesses.

From its roots in South Africa, the former SAB PLC grew rapidly over the previous

decade by expanding into fast growing economies such as China, Eastern Europe, and

Latin America. SAB acquired Miller Brewing Company in 2002, but the U.S. business

failed to gain significant market share in competing with Anheuser-Busch’s pervasive

brand awareness and distribution strength. Molson Coors was formed by the 2005

merger of Colorado’s Adolph Coors Co. and Canada’s Molson Inc., both

family-controlled companies. The families were unwilling to sell their entire companies

to another firm. The JV allows them to keep some control. Molson Coors, with dual

headquarters in Montreal and Denver, has major operations in Canada and Britain that

would remain independent of SABMiller. Reflecting its larger market share, brand

recognition, and negotiating clout with distributors, Anheuser-Busch has operating

profit margins of 23 percent, double SAB’s or Coors’s margins. SAB is larger in terms

of both revenue and profit than Coors.

The major U.S. breweries have been experiencing growing competition from wine,

specialty beers, spirits, and imported beers. Spirits companies have raised the pressure

on beer giants to merge by rolling out sweet cocktails and other drinks to lure younger

consumers. Premixed bottled drinks such as Smirnoff Ice have seen sales triple in the

last decade. The U.S. beer market is largely mature, with consumption growing at an

annual rate of about 1.5 percent.

MillerCoors anticipated annual cost savings to reach $500 million by the third year of

operation and be accretive for both parent firms by the second full year of combined

operations. The cost savings result from streamlining production, reducing shipping

distances between plants and distribution sites, and cutting corporate staff. Shipping

costs represent a significant cost, given the nature of the product. By producing both

firms’ products in the eight plants geographically distributed across the Midwestern and

western United States, MillerCoors should realize significant savings in meeting

customer demand for both products in the immediate proximity of each plant.

SAB and Coors hope to become one-stop shops for distributors, allowing them to save

time and money by dealing with one company instead of two. About 60 percent of

Miller’s volume is distributed by wholesalers also selling Molson Coors brands. U.S.

federal law dating back to the repeal of prohibition requires beer to be sold in many

states through wholesalers. The resulting savings to distributors could increase

MillerCoors overall market share.

By combining their U.S. advertising budgets, MillerCoors expects to have more clout at

the bargaining table with U.S. media outlets, enabling the combined firm to get lower

prices and better sports marketing deals. Such deals are viewed as critical to marketing

beer in the United States. MillerCoors will find it easier to negotiate for better

placement for its ads and compete more effectively for ad rights to major sporting

events. The two firms are also geographically complementary. Miller is strong in the

Midwest, while Coors has large market share in the West.

Immediately following the joint venture announcement, Anheuser-Busch’s CEO August

A. Busch IV said in a message to employees that the brewer must capitalize on the

significant transition confusion he predicted would occur when Miller and Molson

Coors blend their U.S. operations. Such confusion, he predicted, would create great

concern within the SABMiller/Coors field sales and wholesale organizations, as people

attempt to determine if they will have a role in this new structure.

Discussion Questions:

1) What tactics do you think Anheuser might employ to exploit the predicted confusion

during the integration of the SABMiller and Coors operations?

2) How did the combination of the U.S. operations of SABMiller and MolsonCoors

meet the needs of the two parties? Why was a JV viewed as preferable to a merger of

the two firm’s global operations?

3) How do you believe the ownership distribution for MillersCoors was determined?

4) Why do you believe that SAB and Coors agreed to equal board representation and

voting rights in the new JV? What types of governance issues might arise in view of the

governance structure of MillersCoors? What mechanisms might have been put in place

by the partners prior to closing to resolve possible governance issues? Be specific.

Answer:

Post-closing integration may be viewed in terms of a process consisting of the

following activities

a. Integration planning

b. Developing communication plans

c. Creating a new organization

d. Developing staffing plans

e. All of the above

Answer:

The management team of a privately held firm found a lender who would lend them 90

percent of the purchase price of the firm if they pledged the firm’s assets as well as their

personal assets as collateral for the loan. This purchase would best be described by

which of the following terms?

a. Merger

b. Leveraged buyout

c. Joint venture

d. Tender offer

e. Consolidation

Answer:

Teva Pharmaceuticals Buys Ivax Corporation

Teva Pharmaceutical Industries’, a manufacturer and distributor of generic drugs,

takeover of Ivax Corp for $7.4 billion created the world’s largest manufacturer of

generic drugs. For Teva, based in Israel, and Ivax, headquartered in Miami, the merger

eliminated a large competitor and created a distribution chain that spans 50 countries.

To broaden the appeal of the proposed merger, Teva offered Ivax shareholders the

option to receive for each of their shares either 0.8471 of American depository receipts

(ADRs) representing Teva shares or $26 in cash. ADRs represent the receipt given to

U.S. investors for the shares of a foreign-based corporation held in the vault of a U.S.

bank. Ivax shareholders wanting immediate liquidity chose to exchange their shares for

cash, while those wanting to participate in future appreciation of Teva stock exchanged

their shares for Teva shares.

At closing, each outstanding share of Ivax common stock was cancelled. Each

cancelled share represented the right to receive either of these two previously

mentioned payment options. The merger agreement also provided for the acquisition of

Ivax by Teva through a merger of Merger Sub, a newly formed and wholly-owned

subsidiary of Teva, into Ivax. As the surviving corporation, Ivax would be a

wholly-owned subsidiary of Teva. The merger involving the exchange of Teva ADRs

for Ivax shares was considered as tax-free for those Ivax shareholders receiving Teva

stock under U.S. law as it consisted of predominately acquirer shares.

Case Study. JDS UniphaseSDL Merger Results in Huge Write-Off

What started out as the biggest technology merger in history up to that point saw its

value plummet in line with the declining stock market, a weakening economy, and

concerns about the cash-flow impact of actions the acquirer would have to take to gain

regulatory approval. The $41 billion mega-merger, proposed on July 10, 2000,

consisted of JDS Uniphase (JDSU) offering 3.8 shares of its stock for each share of

SDL’s outstanding stock. This constituted an approximate 43% premium over the price

of SDL’s stock on the announcement date. The challenge facing JDSU was to get

Department of Justice (DoJ) approval of a merger that some feared would result in a

supplier (i.e., JDS UniphaseSDL) that could exercise enormous pricing power over the

entire range of products from raw components to packaged products purchased by

equipment manufacturers. The resulting regulatory review lengthened the period

between the signing of the merger agreement between the two companies and the actual

closing to more than 7 months. The risk to SDL shareholders of the lengthening of the

time between the determination of value and the actual receipt of the JDSU shares at

closing was that the JDSU shares could decline in price during this period.

Given the size of the premium, JDSU’s management was unwilling to protect SDL’s

shareholders from this possibility by providing a “collar” within which the exchange

ratio could fluctuate. The absence of a collar proved particularly devastating to SDL

shareholders, which continued to hold JDSU stock well beyond the closing date. The

deal that had been originally valued at $41 billion when first announced more than 7

months earlier had fallen to $13.5 billion on the day of closing.

JDSU manufactures and distributes fiber-optic components and modules to

telecommunication and cable systems providers worldwide. The company is the

dominant supplier in its market for fiber-optic components. In 1999, the firm focused

on making only certain subsystems needed in fiber-optic networks, but a flurry of

acquisitions has enabled the company to offer complementary products. JDSU’s

strategy is to package entire systems into a single integrated unit. This would reduce the

number of vendors that fiber optic network firms must deal with when purchasing

systems that produce the light that is transmitted over fiber. SDL’s products, including

pump lasers, support the transmission of data, voice, video, and internet information

over fiber-optic networks by expanding their fiber-optic communications networks

much more quickly and efficiently than would be possible using conventional electronic

and optical technologies. SDL had approximately 1700 employees and reported sales of

$72 million for the quarter ending March 31, 2000.

As of July 10, 2000, JDSU had a market value of $74 billion with 958 million shares

outstanding. Annual 2000 revenues amounted to $1.43 billion. The firm had $800

million in cash and virtually no long-term debt. Including one-time merger-related

charges, the firm recorded a loss of $905 million. With its price-to-earnings (excluding

merger-related charges) ratio at a meteoric 440, the firm sought to use stock to acquire

SDL, a strategy that it had used successfully in eleven previous acquisitions. JDSU

believed that a merger with SDL would provide two major benefits. First, it would add

a line of lasers to the JDSU product offering that strengthened signals beamed across

fiber-optic networks. Second, it would bolster JDSU’s capacity to package multiple

components into a single product line.

Regulators expressed concern that the combined entities could control the market for a

specific type of pump laser used in a wide range of optical equipment. SDL is one of

the largest suppliers of this type of laser, and JDS is one of the largest suppliers of the

chips used to build them. Other manufacturers of pump lasers, such as Nortel Networks,

Lucent Technologies, and Corning, complained to regulators that they would have to

buy some of the chips necessary to manufacture pump lasers from a supplier (i.e.,

JDSU), which in combination with SDL, also would be a competitor.

As required by the HartScottRodino (HSR) Antitrust Improvements Act of 1976, JDSU

had filed with the DoJ seeking regulatory approval. On August 24 th, the firm received

a request for additional information from the DoJ, which extended the HSR waiting

period. On February 6, JDSU agreed as part of a consent decree to sell a Swiss

subsidiary, which manufactures pump laser chips, to Nortel Networks Corporation, a

JDSU customer, to satisfy DoJ concerns about the proposed merger. The divestiture of

this operation set up an alternative supplier of such chips, thereby alleviating concerns

expressed by other manufacturers of pump lasers that they would have to buy such

components from a competitor.

On July 9, 2000, the boards of both JDSU and SDL unanimously approved an

agreement to merge SDL with a newly formed, wholly owned subsidiary of JDS

Uniphase, K2 Acquisition, Inc. K2 Acquisition, Inc. was created by JDSU as the

acquisition vehicle to complete the merger. In a reverse triangular merger, K2

Acquisition Inc. was merged into SDL, with SDL as the surviving entity. The

post-closing organization consisted of SDL as a wholly owned subsidiary of JDS

Uniphase. The form of payment consisted of exchanging JDSU common stock for SDL

common shares. The share exchange ratio was 3.8 shares of JDSU stock for each SDL

common share outstanding. Instead of a fraction of a share, each SDL stockholder

received cash, without interest, equal to dollar value of the fractional share at the

average of the closing prices for a share of JDSU common stock for the 5 trading days

before the completion of the merger.

Under the rules of the NASDAQ National Market, on which JDSU’s shares are traded,

JDSU is required to seek stockholder approval for any issuance of common stock to

acquire another firm. This requirement is triggered if the amount issued exceeds 20% of

its issued and outstanding shares of common stock and of its voting power. In

connection with the merger, both SDL and JDSU received fairness opinions from

advisors employed by the firms.

The merger agreement specified that the merger could be consummated when all of the

conditions stipulated in the agreement were either satisfied or waived by the parties to

the agreement. Both JDSU and SDL were subject to certain closing conditions. Such

conditions were specified in the September 7, 2000 S4 filing with the SEC by JDSU,

which is required whenever a firm intends to issue securities to the public. The

consummation of the merger was to be subject to approval by the shareholders of both

companies, the approval of the regulatory authorities as specified under the HSR, and

any other foreign antitrust law that applied. For both parties, representations and

warranties (statements believed to be factual) must have been found to be accurate and

both parties must have complied with all of the agreements and covenants (promises) in

all material ways.

The following are just a few examples of the 18 closing conditions found in the merger

agreement. The merger is structured so that JDSU and SDL’s shareholders will not

recognize a gain or loss for U.S. federal income tax purposes in the merger, except for

taxes payable because of cash received by SDL shareholders for fractional shares. Both

JDSU and SDL must receive opinions of tax counsel that the merger will qualify as a

tax-free reorganization (tax structure). This also is stipulated as a closing condition. If

the merger agreement is terminated as a result of an acquisition of SDL by another firm

within 12 months of the termination, SDL may be required to pay JDSU a termination

fee of $1 billion. Such a fee is intended to cover JDSU’s expenses incurred as a result of

the transaction and to discourage any third parties from making a bid for the target firm.

Despite dramatic cost-cutting efforts, the company reported a loss of $7.9 billion for the

quarter ending June 31, 2001 and $50.6 billion for the 12 months ending June 31, 2001.

This compares to the projected pro forma loss reported in the September 9, 2000 S4

filing of $12.1 billion. The actual loss was the largest annual loss ever reported by a

U.S. firm up to that time. The fiscal year 2000 loss included a reduction in the value of

goodwill carried on the balance sheet of $38.7 billion to reflect the declining market

value of net assets acquired during a series of previous transactions. Most of this

reduction was related to goodwill arising from the merger of JDS FITEL and Uniphase

and the subsequent acquisitions of SDL, E-TEK, and OCLI..

The stock continued to tumble in line with the declining fortunes of the

telecommunications industry such that it was trading as low as $7.5 per share by

mid-2001, about 6% of its value the day the merger with SDL was announced. Thus, the

JDS UniphaseSDL merger was marked by two firststhe largest purchase price paid for a

pure technology company and the largest write-off (at that time) in history. Both of

these infamous “firsts” occurred within 12 months.

Case Study Discussion Questions

1) What is goodwill? How is it estimated? Why did JDS Uniphase write down the value

of its goodwill in 2001? Why does this reflect a series of poor management decisions

with respect to mergers completed between 1999 and early 2001?

2) How might the use of stock, as an acquisition “currency,” have contributed to the

sustained decline in JDS Uniphase’s stock through mid-2001? In your judgment what is

the likely impact of the glut of JDS Uniphase shares in the market on the future

appreciation of the firm’s share price? Explain your answer.

3) What are the primary differences between a forward and a reverse triangular merger?

Why might JDS Uniphase have chosen to merge its K2 Acquisition Inc. subsidiary with

SDL in a reverse triangular merger? Explain your answer.

4) Discuss various methodologies you might use to value assets acquired from SDL

such as existing technologies, “core” technologies, trademarks and trade names,

assembled workforce, and deferred compensation?

5) Why do boards of directors of both acquiring and target companies often obtain

so-called “fairness opinions” from outside investment advisors or accounting firms?

What valuation methodologies might be employed in constructing these opinions?

Should stockholders have confidence in such opinions? Why/why not?

Answer:

Which of the following is not true about the primary responsibilities of the management

integration team (MIT)?

a. The MIT should direct the daily operations of the individual work teams set up to

implement certain activities.

b. Focus the organization on meeting ongoing business commitments and operational

performance targets

c. The creation of an early warning system to determine when performance targets are

likely to be missed.

d. Establish a rigorous communication program

e. Establishing a master schedule of what should be done by whom and by what date.

Answer:

Limitations in applying the comparable companies’ method of valuation include which

of the following?

a. Finding truly comparable companies is difficult

b. The use of market-based methods can result in significant under- or overvaluation

during periods of declining or rising stock markets

c. Market-based methods can be manipulated easily, because the methods do not require

a clear statement of assumptions with respect to risk, growth, or the timing or

magnitude of future earnings and cash flows.

a. A, B, & C

b. A & B only

Answer:

In selecting an appropriate business strategy, all of the following are relevant questions

except for

a. Does the firm have sufficient resources to implement the strategy?

b. Have all reasonable alternatives available for implementing the strategy been

evaluated?

c. What are the key assumptions underlying the various strategic options under

consideration?

d. What do the firm’s targeted customers primarily consider in making purchasing

decisions?

e. Why might an acquisition be preferred to a joint venture in implementing the

business strategy?

Answer:

Which of the following is among the least regulated industries in the U.S.?

a. Defenses

b. Communications

c. Retailing

d. Public utilities

e. Banking

Answer:

Which of the following is generally not a motive for firms to expand internationally?

a. Desire to achieve geographic diversification

b. Desire to accelerate growth

c. Desire to consolidate industries

d. Desire to avoid entry barriers

e. Desire to enter countries with less favorable tax rates

Answer:

Which of the following are commonly used sources of funding for leveraged buyouts?

a. Secured debt

b. Unsecured debt

c. Preferred stock

d. Seller financing

e. All of the above

Answer:

Which of the following is true of collar arrangements?

a. A fixed or constant share exchange ratiois one in which the number of acquirer shares

exchanged for each target share is unchanged between the signing of the agreement of

purchase and sale and closing.

b. Collar agreements provide for certain changes in the exchange ratio contingent on the

level of the acquirer’s share price around the effective date of the merger.

c. A fixed exchange collar agreement may involve a fixed exchange ratio as long as the

acquirer’s share price remains within a narrow range, calculated as of the effective date

of merger.

d. A fixed payment collar agreement guarantees that the target firm shareholder receives

a certain dollar value in terms of acquirer stock as long as the acquirer’s stock remains

within a narrow range, and a fixed exchange ratio if the acquirer’s average stock price is

outside the bounds around the effective date of the merger.

e. All of the above.

Answer:

In valuing private businesses, the U.S. tax courts have historically supported the use of

which valuation method for purposes of estate valuation?

a. Discounted cash flow

b. Comparable company method

c. Tangible book value method

d. A combination of a and c

e. All of the above

Answer:

Which of the following are true of real options?

a. Real options give management the ability to delay the implementation of a strategy

b. Real options give management the ability to accelerate the implementation of a

strategy

c. Real options give management the ability to abandon a strategy

d. Real options represent the ability of management to change their strategy after the

strategy has beenmimplemented.

e. All of the above

Answer:

Methods of dividing ownership and control in business alliances may take which of the

following forms.

a. Majority-minority framework

b. Equal division of power framework

c. “Majority rules” framework

d. Multiple party framework

e. All of the above

Answer:

The control market is applicable when which of the following conditions are true?

a. Capital markets are illiquid

b. Equity ownership is heavily concentrated

c. Board members are largely insiders

d. Ownership and control overlap

e. All of the above

`

Answer:

Which of the following is not a motivation for establishing an alliance?

a. Risk sharing

b. Gaining access to new markets

c. Gaining access to a new technology

d. Achieving maximum control

e. Entering into a foreign market

Answer:

A business owner may overstate revenue and understate actual expenses when

a. The business is about to be sold

b. They are being audited by the IRS

c. They are trying to minimize tax liabilities

d. All of the above

e. None of the above

Answer:

Arbitrageurs often adopt which of the following strategies in a share for share exchange

just before or just after

a merger announcement?

a. Buy the target firm’s stock

b. Buy the target firm’s stock and sell the acquirer’s stock short

c. Buy the acquirer’s stock only

d. Sell the target’s stock short and buy the acquirer’s stock

e. Sell the target stock short

Answer:

A firm may be motivated to purchase another firm whenever

a. The cost to replace the target firm’s assets is less than its market value

b. The replacement cost of the target firm’s assets exceeds its market value

c. When the inflation rate is accelerating

d. The ratio of the target firm’s market value is more than twice its book value

e. The market to book ratio is greater than one and increasing

Answer:

Successfully integrated M&As are those that demonstrate leadership by candidly and

continuously communicating which of the following?

a. A clear vision

b. A set of values

c. Unambiguous priorities for each employee

d. A & B only

e. A, B, & C

Answer:

Which of the following factors contribute to the integration of the global capital

markets?

a. The reduction in trade barriers

b. The removal of capital controls

c. The harmonization of tax laws

d. Floating exchange rates

e. All of the above

Answer:

Buyer Consortium Wins Control of ABN Amro

The biggest banking deal on record was announced on October 9, 2007, resulting in the

dismemberment of one of Europe’s largest and oldest financial services firms, ABN

Amro (ABN). A buyer consortium consisting of The Royal Bank of Scotland (RBS),

Spain’s Banco Santander (Santander), and Belgium’s Fortis Bank (Fortis) won control

of ABN, the largest bank in the Netherlands, in a buyout valued at $101 billion.

European banks had been under pressure to grow through acquisitions and compete

with larger American rivals to avoid becoming takeover targets themselves. ABN had

been viewed for years as a target because of its relatively low share price. However,

rival banks were deterred by its diverse mixture of businesses, which was unattractive

to any single buyer. Under pressure from shareholders, ABN announced that it had

agreed, on April 23, 2007, to be acquired by Barclay’s Bank of London for $85 billion

in stock. The RBS-led group countered with a $99 billion bid consisting mostly of cash.

In response, Barclay’s upped its bid by 6 percent with the help of state-backed investors

from China and Singapore. ABN’s management favored the Barclay bid because

Barclay had pledged to keep ABN intact and its headquarters in the Netherlands.

However, a declining stock market soon made Barclay’s mostly stock offer unattractive.

While the size of the transaction was noteworthy, the deal is especially remarkable in

that the consortium had agreed prior to the purchase to split up ABN among the three

participants. The mechanism used for acquiring the bank represented an unusual means

of completing big transactions amidst the subprime-mortgage-induced turmoil in the

global credit markets at the time. The members of the consortium were able to select the

ABN assets they found most attractive. The consortium agreed in advance of the

acquisition that Santander would receive ABN’s Brazilian and Italian units; Fortis

would obtain the Dutch bank’s consumer lending business, asset management, and

private banking operations, and RBS would own the Asian and investment banking

units. Merrill Lynch served as the sole investment advisor for the group’s participants.

Caught up in the global capital market meltdown, Fortis was forced to sell the ABN

Amro assets it had acquired to its Dutch competitor ING in October 2008.

Discussion Questions:

1) In your judgment, what are likely to be some of the major challenges in assembling a

buyer consortium to acquire and subsequently dismember a target firm such as ABN

Amro? In what way do you thing the use of a single investment advisor might have

addressed some of these issues?

2) The ABN Amro transaction was completed at a time when the availability of credit

was limited due to the sub-prime mortgage loan problem originating in the United

States. How might the use of a group rather than a single buyer have facilitated the

purchase of ABN Amro?

3) The same outcome could have been achieved if a single buyer had reached

agreement with other banks to acquire selected pieces of ABN before completing the

transaction. The pieces could then have been sold at the closing. Why might the use of

the consortium been a superior alternative?

Answer:

Consolidation in the Wireless Communications Industry:

Vodafone Acquires AirTouch

.

Deregulation of the telecommunications industry has resulted in increased

consolidation. In Europe, rising competition is the catalyst driving mergers. In the

United States, the break up of AT&T in the mid-1980s and the subsequent deregulation

of the industry has led to key alliances, JVs, and mergers, which have created cellular

powerhouses capable of providing nationwide coverage. Such coverage is being

achieved by roaming agreements between carriers and acquisitions by other carriers.

Although competition has been heightened as a result of deregulation, the

telecommunications industry continues to be characterized by substantial barriers to

entry. These include the requirement to obtain licenses and the need for an extensive

network infrastructure. Wireless communications continue to grow largely at the

expense of traditional landline services as cellular service pricing continues to decrease.

Although the market is likely to continue to grow rapidly, success is expected to go to

those with the financial muscle to satisfy increasingly sophisticated customer demands.

What follows is a brief discussion of the motivations for the merger between Vodafone

and AirTouch Communications. This discussion includes a description of the key

elements of the deal structure that made the Vodafone offer more attractive than a

competing offer from Bell Atlantic.

Vodafone

Company History

Vodafone is a wireless communications company based in the United Kingdom. The

company is located in 13 countries in Europe, Africa, and Australia/New Zealand.

Vodafone reaches more than 9.5 million subscribers. It has been the market leader in the

United Kingdom since 1986 and as of 1998 had more than 5 million subscribers in the

United Kingdom alone. The company has been very successful at marketing and selling

prepaid services in Europe. Vodafone also is involved in a venture called Globalstar, LP,

a limited partnership with Loral Space and Communications and Qualcomm, a phone

manufacturer. “Globalstar will construct and operate a worldwide, satellite-based

communications system offering global mobile voice, fax, and data communications in

over 115 countries, covering over 85% of the world’s population”.

Strategic Intent

Vodafone’s focus is on global expansion. They are expanding through partnerships and

by purchasing licenses. Notably, Vodafone lacked a significant presence in the United

States, the largest mobile phone market in the world. For Vodafone to be considered a

truly global company, the firm needed a presence in the Unites States. Vodafone’s

strategy is focused on maintaining high growth levels in its markets and increasing

profitability; maintaining their current customer base; accelerating innovation; and

increasing their global presence through acquisitions, partnerships, or purchases of new

licenses. Vodafone’s current strategy calls for it to merge with a company with

substantial market share in the United States and Asia, which would fill several holes in

Vodafone’s current geographic coverage.

Company Structure

The company is very decentralized. The responsibilities of the corporate headquarters in

the United Kingdom lie in developing corporate strategic direction, compiling financial

information, reporting and developing relationships with the various stock markets, and

evaluating new expansion opportunities. The management of operations is left to the

countries’ management, assuming business plans and financial measures are being met.

They have a relatively flat management structure. All of their employees are

shareowners in the company. They have very low levels of employee turnover, and the

workforce averages 33 years of age.

AirTouch

Company History

AirTouch Communications launched it first cellular service network in 1984 in Los

Angeles during the opening ceremonies at the 1984 Olympics. The original company

was run under the name PacTel Cellular, a subsidiary of Pacific Telesis. In 1994, PacTel

Cellular spun off from Pacific Telesis and became AirTouch Communications, under the

direction of Chair and Chief Executive Officer Sam Ginn. Ginn believed that the most

exciting growth potential in telecommunications is in the wireless and not the landline

services segment of the industry. In 1998, AirTouch operated in 13 countries on three

continents, serving more than 12 million customers, as a worldwide carrier of cellular

services, personal communication services (PCS), and paging services. AirTouch has

chosen to compete on a global front through various partnerships and JVs. Recognizing

the massive growth potential outside the United States, AirTouch began their global

strategy immediately after the spin-off.

Strategic Intent

AirTouch has chosen to differentiate itself in its domestic regions based on the concept

of “Superior Service Delivery.” The company’s focus is on being available to its

customers 24 hours a day, 7 days a week and on delivering pricing options that meet the

customer’s needs. AirTouch allows customers to change pricing plans without penalty.

The company also emphasizes call clarity and quality and extensive geographic

coverage. The key challenges AirTouch faces on a global front is in reducing churn (i.e.,

the percentage of customers leaving), implementing improved digital technology,

managing pressure on service pricing, and maintaining profit margins by focusing on

cost reduction. Other challenges include creating a domestic national presence.

Company Structure

AirTouch is decentralized. Regions have been developed in the U.S. market and are run

autonomously with respect to pricing decisions, marketing campaigns, and customer

care operations. Each region is run as a profit center. Its European operations also are

run independently from each other to be able to respond to the competitive issues

unique to the specific countries. All employees are shareowners in the company, and the

average age of the workforce is in the low to mid-30s. Both companies are comparable

in terms of size and exhibit operating profit margins in the mid-to-high teens. AirTouch

has substantially less leverage than Vodafone.

Merger Highlights

Vodafone began exploratory talks with AirTouch as early as 1996 on a variety of

options ranging from partnerships to a merger. Merger talks continued informally until

late 1998 when they were formally broken off. Bell Atlantic, interested in expanding its

own mobile phone business’s geographic coverage, immediately jumped into the void

by proposing to AirTouch that together they form a new wireless company. In early

1999, Vodafone once again entered the fray, sparking a sharp takeover battle for

AirTouch. Vodafone emerged victorious by mid-1999.

Motivation for the Merger

Shared Vision

The merger would create a more competitive, global wireless telecommunications

company than either company could achieve separately. Moreover, both firms shared

the same vision of the telecommunications industry. Mobile telecommunications is

believed to be the among the fastest-growing segment of the telecommunications

industry, and over time mobile voice will replace large amounts of telecommunications

traffic carried by fixed-line networks and will serve as a major platform for voice and

data communication. Both companies believe that mobile penetration will reach 50% in

developed countries by 2003 and 55% and 65% in the United States and developed

European countries, respectively, by 2005.

Complementary Assets

Scale, operating strength, and complementary assets were given as compelling reasons

for the merger. The combination of AirTouch and Vodafone would create the largest

mobile telecommunication company at the time, with significant presence in the United

Kingdom, United States, continental Europe, and Asian Pacific region. The scale and

scope of the operations is expected to make the combined firms the vendor of choice for

business travelers and international corporations. Interests in operations in many

countries will make Vodafone AirTouch more attractive as a partner for other

international fixed and mobile telecommunications providers. The combined scale of

the companies also is expected to enhance its ability to develop existing networks and

to be in the forefront of providing technologically advanced products and services.

Synergy

Anticipated synergies include after-tax cost savings of $340 million annually by the

fiscal year ending March 31, 2002. The estimated net present value of these synergies is

$3.6 billion discounted at 9%. The cost savings arise from global purchasing and

operating efficiencies, including volume discounts, lower leased line costs, more

efficient voice and data networks, savings in development and purchase of

third-generation mobile handsets, infrastructure, and software. Revenues should be

enhanced through the provision of more international coverage and through the

bundling of services for corporate customers that operate as multinational businesses

and business travelers.

AirTouch’s Board Analyzes Options

Morgan Stanley, AirTouch’s investment banker, provided analyses of the current prices

of the Vodafone and Bell Atlantic stocks, their historical trading ranges, and the

anticipated trading prices of both companies’ stock on completion of the merger and on

redistribution of the stock to the general public. Both offers were structured so as to

constitute essentially tax-free reorganizations. The Vodafone proposal would qualify as

a Type A reorganization under the Internal Revenue Service Code; hence, it would be

tax-free, except for the cash portion of the offer, for U.S. holders of AirTouch common

and holders of preferred who converted their shares before the merger. The Bell Atlantic

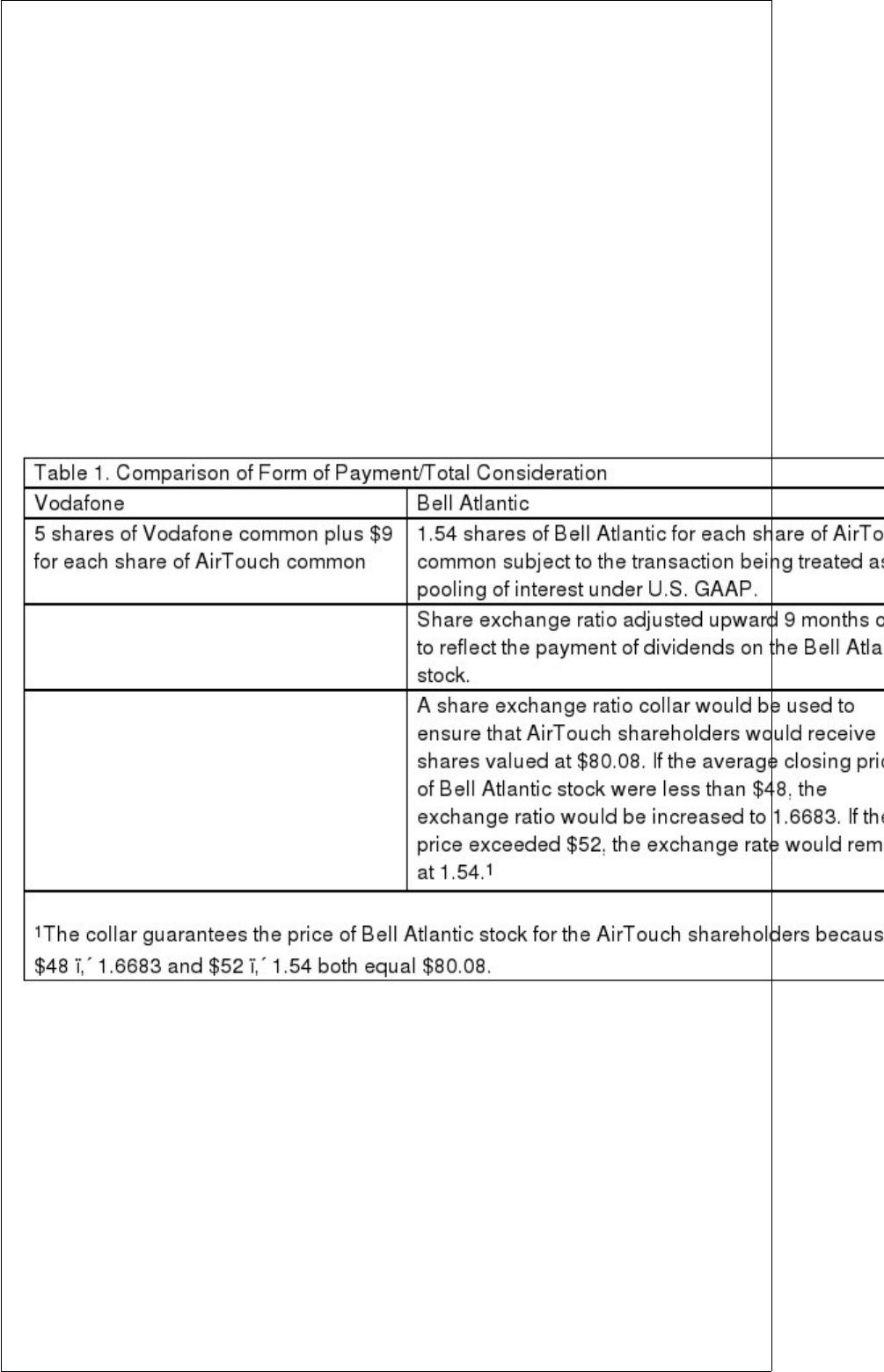

offer would qualify as a Type B tax-free reorganization. Table 1 highlights the primary

characteristics of the form of payment (total consideration) of the two competing offers.

Morgan Stanley’s primary conclusions were as follows:

1)Bell Atlantic had a current market value of $83 per share of AirTouch stock based on

the $53.81 closing price of Bell Atlantic common stock on January 14, 1999. The collar

would maintain the price at $80.08 per share if the price of Bell Atlantic stock during a

specified period before closing were between $48 and $52 per share.

2) The Vodafone proposal had a current market value of $97 per share of AirTouch

stock based on Vodafone’s ordinary shares (i.e., common) on January 17, 1999.

3) Following the merger, the market value of the Vodafone American Depository Shares

(ADSs) to be received by AirTouch shareholders under the Vodafone proposal could

decrease.

4) Following the merger, the market value of Bell Atlantic’s stock also could decrease,

particularly in light of the expectation that the proposed transaction would dilute Bell

Atlantic’s EPS by more than 10% through 2002.

In addition to Vodafone’s higher value, the board tended to favor the Vodafone offer

because it involved less regulatory uncertainty. As U.S. corporations, a merger between

AirTouch and Bell Atlantic was likely to receive substantial scrutiny from the U.S.

Justice Department, the Federal Trade Commission, and the FCC. Moreover, although

both proposals could be completed tax-free, except for the small cash component of the

Vodafone offer, the Vodafone offer was not subject to achieving any specific accounting

treatment such as pooling of interests under U.S. generally accepted accounting

principles (GAAP).

Recognizing their fiduciary responsibility to review all legitimate offers in a balanced

manner, the AirTouch board also considered a number of factors that made the

Vodafone proposal less attractive. The failure to do so would no doubt trigger

shareholder lawsuits. The major factors that detracted from the Vodafone proposal were

that it would not result in a national presence in the United States, the higher volatility

of its stock, and the additional debt Vodafone would have to assume to pay the cash

portion of the purchase price. Despite these concerns, the higher offer price from

Vodafone (i.e., $97 to $83) won the day.

Acquisition Vehicle and Post Closing Organization

In the merger, AirTouch became a wholly owned subsidiary of Vodafone. Vodafone

issued common shares valued at $52.4 billion based on the closing Vodafone ADS on

April 20, 1999. In addition, Vodafone paid AirTouch shareholders $5.5 billion in cash.

On completion of the merger, Vodafone changed its name to Vodafone AirTouch Public

Limited Company. Vodafone created a wholly owned subsidiary, Appollo Merger

Incorporated, as the acquisition vehicle. Using a reverse triangular merger, Appollo

was merged into AirTouch. AirTouch constituted the surviving legal entity. AirTouch

shareholders received Vodafone voting stock and cash for their AirTouch shares. Both

the AirTouch and Appollo shares were canceled. After the merger, AirTouch

shareholders owned slightly less than 50% of the equity of the new company, Vodafone

AirTouch. By using the reverse merger to convey ownership of the AirTouch shares,

Vodafone was able to ensure that all FCC licenses and AirTouch franchise rights were

conveyed legally to Vodafone. However, Vodafone was unable to avoid seeking

shareholder approval using this method. Vodafone ADS’s traded on the New York Stock

Exchange (NYSE). Because the amount of new shares being issued exceeded 20% of

Vodafone’s outstanding voting stock, the NYSE required that Vodafone solicit its

shareholders for approval of the proposed merger.

Following this transaction, the highly aggressive Vodafone went on to consummate the

largest merger in history in 2000 by combining with Germany’s telecommunications

powerhouse, Mannesmann, for $180 billion. Including assumed debt, the total purchase

price paid by Vodafone AirTouch for Mannesmann soared to $198 billion. Vodafone

AirTouch was well on its way to establishing itself as a global cellular phone

powerhouse.

Discussion Questions:

1) Did the AirTouch board make the right decision? Why or why not?

2) How valid are the reasons for the proposed merger?

3) What are the potential risk factors related to the merger?

4) Is this merger likely to be tax free, partially tax free, or taxable? Explain your

answer.

5) What are some of the challenges the two companies are likely to face while

integrating the businesses?

Answer:

Arcelor Outbids ThyssenKrupp for Canada’s Dofasco Steelmaking Operations

Arcelor Steel of Luxembourg, the world’s second largest steel maker, was eager to make

an acquisition. Having been outbid by Mittal, the world’s leading steel firm, in its

efforts to buy Turkey’s state-owned Erdemir and Ukraine’s Kryvorizhstal, Guy Dolle,

Arcelor’s CEO, seemed determined not to let that happen again. Arcelor and Dofasco

had been in talks for more than four months before Arcelor decided to initiate a tender

offer on November 23, 2005, valued at $3.8 billion in cash. Dofasco, Canada’s largest

steel manufacturer, owned vast coal and iron ore reserves, possessed a nonunion

workforce, and sold much of its steel to Honda assembly plants in the United States.

The merger would enable Arcelor, whose revenues were concentrated primarily in

Europe, to diversify into the United States. Contrary to their European operations,

Arcelor found the flexibility offered by Dofasco’s nonunion labor force highly

attractive. Moreover, by increasing its share of global steel production, Arcelor’s

management reasoned that it would be able to exert additional pricing leverage with

both customers and suppliers.

Serving the role of “white knight,” Germany’s ThyssenKrupp, the sixth largest steel

firm in the world, offered to acquire Dofasco one week later for $4.1 billion in cash.

Dofasco’s board accepted the bid, which included a $187 million breakup fee should

another firm acquire Dofasco. Investors soundly criticized Dofasco’s board for not

opening up the bidding to an auction. In its defense, the board expressed concern about

stretching out the process in an auction over several weeks. In late December, Arcelor

topped the ThyssenKrupp bid by offering $4.2 billion. Not to be outdone,

ThyssenKrupp matched the Arcelor offer on January 4, 2006. The Dofasco board

reaffirmed its preference for the ThyssenKrupp bid, due to the breakup fee and

ThyssenKrupp’s willingness (unlike Arcelor) to allow Dofasco to continue to operate

under its own name and management.

In a bold attempt to put Dofasco out of reach of the already highly leveraged

ThyssenKrupp, Arcelor raised its bid to $4.8 billion on January 16, 2006. This bid

represented an approximate 80 percent premium over Dofasco’s closing share price on

the day Arcelor announced its original tender offer. The Arcelor bid was contingent on

Dofasco withdrawing its support for the ThyssenKrupp bid. On January 24, 2006,

ThyssenKrupp said it would not raise its bid. Events in the dynamically changing global

steel market were not to end here. The Arcelor board and management barely had time

to savor their successful takeover of Dofasco before Mittal initiated a hostile takeover

of Arcelor. Ironically, Mittal succeeded in acquiring its archrival, Arcelor, just six

months later in a bid to achieve further industry consolidation.

Discussion Questions and Answers:

1) What were the motives for Arcelor’s and ThyssenKrupp’s interest in Dofasco?

2) What do you think was the logic underlying Arcelor and ThyssenKrupp’s bidding

strategies? Be specific.

3) Why do you believe that Dofasco’s share price rose above ThyssenKrupp’s offer

price per share immediately following the announcement of the bid?

4) Why do you believe that Dofasco’s board was concerned about a lengthy auction

process?

discussion of the MittalArcelor transaction.

Answer:

Cox Enterprises Offers to Take Cox Communications Private

In an effort to take the firm private, Cox Enterprises announced on August 3, 2004 a

proposal to buy the remaining 38% of Cox Communications’ shares that they did not

currently own for $32 per share. Cox Communications is the third largest provider of

cable television, telecommunications, and wireless services in the U.S, serving more

than 6.2 million customers. Historically, the firm’s cash flow has been steady and

substantial.

The deal is valued at $7.9 billion and represented a 16% premium to Cox

Communication’s share price at that time. Cox Communications would become a

subsidiary of Cox Enterprises and would continue to operate as an autonomous

business. In response to the proposal, the Cox Communications Board of Directors

formed a special committee of independent directors to consider the proposal. Citigroup

Global Markets and Lehman Brothers Inc. have committed $10 billion to the deal. Cox

Enterprises would use $7.9 billion for the tender offer, with the remaining $2.1 billion

used for refinancing existing debt and to satisfy working capital requirements.

Cable service firms have faced intensified competitive pressures from satellite service

providers DirecTV Group and EchoStar communications. Moreover, telephone

companies continue to attack cable’s high-speed Internet service by cutting prices on

high-speed Internet service over phone lines. Cable firms have responded by offering a

broader range of advanced services like video-on-demand and phone service. Since

2000, the cable industry has invested more than $80 billion to upgrade their systems to

provide such services, causing profitability to deteriorate and frustrating investors. In

response, cable company stock prices have fallen. Cox Enterprises stated that the

increasingly competitive cable industry environment makes investment in the cable

industry best done through a private company structure.

Discussion Questions::

1) Why did the board feel that it was appropriate to set up special committee of

independent board directors?

2) Why does Cox Enterprises believe that the investment needed for growing its cable

business is best done through a private company structure?

Answer:

A Real Options’ Perspective on Microsoft’s Dealings with Yahoo

In a bold move to transform two relatively weak online search businesses into a

competitor capable of challenging market leader Google, Microsoft proposed to buy

Yahoo for $44.6 billion on February 2, At $31 per share in cash and stock, the offer

represented a 62 percent premium over Yahoo’s prior day closing price. Despite

boosting its bid to $33 per share to offset a decline in the value of Microsoft’s share

price following the initial offer, Microsoft was rebuffed by Yahoo’s board and

management. In early May, Microsoft withdrew its bid to buy the entire firm and

substituted an offer to acquire the search business only. Incensed at Yahoo’s refusal to

accept the Microsoft bid, activist shareholder Carl Icahn initiated an unsuccessful proxy

fight to replace the Yahoo board. Throughout this entire melodrama, critics continued to

ask how Microsoft could justify an offer valued at $44.6 billion when the market prior

to the announcement had valued Yahoo at only $27.5 billion.

Microsoft could have continued to slug it out with Yahoo and Google, as it has been for

the last five years, but this would have given Google more time to consolidate its

leadership position. Despite having spent billions of dollars on Microsoft’s online

service (Microsoft Network or MSN) in recent years, the business remains a money

loser (with losses exceeding one half billion dollars in 2007). Furthermore, MSN

accounted for only 5 percent of the firm’s total revenue at that time.

Microsoft argued that its share of the online Internet search (i.e., ads appearing with

search results) and display (i.e., website banner ads) advertising markets would be

dramatically increased by combining Yahoo with MSN. Yahoo also is the leading

consumer email service. Anticipated cost savings from combining the two businesses

were expected to reach $1 billion annually. Longer term, Microsoft expected to bundle

search and advertising capabilities into the Windows operating system to increase the

usage of the combined firms’ online services by offering compatible new products and

enhanced search capabilities.

The two firms have very different cultures. The iconic Silicon Valleybased Yahoo often

is characterized as a company with a free-wheeling, fun-loving culture, potentially

incompatible with Microsoft’s more structured and disciplined environment. Melding or

eliminating overlapping businesses represents a potentially mind-numbing effort given

the diversity and complexity of the numerous sites available. To achieve the projected

cost savings, Microsoft would have to choose which of the businesses and technologies

would survive. Moreover, the software driving all of these sites and services is largely

incompatible.

As an independent or stand-alone business, the market valued Yahoo at approximately

$17 billion less than Microsoft’s valuation. Microsoft was valuing Yahoo based on its

intrinsic stand-alone value plus perceived synergy resulting from combining Yahoo and

MSN. Standard discounted cash flow analysis assumes implicitly that, once Microsoft

makes an investment decision, it cannot change its mind. In reality, once an investment

decision is made, management often has a number of opportunities to make future

decisions based on the outcome of things that are currently uncertain. These

opportunities, or real options, include the decision to expand (i.e., accelerate investment

at a later date), delay the initial investment, or abandon an investment. With respect to

Microsoft’s effort to acquire Yahoo, the major uncertainties dealt with the actual timing

of an acquisition and whether the two businesses could be integrated successfully. For

Microsoft’s attempted takeover of Yahoo, such options included the following:

Base case. Buy 100 percent of Yahoo immediately.

Option to expand. If Yahoo were to accept the bid, accelerate investment in new

products and services contingent on the successful integration of Yahoo and MSN.

Option to delay. (1) Temporarily walk away keeping open the possibility of returning

for 100 percent of Yahoo if circumstances change, (2) offer to buy only the search

business with the intent of purchasing the remainder of Yahoo at a later date, or (3)

enter into a search partnership, with an option to buy at a later date.

Option to abandon. If Yahoo were to accept the bid, spin off or divest combined

Yahoo/MSN if integration is unsuccessful.

The decision tree in the following exhibit illustrates the range of real options (albeit an

incomplete list) available to the Microsoft board at that time. Each branch of the tree

represents a specific option. The decision-tree framework is helpful in depicting the

significant flexibility senior management often has in changing an existing investment

decision at some point in the future.

With neither party making headway against Google, Microsoft again approached Yahoo

in mid-2009, which resulted in an announcement in early 2010 of an internet search

agreement between the two firms. Yahoo transferred control of its internet search

technology to Microsoft in an attempt to boost its sagging profits. Microsoft is relying

on a 10-year arrangement with Yahoo to help counter the dominance of Google in the

internet search market. Both firms hope to be able to attract more advertising dollars

paid by firms willing to pay for links on the firms’ sites.

Option to expand contingent on successful integration of Yahoo and MSN

Purchase Yahoo online search only. Buy remaining businesses later.

Base Case: Microsoft offers to buy all outstanding share of Yahoo

Option to postpone contingent on Yahoo’s rejection of offer

Enter long-term search partnership with option to buy.

Offer revised price for all of Yahoo if circumstances change

Spin off combined Yahoo and MSN to Microsoft shareholders

Option to abandon contingent on failure to integrate Yahoo and MSN

Divest combined Yahoo and MSN. Use proceeds to pay dividend or buy back stock.

Microsoft Real Options Decision Tree

Merrill Lynch and BlackRock Agree to Swap Assets

During the 1990s, many financial services companies began offering mutual funds to

their current customers who were pouring money into the then booming stock market.

Hoping to become financial supermarkets offering an array of financial services to their

customers, these firms offered mutual funds under their own brand name. The

proliferation of mutual funds made it more difficult to be noticed by potential customers

and required the firms to boost substantially advertising expenditures at a time when

increased competition was reducing mutual fund management fees. In addition,

potential customers were concerned that brokers would promote their own firm’s mutual

funds to boost profits.

This trend reversed in recent years, as banks, brokerage houses, and insurance

companies are exiting the mutual fund management business. Merrill Lynch agreed on

February 15, 2006, to swap its mutual funds business for an approximate 49 percent

stake in money-manager BlackRock Inc. The mutual fund or retail accounts represented

a new customer group for BlackRock, founded in 1987, which had previously managed

primarily institutional accounts.

At $453 billion in 2005, BlackRock’s assets under management had grown four times

faster than Merrill’s $544 billion mutual fund assets. During 2005, BlackRock’s net

income increased to $270 million, or 63 percent over the prior year, as compared to

Merrill’s 27 percent growth in net income in its mutual fund business to $397 million.

BlackRock and Merrill stock traded at 30 and 19 times estimated 2006 earnings,

respectively.

Merrill assets and net income represented 55 percent and 60 percent of the combined

BlackRock and Merrill assets and net income, respectively. Under the terms of the

transaction, BlackRock would issue 65 million new common shares to Merrill. Based

on BlackRock’s February 14, 2005, closing price, the deal is valued at $9.8 billion. The

common stock gave Merrill 49 percent of the outstanding BlackRock voting stock. PNC

Financial and employees and public shareholders owned 34 percent and 17 percent,

respectively. Merrill’s ability to influence board decisions is limited, since it has only 2

of 17 seats on the BlackRock board of directors. Certain ‘significant matters” require a

70 percent vote of all board members and 100 percent of the nine independent

members, which include the two Merrill representatives. Merrill (along with PNC) must

also vote its shares as recommended by the BlackRock board.

Discussion Questions:

1) Merrill owns less than half of the combined firms, although it contributed more than

one- half of the combined firms’ assets and net income. Discuss how you might use

DCF and relative valuation methods to determine Merrill’s proportionate ownership in

the combined firms.

2) Why do you believe Merrill was willing to limit its influence in the combined firms?

3) What method of accounting would Merrill use to show its investment in BlackRock?

Answer:

Mars Buys Wrigley in One Sweet Deal

Under considerable profit pressure from escalating commodity prices and eroding

market share, Wrigley Corporation, a U.S.-based leader in gum and confectionery

products, faced increasing competition from Cadbury Schweppes in the U.S. gum

market. Wrigley had been losing market share to Cadbury since 2006. Mars

Corporation, a privately owned candy company with annual global sales of $22 billion,

sensed an opportunity to achieve sales, marketing, and distribution synergies by

acquiring Wrigley Corporation.

On April 28, 2008, Mars announced that it had reached an agreement to merge with

Wrigley Corporation for $23 billion in cash. Under the terms of the agreement, which

were unanimously approved by the boards of the two firms, shareholders of Wrigley

would receive $80 in cash for each share of common stock outstanding, a 28 percent

premium to Wrigley’s closing share price of $62.45 on the announcement date. The

merged firms in 2008 would have a 14.4 percent share of the global confectionary

market, annual revenue of $27 billion, and 64,000 employees worldwide. The merger of

the two family-controlled firms represents a strategic blow to competitor Cadbury

Schweppes’s efforts to continue as the market leader in the global confectionary market

with its gum and chocolate business. Prior to the announcement, Cadbury had a 10

percent worldwide market share.

As of the September 28, 2008 closing date, Wrigley became a separate stand-alone

subsidiary of Mars, with $5.4 billion in sales. The deal is expected to help Wrigley

augment its sales, marketing, and distribution capabilities. To provide more focus to

Mars’s brands in an effort to stimulate growth, Mars would in time transfer its global

nonchocolate confectionery sugar brands to Wrigley. Bill Wrigley Jr., who controls 37

percent of the firm’s outstanding shares, remained the executive chairman of Wrigley.

The Wrigley management team also remained in place after closing.

The combined companies would have substantial brand recognition and product

diversity in six growth categories: chocolate, nonchocolate confectionary, gum, food,

drinks, and pet care products. While there is little product overlap between the two

firms, there is considerable geographic overlap. Mars is located in 100 countries, while

Wrigley relies heavily on independent distributors in its growing international

distribution network. Furthermore, the two firms have extensive sales forces, often

covering the same set of customers.

While mergers among competitors are not unusual, the deal’s highly leveraged financial

structure is atypical of transactions of this type. Almost 90 percent of the purchase price

would be financed through borrowed funds, with the remainder financed largely by a

third-party equity investor. Mars’s upfront costs would consist of paying for closing

costs from its cash balances in excess of its operating needs. The debt financing for the

transaction would consist of $11 billion and $5.5 billion provided by J.P. Morgan Chase

and Goldman Sachs, respectively. An additional $4.4 billion in subordinated debt would

come from Warren Buffet’s investment company, Berkshire Hathaway, a nontraditional

source of high-yield financing. Historically, such financing would have been provided

by investment banks or hedge funds and subsequently repackaged into securities and

sold to long-term investors, such as pension funds, insurance companies, and foreign

investors. However, the meltdown in the global credit markets in 2008 forced

investment banks and hedge funds to withdraw from the high-yield market in an effort

to strengthen their balance sheets. Berkshire Hathaway completed the financing of the

purchase price by providing $2.1 billion in equity financing for a 1 percent ownership

stake in Wrigley.

Discussion Questions:

1) Why was market share in the confectionery business an important factor in Mars’

decision to acquire Wrigley?

2) It what way did the acquisition of Wrigley’s represent a strategic blow to Cadbury?

3) How might the additional product and geographic diversity achieved by combining

Mars and Wrigley benefit the combined firms?

4) Speculate as to the potential sources of synergy associated with the deal. Based on

this speculation what additional information would you want to know in order to

determine the potential value of this synergy?

5) Given the terms of the agreement, Wrigley shareholders would own what percent of

the combined companies? Explain your answer

Answer:

Oracle Attempts to Takeover PeopleSoft

PeopleSoft, a maker of human resource and database software, announced on February

9, 2004 that an increased bid by Oracle, a maker of database software, of $26 per share

made directly to the shareholders was inadequate. PeopleSoft’s board and management

rejected the bid even though it represented a 33% increase over Oracle’s previous offer

of $19.50 per share. The PeopleSoft board urged its shareholders to reject the bid in a

mailing of its own to its shareholders. If successful, the takeover would be valued at

$9.4 billion. After an initial jump to $23.72 a share, PeopleSoft shares had eased to

$22.70 a share, well below Oracle’s sweetened offer.

The rejection prolonged a highly contentious and public eight-month takeover battle

that has pitted the two firms against each other. PeopleSoft was quick to rebuke publicly

Oracle’s original written offer made behind the scenes to PeopleSoft’s management that

included a requirement that PeopleSoft respond immediately. At about the same time,

Oracle filed its intentions with respect to PeopleSoft with the SEC when its ownership